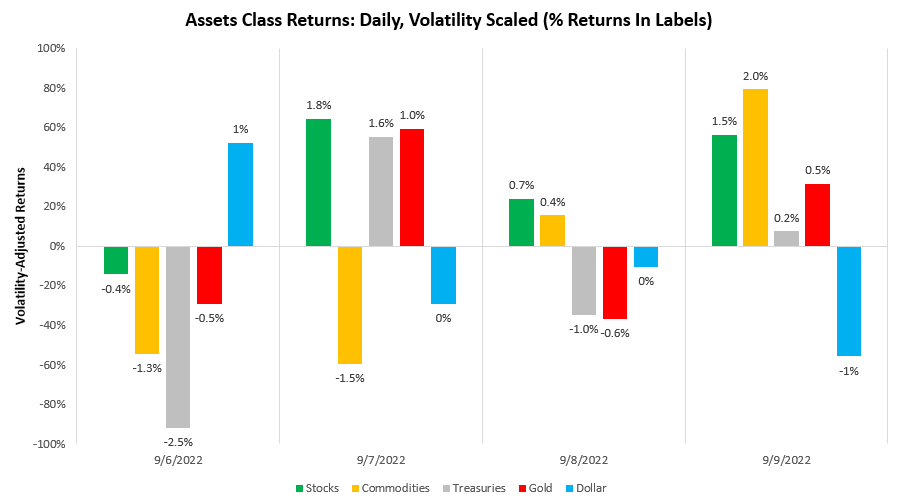

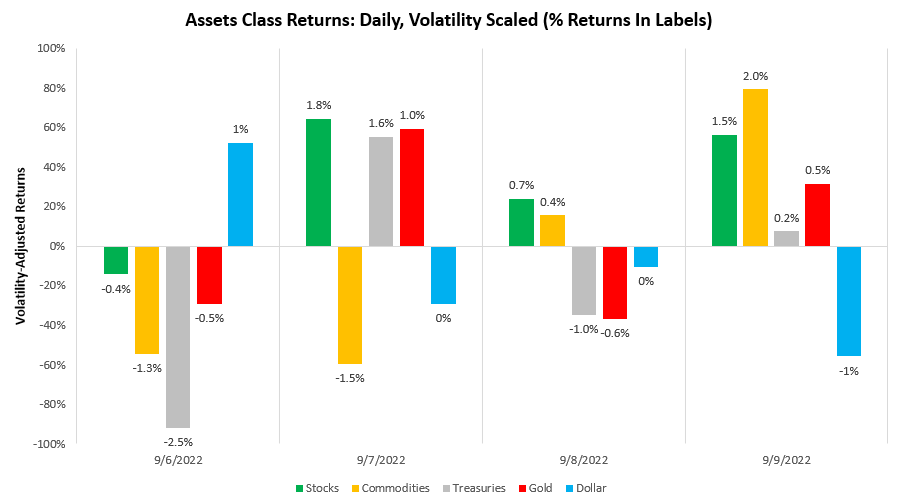

Last week, equities rallied while commodities and treasuries showed mixed performance. The dollar suffered losses through the week after an initial strong start. We offer the evolution of asset prices over the last week below:

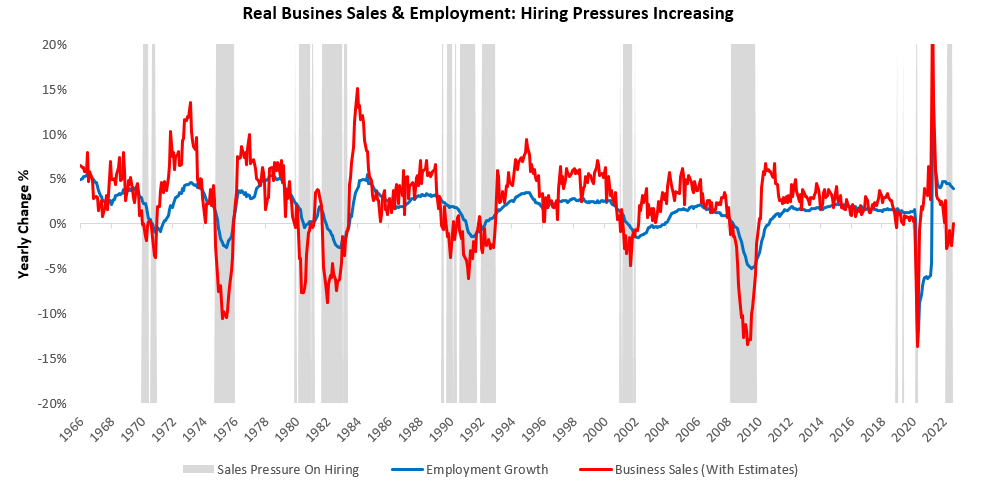

These moves came alongside economic data that continue to signal pressures building on businesses as we move into the late stages of the current business cycle. ISM PMI data surprised consensus expectations, labor market data came in better than expected, but business sales data missed expectations considerably. These data points and our broader tracking of economic conditions tell us that US businesses remain under pressure. Today’s stagflationary dynamics create a challenging environment for businesses, as every dollar invested in capital or labor for future production yields less output. This comes alongside a declining demand for real goods & services. Combining these two factors, it is highly likely that deteriorating real economic activity will eventually find its way into business hiring. We offer data reprensatitive of these pressures below in the form of real business sales and employment:

Businesses hire and fire employees pro-cyclcially, i.e., when sales and profits are increasing and need to increase output, they hire more workers and invest to increase production. Conversely, when sales deteriorate and do not need as much labor and layoff workers. Today, we are seeing a significant deterioration in sales, which have contracted 3.5% versus the prior year. Since 1966, there have been eight periods that resemble today in terms of the decline in real sales relative to employmentand all of them have resolved themselves in a contraction in labor markets.

Therefore, we continue to think that the imbalance between production and nominal spending will be resolved through lower nominal spending, with real spending likely to move into contractionary territory. We will receive essential data in assessing this outlook next week; we show the upcoming data relevant to our systematic tracking of economic conditions:

-

Monday:

-

Tuesday: CPI, Real Hourly Earnings, Budget Statement, NFIB Small Business Optimism

-

Wednesday: PPI

-

Thursday: Initial Jobless Claims, Empire Manufacturing, Retail Sales, Import-Export Prices, Industrial Production & Capacity Utilization, Empire Manufacturing

