Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

If you haven’t already, check out Episode 5 of the Prometheus Podcast! For this episode, we have another exceptional guest for you- Bob Elliott. Bob is the Co-Founder and CEO of Unlimited- a company that uses machine learning to replicate hedge fund strategies in a low-cost ETF format. Before starting Unlimited, Bob spent over a decade at Bridgewater Associates, one of the largest and most successful macro hedge funds, and was integral to building their systematic process. Bob brings a rich mixture of economic analysis, portfolio construction, and systematic thinking to this episode, which is not to be missed! Aahan & Bob cover almost every aspect of macro in their discussion and provide a rigorous framework for thinking about the current environment. If Alpha was ever available on a podcast, it’s this one!

Now, let’s dive into our observations. Summarily:

-

Our systems tell us that CPI will likely surprise expectations to the upside.

-

Our estimates for future real GDP growth remain bleak.

-

Markets continue to price stagflationary nominal growth & tightening liquidity conditions. Shorting asset remains a preferred orientation; we show our short-only candidates.

Conditions continue to push us towards stagflation amidst one of the sharpest monetary tightening in history. We discuss all these points below:

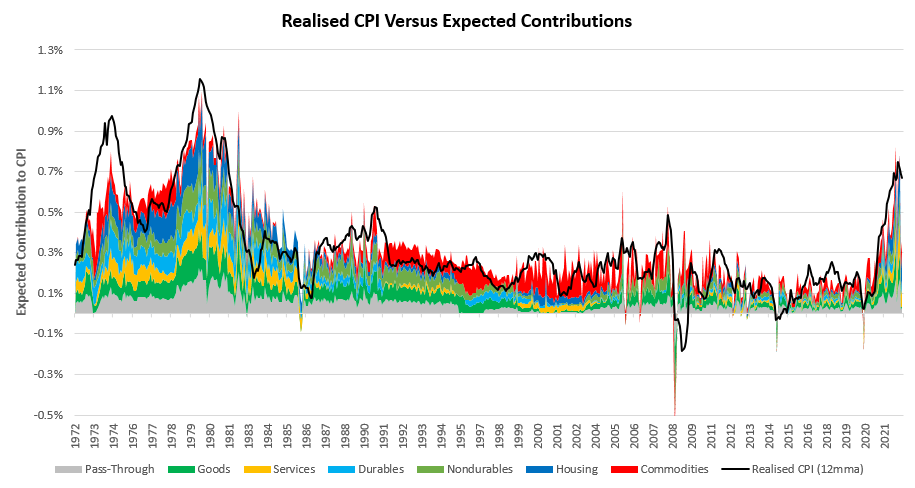

i. CPI is likely to surprise expectations to the upside, but we don’t see this as a significant opportunity. Our systems estimate that CPI will increase 0.36% versus the prior month, while consensus expects a 0.2% increase. The primary driver of our forecast is Housing inflation, with a contribution of 0.15%. Based on the historical performance of our forecasts, our systems estimate a 71.84% probability of a surprise. We show our historical estimates versus realized CPI below (we smooth realized CPI for a better visual representation):

Additionally, we show the fit of our estimates versus realized future inflation:

As we can see, our estimates have generally been good predictors of monthly changes in CPI. However, unlike the last CPI print, we don’t see this print as a large opportunity (despite a 72% chance of a surprise). The reason we believe so is that there is a significant amount of stagflationary pressure built into markets, and the surprise required to generate a large move is quite large. This dynamic contrasts significantly with the setup going into the last CPI print, where consensus estimates expected deflation. Therefore, while we expect a surprise, we think the reward for the risk of betting on a surprise isn’t large relative to the last print. Nonetheless, we enter the print shorting equities & long the dollar.

ii. Real GDP Growth is weak, & likely to get weaker. Our latest Real GDP Nowcast places economic growth at 0.8% versus one year ago. Our latest estimates of future growth show real GDP moving into negative territory over the next six months:

As we can see above, our estimates have generally done a good job of flagging large cyclical slowdowns in real GDP ahead of time. For a more detailed understanding of the factors driving these estimates, check out our latest Month In Macro note:

The outlook presents an environment that doesn’t favor equities or credit.Prematurely deploying risk can result in significant drawdowns, and economic conditions simply do not make a case for increasing long exposure to pro-cyclical assets.

iii. The current environment continues to favor short positions over long positions. Below, we show our estimates of today’s expected return environment (above cash):

As we can see, the environment is skewed towards shorting. Recent history has convinced investors that passive long-only investing can generate returns over active performance this is one of the key drivers of underperformance today. Below, we show how adding a short-only strategy, in the form of our Prometheus Short-Only Strategy, can add immense value during downturns like today:

Above, we show the performance of equities, our short-only strategy, and the combination of the two. The short-only strategy may not seem like much by itself, but when added to a long-only equity portfolio, it massively improves performance and reduces drawdowns. Given that this is a time for opportunistic shorting, we show the current menu of options for shorting today:

We show the prospective sizing of these positions as well:

Recall, that shorting is a highly active endeavor and while these positions reflect the potential shorts we think will do well in this environment, they need further timing signals to catalyze positions. If these strategies would be of interest, let us know in the comments below. For those unable to short/efficiently short assets, we continue to think that higher cash levels will generate outperformance in this environment. Stay nimble.

most powerful legal steroid

Others have instructed that anabolic steroid use could suppress the increases

usually shown in myocardial capillary density following prolonged endurance training (Tagarakis et al., 2000).

In addition, the exercise stimulus employed (prolonged endurance training) isn’t the first mode of train regularly utilized by anabolic steroid customers.

This is identified as concentric hypertrophy and doesn’t

occur on the expense of left ventricular diameter. In common, cardiac hypertrophy (resulting from a strain overload, i.e.

hypertension) will not be accompanied by a proportional improve in capillary

density (Tomanek, 1986). Therefore, the potential for

a discount in coronary vasculature density exists for the resistance- skilled athlete.

Nonetheless, it doesn’t seem to pose a significant cardiac threat

for these athletes.

The unique vulnerabilities of older adults to steroid unwanted effects underscore the necessity for individualized

therapy plans. Careful consideration of age-related modifications, current well being

conditions, and current drugs may help maximize the benefits of steroid remedy while

minimizing the side effects of medicine in seniors.

Aged sufferers could additionally be more delicate to the

effects of steroids, both helpful and opposed. This increased sensitivity can lead to extra pronounced therapeutic outcomes, however it also raises the risk of unwanted effects.

Nonetheless, others argue that tren’s antagonistic effects are exaggerated and never notably worse than those of different anabolics.

If you or someone you understand is struggling with steroid use,

there are resources out there. Medical professionals can help handle withdrawal symptoms and provide steering on how

to safely stop utilizing steroids. Counseling also can help address the mental challenges that come with stopping steroid use.

Getting sufficient sleep and allowing time for

muscle groups to get well is crucial for protected and effective muscle growth.

They cause the kidneys to work harder, which may lead to kidney failure in extreme circumstances.

Steroid use can also lead to dehydration, which

further will increase the chance of kidney problems.

Although urine testing can detect latest AAS use, individuals who’ve

used AAS months or years earlier can’t be identified and excluded – and the inclusion of such individuals will

result in an underestimate of impact sizes.

Tren can additionally be nonetheless obtainable in pellet type and can be purchased from a feed provide retailer

and transformed to injectable Tren very simply with a simple package.

When bought on this kind it’s not a managed substance as this may harm the livestock market,

but it’s something many supply stores maintain a watchful eye on. Further,

many pellets now comprise added estrogen, which is one

thing you don’t want.

