Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

If you would like to get a sense of our picture thoughts and outlook, our Founder, Aahan Menon, recently hosted a Twitter space with @RosannaInvests. Make sure to give it listen if you’re trying to get caught up on our views! Click below to listen on Twitter:

Let’s dive into today’s note. In brief:

-

PMIs showed mixed readings, but the trend remains decelerating.

-

Nominal retail sales came in higher than consensus expectations, but real retail sales are contracting.

-

Industrial production weakened in August and is likely the first sign of slower output.

The combination of these factors brings us one step closer to outright stagflation. We discuss this and more below.

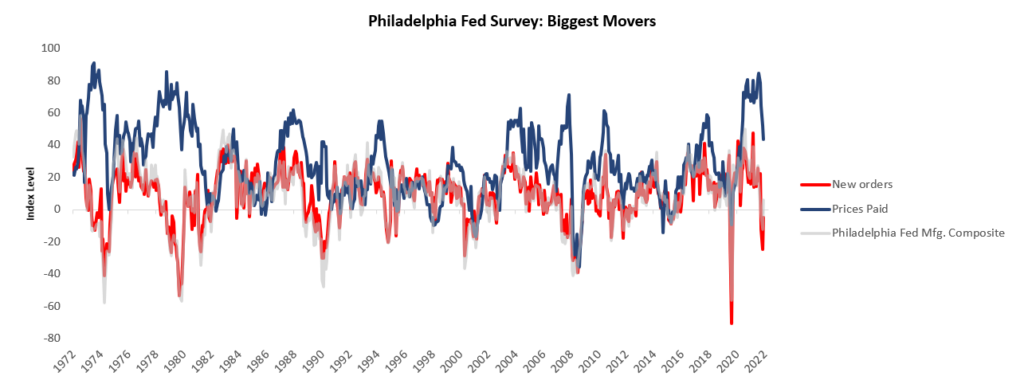

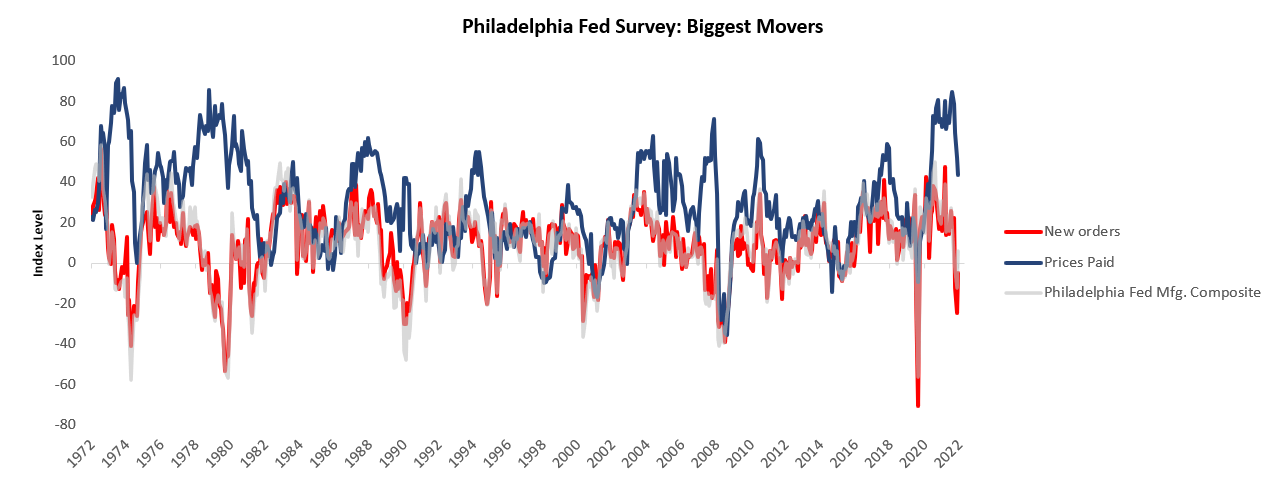

i. PMIs showed mixed readings, but the trend remains decelerating. Today’s PMI data from Philadephia & New York painted opposing sequential pictures- albeit with both remaining in contractionary territory, with Philadelphia surveys indicating significantly weaker manufacturing activity, while New York Fed PMIs improved sequentially (though they remain in contractionary territory. Philadelphia Fed manufacturing survey data showed a contractionary reading of -9.9, disappointing consensus expectations of 2.25. This reading was a sequential deceleration within a decelerating trend. The largest gaining segment was Prices Paid, and the most significant slowdown was in Unfilled Orders. We show these below:

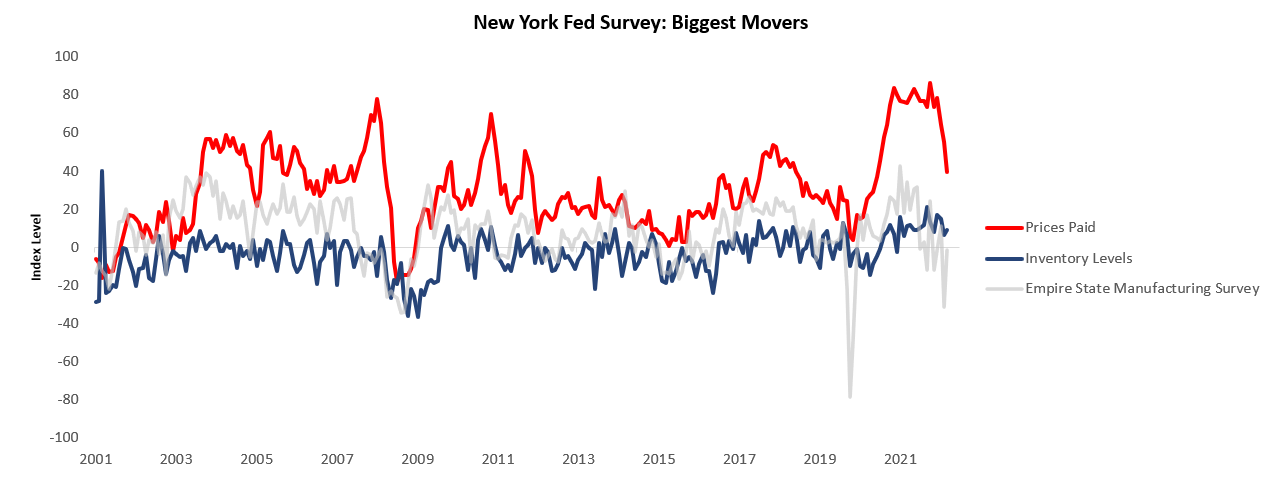

On the other hand, the latest New York Fed manufacturing survey data showed a contractionary reading of -1.5, surprising consensus expectations of -12.9. This reading was a sequential acceleration within an accelerating trend. The largest gaining segment was Prices Paid, and the most significant slowdown was in Unfilled Orders. We show these items below:

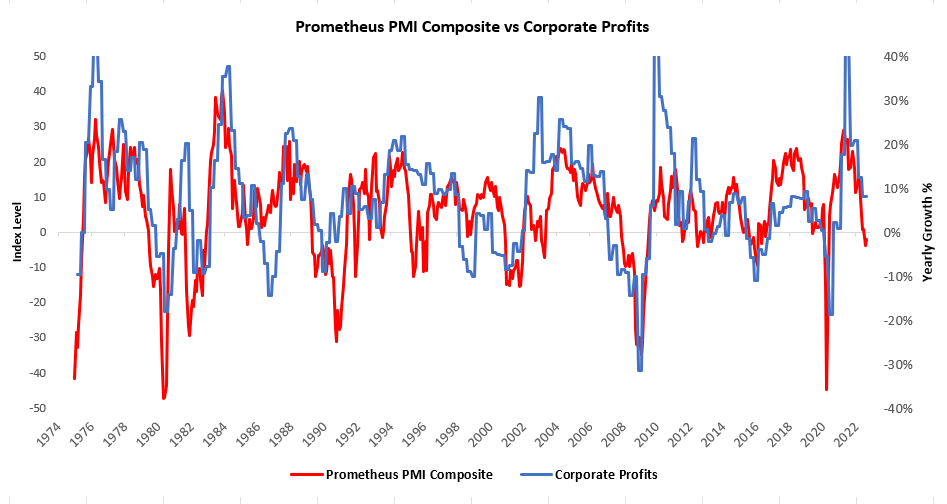

Therefore, while there may seem to be some mixed messaging on the sequential evolution of the data, we continue to see a broad-based trend lower in our PMI Composite, which aggregates all US PMIs. PMIs offer us good insight into the marginal changes in demand and supply dynamics for businesses and provide us incremental information on the trajectory of the profits cycle. Our PMI Composite continues to paint a bleak picture for corporate profits:

A weakening profit outlook is not one during which equities are well supported; therefore, our systems expect equities to continue floundering.

