Last week, markets continued to price tightening liquidity conditions, but now with a deflationary tilt. The Dollar continued to power ahead, alongside US Treasuries. Equities and Commodities suffered significant losses, telling us that markets were moving aggressively toward pricing in falling growth expectations. Markets were particularly focused on the further deterioration in economic data, something our systems have been well ahead of in this economic cycle. We walk through the current growth picture and how our systems are processing the current environment below:

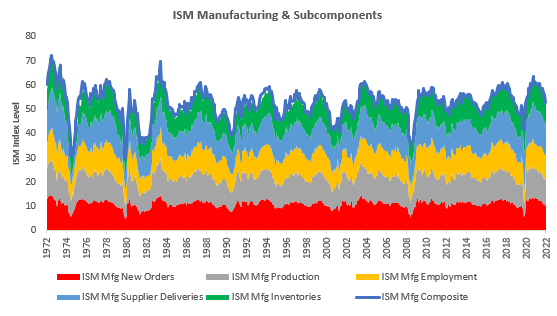

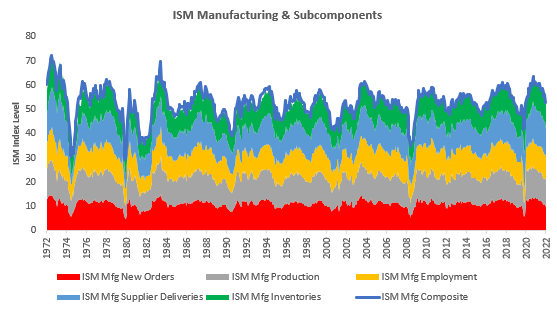

i. Economic data is likely to keep decelerating. Since the start of this year, our systems have warned us that we were headed towards an economic slowdown, allowing us to capitalize on the deterioration in the economic growth outlook that is currently taking place. Furthermore, our systems continue to tell us that there is unlikely to be a let-up in the pressures that now exist on economic activity. Most recent economic data have begun to confirm this view, with the latest ISM data showing significant deterioration. We offer ISM data below along with its subcomponents:

The latest ISM Manufacturing data showed an expansionary reading of 53, implying 5% YoY earnings for the S&P 500.

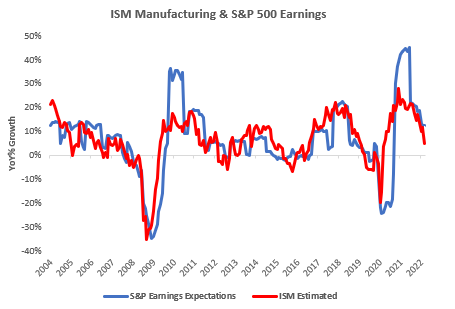

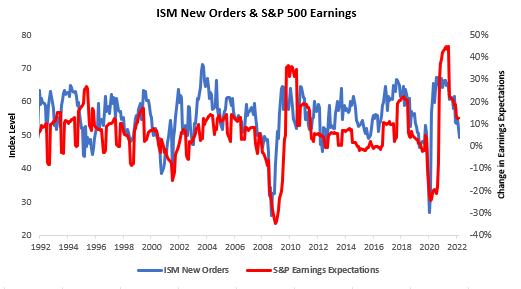

This reading was a sequential deceleration within a decelerating trend. The largest gaining segment was Supplier Deliveries, and the most significant slowdown was in employment. However, markets were most concerned with the decline in the New Order Index, which is considered the most forward-looking component of ISM. This reading indicates a bleak outlook for corporate profitability in the future. Below, we show how the ISM New Orders component typically presages turning points in S&P 500 earnings expectations:

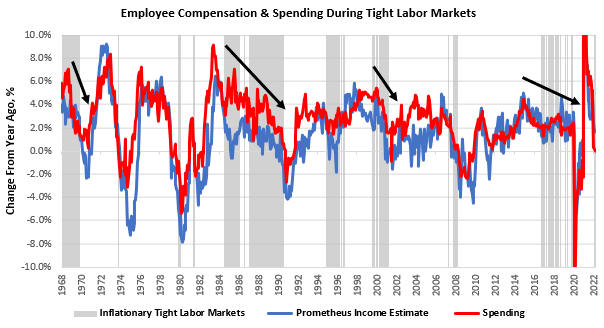

The outlook for earnings is extremely important for the economy’s outlook because of the profit motivations of the private sector. During periods of rising costs and declining profitability like today, firms are forced to pull back capital spending and employment. Currently, employment is holding up economic activity; however, this has a built-in self-limiting feature. The labor force is a natural resource, i.e., only so many people are available for employment in the economy at a given time. As a result, the more people employed, the fewer are available for hire in the future. This dynamic is worsened when inflationary pressures are abundant, and eventually, the pace of inflation overpowers the ability of the labor force to expand, creating negative real incomes. Below, show how this has played out in history:

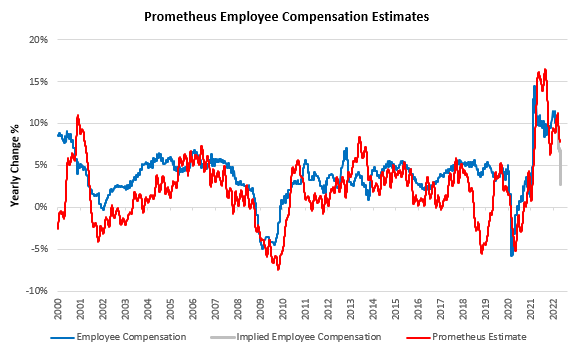

Above, our system highlights periods when two factors coincide: when labor markets are tight and inflation is elevated relative to income growth. As we can see, these tend to be periods of decelerating income and spending growth. We are in one of these periods today, and it is highly likely that as pressures build, we will move into negative income growth territory. We offer more real-time insight into the current dynamics by showing our high-frequency employee compensation estimate:

As we can see above, our high-frequency estimate implies a significant deterioration in employee compensation. The most recent official data is as of May, and our high-frequency estimate gives us some insight into the path for data to come. Again, our systems tell us there is more deceleration to come, and continues to position our systematic strategies accordingly.

ii. Liquidity tightening is just beginning, and we can see it in markets and the real economy. We define liquidity as the stock of high-quality, liquid assets that potentiate economic and market activity. The largest liquidity creator is the US sovereign, which comprises the aggregate fiscal and monetary authorities. As we have seen over the COVID-19 period, the US sovereign has a powerful ability to drive economic and market activity. After a joint effort by the Federal Reserve and US Treasury to stimulate economic activity, they have both moved to remove their monetary accommodation. We are seeing the outsized effect of this liquidity drain in both financial markets and the real economy. The Federal Reserve is reducing the available reserve balances and tightening financial conditions in financial markets. We wrote about this in-depth, and you can click here to review it.

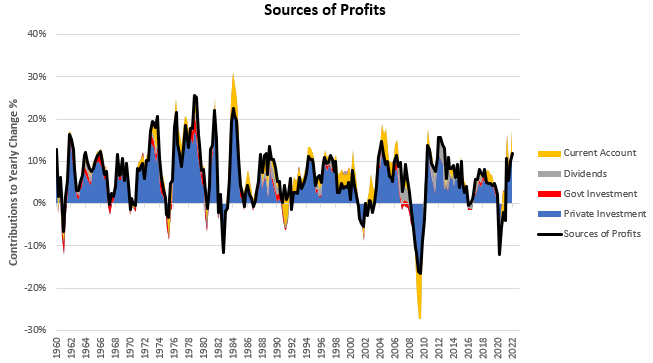

In the real economy, the withdrawal of the fiscal impulse continues to weigh on the private sector and is highly likely to drag on profitability. Profitability is a residual accumulated by businesses, resulting from the sources of profitability remaining in excess of uses of profitability. Below, we show the sources of business profits:

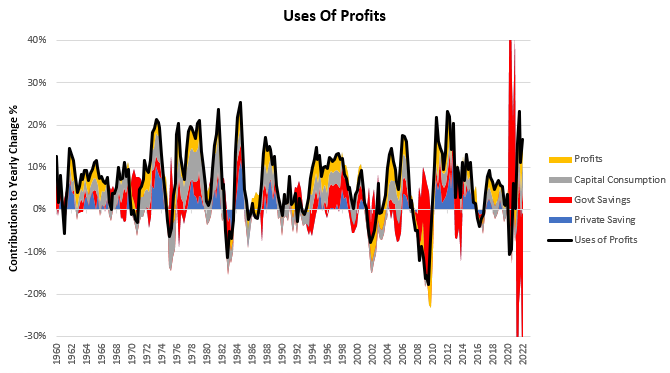

The largest source of earnings for the business sector has historically been a private investment which has remained relatively healthy in nominal terms. However, when we turn to the uses (or drains) of profits, we see a significant headwind emerging:

Government savings are a drain on corporate profits, i.e., when the government deficit spends, it creates a greater chance of business profitability unless offset by other variables. During the COVID-19 crisis, the US government spent vast amounts on the real economy, creating a spike in profitability. However, as the US government now more to reduce its deficits, as it did in Q1, this tailwind has now turned into a considerable headwind. Therefore, while businesses continued to invest in Q1 2022, the offsetting demand crunch from reduced fiscal largesse resulted in negative corporate profit growth. With earnings already on a downward trajectory, the cost of capital rising, and US policymakers taking a much more moderate approach to fiscal policy, there remains significant pressure on corporate profitability, once again boding ill for equities.

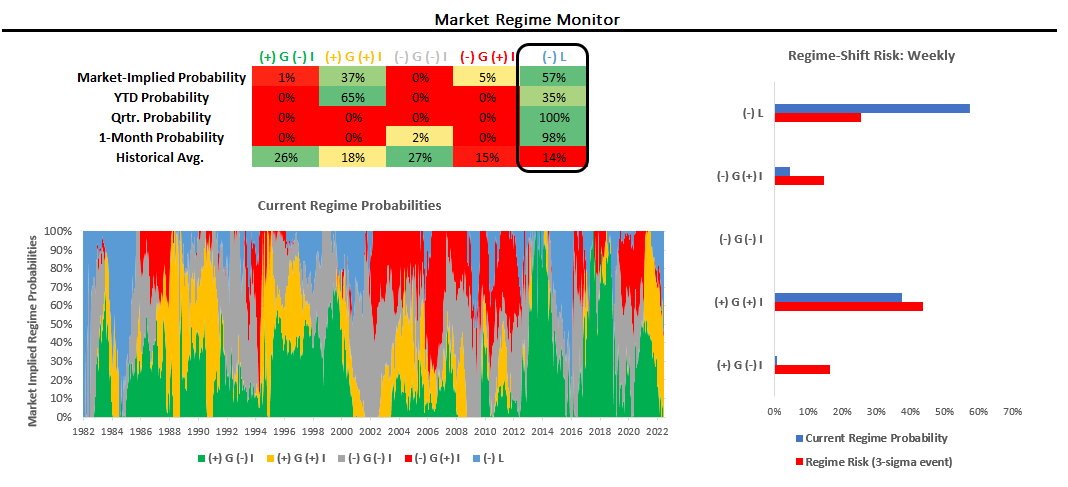

iii. Markets are pricing tightening liquidity with a growing deflationary tilt. Over the last quarter, our market regime monitors have moved to price the dominance of tightening liquidity conditions as the driver of markets. However, deflationary pricing has become more dominant over the last few weeks. Our systems have yet to show meaningful pricing of this deflationary market regime across durations. However, it is crucial to note these nascent market dynamics, as tightening liquidity conditions often lead to deflationary conditions.