Trenbolone and Deca-Durabolin are both injectable bulking steroids, yet they are unique of their pharmacology and

effects. Research have found Equipoise to be extra

estrogenic than Deca-Durabolin, with Equipoise displaying 50% fewer estrogenic results than testosterone but

400% greater than Deca-Durabolin. Studies point out that

Deca-Durabolin is mostly well-tolerated by ladies when taken in dosages of one hundred mg (6), administered every

different week for 12 weeks. Though Deca-Durabolin is

most likely not probably the most optimal steroid for women, with Anavar being a extra suitable compound, analysis

suggests Deca-Durabolin presents a low risk of virilization.

We find that this before-and-after transformation is typical of someone stacking

Deca-Durabolin with another bulking steroid.

Stretch marks may be seen on his proper deltoid within the

after picture, indicating the fast anabolic effects

of Anadrol and Deca.

Furthermore, this publicity disrupts the secretion of reproductive hormones in females,

leading to altered ovulation patterns and impaired

follicular development (Padmanabhan and Veiga-Lopez, 2014).

They may trigger a brief lived rise in blood pressure and a rise in LDL (“bad”) cholesterol levels

while HDL (“good”) cholesterol levels lower.

This can place folks at an elevated threat of coronary artery illness and a life threatening irregular heart price.

Anavar, classified as an androgenic anabolic steroid, is banned by most sports activities

organizations as a end result of its performance-enhancing effects.

Athletes who take a look at constructive for Anavar can face

severe penalties, including suspension or lifetime bans from competition. This can have vital

implications for an athlete’s profession and future opportunities.

The use of anabolic androgenic steroids, together

with Anavar, just isn’t with out legal and moral implications.

Hair loss, while it could also probably have an result on female customers, is primarily a

concern for men who use steroids. These genetically predisposed

to male pattern baldness can see this growing prematurely as a

outcome of increased DHT. While not a health problem,

hair loss could be distressing for young steroid customers.

One frequent technique to take care of this is to incorporate a fast-acting steroid at the start of

the cycle (usually an oral steroid), which acts as the first anabolic agent, while your slower steroids take time to kick in. But a more advanced and probably

much more efficient approach is to do frontloading.

The primary goal of frontloading is to get your blood

ranges of a steroid as much as an optimum stage as quick as attainable.

This, after all, enables you to benefit from quicker efficiency

results and features.

These hormones include aldosterone, which helps regulate sodium concentration within the body, and cortisol,

which performs many roles in the physique, together with serving as part

of the physique’s stress response system to lower inflammation. The nature of erectile dysfunction can be categorised as psychogenic, natural or mixed

psychogenic and organic (193). As A Outcome Of of the intimate function of testosterone in erectile function, erectile

dysfunction can develop as a post-cycle aspect effect

of AAS use. Nevertheless, it must be saved

in thoughts that erectile dysfunction in an AAS person is not essentially the outcome

of AAS use per se and could be a symptom of an underlying psychiatric disorder.

The presence of rigid morning or night time erections, sudden onset, intermittent course and

brief length are a great indication of a psychogenic cause.

In the next sections, we’ll delve into the potential unwanted effects of Anavar

in females. Androgens play a job in the growth and upkeep of male sex characteristics, such as facial and physique hair growth, muscle mass, and

a deep voice. In ladies, androgens like trenbolone

can cause virilization, a condition characterised by masculine traits

developing. Anabolic steroids also can trigger gynecomastia by growing ranges of estrogen within the body.

Estrogen is the female intercourse hormone,

and it could promote the expansion of breast tissue.

Injectable Dianabol is considerably less hepatotoxic in our testing, as liver enzymes won’t rise as a lot; thus, the risk of liver harm is

considerably decreased. This is due to the injection enabling Dianabol to

enter the bloodstream immediately as an alternative of having

to bypass the liver. Upon its launch in 1958, Dr. Ziegler recommended an original dosage of 5–15 mg per day.