-

Friday: University Of Michigan Surveys

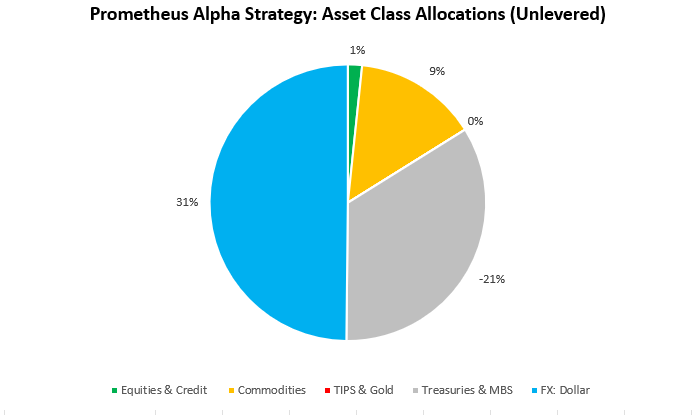

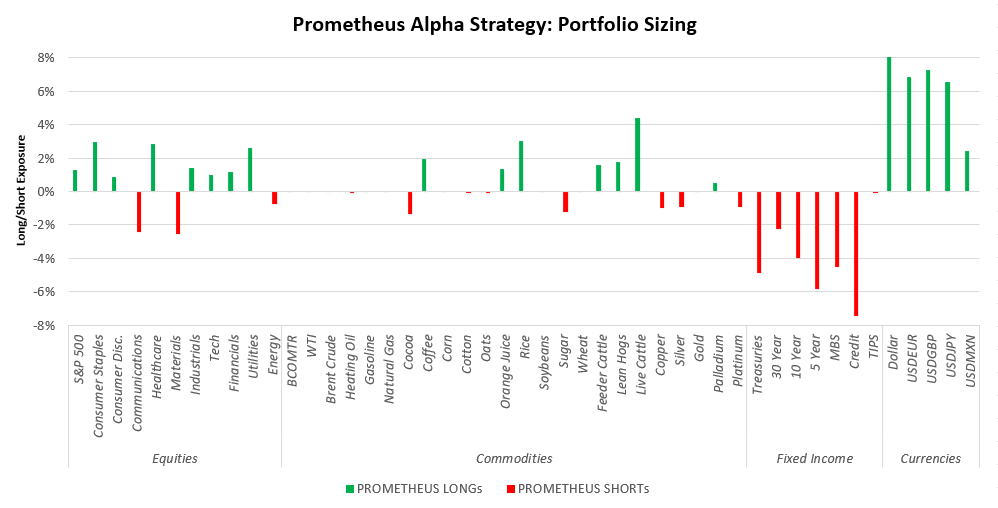

Next week will bring a significant amount of information on the inflation outlook, with PPI, CPI, & Import-Export prices all offering incremental insight. Furthermore, we will receive information on both the state of businesses through Industrial Production and PMIs. Finally, we will get more insight into the consumer from hourly wages, retail sales, and Michigan surveys. For our part, we will be focused on inflation data as it is the most significant risk to our current positioning. We show our systematic portfolio allocations at the asset class level for next week below:

We drill down to the security level below:

As we can see above, we maintain short exposure to treasuries & long exposures to the dollar as our primary risk next week. Resultantly, here are the top observations coming from our systematic process that stand out to us heading into next week:

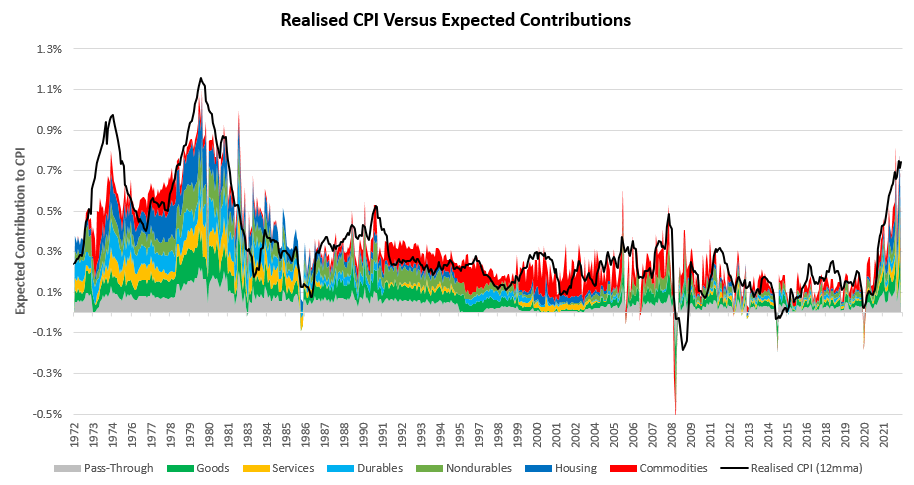

i. Consensus expects deflation in headline CPI, while we expect it to rise. Our systems estimate that CPI will increase 0.29% versus the prior month, while consensus expects a -0.1% increase. The primary driver of our forecast is commodity inflation, with a contribution of 0.08%. We show the history of our estimates versus realized CPI (smoothed) below:

While our positioning is not based on point estimates of CPI, we think this print offers an asymmetric opportunity to our Treasury shorts. If CPI comes in in positive territory, Treasuries are likely to sell off as they price in a tighter path for the Fed. Conversely, the bar to beating consensus CPI to the downside is high. Consecutive months of negative CPI are a rarity, occurring less than 3.5% of the time since 1965. Finally, estimates for core CPI remain positive, telling us that consensus broadly estimate the drop will come from food & energy prices. Our examination of commodity prices does not match up with these estimates. Overall, we think there is a significant chance of a surprise and will observe how the data evolve.