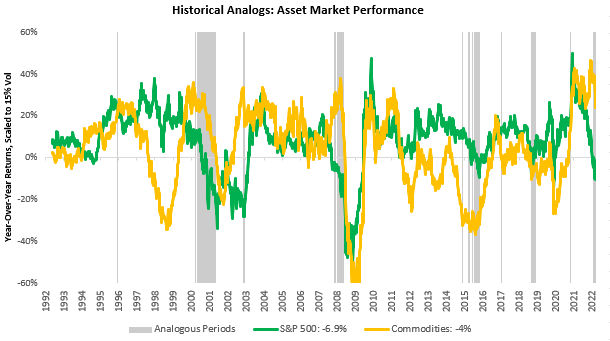

Our system looks for comparable periods in time based on growth, inflation, liquidity, and the market environment to estimate what kind of returns we can expect from different asset classes today. We show below that our analog finder now tells us that both Equities and Commodities typically have negative returns in environments similar to today:

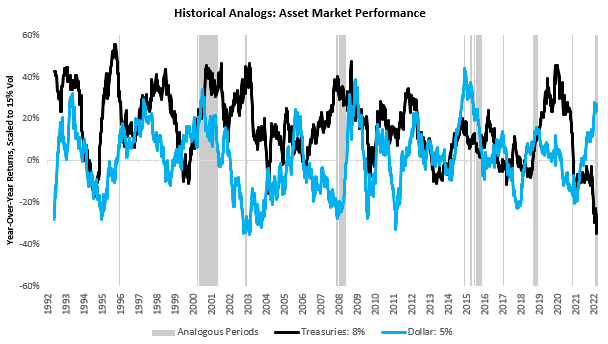

Conversely, the Dollar and Treasuries tend to benefit from an environment such as today:

We are in the early stages of a turning point in the market cycle, and as we have stressed, this is a time for capital preservation above all else. Tightening liquidity in markets and the real economy sow the seeds for deflationary pressures. Our systems account for current economic data, market environments, and historical analogs and are now telling us there is strong potential for a market turning point. After a tremendously negative period, Treasuries may again begin to perform as a risk-off asset. Our systems have now positioned neutrally in Treasuries heading into next week. Before we discuss positions, let US look at the data calendar:

Monday: US HolidayTuesday: Manufacturer’s New Orders

Wednesday: MBA Mortgage Application, S&P PMIs (Services + Composite), ISM Services PMI, JOLTS Job Openings

Thursday: Trade Balance, Jobless Claims

Friday: Payrolls, Unemployment Rates, Average Hourly Wage Data, Wholesale Inventories & Trade, Consumer Credit

Our systems expect PMI data to continue to deteriorate. We will be watching New Orders data to understand the composition of demand pressures. Jobless claims are likely to continue on their trajectory of coming in higher than expected, but as we have explained, we expect labor market deterioration to be one of the last signs of the current slowdown.

