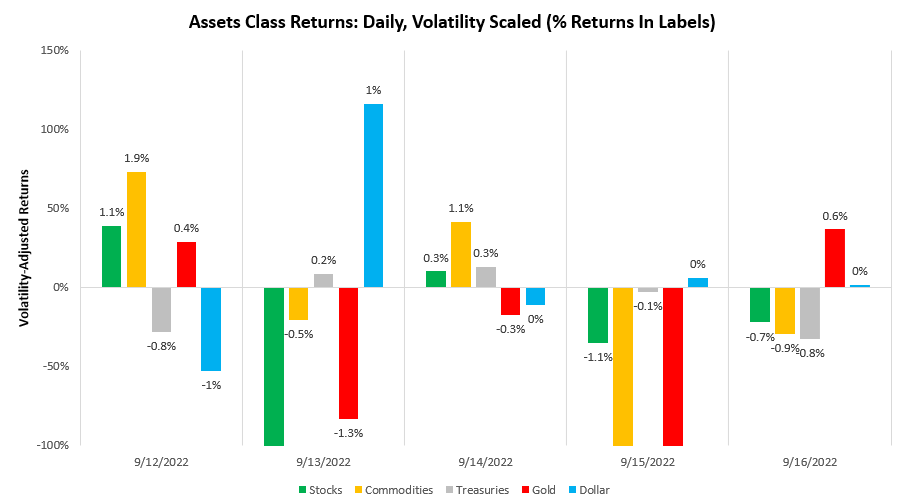

Last week proved a good one for our systematic strategies, with markets moving to price a tighter Fed on the back of a higher-than-expected CPI report. Below, we show the path of asset market returns over the last week:

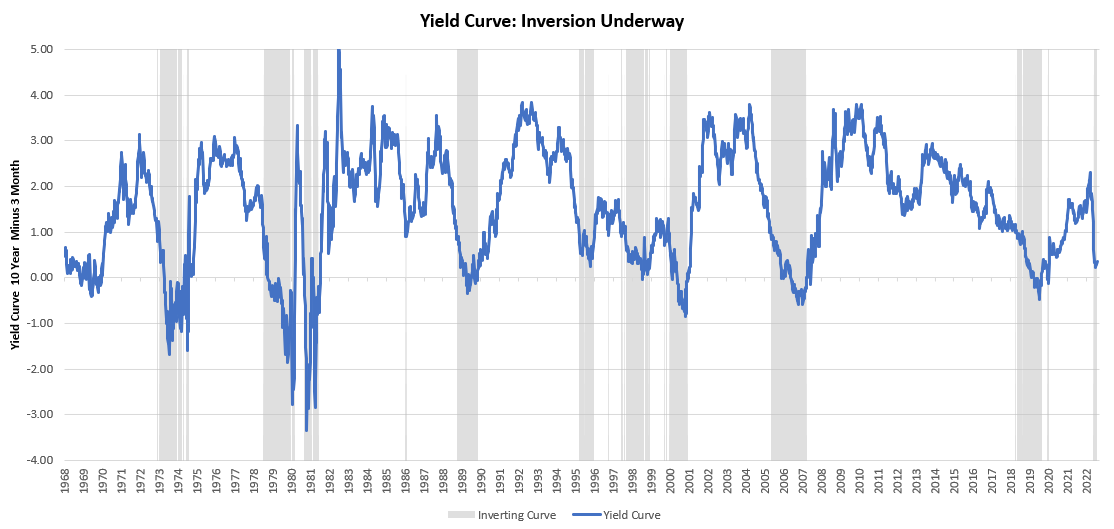

Equities and treasuries suffered last week as persistent inflation pressures led markets to discount a tighter path for policy rates. These forces continue to push the yield curve towards inversion, creating a difficult backdrop for the economy:

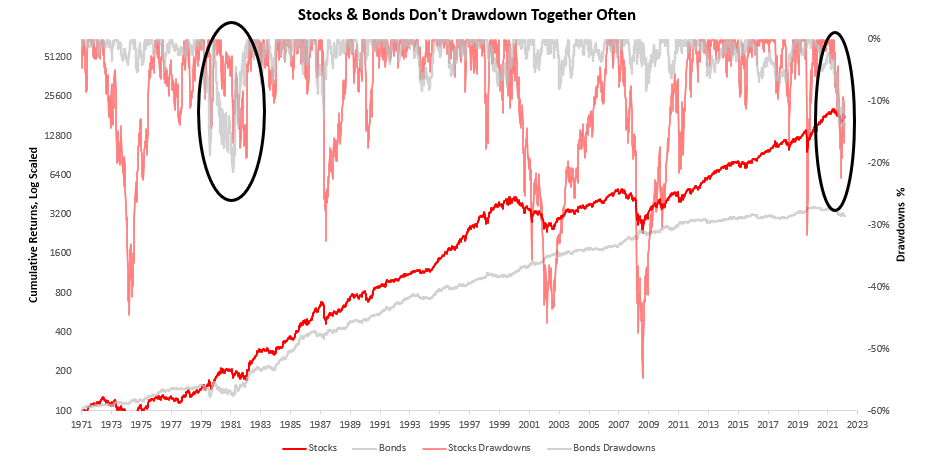

Our systems continue to flag that the yield curve is on the path to inversion and has been so since July. Yield curve inversion is challenging for both the economy and markets, as it erodes the time value of money, i.e., disincentivizes capital formation in the economy. This is because yield curve inversion puts pressure on all long-duration yields relative to cash, disincentivizing long-term lending. This dynamic is usually unsustainable unless it is underwritten by the government (yield curve control). However, these periods can be excruciating for the private sector, as the yield on cash compresses all forward-looking excess returns over cash. The result is the sell-off that we have seen in both stocks and bonds over this year, with both showing significant and simultaneous drawdowns:

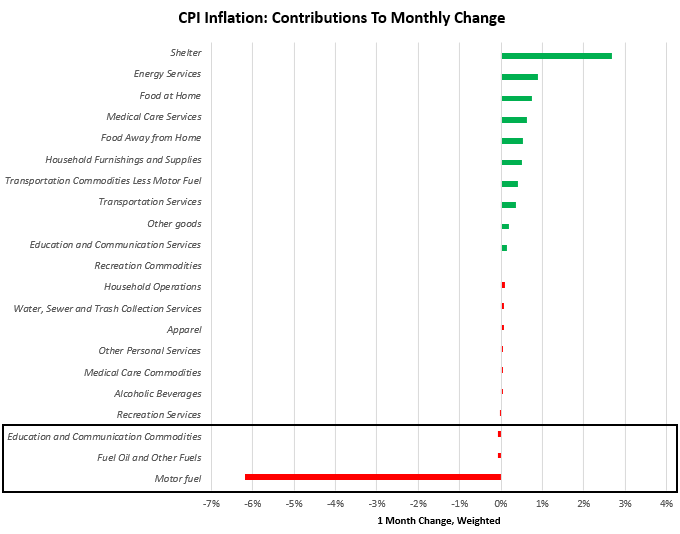

These dynamics are being driven by an environment of stagflationary nominal growth and tightening liquidity, and we increasingly see the possibility of a transition to outright stagflation. The pressures remain entrenched and continue to be building in this direction. As we have said in the recent past, the future of inflation will be determined by the balance between the commodities impulse and the trend in services inflation. In the most recent CPI print, we received information that showed us that despite extreme downwards pressures coming from energy prices, headline CPI remained in expansionary territory. We offer the composition of this print below:

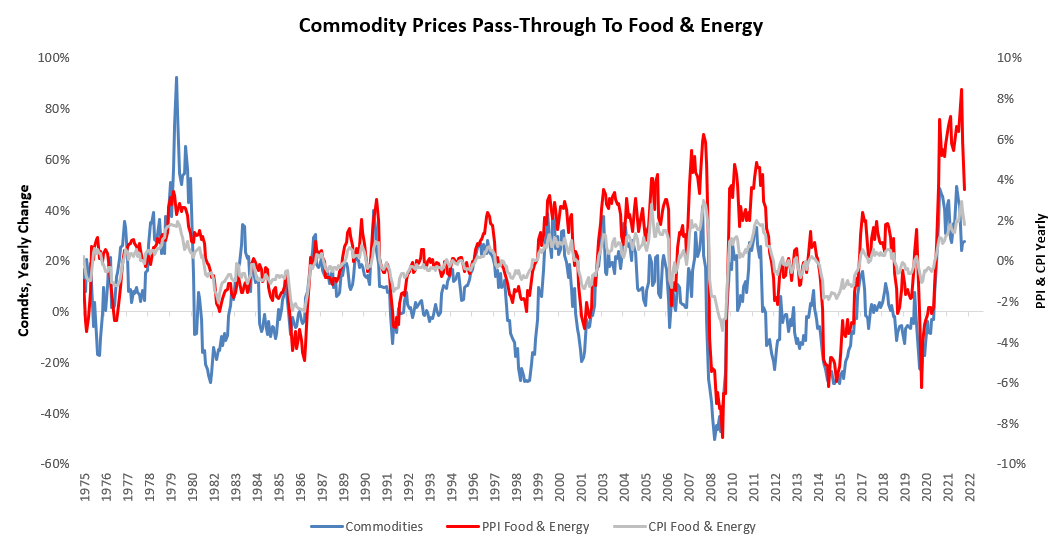

The above tells us that there is a widening of inflationary pressures, enough to offset commodity disinflation. Furthermore, there is likely to be a timing mismatch between the two. The inflationary process begins with the demand for commodities and other real assets and goes through the supply chain to the consumer. Food and energy price shocks can be transmitted to the consumer fairly quickly (one to two months, by our estimates), but commodity shocks take more time to make their way into service prices. Below we show commodities and food & energy prices tend to coincide:

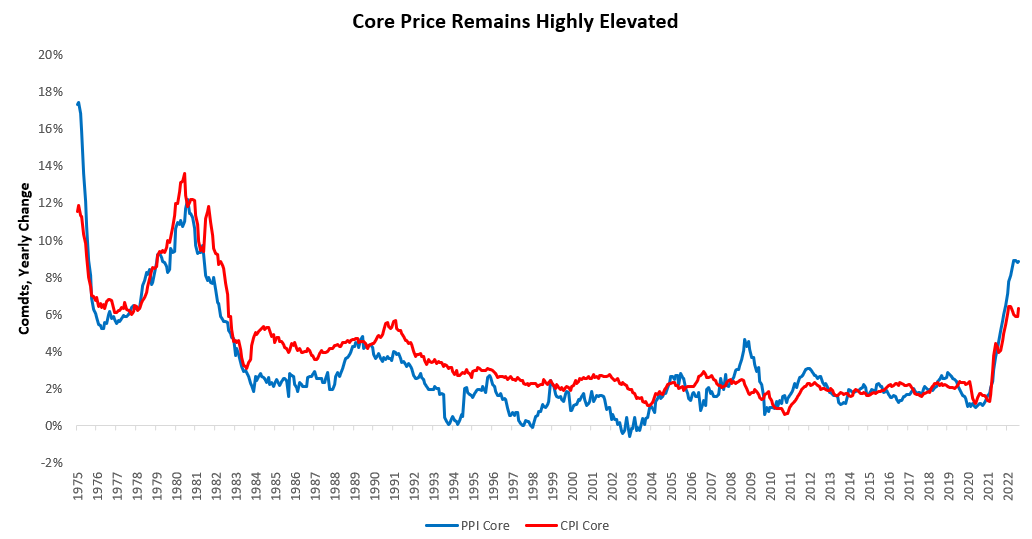

In contrast with food and energy, core CPI & PPI are more persistent due to their significant service components. These items reflect contractual obligations that are “marked-to-market” far less than commodity prices. Therefore, as we move further up the supply chain, prices tend to follow stable trajectories, i.e., they are autocorrelated:

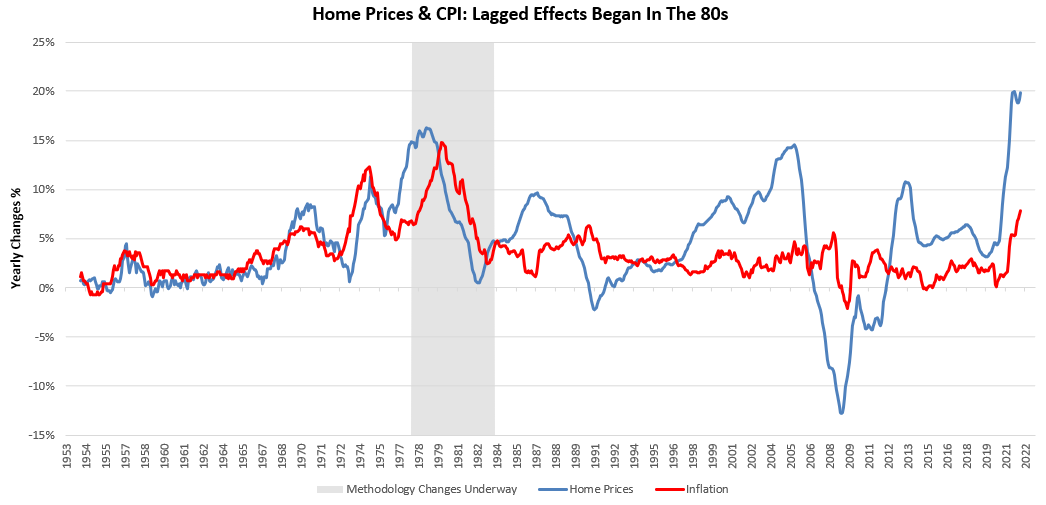

These components continue to suggest sustained and entrenched inflationary pressures. Furthermore, we will likely see further support for core CPI from housing prices. In 1984, the government changed their CPI calculations to reflect rents rather than house prices to capture consumer costs better they did so by creating an item called owners’ equivalent rent, which estimates what homeowners would charge were they to rent their homes. However, their methodology included a smoothing process, which resulted in perceived rents (i.e., home prices) passing into CPI with a lag of approximately 20 months. We show this below:

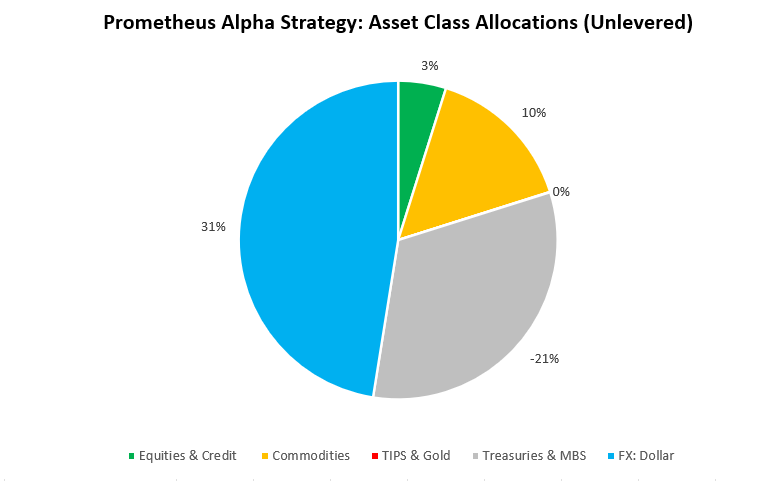

Therefore, even if home prices fell dramatically in the coming months, the methodology would not fully reflect those changes for six to eighteen months. These insights and a multitude of data we received last week continue to tell us that we remain on the trajectory toward stagflation. Resultantly, our positioning roughly remains the same:

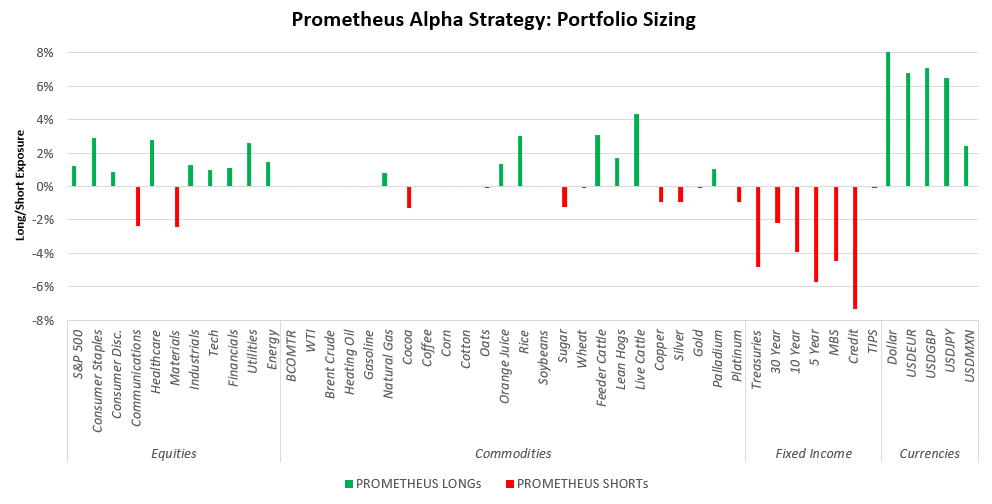

We show our positions at the security level below:

We maintain these positions in the context of the upcoming week in data:

-

Monday: NAHB Housing Index

-

Tuesday: Building Permits, Housing Starts

-

Wednesday: MBA Mortgage Applications, Existing Home Sales, FOMC

-

Thursday: Current Account Balance (Q2), Jobless Claims, Kansas Fed PMI

-

Friday: S&P Mfg. & Svcs PMIs.

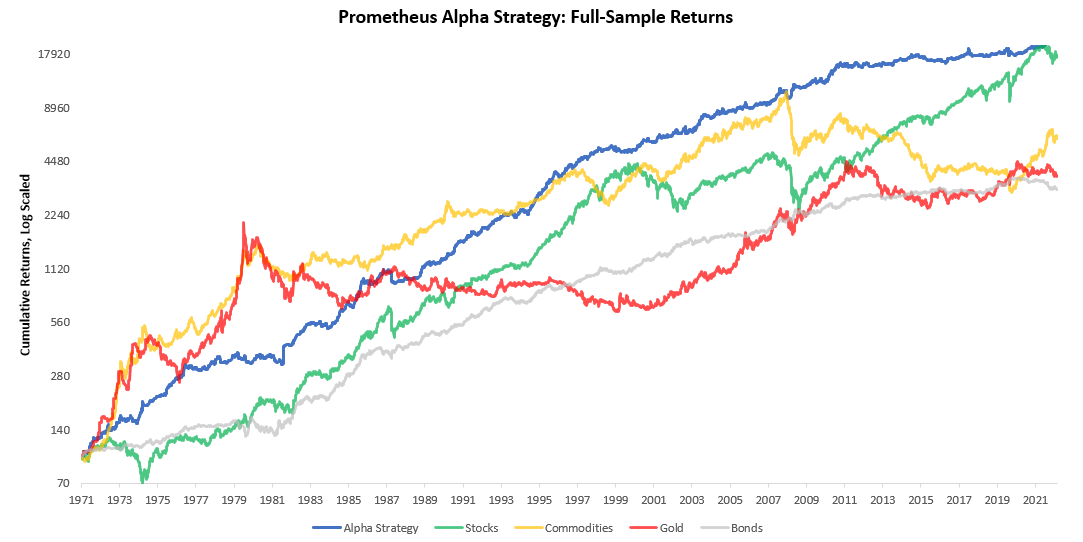

This week, the FOMC meeting will be of particular importance, with markets pricing in a high probability of a 75 basis point hike. We expect the Fed to raise rates in line with this consensus expectation, and we think the primary risk to our positioning will be Powell’s press conference. However, we think the balance of probability remains tilted towards Powell remaining on the hawkish side/in-line with expectations, particularly in light of the most recent inflation data. The Fed is attempting to cause a contraction in nominal demand through weaker financial conditions dovish messaging at this junction would be grossly at odds with their objectives. Nonetheless, we will monitor developments closely. Regardless of the FOMC next week, we remain on a path to stagflation and our systems are well prepared for this potential transition. Furthermore, expect our approach to perform well regardless of whether we move into stagflation or not. However, the key is that we are well-equipped to deal with stagflationary nominal growth or even outright stagflation. We show the full-sample backtests for our Alpha Strategy below:

Stay nimble.