Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

If you haven’t already, check out Episode 5 of the Prometheus Podcast! For this episode, we have another exceptional guest for you- Bob Elliott. Bob is the Co-Founder and CEO of Unlimited- a company that uses machine learning to replicate hedge fund strategies in a low-cost ETF format. Before starting Unlimited, Bob spent over a decade at Bridgewater Associates, one of the largest and most successful macro hedge funds, and was integral to building their systematic process. Bob brings a rich mixture of economic analysis, portfolio construction, and systematic thinking to this episode, which is not to be missed! Aahan & Bob cover almost every aspect of macro in their discussion and provide a rigorous framework for thinking about the current environment. If Alpha was ever available on a podcast, it’s this one!

Now, let’s dive into our observations. Summarily:

-

The latest inflation data has shown significant evidence of inflation entrenchment, i.e., inflationary pressures are likely to be persistent.

-

Real income data continues to deteriorate, but labor markets remain extremely tight.

-

The combination of entrenched inflation, weakening real incomes, & tight labor markets will push the Fed to tighten monetary policy more than discounted.

The odds for incrementally more tightening continue to rise, and markets have moved to price out some of this move for future tightening. However, there remains potential for more to come. We discuss these views below:

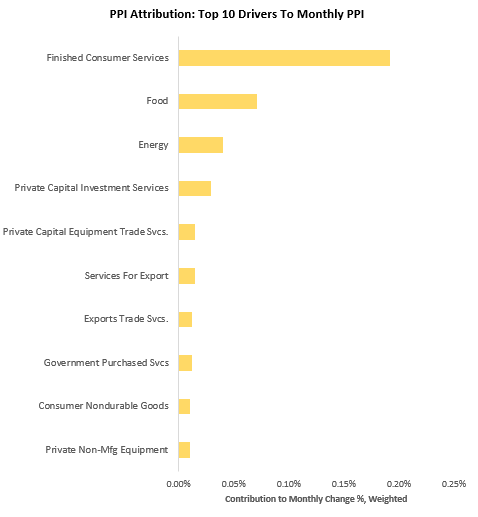

i. Inflation has shown signs of entrenchment. It is often said that once inflation takes off, it is hard to tame. The most recent PPI & CPI data lend credence to this notion in today’s context. PPI data came out higher than expected and showed significant contributions coming from consumer services. we show the biggest contributors to the print below:

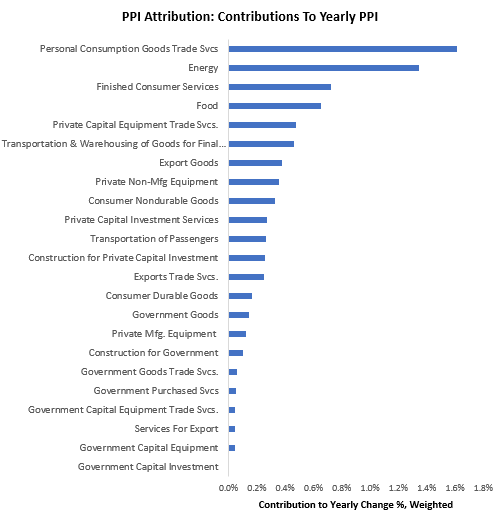

Furthermore, this outsized contribution of consumer services is not a one-off event; consumer-facing prices are now one of the largest drivers of PPI versus one year ago:

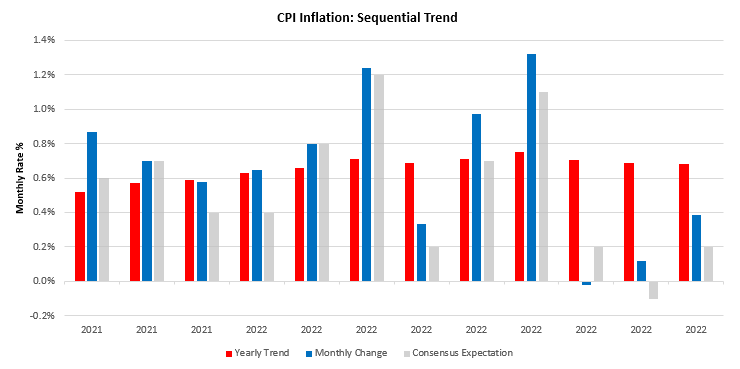

These signs of strong services inflation came ahead of CPI, which also came in higher than expected. CPI Inflation increased by 0.39% in September, surprising consensus expectations of 0.2%. This print contributed to a sequential deceleration in the quarterly trend relative to the yearly trend. Below, we show the monthly evolution of the data relative to its 12-monthly trend and consensus expectations:

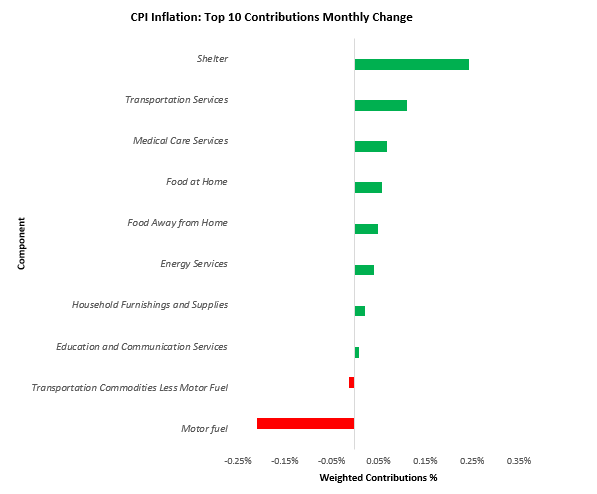

The primary driver of this report was a large rise in shelter inflation. We show the top 10 contributors to the CPI print below:

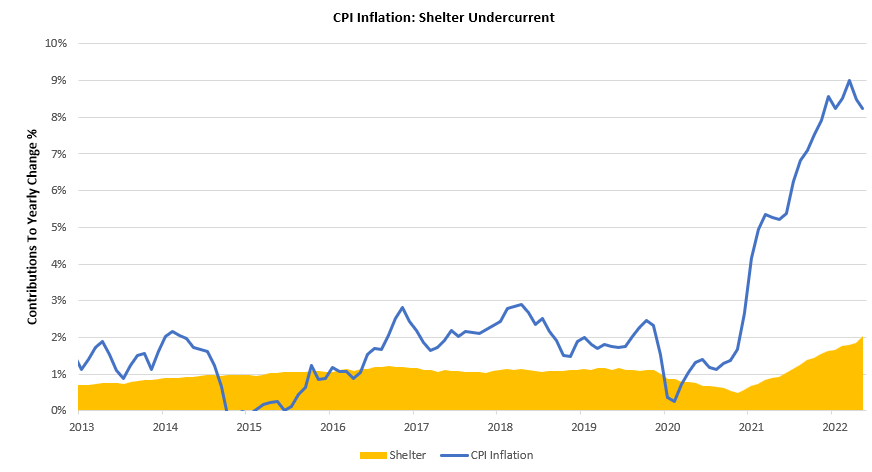

We find the shelter component of CPI to be of particular note. At the current pace of shelter inflation, shelter costs alone will keep both headline and core CPI above the Feds’ 2% inflation target. Furthermore, our expectation is for this component to rise even further. Shelter continues to form a significant undercurrent supporting inflationary pressures. We visualize this below:

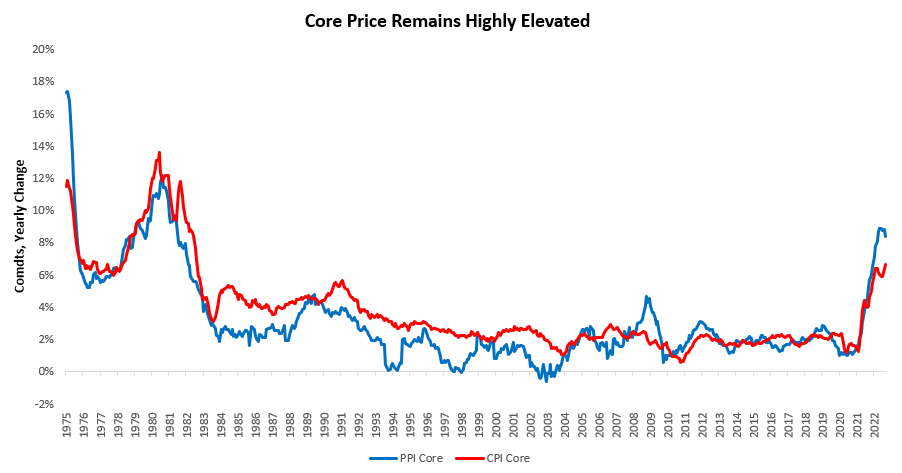

Additionally, other core components of CPI & PPI continue to show stabilization at high levels, largely coming from wage pressures. Below, we show how core PPI & CPI remain elevated:

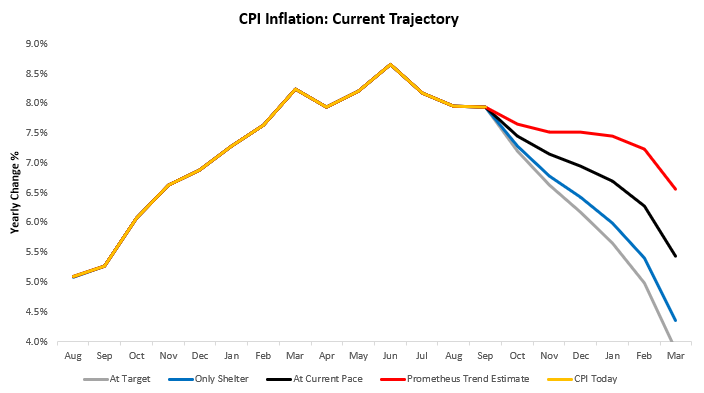

When we add together the undercurrent from shelter inflation & likely persistence of wage inflation, the outlook for CPI remains one where we are highly unlikely to return to the Fed’s 2% objective anytime soon. To get a sense of the trajectory of future CPI, we offer the following scenarios below:

Above, we show the future path for CPI based on various scenarios in red is CPI continuing at our estimate of the annualized trend, in black is the if we continue the pace set by the most recent print, in blue is the path if we only realize shelter CPI at the current rate (i.e., all other inflation is 0), & finally, in grey, we show CPI if the Fed brings every monthly print over the next 6 months in line with its 2% objective. What is crucial to note is that even if the Fed can bring us back to 2% inflation, we will still end this year with 6.3% inflation. Furthermore, it is highly unlikely that the Fed can do so. While the Fed may discount year-over-year numbers to a certain extent due to commodity price shocks, we think it would be dangerous for them to begin to ease conditions before the year-over-year numbers are back to target lest they make the same mistakes as were made in the 1970s of celebrating too early. More on this in the future.

