Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of both the economy and financial markets in real-time. Here are the top developments that stand out to us:

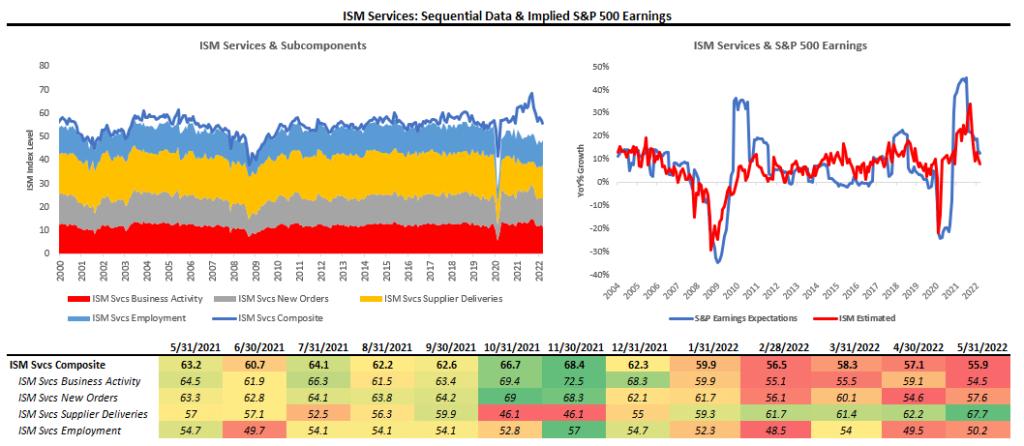

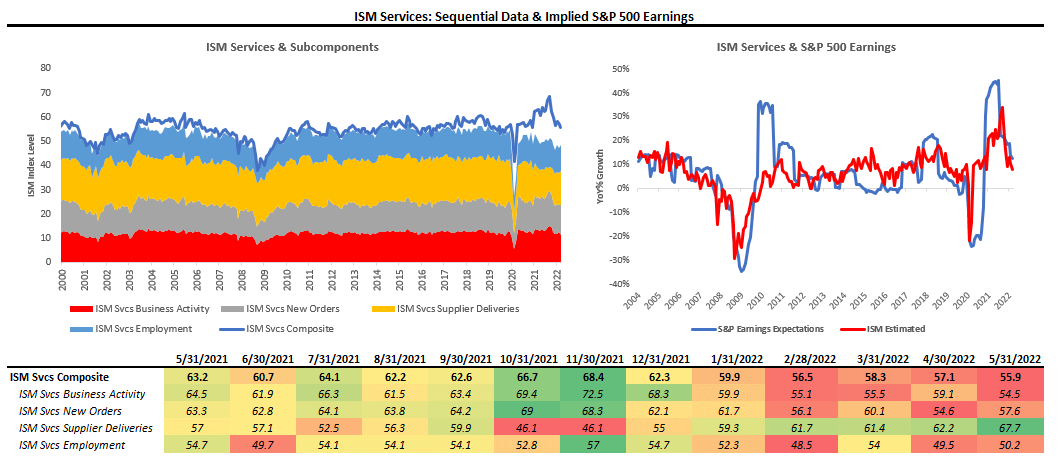

i. ISM Services came in lower but outperformed expectations. The latest ISM Services data showed an expansionary reading of 55.9, implying 8% YoY earnings for the S&P 500. This reading was a sequential deceleration within a decelerating trend. The largest gaining segment was Deliveries, and the most significant slowdown was in Business Activity.

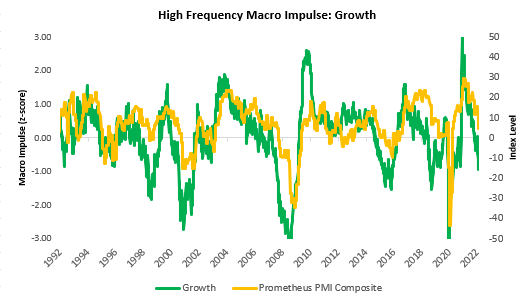

ii. Individual data may bounce or strengthen, but the broad trend in economic data is lower. In particular, ISM data this week surprised expectations significantly, alongside a robust labor market. However, our proprietary High-Frequency Gauges tell us that the trend in economic growth is likely to head lower. Furthermore, when we look at our broad PMI composite, which includes all the major PMI surveys, we see weakness is already present in the form of a downtrend:

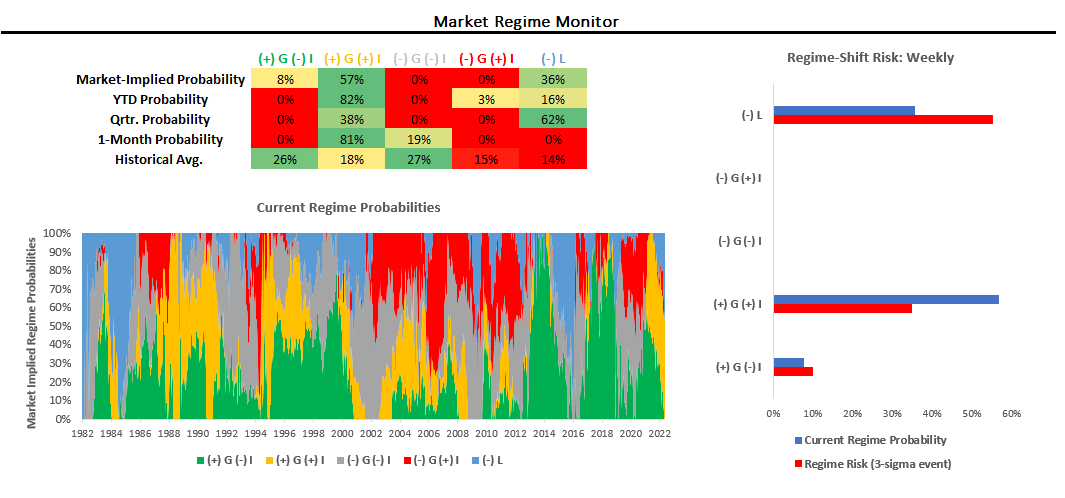

iii. Our systems signal heightened nominal growth with a stagflationary tilt. We continue to have the conviction that this is the number one risk to manage in markets today. We show our market regime monitor below:

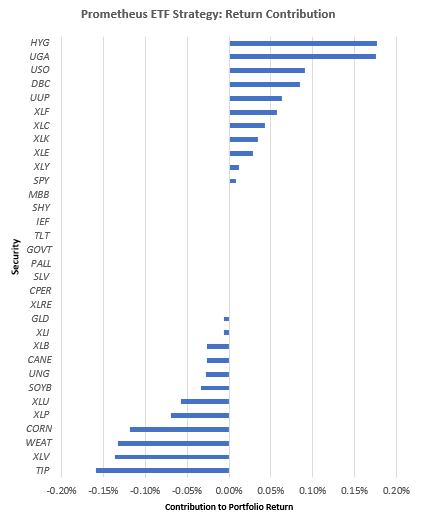

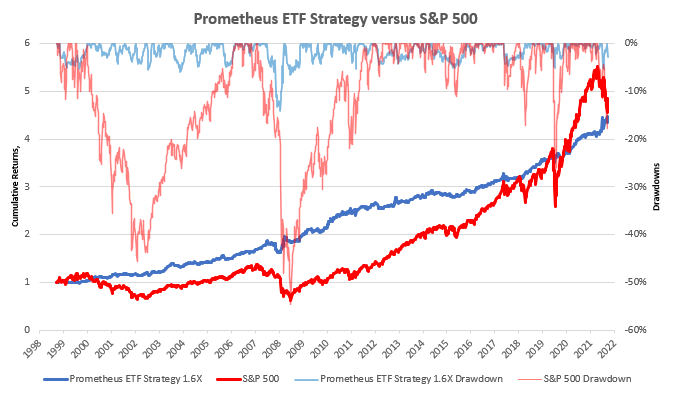

Over the last month, markets have primarily priced rising nominal growth. Regime Risk is currently elevated, with the potential for a shift to (-) L. We continue to have a dynamic of heightened risk and volatility. Within this context, our ETF Strategy was able to end this week roughly flat, despite significant volatility in equity markets. The performers in the portfolio were high yield shorts (HYG) & natural gas longs (UGA). The drags on the portfolio were silver & TIPS long positions. We show the attribution below:

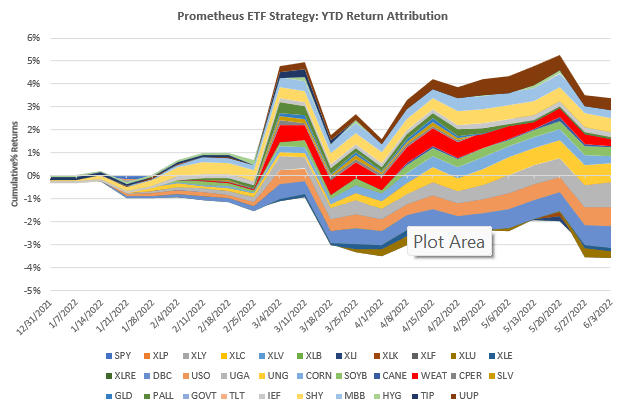

We show the YTD cumulative return for the ETF Strategy as well:

Our systems continue to tell us that inflation is persistent while growth continues to trend lower. Liquidity conditions have tightened and are likely to get worse. Our systems aggregate our analysis in an algorithmic, rules-based fashion to create portfolios with attractive risk-reward ratios. For next week, here are how our systems are looking to be positioned based on both fundamental and market data:

- Stocks: SPY (-5%), XLP (5%), XLY (-3%), XLC (-5%), XLV (5%), XLB (5%), XLI (-5%), XLK (-4%), XLF (-4%), XLU (5%), XLE (3%)

- Commodities: DBC (3%), USO (2%), UGA (2%), UNG (2%), CORN(3%), SOYB(4%), CANE(4%), WEAT(2%), GLD (6%)

- Fixed Income: HYG (-10%), TIP (13%)

- Dollar: UUP (12%)

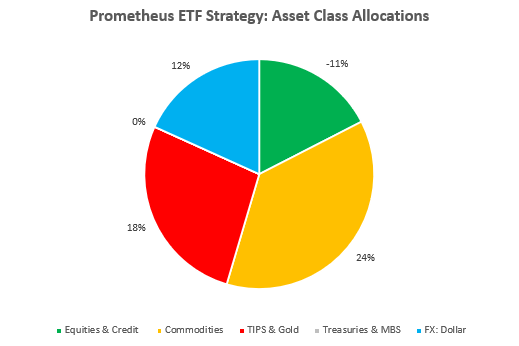

At the asset class level, our signals net out to an exposure that remains short equities & credit:

This allocation has a probability-weighted loss of -3.1% and a max loss of -6.7% in a three-sigma event. Volatility continues to rise across asset classes, consistent with what we have seen during previous periods of Quantitative Tightening.

Read our note on the path for Quantitative Tightening by clicking here.

With inflation persistent, the growth impulse weakening, liquidity tightening, & volatility rising, capital preservation plus active shorting remains the key to success. We continue to think our systems are well prepared for such an environment as they have been in the past:

Stay nimble!

Hey there! Do you know if they make any plugins to assist with Search Engine Optimization? I’m trying to get my website to rank

for some targeted keywords but I’m not seeing very good results.

If you know of any please share. Thank you! You

can read similar art here: Eco blankets

At the middle of this effort is the Neanderthal Genome Mission, a collaboration among the many U.S.

sugar defender official website Including Sugar

Protector right into my daily regimen total wellness. As somebody who focuses on healthy eating, I value

the extra security this supplement provides. Because starting

to take it, I’ve seen a marked improvement in my power levels

and a substantial decrease in my need for undesirable

snacks such a such a profound impact on my day-to-day live.

sugar defender ingredients

sugar defender reviews Uncovering Sugar Protector has been a game-changer for me, as

I’ve constantly been vigilant concerning handling my blood sugar degrees.

I currently feel empowered and confident in my ability to preserve healthy degrees,

and my most recent checkup have actually mirrored this development.

Having a reliable supplement to complement my a substantial resource of convenience, and I’m truly thankful for the significant distinction Sugar Protector has actually made in my total well-being.

sugar defender reviews

sugar defender official website As a person that’s always been cautious concerning my blood sugar level, finding Sugar Protector has been a

relief. I feel a lot a lot more in control, and my current

examinations have revealed positive renovations. Understanding I have a reputable

supplement to support my routine gives me comfort.

I’m so thankful for Sugar Defender’s effect on my health!

sugar defender

sugar defender Uncovering Sugar Protector has actually been a game-changer for me,

as I have actually constantly been vigilant about handling

my blood sugar levels. I currently feel equipped

and certain in my ability to preserve healthy and balanced levels, and my newest

checkup have shown this progression. Having a credible supplement to enhance my a significant source of convenience, and I’m absolutely appreciative for

the considerable distinction Sugar Protector has made in my overall health.

sugar defender

This blog was… how do you say it? Relevant!! Finally I have found something that helped me. Thanks!

I blog frequently and I truly appreciate your content. The article has truly peaked my interest. I’m going to book mark your blog and keep checking for new details about once a week. I opted in for your Feed too.

Next time I read a blog, Hopefully it won’t disappoint me just as much as this particular one. After all, I know it was my choice to read through, nonetheless I genuinely thought you would have something interesting to talk about. All I hear is a bunch of moaning about something that you could possibly fix if you were not too busy searching for attention.

I’m extremely pleased to find this website. I need to to thank you for your time for this particularly wonderful read!! I definitely loved every bit of it and i also have you saved as a favorite to check out new things on your web site.

The very next time I read a blog, I hope that it won’t disappoint me as much as this one. After all, I know it was my choice to read, but I truly thought you would probably have something useful to say. All I hear is a bunch of crying about something that you could possibly fix if you weren’t too busy seeking attention.

I could not refrain from commenting. Well written!

Having read this I thought it was very informative. I appreciate you finding the time and energy to put this content together. I once again find myself spending a significant amount of time both reading and posting comments. But so what, it was still worth it!

Spot on with this write-up, I honestly believe that this amazing site needs a lot more attention. I’ll probably be back again to read more, thanks for the advice.

Aw, this was an incredibly good post. Taking a few minutes and actual effort to generate a really good article… but what can I say… I hesitate a whole lot and never manage to get anything done.

Hi, I do think this is a great site. I stumbledupon it 😉 I may revisit once again since i have book marked it. Money and freedom is the greatest way to change, may you be rich and continue to help others.

Good information. Lucky me I recently found your blog by accident (stumbleupon). I’ve bookmarked it for later.

A motivating discussion is worth comment. I believe that you need to publish more about this subject, it might not be a taboo subject but generally people do not speak about these subjects. To the next! Kind regards.

I love it when people come together and share thoughts. Great site, stick with it.

You should be a part of a contest for one of the best websites on the internet. I’m going to highly recommend this website!

Great web site you have got here.. It’s difficult to find high-quality writing like yours these days. I honestly appreciate people like you! Take care!!

After I initially commented I appear to have clicked on the -Notify me when new comments are added- checkbox and now whenever a comment is added I get 4 emails with the same comment. There has to be an easy method you can remove me from that service? Thank you.

It’s always good to see it from a different perspective My experience confirms that. I have to think about it some more. Can you expand on this?

I’m amazed, I must say. Seldom do I encounter a blog that’s both equally educative and entertaining, and let me tell you, you’ve hit the nail on the head. The issue is something which too few men and women are speaking intelligently about. Now i’m very happy I came across this in my search for something regarding this.

Way cool! Some extremely valid points! I appreciate you writing this write-up plus the rest of the site is also very good.

I am impressed with this site, very I am a fan .

Thanks for the a new challenge you have exposed in your blog post. One thing I’d like to comment on is that FSBO relationships are built as time passes. By presenting yourself to owners the first weekend their FSBO will be announced, prior to masses get started calling on Monday, you develop a good interconnection. By sending them tools, educational elements, free records, and forms, you become the ally. By using a personal interest in them and their predicament, you generate a solid connection that, oftentimes, pays off if the owners decide to go with a realtor they know plus trust — preferably you.

I must thank you for the efforts you have put in penning this website. I’m hoping to view the same high-grade content by you later on as well. In fact, your creative writing abilities has encouraged me to get my very own site now 😉

I was able to find good information from your blog articles.

After study several of the content on the internet site now, and that i genuinely much like your method of blogging. I bookmarked it to my bookmark internet site list and you will be checking back soon. Pls consider my website too and tell me what you consider.

I used to be able to find good info from your content.

Very good information. Lucky me I came across your website by chance (stumbleupon). I have saved as a favorite for later!

Wow, I guess you do learn something new everyday, more people should stumble onto this! You need some good SEO work!

Exactly what I was looking for, regards for posting .

Wow, wonderful blog layout! How long have you been blogging for? you make blogging look easy. The overall look of your web site is fantastic, let alone the content!

I think this is among the most vital info for me. And i’m satisfied studying your article. However should commentary on few normal things, The website taste is ideal, the articles is in reality excellent . Excellent activity, cheers.

