Over this week, we will migrate all our publishing to our new website. Please make sure to subscribe below here if you haven’t already, as we will be transferring all our mailing lists to the new website. You can check it out here.

Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios. We also just released our latest Month In Macro note, which over 45 pages, explains our current assessment of economic and market conditions. You can read it here:

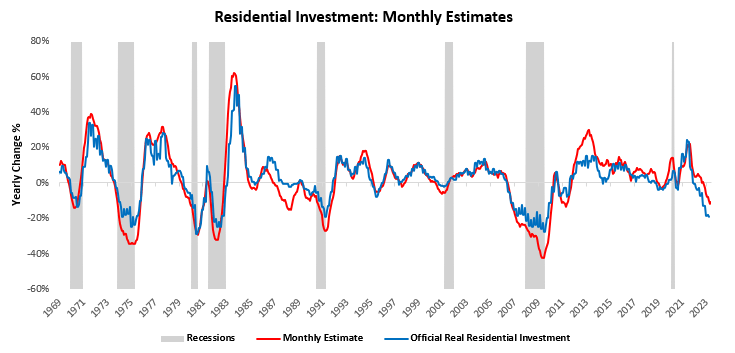

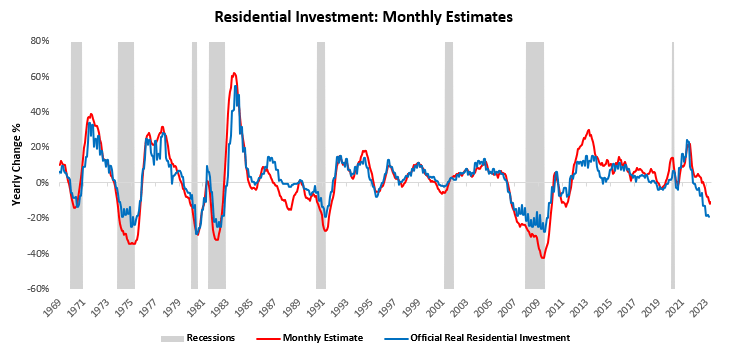

Today, we assess the latest information coming from the residential real estate sector. The latest information has shown a marginal improvement in our tracking of real residential investment within a broader contraction. At best, we currently estimate that real residential investment has increased by approximately 0.8% over the last quarter. Overall, the data show sequential improvement within cyclical weakness. Let’s dive in.

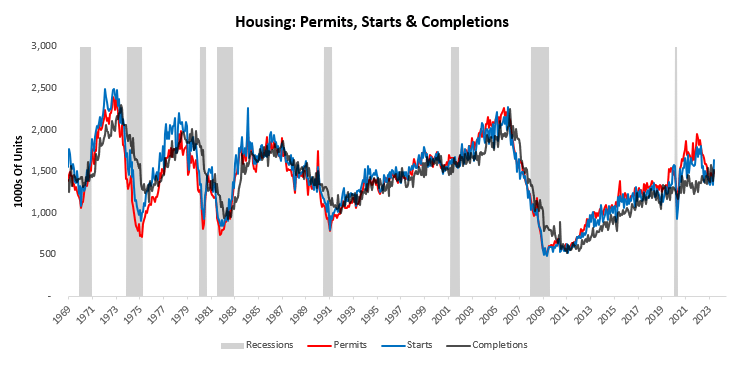

The latest data for May showed housing permits increased by 5.22%, housing starts increased by 21.72%, and housing completions increased by 9.52%. Below, we show the current levels for the same:

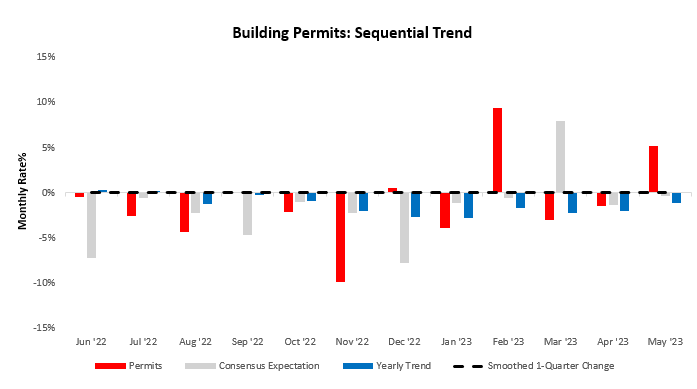

Zooming into the data, housing permits increased by 5.22%, surprising consensus expectations of -0.35%. Below, we show the sequential evolution of the data, along with the smoothed one-quarter change in the most recent data. We provide the smoothed version as monthly housing data contain significant noise.