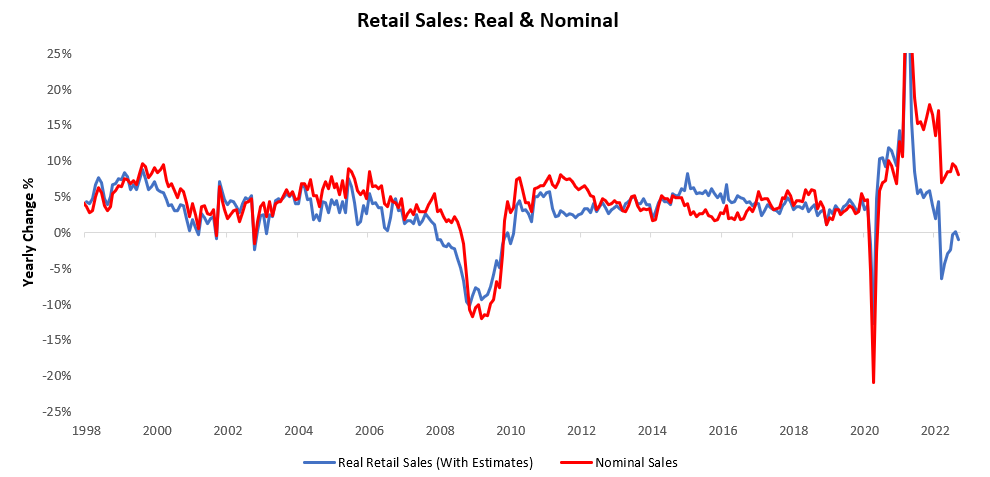

ii. Nominal activity stays elevated, but real spending continues to decline. Retail Sales increased by 0% in September, disappointing consensus expectations of 0.2%. This print contributed to a sequential deceleration in the quarterly trend relative to the yearly trend. While nominal retail sales contracted by 0%, real retail sales contracted by -0.5% this month, resulting in a yearly change in real retail sales of -1% versus the prior year. We show nominal vs. real retail sales below:

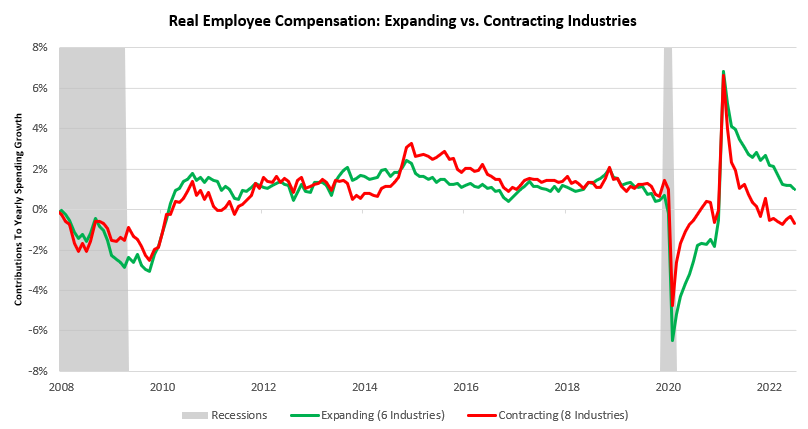

This decline in real spending is of no surprise, as we have recently seen a widening of our tracking of real employee compensation, which is the largest component of income in the economy. Below, we show employee compensation after dividing the aggregate data into two groups those with rising incomes and those with falling incomes over the last year:

There are now more industries with falling real incomes than those with rising ones. This creates immense pressure on real demand, which is likely to find its way into real output. Conditions continue to push us marginally toward outright stagflation.

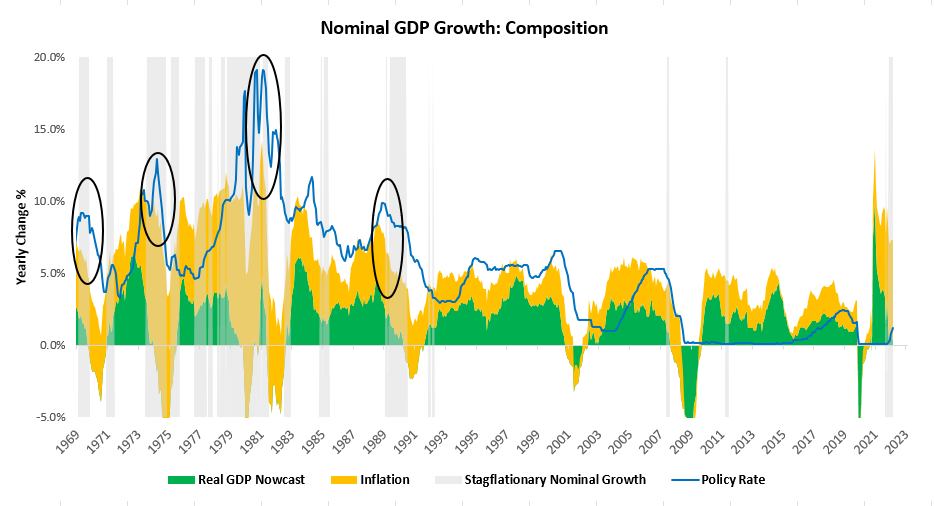

iii. Heightened nominal demand and entrenched inflation are likely to push the Fed to tighten conditions even more than expected. Below, we show how during past periods of stagflationary nominal growth (highlighted in grey), policy rates need to be in excess of nominal growth to break the inflationary spiral (instances circled):

During these tightening cycles, policy rates needed to rise until they exceeded nominal growth by approximately 3-4%. In today’s context, if we use a wide range around our estimates of future nominal growth this would imply a peak Fed Funds Rate between 5.9% (best case) and 8.4% (worst case). What we think is important is to note that there is a significant range of these outcomes however, all of them sit above current market pricing of peak policy rates of 5%. Therefore, the current path for monetary policy will likely continue to drag on both stocks & bonds at the same time.