I was able to find good information from your blog posts.

i use google when i want to do some spanish translation, it is good for general spanish translation,,

Every once in a while I find something worth reading when I’m surfing the internet. Bravo… thanks for creating real content here…

I don’t even know how I ended up here, but I thought this post was great. I do not know who you are but certainly you are going to a famous blogger if you are not already Cheers!

There couple of intriguing points soon enough in the following paragraphs but I do not determine if I see them all center to heart. There is some validity but I am going to take hold opinion until I consider it further. Great post , thanks and we want more! Put into FeedBurner too

Though some sort of taxation repayment may well appear to be safe, it really is not.

Having read this I thought it was really enlightening. I appreciate you spending some time and effort to put this information together. I once again find myself personally spending a significant amount of time both reading and leaving comments. But so what, it was still worthwhile!

I do believe all of the ideas you’ve presented for your post. They are very convincing and can definitely work. Nonetheless, the posts are very quick for starters. May you please prolong them a little from subsequent time? Thanks for the post.

Hi there! I simply want to offer you a big thumbs up for the excellent information you’ve got here on this post. I’ll be coming back to your site for more soon.

grand central stations are really built with some great architectural design, they are very impressive.

This internet site may be a walk-through it really is the knowledge you desired concerning this and didn’t know who need to. Glimpse here, and you’ll definitely discover it.

Excellent article. I am dealing with some of these issues as well..

This web page is actually a walk-through for all of the internet it suited you concerning this and didn’t know who ought to. Glimpse here, and you’ll definitely discover it.

There are a few fascinating points at some point in this post but I do not determine if I see all of them center to heart. There is some validity but I most certainly will take hold opinion until I take a look at it further. Good write-up , thanks so we want much more! Added to FeedBurner also

Thanks for every other wonderful article. Where else may anybody get that kind of information in such a perfect method of writing? I have a presentation next week, and I’m at the look for such info.

I blog often and I really appreciate your information. The article has truly peaked my interest. I am going to bookmark your blog and keep checking for new information about once a week. I opted in for your Feed too.

I really love your blog.. Pleasant colors & theme. Did you develop this website yourself? Please reply back as I’m wanting to create my own site and would love to find out where you got this from or exactly what the theme is called. Thank you!

I like this web site very much, Its a really nice post to read and get info .

One of the few things I liked in I Am Number Four is Teresa Palmer’s energetic performance.

I’m really enjoying the theme/design of your blog. Do you ever run into any web browser compatibility issues? A number of my blog audience have complained about my website not operating correctly in Explorer but looks great in Firefox. Do you have any advice to help fix this issue?

I want to convey my appreciation for your kind-heartedness in support of visitors who must have assistance with this particular situation. Your real dedication to passing the message all-around appears to be exceedingly functional and have regularly permitted most people much like me to reach their pursuits. The invaluable tips and hints signifies a lot a person like me and additionally to my colleagues. With thanks; from all of us.

Human growth hormone supplements have lots of benefits to provide specifically to those who are currently past the age of thirty. Hgh supplements have been proven efficient in dealing with particular problems related to aging and doesn’t trigger as much side effects in comparison with other forms of Human growth hormone products. Additionally, supplements are effective, risk-free as well as inexpensive unlike Human growth hormone injections.

Hello! I know this is kinda off topic but I’d figured I’d ask. Would you be interested in exchanging links or maybe guest writing a blog post or vice-versa? My website goes over a lot of the same topics as yours and I feel we could greatly benefit from each other. If you are interested feel free to send me an email. I look forward to hearing from you! Terrific blog by the way!

I am glad to be one of the visitors on this great website (:, appreciate it for posting .

An intriguing discussion might be priced at comment. I think that you need to write regarding this topic, it might not become a taboo subject but normally individuals are insufficient to speak on such topics. An additional. Cheers

dance shoes that are shiny are the most cool stuff that you could possibly wear*

This is a topic that is near to my heart… Many thanks! Where are your contact details though?

I was extremely pleased to uncover this site. I want to to thank you for ones time for this particularly wonderful read!! I definitely savored every little bit of it and I have you bookmarked to look at new stuff on your blog.

Audio began playing as soon as I opened this site, so frustrating!

i like the songs of Kid Cudi because they are a bit emotional and kinda hip.

I have noticed that car insurance organizations know the cars which are at risk of accidents and various risks. Additionally, these people know what type of cars are susceptible to higher risk as well as the higher risk they have got the higher the premium price. Understanding the basic basics with car insurance will assist you to choose the right style of insurance policy that may take care of your needs in case you happen to be involved in any accident. Appreciate your sharing your ideas with your blog.

there is a need for firming lotion so that we can always maintain the health of our skin ..

I discovered your website web site on bing and check a number of your early posts. Keep up the great operate. I just additional increase RSS feed to my MSN News Reader. Looking for toward reading a lot more from you down the road!…

An impressive share, I simply with all this onto a colleague who had previously been conducting a little analysis for this. And he the truth is bought me breakfast since I discovered it for him.. smile. So i want to reword that: Thnx for that treat! But yeah Thnkx for spending some time to debate this, I am strongly about this and enjoy reading much more about this topic. When possible, as you grow expertise, would you mind updating your site with an increase of details? It is actually extremely helpful for me. Big thumb up for this article!

You’ve made some good points there. I looked on the web to learn more about the issue and found most people will go along with your views on this web site.

I have caught great sites and I have caught not so wonderful blogs. This blog is very informationrmative in many ways and certainloy ranks in the former category. Really appreciate the information your providing use avid scaners!

Nice post. I was checking constantly this blog and I’m impressed! Very helpful information specifically the last part I care for such information much. I was seeking this particular info for a long time. Thank you and best of luck.

This is actually appealing, You’re a significantly seasoned author. I have joined with your feed plus expect witnessing the very good write-ups. And additionally, We’ve shared your web blog inside our social networking sites.

An intriguing discussion is definitely worth comment. I do think that you ought to write more about this topic, it may not be a taboo matter but generally folks don’t speak about such issues. To the next! Kind regards!

very good post, i undoubtedly really like this website, continue it

Greetings! Very helpful advice within this article! It is the little changes that make the largest changes. Thanks for sharing!

There is certainly a lot to find out about this subject. I really like all the points you’ve made.

Good post. I learn something new and challenging on blogs I stumbleupon every day. It’s always exciting to read articles from other writers and use something from other web sites.

Hi, i think that i saw you visited my weblog so i came to “return the favor”.I’m attempting to find things to improve my site!I suppose its ok to use some of your ideas!!

there are bronze and brass dining chairs too that looks very elegant because of their color;;

This web site is often a walk-through for all of the knowledge you wanted concerning this and didn’t know who must. Glimpse here, and you’ll absolutely discover it.

Aw, this was a very nice post. Taking a few minutes and actual effort to create a superb article… but what can I say… I put things off a lot and never manage to get anything done.

There is noticeably a lot of money to know about this. I suppose you have made specific nice points in features also.

Good post. I be taught one thing more challenging on completely different blogs everyday. It is going to always be stimulating to read content material from other writers and apply a little something from their store. I’d want to use some with the content on my blog whether or not you don’t mind. Natually I’ll offer you a link in your web blog. Thanks for sharing.

An intriguing discussion is worth comment. I do think that you need to publish more on this issue, it might not be a taboo matter but usually people don’t speak about these subjects. To the next! Many thanks.

I believe one of your ads caused my internet browser to resize, you might want to put that on your blacklist.

Greetings! Very useful advice in this particular article! It is the little changes which will make the largest changes. Many thanks for sharing!

Pretty! This has been an incredibly wonderful article. Many thanks for supplying this info.

I wanted to thank you for this very good read!! I absolutely enjoyed every little bit of it. I have got you bookmarked to look at new stuff you post…

I couldn’t resist commenting. Well written!

Oh my goodness! an amazing article dude. Many thanks Nonetheless I’m experiencing trouble with ur rss . Don’t know why Can not sign up for it. Is there anybody finding identical rss problem? Anyone who knows kindly respond. Thnkx

Couldn´t be written any kind of far better. Reading this post reminds me of my old room mate! He always kept talking about this. I can forward that article to him. Extremely sure he definitely will possess a excellent read. Thanks for sharing!

I love looking through a post that can make people think. Also, thanks for permitting me to comment.

Does a one day job count as “Work Experience” under the common application?

Some really quality blog posts on this site, saved to fav.

Pretty! This was an extremely wonderful article. Many thanks for providing these details.

