Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

If you would like to get a sense of our picture thoughts and outlook, our Founder, Aahan Menon, recently hosted a Twitter space with @RosannaInvests. Make sure to give it listen if you’re trying to get caught up on our views! Click below to listen on Twitter:

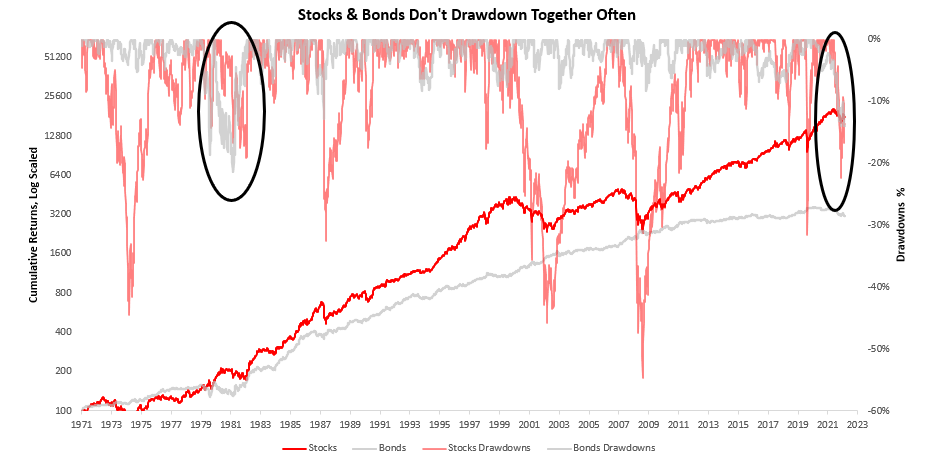

Today, we’ll take a step back from our granular tracking to address the bigger picture for asset allocation, as we think it is one of the most undercovered aspects of the current investment landscape. We’re currently in one of the most challenging environments for risk assets on record, with stocks and bonds experiencing losses from their highs. Below, we show how unusual it is for stock and bond losses to coincide this way, from 1971 to the present.

As we can see above, these periods are indeed anomalous and create a challenging environment for most traditional investorswho mostly have allocations to just stocks and bonds. Over the last 40 years, this conventional approach has served investors well as stocks and bonds have both been supported by a secular decline in interest rates, which we show below along with our estimates of the market-implied regime:

Market movements over time reflect the underlying demand and supply dynamics in the economy. Using our understanding of this pricing, we can extract information about what markets are telling us about the current economic environment, i.e., the market regime. Based on our regime recognition, we can be in one of 5 regimes:

-

(+) G (-) I: Rising Real Growth, Falling Inflation

-

(+) G (+) I: Rising Real Growth, Rising Inflation

-

(-) G (-) I: Falling Real Growth, Falling Inflation

-

(-) G (+) I: Falling Real Growth, Rising Inflation

-

(-) L: Tightening Liquidity

In reality, we can be in 8 different regimes based on the various permutations of growth, inflation, & liquidity. However, we compress the tightening liquidity environments into one regime to show the dramatic impact of tightening liquidity conditions on markets.

It is pertinent to note that since 1984, markets have spent 65% of their time pricing in falling inflation an environment beneficial to both stocks and bonds. Stocks and bonds have opposing growth biases, i.e., stocks prefer environments where growth rises because earnings stay healthy. In contrast, bonds outperform when their fixed cashflows look relatively attractive, i.e., when growth falters. Thus, stocks and bonds have been extremely good diversifiers. However, while stocks and bonds have opposing growth biases, they have the same inflation bias they need stable inflation to perform well. Therefore, when inflation becomes a dominant force in the economy, stocks and bonds perform poorly, both individually and together in a portfolio.

To show periods where inflation is a dominant force in the economy, we offer below our real GDP Nowcast, overlaid with CPI inflation giving us a sense of the composition of nominal growth:

Additionally, we highlight periods of stagflationary nominal growth, i.e., periods where nominal growth is elevated, but the real growth is meager relative to inflation. As we can see, were are in one of these periods today, and we had two similar periods from 1967 to 1980. What these periods have in common with today is high nominal demand, high inflation, and rising interest rates creating a dramatically different set of outcomes for asset markets from those we have seen from 1984 to 2021. Therefore, as investors, it is essential to both understand how assets behave in this environment and test your strategies within these subsamples.

To illustrate the differences in asset class performance, we divide the history of the data into two periods to display the diametrically opposing market impacts of two secular environmentsStagflationary Nominal growth (1967 to 1984) and Disinflationary Real Growth from (1984 to 2022):

We can see that relative asset class performance during these periods differed dramatically. During stagflationary nominal growth, commodities and gold performed exceptionally well. From 1967 to 1980 (the first peak in interest rates), equities & bonds returned 2% and 5%, respectively, whereas commodities and gold returned 25% each. In contrast, during disinflationary real growth, stocks & bonds returned 10% and 7%, while commodities and gold returned 5% and 6%, respectively.

What we hope to make evident with the above visualization and numbers is that the returns on stocks and bonds that most investors are used to are not features of the asset classes but rather a feature of the economic environment.

To help investors further prepare for the risks these environments bring, we show our proprietary estimates for expected returns below. Periods of stagflationary nominal growth fall under (+) G (+) I, and our expected returns should serve as a good starting point in assessing the relative returns of securities within this regime:

As we can see above, the expected returns during (+) G (+) I are quite different from those during either of the (-) I regimes. Therefore, when considering investment strategies, we must be cognizant of the risks we are taking by allocating based on what has worked in the recent past. While our Alpha Strategy was constructed with all these environments in mind, our backtest history was relatively limited. It relied less on historical precedent and more on mechanical rigor to perform well in such environments. However, we have now extended our strategy lookback to test whether our Alpha Strategy could perform during these periods.

We begin by showing the Alpha Strategy during disinflationary rising growth:

As we can see above, equities outpaced our Alpha Strategy during this period. However, this was not a function of better risk-reward characteristics in equities but rather due to higher volatility taken on by equities. On a volatility-matched basis, the picture is dramatically different. Nonetheless, our Alpha Strategy targets a 10% volatility, and we report it as such.

Next, we show our Alpha Strategy during stagflationary nominal growth:

Much like during disinflationary real growth, our Alpha Strategy performs well but falls just behind the leading asset in the regime- commodities. Again, this is largely a function of higher volatility in commodities than our Alpha Strategy. Therefore, our Alpha Strategy has not been the optimal allocation in either disinflationary real growth or stagflationary nominal growth. However, unlike the major asset classes, our Alpha Strategy performs well in both environments. Resultantly, while our Alpha Strategy approach was not optimal in any one environment, it was a better performer than asset classes across environments. We show the full-sample history of the cumulative return series below:

Therefore, we expect our approach to perform well regardless of whether we move into stagflation or not. However, the key is that we are well-equipped to deal with stagflationary nominal growth or even outright stagflation. The purpose of sharing these return series is not to provide any false sense of certainty about the future or to ex-post make claims about performance. The purpose of this exercise is for us to share our internal preparation for an environment that is dramatically different from the recent past and share with our readers the potential outcomes based on historical analog. Therefore, we remain confident that we will be able to help our subscribers and clients adequately navigate today’s environment of stagflationary nominal growth and an eventual transition to outright stagflation. Stay nimble.

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.