We continue to think that the hierarchy investors must abide by today is as follows:

-

Capital preservation remains of paramount importance. High cash positions are not an opportunity cost but rather opportunities for future returns being long assets.

-

True diversification across asset classes is required. The financial system is not built for continuous periods of tightening liquidity as conditions unfold, cash will once again flow to assets, the distribution of which will depend on the environment.

-

Active management remains essential for outperformance. Those with the ability to effectively short assets are likely to generate outsized returns relative to traditional benchmarks.

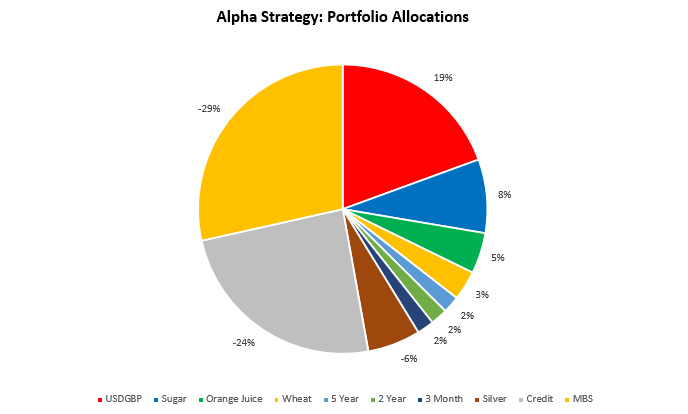

Our systems continue to serve us well toward these ends. This week was a strong one for our short in real estate equities, alongside long USDJPY positions. Heading into next week, our systems have found opportunities in shorting credit (IG), MBS, & GBPUSD, along with long positions in select commodities:

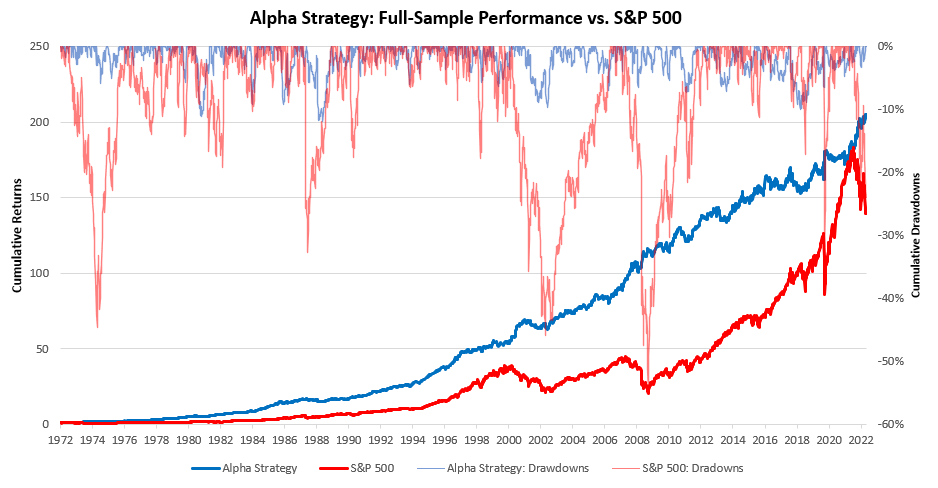

For those who have been following our Alpha Strategy closely, you will recognize that these positions are far more concentrated than our previous iterations and are a function of serval upgrades performed on the strategy. The upgrades have added further protection & timeliness to our strategies. We continue to think that our strategies remain well-suited to navigate today’s challenging. We show the full-sample backtest returns on our upgraded Alpha Strategy below:

Stay nimble.