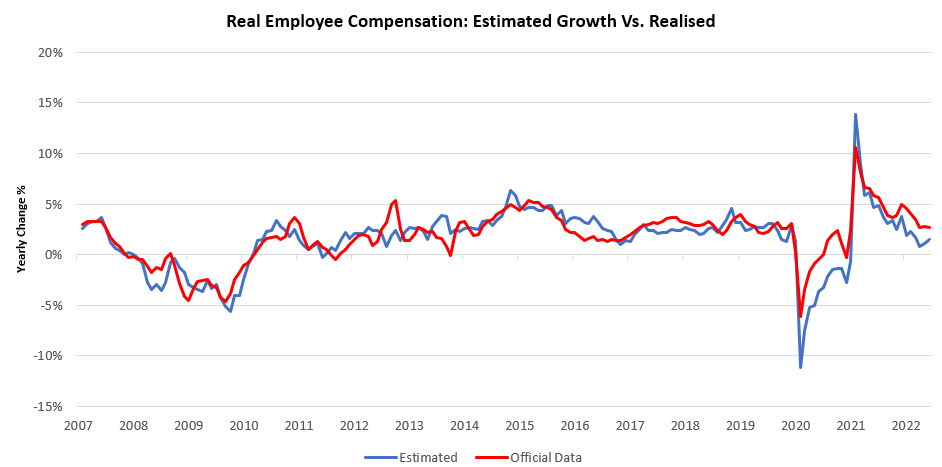

ii. Real wage data will offer us significant information on total spending in the economy. Spending in the economy is primarily driven by labor force spending, i.e., employee incomes. Employee incomes are a product of wages, hours worked, and total employment. Currently, incomes are supported by a robust labor market, which remains at multi-generational levels of tightness. However, real wages and hours are not as supportive of employee incomes. If we see further weakening in real wages this week, it will indicate that there is a high probability of a labor market slowdown ahead of us. Below, we show our current estimates of real employee compensation versus the official data:

The evolution of these drivers of real spending will be critical to the outlook.

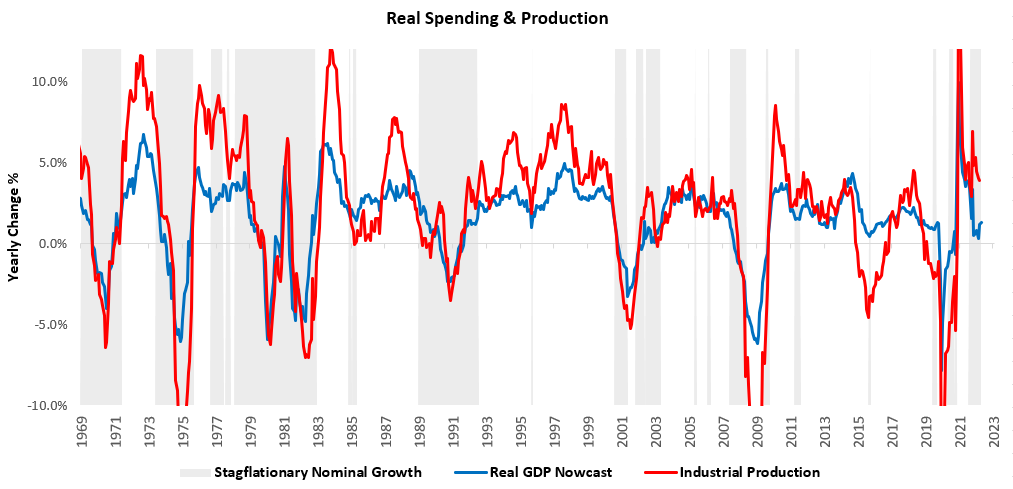

iii. We will be looking to see if industrial production moderates to conform to real spending. Currently, industrial production is elevated relative to the amount of real spending in the economy. We will be watching the industrial production data to understand better if lower real incomes and business spending have passed through the supply chain to lower production. We show industrial production relative to our GDP Nowcast below:

Much like labor markets, there are physical limitations on how much production can increase. With capacity utilization near 2018 highs, we judge that the room for improvement here is fast receding.

Overall, our systematic tracking of conditions continues to tell us that we are in a period of stagflationary nominal growth and tightening liquidity. This period is unlike any period we have seen over the last 40 years, and managing risk through this period will be imperative to long-term performance. Stay nimble.

Stellar service in every department.

where to buy lisinopril price

Their staff is always eager to help and assist.

The free blood pressure check is a nice touch.

get cheap cipro without rx

They never compromise on quality.

They keep a broad spectrum of rare medications.

can i get generic cytotec tablets

Providing international caliber services consistently.

Their pet medication section is comprehensive.

where to get cheap cipro price

Love the seasonal health tips they offer.

Everything what you want to know about pills.

how to buy cytotec online

They consistently exceed global healthcare expectations.