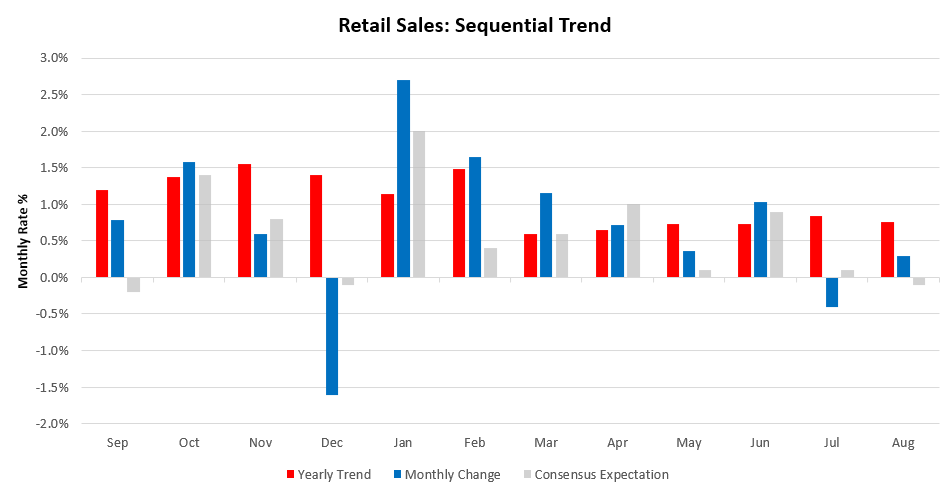

ii. Nominal retail sales came in higher than consensus expectations, but real retail sales are contracting. We continue to be in an environment of elevated nominal growth but with increasingly deteriorating real growth. Retail Sales increased 0.29% in August, surprising consensus expectations of -0.1%. This print contributed to a sequential deceleration in the quarterly trend relative to the yearly trend. Below, we show the monthly evolution of the data relative to its 12-monthly trend and consensus expectations:

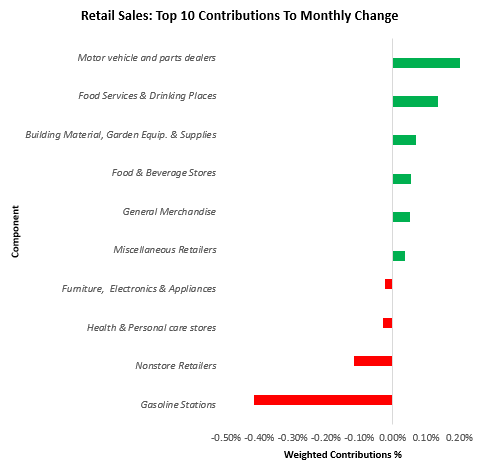

What’s more, a significant number of industries actually saw contractions in their nominal sales:

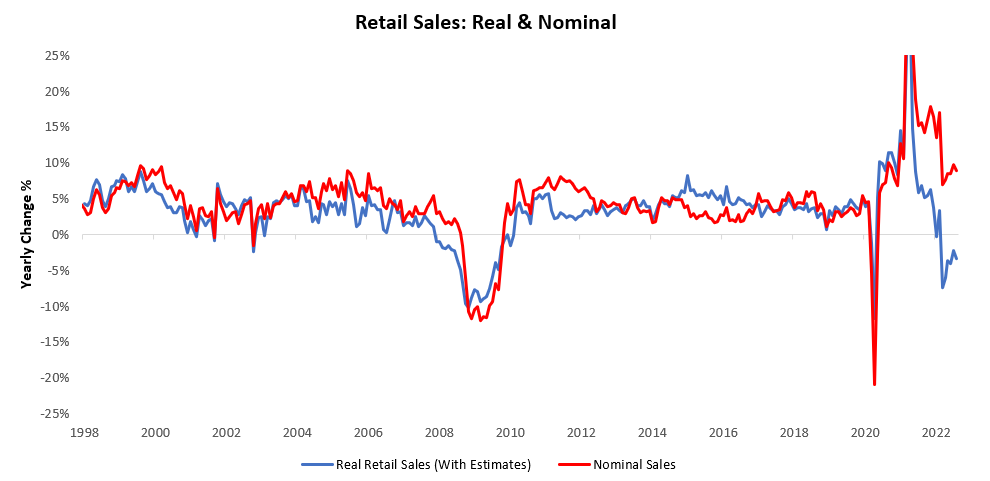

Therefore, while it is evident that real demand is weakening, these are initial signs that nominal demand will weaken as well. However, with nominal demand many multiples ahead of real spending, we are increasingly likely to enter stagflation, i.e., contractionary growth with high inflation. By our estimates, we’re already seeing this in retail sales data. While nominal retail sales increased by 0.3%, real retail sales contracted by -0.2% in August, resulting in a yearly change of -3.4% yearly compared to the prior year. Said differently, inflation is now contributing to more than 100% of nominal retail sales growth. We show nominal and real retail sales below:

With real demand weakening, we see an increasing likelihood that there will be pressure to reduce both output and employment, and today’s industrial production data offered us incremental insight that we are indeed on this path. We will discuss this next.