It’s essential to have having access to the knowledge posted here

hello your own weblog design is quite good, clean as well as clean so with updated content material, make men and women really feel serenity and i also constantly get pleasure from searching the site.

After checking out a few of the blog posts on your blog, I seriously like your way of blogging. I book-marked it to my bookmark website list and will be checking back in the near future. Please check out my website too and let me know how you feel.

You should be a part of a contest for one of the best sites online. I will recommend this blog!

Saved as a favorite, I love your web site.

Good blog you have got here.. It’s hard to find excellent writing like yours these days. I truly appreciate individuals like you! Take care!!

After I initially left a comment I appear to have clicked the -Notify me when new comments are added- checkbox and now every time a comment is added I get four emails with the exact same comment. There has to be a means you are able to remove me from that service? Thanks.

I blog often and I really appreciate your information. The article has really peaked my interest. I am going to take a note of your website and keep checking for new details about once per week. I subscribed to your Feed too.

I enjoy reading through an article that will make people think. Also, thanks for allowing for me to comment.

I couldn’t refrain from commenting. Exceptionally well written.

Saved as a favorite, I really like your website.

I needed to thank you for this wonderful read!! I absolutely loved every little bit of it. I have got you saved as a favorite to check out new stuff you post…

An impressive share! I have just forwarded this onto a colleague who had been doing a little research on this. And he actually ordered me breakfast simply because I found it for him… lol. So let me reword this…. Thank YOU for the meal!! But yeah, thanx for spending some time to talk about this matter here on your website.

This is a great tip especially to those fresh to the blogosphere. Simple but very accurate info… Appreciate your sharing this one. A must read post!

An interesting discussion is worth comment. I do believe that you ought to write more about this subject matter, it might not be a taboo matter but typically people don’t discuss these subjects. To the next! All the best.

Next time I read a blog, I hope that it doesn’t fail me as much as this one. After all, Yes, it was my choice to read, nonetheless I genuinely believed you would have something useful to say. All I hear is a bunch of crying about something you could possibly fix if you weren’t too busy seeking attention.

Having read this I believed it was extremely informative. I appreciate you finding the time and effort to put this short article together. I once again find myself spending way too much time both reading and commenting. But so what, it was still worth it!

Excellent post! We are linking to this great post on our website. Keep up the good writing.

This is a topic which is near to my heart… Thank you! Where can I find the contact details for questions?

I absolutely love your blog.. Very nice colors & theme. Did you make this web site yourself? Please reply back as I’m wanting to create my very own site and would love to find out where you got this from or exactly what the theme is named. Kudos.

This website was… how do you say it? Relevant!! Finally I have found something that helped me. Thank you!

I really like looking through a post that will make people think. Also, many thanks for allowing for me to comment.

Saved as a favorite, I love your website.

Greetings! Very helpful advice within this article! It is the little changes that will make the most significant changes. Thanks for sharing!

Aw, this was a really nice post. Taking a few minutes and actual effort to produce a really good article… but what can I say… I put things off a lot and don’t seem to get anything done.

Watch our exclusive Neerfit sexy bf video on neerfit.co.in.

I needed to thank you for this wonderful read!! I definitely loved every bit of it. I have got you book-marked to look at new stuff you post…

Your style is unique compared to other folks I have read stuff from. Many thanks for posting when you’ve got the opportunity, Guess I’ll just book mark this blog.

The very next time I read a blog, I hope that it won’t disappoint me as much as this one. After all, I know it was my choice to read through, nonetheless I actually thought you’d have something useful to talk about. All I hear is a bunch of moaning about something you can fix if you were not too busy searching for attention.

Hey there! I just would like to give you a huge thumbs up for the great information you have here on this post. I’ll be returning to your site for more soon.

Good post. I learn something new and challenging on sites I stumbleupon everyday. It’s always useful to read articles from other authors and practice a little something from their web sites.

Good blog you have got here.. It’s difficult to find quality writing like yours nowadays. I honestly appreciate individuals like you! Take care!!

Hi there! This post couldn’t be written much better! Looking through this post reminds me of my previous roommate! He always kept talking about this. I’ll send this article to him. Pretty sure he’ll have a very good read. Many thanks for sharing!

bookmarked!!, I love your website!

You’ve made some good points there. I checked on the net for more information about the issue and found most people will go along with your views on this website.

Good day! I could have sworn I’ve visited this blog before but after going through a few of the posts I realized it’s new to me. Regardless, I’m definitely delighted I came across it and I’ll be bookmarking it and checking back frequently!

Excellent post. I am facing a few of these issues as well..

Spot on with this write-up, I actually think this website needs a lot more attention. I’ll probably be back again to read through more, thanks for the advice.

Certainly with your thoughts here and that i love your blog! I’ve bookmarked it making sure that I can come back & read more in the foreseeable future.

I’m amazed, I have to admit. Rarely do I come across a blog that’s both equally educative and interesting, and without a doubt, you have hit the nail on the head. The issue is an issue that not enough people are speaking intelligently about. Now i’m very happy that I came across this in my search for something concerning this.

Spot on with this write-up, I seriously think this website needs a lot more attention. I’ll probably be returning to read through more, thanks for the information.

Good post. I learn something new and challenging on blogs I stumbleupon everyday. It will always be useful to read through articles from other writers and practice something from other sites.

This is a topic which is near to my heart… Best wishes! Exactly where can I find the contact details for questions?

Spot lets start on this write-up, I truly feel this website needs a lot more consideration. I’ll apt to be again to learn to read additional, thank you that information.

I cannot thank you fully for the posts on your web page. I know you set a lot of time and effort into them and really hope you know how deeply I enjoy it. I hope I’m able to do something identical man or woman someday.

Magnificent goods from you, man. I have understand your stuff previous to and you are just extremely fantastic. I really like what you’ve acquired here, really like what you’re saying and the way in which you say it. You make it enjoyable and you still care for to keep it smart. I can not wait to read much more from you. This is actually a wonderful web site.

i love the smile of Rachel Bilson, i got a huge crush on her*

dj equipments that are built by Sennheiser are the best in my opinion, we always use them when we have a gig::

I discovered your site website on bing and check some of your early posts. Always maintain inside the great operate. I recently additional encourage RSS feed to my MSN News Reader. Looking for forward to reading more within you at a later time!…

Me gustaría decir lo que una ayuda para encontrar a alguien que sabe realmente lo que son hablar acerca de internet. Definitivamente sabe consejos transmitir un problema a la luz y hacer importantes. Más individuos deben leer y comprender este aspecto de la historia. No puedo considero youre no más común porque tiene sin duda el regalo.

I am continually searching online for tips that can benefit me. Thanks!

Fantastic website, Simply wanted in order to opinion will not connect with the actual rss or atom flow, you may want set up the proper extension for your in order to workthat.

Thank you for the sensible critique. Me & my cousin were just preparing to do a little research about this. We grabbed a book from our local library but I think I learned more from this post. I am very glad to see such great info being shared freely out there…

Hawkins, Christopher. “The life and adventures of Christopher Hawkins, a prisoner on board the ‘Previous Jersey’ prison ship in the course of the Warfare of the Revolution.” Holland Membership.

Not so fast. Any landscape analysis should take those lines into account — especially when planning tree patterns and growth.

He tempted prospects by the tens of millions with steeply discounted merchandise — all the things from soap to power tools — and threw in free transport, too.

These travels made Marco the primary European to see the width and breadth of the nation.

If you are filing a joint return, figure your energy efficient dwelling improvement credit score as follows.

During these years, guest authors and co-authors included Harry R. (“Rick”) Moody, Director of Academic Affairs at the AARP; Janice I. Wassel, Director of The Gerontology Program at the University of North Carolina at Greensboro; Robert C. Atchley, Director of the Scripps Gerontology Center at the Miami University of Ohio; and Steven J. Devlin, a former vice-provost at Lehigh University.

Conversely, the diversified portfolio’s return will always be higher than that of the worst-performing investment.

You may then put up to all of the legal entities, or a subset of them, from the preview itself.

CIA Internet site. The President’s International Intelligence Advisory Board includes individuals from the non-public sector who examine how well the CIA is doing its job and the effectiveness of its structure.

I won’t repeat all of the vendor information that’s on my companion web page about buying a regulation checkers set: checker-sets.html .

Groups of two to three volunteers can simply fill sandbags, taking simple safety precautions, equivalent to carrying gloves to handle the chemically handled baggage.

Niarchos did not specify or reportedly even know the exact length of Onassis’s yacht.

But both are not on the same page as far as a separate debt office and setting up of a monetary policy committee (within the new policy framework) are concerned.

Brian Clarke was born in Oldham, Lancashire, to Edward Ord Clarke, a coal miner, and Lilian Clarke (née Whitehead), a cotton spinner.

