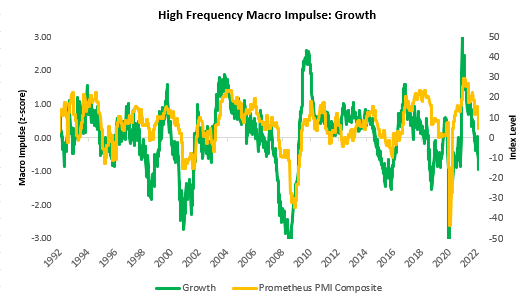

Our systematic tracking of economic and financial conditions paints a bleak picture for US equities. Commodity strength remains unrelenting in aggregate; however, we see areas of the commodity complex begin to weaken. Nonetheless, the fundamental backdrop remains where the growth impulse is negative, and inflation remains resiliently high. Markets continue to price these dynamics on a trending basis, with market discounting high nominal growth and tight liquidity conditions. Economic data over the last week outperformed expectations; however, we think it is essential to see the forest from the trees at this juncture and keep in mind that the trend in growth is lower. On the first count, we had ISM data surprising to the upside. However, when we aggregate all PMI data in the form of our PMI composite and put them in a cyclical context, we continue to see a downtrend:

On the second count, we have seen employment data remain resilient. However, as we have highlighted many times, employment data typically begins to deteriorate only after incomes & spending deteriorate. With real incomes already in negative territory, and negative wealth effect accumulating, spending is highly likely to continue lower. We aren’t likely to exit this dynamic anytime soon and offer insight into what this typically means for assets; we show our algorithmic analysis of analogous periods. Our systems look for periods in time that have similar growth, inflation, and market regime characteristics to better understand the path ahead of us:

As we can see, the last two cycles (2000 and 2008) saw periods similar to what we are seeing today, though they vary by extent significantly. Most importantly, these periods sustained significant equity drawdowns. We show the performance of various asset markets in this context:

In environments with weak growth, high inflation, and stagflationary market dynamics, equity markets have typically returned -10% on an annualized basis. Furthermore, even Treasuries have only eked out a 1% nominal return during these periods. Our strategies account for these dynamics in a rules-based manner, and they continue to tell us that equities and credit are not particularly good exposures in the current context. Our systems continue to advocate for net short positions in the same, though the degree of short positions (reflecting our systems conviction) has reduced. We show this below:

At the asset class level, the Prometheus Alpha Strategy dominantly has exposure to commodities & the dollar. This pairing has served well year-to-date, and given macroeconomic dynamics; we expect it will continue to do so in the very immediate future:

At the asset level, here’s how the systems are positioned going into next week:

In terms of catalyst/risks for next week, we have a relatively light week:

- Monday: NA

- Tuesday: Trade Balance, Consumer Credit

- Wednesday: Crude Oil Inventories, MBA Mortgage Applications

- Thursday: Jobless Claims

- Friday: CPI, Michigan Surveys

For our part, we will focus on consumer credit data and CPI. Consumer credit data will help better assess the health of households and help us better understand the likely trajectory for incomes and spending. Incremental spending can come from income, employment, or credit. Real wages are negative, employment is near all-time highs, and consumer borrowing is significantly elevated. These dynamics look increasingly unstable and are likely to resolve in lower spending. With regards to CPI, our high-frequency measures tell us there may be some abatement in inflation pressures:

Nonetheless, the inflation trend persists: allocate accordingly. Stay nimble!