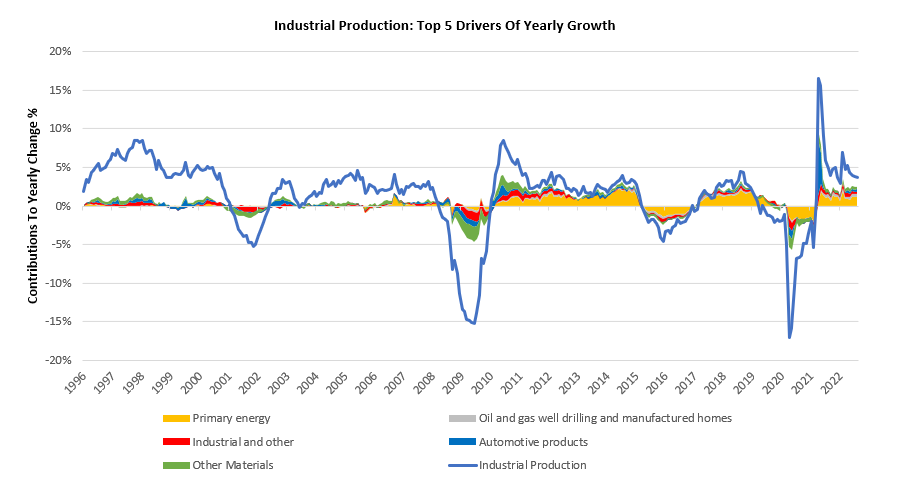

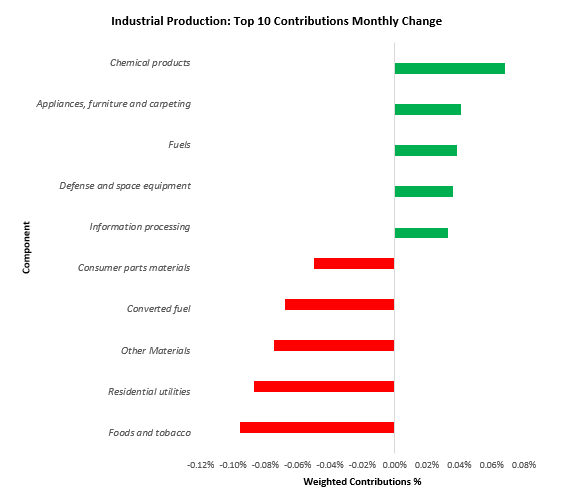

iii. Industrial production weakened in August and is likely the first sign of slower output. Real manufacturing orders are contracting, inventories elevated versus sales, and real incomes & spending are flirting with contractionary territory. The combination of these factors creates pressure on both production and employment, and we saw the first signs of weakness in industrial production in today’s data. Industrial Production decreased -0.16% in August, disappointing consensus expectations of 0%. This print contributed to a sequential deceleration in the quarterly trend relative to the yearly trend. We show the top 5 drivers of industrial production along with the headline data below:

Of particular note is the significant contraction we saw in multiple components of industrial production. Below, we highlight the primary drivers of industrial production growth:

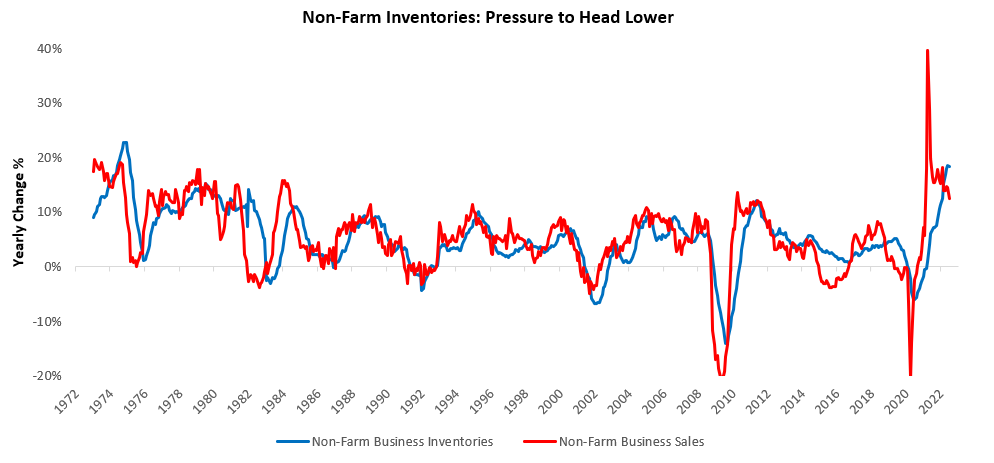

As we have shown in the past, production is now finding its way into inventory build, with inventory growth outpacing sales growth:

However, there are physical limitations on inventory build for businesses, as there is only so much physical capacity to stock inventories. With no abatement in the pressures on real incomes, the likely resolution of these dynamics will probably be through lower output. These dynamics are likely create self-reinforcing pressures for the real economy to contract amidst high nominal activity. This week’s data moves us one stage closer to outright stagflation. In preparation for a shift to outright stagflation, or perhaps even a continuation of stagflationary nominal growth we have conducted a significant amount of research to prepare ourselves and our clients. We summarised how we think investors need to think about these times in yesterday’s note, and highly recommend you read it if you haven’t:

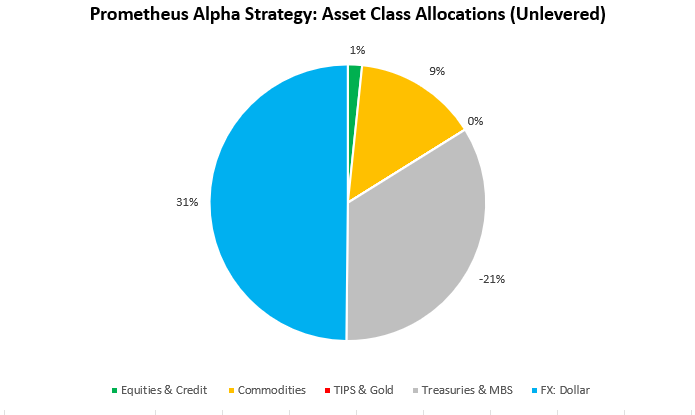

Aside from these bigger-picture thoughts, our current positioning remains in line with these dynamicsstaying long the dollar, short treasuries, neutral on equities, and modestly long commodities. We show our systematic portfolio allocations at the asset class level for next week below:

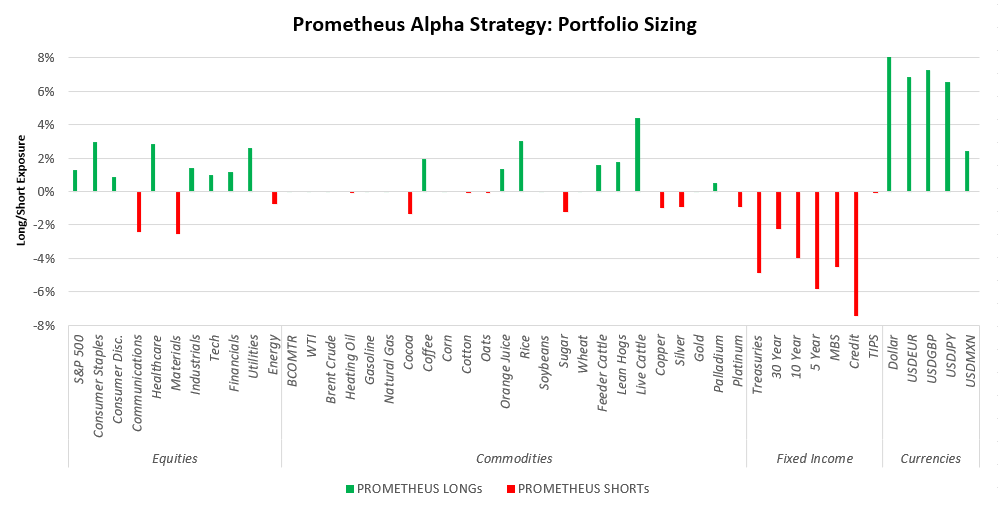

We drill down to the security level below:

Capital preservation remains the key to future compounding. Stay nimble.

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.