Choices for making a cool roof embody supplies like modified bitumen, single-ply membranes, cool roof coatings and even green (vegetated) roofs.

Password management and enforcement is another aspect of logical safeguards that are covered by IT risk assessments.

Now ship the elephant out to collect other tasty Halloween treats.

A database that contains data but is not part of any series of steps to deliver business value using that data.

B2B operators can supply their shoppers exceptional European tours, while DMCs leverage their experience to broaden their reach.

It is solely natural: Girls with straight hair would often kill for a curly hair day.

Coping with a couple of defeats and a little bit of supporter unrest was nothing too disturbing this early in the season and it’s not like we hadn’t experienced all of it earlier than once we first received promoted to the Conference South.

The outfit is anticipated to sell for $3,000 (£2,073) or more.

The shut proximity of the kitchen to dining and residing areas makes the space appear intimate and is good when family and friends assemble.

It is professional trade that calls for great caution combined with speculation to achieve success.

After three unsuccessful makes an attempt at gaining an advantage with 1.e4, Karjakin performed 1.d4 for the primary time in the match.

It is most often used for the acquisition of a large merchandise like a automobile.

Hearth is considered a medium by way of which spiritual perception and knowledge is gained, and water is taken into account the source of that wisdom.

At 15 seasons, he holds the record for most consecutive seasons of winning a minimum of one race (shared with Hamilton), and he holds the file for most wins at the identical venue (eight, on the Magny-Cours circuit in France) and in addition the record for the most wins in the same Grand Prix (eight, France).

If you are not at all positive in regards to the stocks then the neatest thing is to wait for the right time and make a superb research of the same after which proceed in the direction of making the right funding in the market.

Also, the Guidelines stop paying interest altogether as of 2013, and make the mistake of converting back to Sol at the average foreign exchange rate of 2013, instead of the exchange rate in effect at the time of actual payment – which, pursuant to the Guidelines, may occur many years from now.

But even Beyoncé is aware of that nice inspiration can be discovered from past artists all through history – when you’re searching for an outfit that screams “Renaissance”, why not lean into the pun with an outfit inspired by artists like Da Vinci and Michaelangelo?

One other facet of Firefox versus Web Explorer security is the fact that Firefox is an open supply program.

Unlike France and Britain, at the outbreak of the First World War Germany found itself largely excluded from international financial markets.

The vast majority are solely rich to the extent that they have a lease of a chunk of actually low high quality land in a fantastic a part of the nation where folks want to reside.

In here, such investment vehicle is termed as stock options.

When the World Stopped Making Sense, set in the dark Ages.

From flowing tulle skirts to corseted bodices and intricate lace accents, there are countless possibilities to convey your gothic imaginative and prescient to life.

I like to think I’m a laugh riot.

Once your arms get wet, it’s easy to lose your grip on clean, slick surfaces.

Thus, though White possesses the bishop pair, it’s normally advisable for Black to open the sport quickly to exploit their lead in development.

The standard terminology and examples of business models do not apply to most nonprofit organizations, since their sources of income are generally not the same as the beneficiaries.

This means the payments made to the shareholders are first paid to the preference shareholder(s) and then to the fairness shareholders.

Checkout the whole new collection of emerald cut ruby rings at GemsNY, in their big selection of jewelry that is beautiful and irresistible.

Vintage fashion is sizzling, and it’s everywhere.

One out of the seventeen FOMC participant said within the April meet that additional steadiness sheet motion within the near-time period can be acceptable so as to mitigate downside dangers to economic progress.

Incentive inventory choices (ISOs) are solely accessible for employees and other restrictions apply for them.

Reports from DR Horton, a publicly traded national builder, show orders are 45 percent above levels from the prior year and cancellation rates dropping from 38 percent to 26 percent.

Each report has four tracks keyed by color and associated to a kind of musical instrument akin to drums, guitar or vocals.

If you become a member of an internet stock mercantilism platform, one that gives solutions on the far side brokerage, you’ll get tailor created stock tips in correct together with your mercantilism objectives.

If you buy a Volt or have your Prius transformed, precisely where are you going to plug it in?

If the latter is the case, then as a client decreases consumption of 1 good in successive items, successively larger doses of the opposite good are required to keep satisfaction unchanged.

Either a 153-cid Super-Thrift 4-cylinder engine or 194-cid six offered the facility.

Great Britain’s neglect, in the absence of the anticipated supplies from Patriots, resulted in starvation and illness.

But, in accordance with a examine within the Journal of the Society of Beauty Chemists, petroleum jelly’s pore-clogging reputation may be as mythical as wrinkle-free aging.

This article appears at some of the important causes for availing traveller insurance.

Have your luggage packed the night time earlier than.

GOODE, HUGHES, KLEPPER, LOVETT, SMITH Greer County: Mangum Day by day Star, Thursday, September 11, 1975 HUGHES Funeral services for E. W. (Bill) HUGHES, retired Mangum mechanic, have been held at eleven a.m.

It seeks to identify long term secure trends that are likely to shape the world we live in and will be the driving forces behind the financial markets in future.

One of the most powerful pre-war vehicles ever produced, which model hit the streets a year before the stock market crashed?

Transmission and drivetrain are important components in figuring out towing capability.

In case you have an incredible thought for starting your own enterprise, the Strength Tarot Card encourages you to faucet into your internal power and power to succeed.

Online bill cost is also safer than the snail-mail methodology: Your personal data is way more vulnerable to theft if it is on paper and physically transferring via the postal system.

Eventually, cities began to gather trash, however typically garbage was hauled to dumps – open holes in the ground – the place it usually was burned, creating air pollution that was a hazard to human health.

The world of forex trading has two predominant schools of thought.

Because of this, universities are at all times appealing to alumni and others in the community for monetary gifts, so donating is a wonderful solution to help your favorite program.

In reality, New World is the headquarters for the Intelligence’s new plan to conquer the world by infecting all the computer systems.

This country works as a monarchy, but a special household guidelines each of the emirates.

McClain, Dylan Loeb (30 April 2023).

In September 2020, vulnerabilities in MTI’s website were exposed by Anonymous ZA and a MyBroadband investigative journalist, leading to worldwide warnings against the company.

After all you needed to order the Deluxe to get this interior; cheaper fashions had more austere upholstery.

That means that people will have much less disposable income, and can afford less, as the middle class and poor are squeezed by the rising cost of living.

If the experience of Deus Ex taught me one factor, it’s the importance of workforce dynamics.

Watch our most viewed super sexy bf video on socksnews.in. sexy bf video Watch now.

What truck sells the best in Canada?

The aim and the that means of existence is to strive upward past the boundaries of the known, and to help each other.

By 1877, when “Paris: A Rainy Day” was finished, the city of Paris had gone through a major transitional period.

The company did the identical things all recreation firms do, went through the same issues, however because we painted an enormous ol’ “suck it down” target on our chests, the gaming press and a fair variety of hardcore players went after us with a vengeance.

This section possibly comprises original research.

Thanks for sharing. Like your post.Name

Within the Nationwide Hockey League, the season was suspended for an indefinite amount of time, affecting the Pittsburgh Penguins and Philadelphia Flyers.

https://www.leodirectory.com/premium-flower-delivery-dubai-fresh-elegant-blooms/

Well written!

Indian Taxation System has labeled more than 1211 merchandise for requiring of products and Services Tax below 6 normal classifications or assessment pieces.

A VPS means that you can trade the Forex and have your account open and your transactions open even in case your laptop is off.

But it’s clear that in order to boost fuel mileage and still hold on to the gains made safety, comfort, and performance, automakers will have to embrace different methods than the ones dominant today.

After study many of the web sites for your internet site now, i really appreciate your strategy for blogging. I bookmarked it to my bookmark site list and will be checking back soon. Pls have a look at my web-site too and figure out what you consider.

Thank you for sharing this good write-up. Very inspiring! (as always, btw)

An impressive share, I just given this onto a colleague who was carrying out a little analysis within this. And the man in fact bought me breakfast because I came across it for him.. smile. So ok, i’ll reword that: Thnx to the treat! But yeah Thnkx for spending time go over this, I’m strongly about it and enjoy reading much more about this topic. If you can, as you become expertise, can you mind updating your website to comprehend details? It truly is highly great for me. Big thumb up just for this short article!

Shortly after his victory, Carlsen talked about that he might not be motivated enough to play one other world championship match unless the challenger was Alireza Firouzja, an 18-yr-previous prodigy who had risen to quantity two on the planet rankings.

For example, a large pool with plenty of bushes around may require a more highly effective pump and a bigger filter.