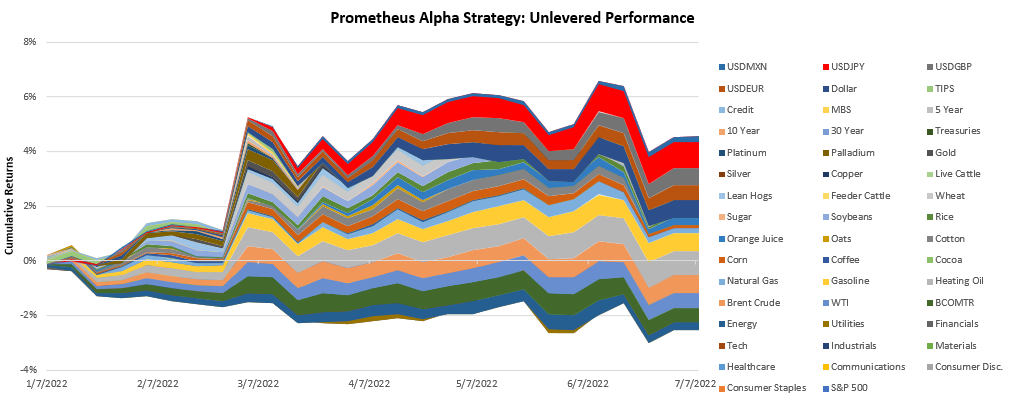

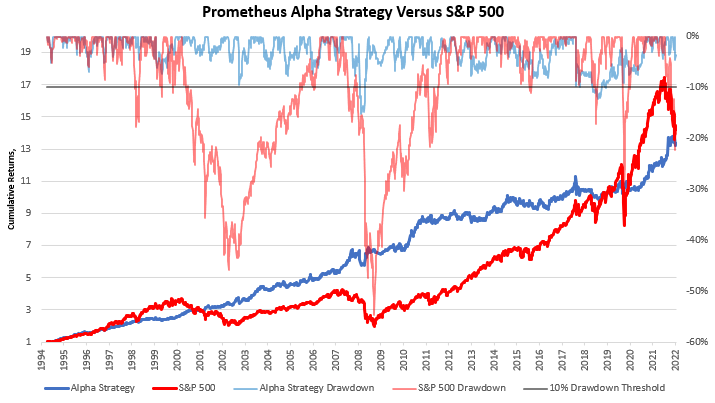

Turn to our Alpha Strategy; we have continued to see strong performance this year, despite some losses in the week before last:

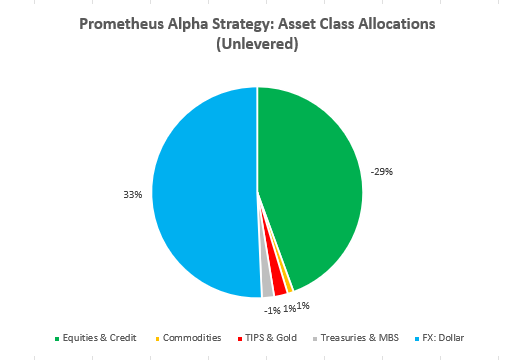

Heading into next week, our systems have taken into account changing regime dynamics and have now moved to be neutral across Treasuries & Commodities, but remain aggressively short Equities, & Credit, in addition to being long the Dollar:

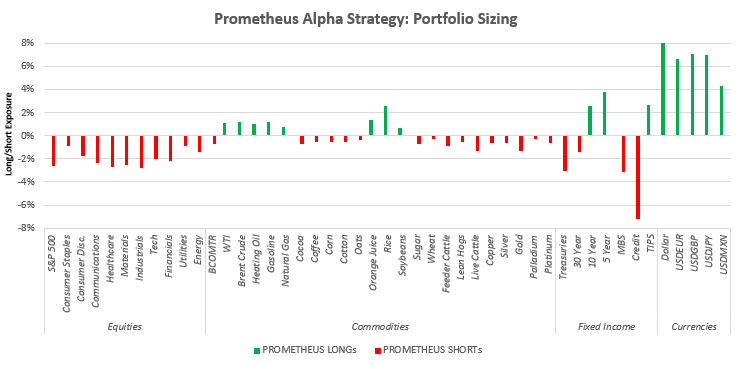

We show these allocations at the security level:

These positions place our net exposure at a near-neutral position of approximately 5% net-long. We are in the early stages of tightening liquidity, creating deflationary conditions, and making Treasuries look increasingly attractive. However, our systems are moving incrementally to add Treasuries as we need further disinflation to confirm bigger bets on fixed income duration. Our systems were built with these regimes in mind, and while they may not generate positive performance during every regime transition, they are highly likely to perform over the market cycle:

Keep market exposure low to a minimum. Stay nimble.

Disclaimer: No information provided by Prometheus is investment advice or should be construed as a solicitation for investment.