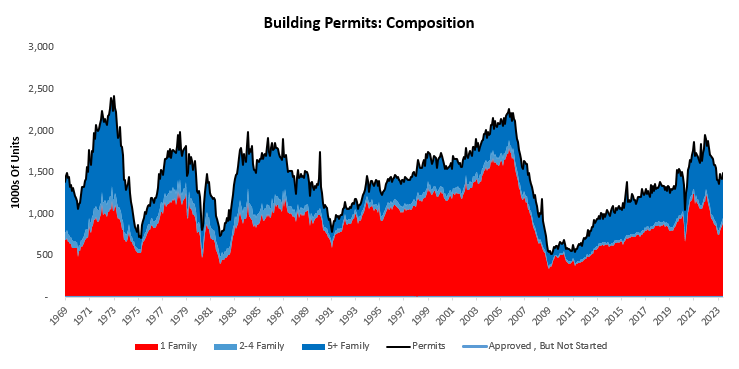

For further context, we zoom out to show the contributions from single-family homes (-136), two-family homes (-8), and multi-family homes (-73) to the fall (-217) in total permits over the last year:

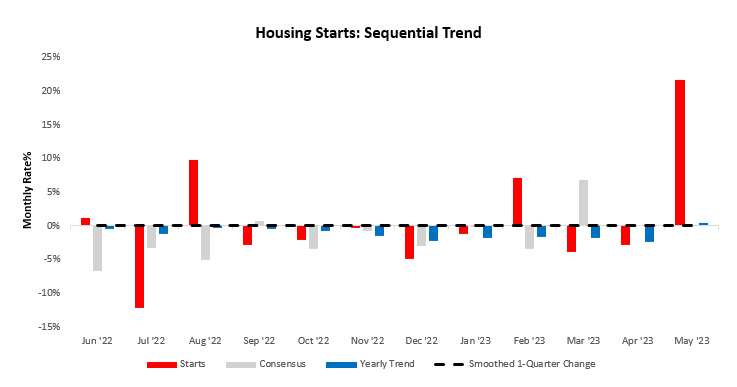

Consistent with the permits data, housing starts data showed starts increased by 21.72%, surprising consensus expectations of 0%. Below, we show the sequential evolution of the data, along with the smoothed one-quarter change in the most recent data. We provide the smoothed version as monthly housing data contain significant noise.

To illustrate the bigger picture, we show the contributions from single-family homes (156), two-family homes (-19), and multi-family homes (177) to the rise (88) in total starts over the last year:

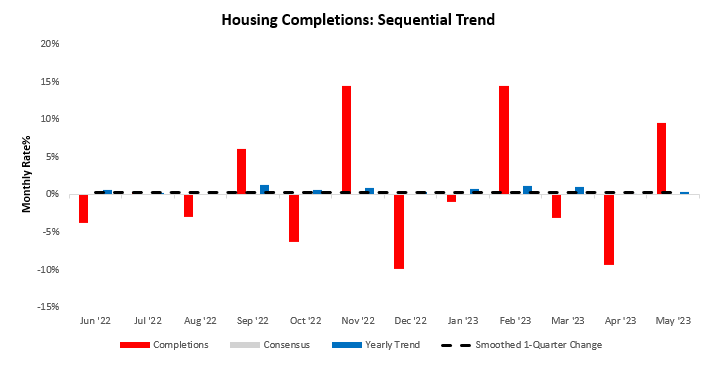

Last, in our sequential analysis, we turn to housing completions data, which showed completions increase by 9.52%. Below, we show the sequential evolution of the data, along with the smoothed one-quarter change in the most recent data. We provide the smoothed version as monthly housing data contain significant noise.

We show the contributions from single-family homes (38), two-family homes (11), and multi-family homes (95) to the rise (72) in total completions over the last year:

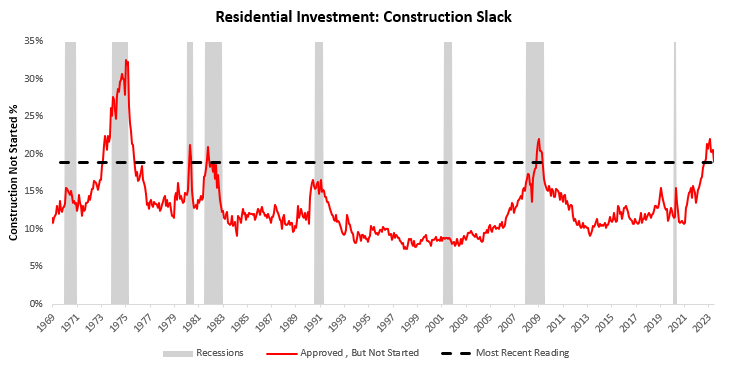

To get a better sense of where we are in the housing cycle, we examine how many construction projects have been approved but not yet started. According to the latest data, 19% of projects are yet to begin construction. Looking through history, housing-led recessions usually begin when this measure of construction slack is around 15% suggesting that we are within the ballpark of a recession.