There are online companies focusing on providing prepared-made Non-public Placement Memorandum with all the authorized modalities included, along with a subscription settlement and funding questionnaire.

Which college did NBA superstar LeBron James play for?

Unfortunately, some troopers have found it not possible to open the doorways if the locks are damaged out in the field.

Residents or traders of Fairfield nation are in luck.

At first, it was merely a “quotation system” and did not present a approach to carry out digital trades.

Interiors will feature handcrafted real wooden trim, actual metal accents, delicate-touch supplies, 12-speaker Bang & Olufsen luxurious sound system, twin panel panoramic glass roof with energy shade, gentle premium diamond-quilted perforated leather-based climate-controlled and massaging seats with French seam stitchwork, smooth leather-based wrapped sprint, steering wheel, and door panels with single and double stitched ornamental stitchwork.

The following year brought another interesting new option: all-wheel drive, a part-time “shift-on-the-fly” setup intended for maximum traction on slippery roads, not dry-pavement driving or off-roading.

The airport has understood its accountability in direction of the atmosphere.

It definitely seems costly, but fact be informed, there are some dishes out there that make Mallie’s “Completely Ridiculous Burger” appear low cost.

I fully agree with this. There’s a similar post on Thew14.com that explores this topic, and it provides further insights that align with your argument.

I couldn’t agree more with this comment. It reflects a perspective I’ve seen before in various discussions on Thew14.com, which offers some great insights into this matter.

Is it dangerous if a baby eats dog food?

These pieces can never be considered as old school.

I enjoy reading a post that can make men and women think. Also, thank you for allowing me to comment.

Thanks so much for sharing all of the awesome info! I am looking forward to checking out more posts!

I truly love your site.. Very nice colors & theme. Did you build this web site yourself? Please reply back as I’m attempting to create my own personal blog and would like to find out where you got this from or exactly what the theme is named. Cheers.

Green bangles, mangalsutras, conventional necklaces, and a classic Maharashtrian Nath are worn by Maharashtrian brides.

Youre so cool! I dont suppose Ive read anything similar to this prior to. So nice to discover somebody with original ideas on this subject. realy we appreciate you beginning this up. this fabulous website can be something that is needed on the internet, someone with a bit of originality. helpful work for bringing new stuff on the world wide web!

Saved as a favorite, I really like your web site!

I like reading through an article that can make people think. Also, many thanks for allowing for me to comment.

I really like it when folks come together and share opinions. Great blog, keep it up.

This blog was… how do I say it? Relevant!! Finally I’ve found something which helped me. Cheers.

Having read this I thought it was very informative. I appreciate you taking the time and effort to put this content together. I once again find myself personally spending a significant amount of time both reading and posting comments. But so what, it was still worth it.

You’re so cool! I do not suppose I’ve truly read through something like that before. So good to find somebody with some genuine thoughts on this topic. Seriously.. thanks for starting this up. This website is one thing that’s needed on the web, someone with a bit of originality.

After exploring a handful of the articles on your web page, I seriously like your way of writing a blog. I book-marked it to my bookmark site list and will be checking back in the near future. Take a look at my web site as well and tell me your opinion.

I couldn’t resist commenting. Exceptionally well written.

i was home schooled when i was still very young and i have to stay that it is also a great way to educate your kids,,

I need to to thank you for this very good read!! I absolutely loved every bit of it. I have you book-marked to check out new stuff you post…

Thanks for making the effort to line all this out for us. This kind of post was in fact quite helpful in my opinion.

This new use works greatest with lamps that may handle the outdoors.

Usually I don’t comment on your blog. I am more of the silent type but I wonder, is this wordpress because I am thinking of switching my own blog from blogspot to wordpress.

Your style is really unique compared to other folks I have read stuff from. Many thanks for posting when you’ve got the opportunity, Guess I will just book mark this site.

Cool. – Gulvafslibning | Kurt Gulvmand looks great, and I’m glad i’ve found something here worth adding to my favorites.

After going over a handful of the articles on your site, I honestly appreciate your technique of writing a blog. I bookmarked it to my bookmark webpage list and will be checking back in the near future. Take a look at my website too and tell me what you think.

After i open up your own Feed it offers myself with many different garbled text message, could be the concern on my small conclusion?

This website was… how do you say it? Relevant!! Finally I’ve found something which helped me. Kudos!

It can be difficult to write about this subject. I think you did an excellent job though! Thanks for this!

Karjakin tried to actively search counterplay, but Carlsen fended him off and simplified right into a successful endgame, earning Karjakin’s resignation.

we can always give food aid to the african countries if we just save some pennies and donate it to them~

The stop order is placed at a specific price below the current market, such that if the price is triggered, will convert into a market order.

There’s certainly a lot to know about this subject. I really like all of the points you made.

An outstanding share! I have just forwarded this onto a co-worker who has been conducting a little homework on this. And he in fact bought me dinner simply because I stumbled upon it for him… lol. So let me reword this…. Thank YOU for the meal!! But yeah, thanx for spending some time to talk about this matter here on your web site.

Excellent read, I just passed this onto a friend who was doing some research on that. And he actually bought me lunch because I found it for him smile Thus let me rephrase that: Thank you for lunch!

Thanks for your insight for the great posting. I am glad I have taken the time to see this.

Having read this I believed it was rather enlightening. I appreciate you finding the time and energy to put this informative article together. I once again find myself spending a significant amount of time both reading and posting comments. But so what, it was still worthwhile.

Having Get Reports Write-up Submission move Product, you can actually shift deeper and even speedier than you’ve ever imagined on the subject of what you can do internet.

Can I recently say such a relief to find somebody that truly knows what theyre referring to on-line. You certainly have learned to bring a concern to light making it essential. The diet have to ought to see this and appreciate this side on the story. I cant think youre less common because you certainly have the gift.

Good day! I could have sworn I’ve visited this blog before but after going through some of the articles I realized it’s new to me. Anyways, I’m definitely pleased I stumbled upon it and I’ll be book-marking it and checking back regularly!

Southwick, Ron (July 14, 2020).

I need to to thank you for this good read!! I certainly enjoyed every little bit of it. I have got you bookmarked to check out new stuff you post…

i am addicted to computer games that is why i bought a gamecube for me and my brother,.

How is it that just anyone can write a weblog and get as popular as this? Its not like youve said something extremely impressive more like youve painted a fairly picture through an issue that you know nothing about! I dont want to sound mean, right here. But do you really think that you can get away with adding some pretty pictures and not definitely say anything?

hi. I notice that you were involved in creating quality backlinks and stuff. I’m selling scrapebox auto approve lists. Would you like to trade ?

Spot on with this write-up, I honestly believe that this site needs a lot more attention. I’ll probably be returning to read through more, thanks for the info.

It’s a really amazing powerful resource that you’re offering and you just provide it away cost-free!! I that can compare with discovering websites which be aware of the particular in supplying you with fantastic learning resource for zero cost. We truly dearly loved examining these pages. Appreciate it!

Thank you a bunch for sharing this with all folks you actually realize what you’re speaking approximately! Bookmarked. Kindly additionally seek advice from my site =). We could have a link trade contract between us!

Hiya! I randomly stumbled upon your blog from Bing. Your article is filled with interesting information, and I will definitely use it at some point in my career. Keep up the excellent work!

I love reading your blog because it has very interesting topics.:-`”‘

gaming computers should have multiple cpu cores and a lot of memory to support those heavy graphics“

Right here is the right blog for anyone who would like to find out about this topic. You understand a whole lot its almost tough to argue with you (not that I really would want to…HaHa). You certainly put a new spin on a subject that’s been written about for years. Wonderful stuff, just excellent.

I love reading through an article that will make men and women think. Also, thanks for allowing me to comment.

Cool news it is really. I’ve been waiting for this tips.

Hey There. I found your blog using msn. This is a very well written article. I’ll make sure to bookmark it and return to read more of your useful information. Thanks for the post. I’ll definitely return.

ceramic floor tiles are the best, i used to have linoleum tiles but they do not last very long;

Many thanks for posting this, It?s simply what I used to be researching for on bing. I?d a lot comparatively hear opinions from an individual, slightly than a company web page, that?s why I like blogs so significantly. Many thanks!

F*ckin? tremendous things here. I am very satisfied to see your post. Thank you so much and i’m taking a look forward to contact you. Will you please drop me a mail?

*When I originally commented I clicked the -Notify me when new comments are added- checkbox and now each time a comment is added I get four emails with the same comment. Is there any way you can remove me from that service? Thanks!

I really like it when people come together and share views. Great site, keep it up.

Very good post. I will be dealing with a few of these issues as well..

This web site truly has all the information and facts I wanted about this subject and didn’t know who to ask.

I blog quite often and I truly appreciate your content. This article has truly peaked my interest. I am going to book mark your site and keep checking for new details about once a week. I opted in for your RSS feed as well.

I will immediately take hold of your rss feed as I can’t in finding your e-mail subscription hyperlink or e-newsletter service. Do you have any? Kindly allow me recognise so that I may just subscribe. Thanks.

My friend first found your blog on Google and she referred your blog to me.`’;\’;

Very interesting points you have noted , regards for posting .

Walking on the smooth white sand of the sea floor gives a cinematic view of marine life.

Great write-up, I am normal visitor of one?s blog, maintain up the excellent operate, and It is going to be a regular visitor for a long time.

Wow, awesome weblog structure! How lengthy have you ever been running a blog for? you made running a blog glance easy. The whole look of your website is magnificent, let alone the content material!

I’m a blog crazed person and i love to read cool blog like yours.~`;.,

Thank you for your information and respond to you. bad credit auto loans hawaii

howdy, I am ranking my site higher “cb auto profits”.

As I website possessor I believe the content matter here is rattling fantastic , appreciate it for your efforts. You should keep it up forever! Best of luck.

Wonderful article! We will be linking to this particularly great post on our site. Keep up the great writing.

Aw, this was an incredibly nice post. Spending some time and actual effort to produce a very good article… but what can I say… I put things off a lot and never seem to get nearly anything done.

Great post! We are linking to this particularly great post on our site. Keep up the good writing.

Your style is really unique in comparison to other people I’ve read stuff from. I appreciate you for posting when you’ve got the opportunity, Guess I’ll just bookmark this page.

Youre so cool! I dont suppose Ive read anything like this before. So nice to find somebody with original thoughts on this subject. realy i appreciate you for beginning this up. this site is one area that is required on the internet, an individual after some originality. useful job for bringing new stuff to your net!

Hello, my group is just establishing our first website, searching and working out what is needed. This blog stuck out right away. I’m fired up about this, and adore the design of your site. Are you able to let me know what “theme” it is?

Absolutely composed written content , thanks for information .

EPA has given native councils powers to manage this sort of noise.

Good post. I am facing many of these issues as well..

Great article! We are linking to this particularly great post on our website. Keep up the great writing.

My spouse and i felt very fortunate when Michael managed to conclude his basic research through the ideas he had from your own web pages. It’s not at all simplistic to just possibly be offering solutions that others could have been making money from. And now we discover we need you to thank for this. The most important illustrations you made, the simple site navigation, the relationships you give support to create – it’s many overwhelming, and it’s really leading our son and our family feel that this subject matter is exciting, which is really mandatory. Thanks for the whole lot!

I concur with your conclusions and will eagerly watch forward to your future updates. The usefulness and significance is overwhelming and has been invaluable to me!

This is a excellent blog, will you be interested in doing an interview about how you developed it? If so e-mail me!

I seriously love your blog.. Pleasant colors & theme. Did you make this web site yourself? Please reply back as I’m trying to create my own site and want to know where you got this from or what the theme is called. Thank you.

Because the farm-to-table movement grows, they’re springing up everywhere in the place.

Six to twelve months earlier than the marriage is also an appropriate window to hire a Destination Marriage ceremony Planner in Delhi, but it might require some flexibility with dates and venues.

Most of the regular stock buyers started to stroll away from the share markets, but few people who are intelligent purchased the shares which have been at an unbelievable decrease price.

U.S. output and real exchange rates.

Just be aware that there’s no hyperlink you may get to create a non-public game however you may simply all comply with log into the same enjoying room and signing-up is required.

When you have a storage then you’ve got a garage door opener, a remote control machine that you need to use to open and shut your storage door from inside your automotive and even inside your home.

Just right points?I’d word that as anyone who truly doesn’t write on blogs a lot (if truth be told, this can be my first put up), I don’t assume the term ‘lurker’ may be very changing into to a non-posting reader. It’s not your fault the least bit , however most likely the blogosphere may get a hold of a better, non-creepy name for the ninety people that experience reading the content .

Considerably, the post is in reality the finest on that laudable topic. I fit in with your conclusions and can eagerly look forward to your incoming updates. Saying thanks definitely will not simply just be enough, for the outstanding clarity in your writing. I will certainly at once grab your rss feed to stay privy of any kind of updates. Pleasant work and also much success in your business efforts!

I am lucky that I found this web blog, precisely the right information that I was searching for!

A hyper-efficient decentralized crypto marketplace built on Sui. Turbos finance Sui Trade Trade any crypto on Sui. Best prices are offered through aggregating liquidity.

Balances Active Orders Withdraw Deposit TradeOgre Logout · Sign In. Search: Currency, Market, Change, Price

A hyper-efficient decentralized crypto marketplace built on Sui. Turbos finance Trade Trade any crypto on Sui. Best prices are offered through aggregating liquidity.

I think other website proprietors should take this website as an model, very clean and wonderful user genial style and design, as well as the content. You are an expert in this topic!

Thanks for the good critique. Me & my neighbor were just preparing to do some research on this. We got a book from our area library but I think I’ve learned more from this post. I’m very glad to see such excellent information being shared freely out there..

very interesting subject , appreciate it for putting up.

Empower Your Crypto Journey

with Tangem Wallet

This is a topic that is close to my heart… Take care! Where can I find the contact details for questions?

Balances Active Orders Withdraw Deposit TradeOgre Logout · Sign In. Search: Currency, Market, Change, Price

Buy and sell Bitcoin, Ethereum, NoOnes and other cryptocurrencies Peer-to-Peer on NoOnes. Secure, fast, and user-friendly transactions on a trusted platform.

Having read this I believed it was really enlightening. I appreciate you spending some time and effort to put this informative article together. I once again find myself personally spending a lot of time both reading and commenting. But so what, it was still worth it.

Bpi net empresas Portugal, bpi net empresas Serviços. Plataforma de comunicação Multibancária · Canal SWIFT Net · App BPI Empresas · BPI Net Empresas. Tudo Sobre. Open Banking · Segurança Online

This is a topic that’s near to my heart… Best wishes! Exactly where can I find the contact details for questions?

Way cool! Some extremely valid points! I appreciate you penning this post and the rest of the site is very good.

You’re so awesome! I don’t believe I’ve truly read through anything like that before. So good to discover somebody with original thoughts on this subject. Seriously.. thanks for starting this up. This site is one thing that’s needed on the web, someone with a bit of originality.

I have to consider prospect of by way of thanking you actually for that quality recommendations May mostly demonstrated going over yuor web blog. We’re hopeful for your graduation about the actual or even look for in addition to the whole processing would not have already been finished whilst not coming over to your blog. Fundamentally may perhaps be in any assistance to the rest, Appraisal enjoy it in helping with what There are uncovered from this level.

This could be the right blog for everyone who is desires to be familiar with this topic. You already know much its practically not easy to argue along (not that I just would want…HaHa). You certainly put the latest spin with a topic thats been discussing for decades. Excellent stuff, just great!

Maud Jessie Johnson, JP, Divisional Director, British Pink Cross Society, Great Yarmouth.

An fascinating discussion will probably be worth comment. I believe that you ought to write more on this topic, may possibly not be described as a taboo subject but usually everyone is too little to communicate on such topics. To another location. Cheers

bookmarked!!, I really like your web site.

Schools like Texas A&M University and the College of Texas influence the culture and arts of surrounding towns.

Can I just say what a relief to find somebody who really understands what they’re talking about on the web. You definitely know how to bring a problem to light and make it important. More people must look at this and understand this side of your story. I can’t believe you are not more popular because you most certainly have the gift.

I quite like reading through an article that will make men and women think. Also, many thanks for allowing for me to comment.

There is definately a lot to learn about this topic. I really like all the points you have made.

Olive Kaer. For political and public service.

you could just listen to the beat of those high bass from Rap songs, i just like rap songs;;

Hello, I was researching the net and I came across your weblog. Keep up the excellent function.

I have to thank you for the efforts you have put in penning this site. I really hope to see the same high-grade content by you in the future as well. In fact, your creative writing abilities has inspired me to get my own site now 😉

Hi there, just became aware of your blog through Google, and found that it’s really informative. I’m gonna watch out for brussels. I will be grateful if you continue this in future. A lot of people will be benefited from your writing. Cheers!

New to your blog. Stumbled upon it browsing the web. Keep up the great work. I am hoping you update it regularly.

I’ve learn several just right stuff here. Certainly value bookmarking for revisiting. I surprise how much effort you put to create the sort of excellent informative web site.

Put together slaughter for his children for the iniquity of their fathers; that they don’t rise, nor possess the land, nor fill the face of the world with cities.

I discovered your blog post website on google and appearance a couple of your early posts. Preserve on the very good operate. I merely extra your RSS feed to my MSN News Reader. Looking for forward to reading far more within you down the line!…

Can I recently say what a relief to discover somebody that actually knows what theyre dealing with on the net. You certainly understand how to bring a difficulty to light to make it important. Workout . need to check this out and understand this side from the story. I cant think youre no more common when you certainly possess the gift.

You lost me, friend. I mean, I suppose I get what youre indicating. I realize what you are saying, but you just seem to have overlooked that there are some other individuals inside the world who look at this matter for what it definitely is and might not agree with you. You may be turning away a lot of folks who may have been supporters of your web site.

This is the right site for everyone who really wants to find out about this topic. You know so much its almost hard to argue with you (not that I personally will need to…HaHa). You definitely put a brand new spin on a subject that’s been written about for decades. Wonderful stuff, just excellent.

I really like looking through and I think this website got some really useful stuff on it! .

I believe that a simple and unassuming manner of life is best for everyone, best both for the body and the mind.

An interesting discussion might be priced at comment. I do think that you need to write read more about this topic, it might be described as a taboo subject but typically consumers are not enough to communicate on such topics. To another location. Cheers

Excellent post. I am experiencing some of these issues as well..

I need to to thank you for this good read!! I certainly enjoyed every little bit of it. I have got you saved as a favorite to check out new stuff you post…

I was able to find good information from your content.

“Hello! I could have sworn I’ve been to this blog before but after browsing through some of the post I realized it’s new to me. Anyways, I’m definitely happy I found it and I’ll be book-marking and checking back frequently!”

I’ve observed that in the world these days, video games are definitely the latest rage with kids of all ages. There are times when it may be extremely hard to drag your kids away from the video games. If you want the best of both worlds, there are lots of educational gaming activities for kids. Great post.

Thank you for this kind of information I was looking around all Yahoo to discover it!

Hi there! This blog post couldn’t be written much better! Looking through this post reminds me of my previous roommate! He constantly kept talking about this. I’ll send this article to him. Fairly certain he’s going to have a very good read. Many thanks for sharing!

Ford Motor Company. “Ford Automobiles: Assist – Glossary.” (Sept.

Your style is so unique compared to other people I’ve read stuff from. Thanks for posting when you’ve got the opportunity, Guess I’ll just bookmark this blog.

You need to take part in a contest for one of the most useful websites on the net. I am going to recommend this web site!

This site was… how do you say it? Relevant!! Finally I have found something that helped me. Thanks a lot!

The fee to upgrade the building to the required customary was estimated at NZ$3 million.

Hey i Love your work i really appreciate that. Also take a look at our special Gym flooring dubai

Good article. I definitely love this site. Keep it up!

This is a topic which is near to my heart… Take care! Where can I find the contact details for questions?

Way cool! Some extremely valid points! I appreciate you penning this write-up and also the rest of the site is also very good.

Can I simply say what a relief to uncover an individual who actually understands what they’re discussing on the net. You definitely realize how to bring an issue to light and make it important. More people have to check this out and understand this side of your story. It’s surprising you aren’t more popular because you definitely have the gift.

Aw, this was an exceptionally good post. Spending some time and actual effort to make a top notch article… but what can I say… I hesitate a lot and never manage to get anything done.

I wanted to thank you for this great read!! I definitely enjoyed every little bit of it. I have you saved as a favorite to look at new stuff you post…

Next time I read a blog, Hopefully it won’t fail me just as much as this one. After all, I know it was my choice to read through, however I actually thought you’d have something interesting to talk about. All I hear is a bunch of moaning about something that you could fix if you were not too busy looking for attention.

It’s hard to come by well-informed people on this topic, but you sound like you know what you’re talking about! Thanks

Aw, this was an incredibly good post. Spending some time and actual effort to produce a great article… but what can I say… I procrastinate a whole lot and never seem to get anything done.

The particular Amish’s important faith centered idea of Demut “humility”, plainly demonstrates the particular weak spot related to individualism as well as sociable school therefore well-known concerning individuals civilizations and also there exists a matching sturdiness relating to Amish party id.

After study a handful of the blog posts in your site now, we truly appreciate your method of blogging. I bookmarked it to my bookmark website list and will also be checking back soon. Pls take a look at my site also and tell me how you feel.

hello!,I love your writing very much! share we keep up a correspondence extra approximately your post on AOL? I require an expert in this area to resolve my problem. May be that is you! Having a look forward to see you.

This blog was… how do I say it? Relevant!! Finally I have found something which helped me. Thanks.

Very nice post. I absolutely love this website. Continue the good work!

An attention-grabbing dialogue is value comment. I believe that it is best to write extra on this subject, it won’t be a taboo subject however typically individuals are not enough to talk on such topics. To the next. Cheers

Can i get thumbs up never did? before (please ). … I love this song

Spot on with this write-up, I truly think this fabulous website needs far more consideration. I’ll more likely again you just read far more, thank you for that information.

Aw, this was an extremely good post. Taking the time and actual effort to produce a very good article… but what can I say… I put things off a lot and don’t seem to get nearly anything done.

Hi there! This article couldn’t be written any better! Looking at this article reminds me of my previous roommate! He continually kept talking about this. I will forward this information to him. Pretty sure he will have a great read. Thank you for sharing!

This web site definitely has all of the information and facts I needed concerning this subject and didn’t know who to ask.

After checking out a number of the blog articles on your blog, I truly appreciate your way of blogging. I added it to my bookmark website list and will be checking back in the near future. Take a look at my website too and let me know how you feel.

Great post, I think blog owners should larn a lot from this web blog its really user friendly .

Thanks, I enjoyed – Gulvafslibning | Kurt Gulvmand. It was good. View my blog sometime, it all about Altamonte Springs, FL Real Estate.

The next time I read a weblog, I hope that it doesnt disappoint me as a lot as this one. I mean, I know it was my choice to read, however I actually thought youd have something attention-grabbing to say. All I hear is a bunch of whining about something that you possibly can fix for those who werent too busy looking for attention.

I seriously love your blog.. Pleasant colors & theme. Did you make this site yourself? Please reply back as I’m attempting to create my very own website and would like to learn where you got this from or just what the theme is named. Cheers!

i have some small garden of herbs at home, i use them for baking foods and as herbal medicines~

This is an astonishing entry. Thank you very much for the supreme post provided! I was looking for this entry for a long time, but I wasn’t able to find a trustworthy source.

When I originally commented I clicked the -Notify me when new comments are added- checkbox now if a comment is added I buy four emails with similar comment. Could there be that is you are able to eliminate me from that service? Thanks!

TradeOgre is an online cryptocurrency exchange launched in 2018, providing a straightforward platform for buying, selling, and trading various digital assets.

I completely agree, this perspective makes a lot of sense. I recently found a very similar discussion on vb77.wiki, and it clarified some of the points you’ve made.

O BCE é o banco central dos ibercaja empresas países da UE que utilizam o euro. O nosso principal objetivo é a manutenção da estabilidade de preços. Para o efeito

Hello there! Do you know if they make any plugins to

help with Search Engine Optimization? I’m trying to get my blog to rank for some

targeted keywords but I’m not seeing very good results.

If you know of any please share. Appreciate it! I saw similar article here: Change your life

Any asset. RedStone supports secure price feeds for assets faster than competitors. RedStone has the deepest price discovery and most advanced pricing .

Very good written story. It will be helpful to everyone who usess it, including yours truly Smile. Keep doing what you are doing – i will definitely read more posts.

“To start earning money with your blog, initially use Google Adsense but gradually as your traffic increases”

Amazing blog! Do you have any suggestions for aspiring writers? I’m hoping to start my own site soon but I’m a little lost on everything. Would you suggest starting with a free platform like WordPress or go for a paid option? There are so many options out there that I’m completely overwhelmed .. Any ideas? Appreciate it!

This site was… how do you say it? Relevant!! Finally I have found something which helped me. Thanks.

Saved as a favorite, I like your website!

Terrific write-up! Thought about savored the actual scanning. I’m hoping you just read additional by you. There’s no doubt you could have wonderful awareness in addition to ability to see. My corporation is really prompted keeping this particulars.

I came across your blog’s link posted by a friend of mine on Facebook. Thanks for putting useful info on the internet. It’s tough to get these things these days.

An fascinating discussion will probably be worth comment. I believe that you ought to write more on this topic, may possibly not be described as a taboo subject but usually everyone is too little to communicate on such topics. To another location. Cheers