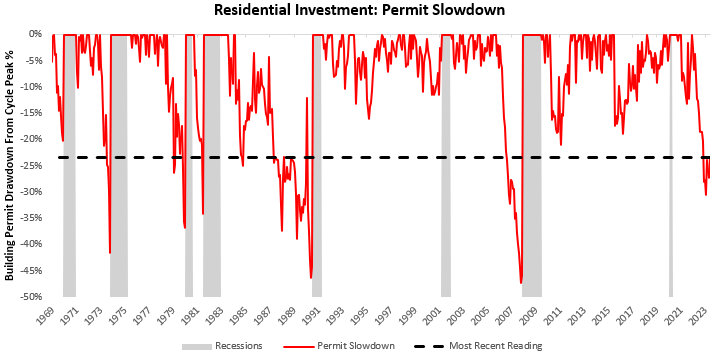

We conclude our sequential analysis by examining another measure of housing weakness, i.e., permit slowdowns- which measures how much building permits have fallen from their cycle highs. Large drops in permits bode ill for the broader residential investment complex & GDP. The latest data shows that building permits are off their cycle highs by -35%. Typically, housing-led recessions usually begin when this measure of cyclical weakness is around -35% suggesting that we are within the ballpark of a recession.

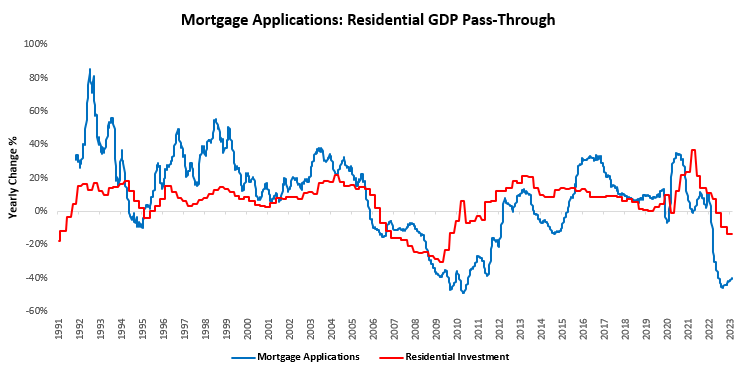

Next, we turn to the most recent data coming from mortgage applications. The latest data shows a sequential improvement in our weekly tracking of mortgage applications. Our latest estimate suggests downward pressure on mortgage borrowing and residential investment. Our latest estimates show mortgage applications down by -40.03% compared to one year prior. We present this information below:

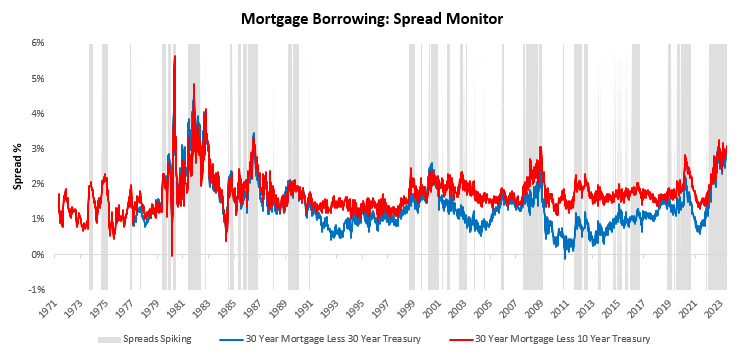

To assess the borrowing conditions driving these changes in mortgage applications, we turn to mortgage spreads. According to our measures, mortgage spreads are rising. Spreads have begun to rise since February 2022. Since then, the 30-year mortgage yield relative to 10-year Treasury yields has increased by 1.29%. Below, we present the 30-Year Mortgages relative to 10 & 30-Year Treasuries:

The combination of these various factors leads to a picture where our estimates of residential investment have sequentially improved, with the potential for a very modest one-quarter expansionary reading. While we are seeing this sequential improvement, our estimates remain depressed versus one year prior, i.e., residential investment remains weak:

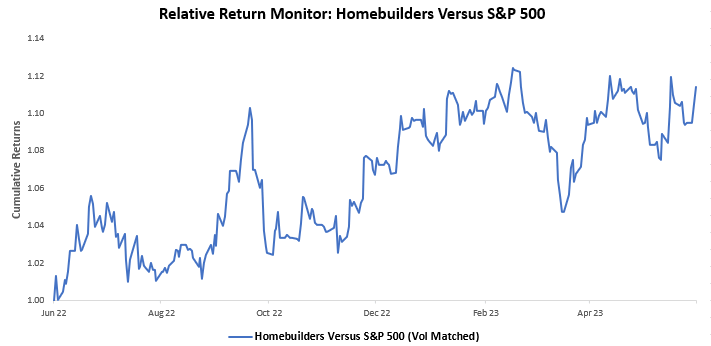

We see some of these marginal improvements priced into homebuilder stocks, which are most exposed to these improvements:

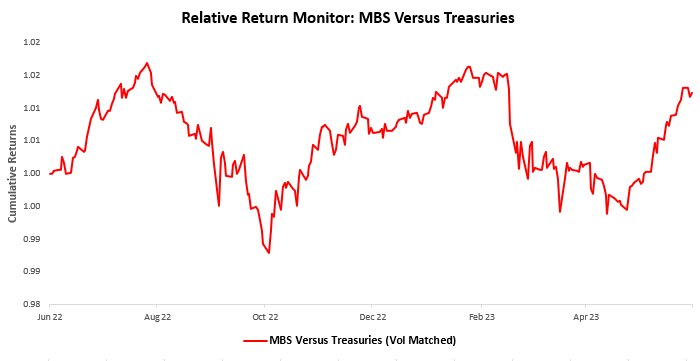

And much more modestly in MBS relative to Treasuries:

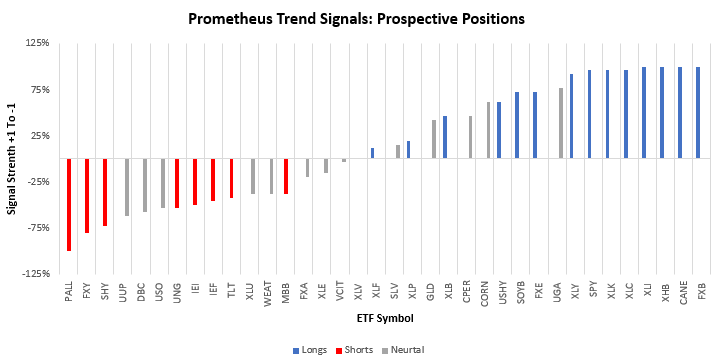

Whether this outperformance can continue largely depends on the ability of the consumer to continue to leverage current income growth into rising mortgage rates. At the same time, there remains room for residential construction to improve as some degree of building slack slows. Overall, our expectation is that the pass-through of higher rates will prevail over the course of the cycle. In the meantime, our trend signals continue to flag XHB as a potential long position and MBB as a potential short:

Until next time.

Hi there! Do you know if they make any plugins to help with SEO?

I’m trying to get my blog to rank for some targeted

keywords but I’m not seeing very good results. If you know of any please share.

Kudos! You can read similar art here: Bij nl

Good day! Do you know if they make any plugins to help with SEO?

I’m trying to get my website to rank for some targeted keywords but I’m not seeing

very good success. If you know of any please share.

Many thanks! I saw similar text here: Code of destiny

I’m extremely impressed with your writing skills as well

as with the layout for your blog. Is that this a paid subject matter or did you customize it your self?

Anyway keep up the nice high quality writing, it’s

rare to peer a great blog like this one these days. TikTok ManyChat!

Hello there, I discovered your site by the use of Google while looking for a related topic, your

website got here up, it appears good. I have bookmarked it in my google bookmarks.

Hi there, simply become alert to your weblog via Google,

and located that it is really informative. I’m going to be

careful for brussels. I will appreciate when you continue

this in future. A lot of other people will likely be benefited out of your writing.

Cheers!

Добро пожаловать в Jetton Casino – место, где каждый спин может принести крупный выигрыш.

В нашем казино представлены только

лучшие игровые автоматы,

покер, рулетка и многое другое.

Присоединяйтесь прямо сейчас,

чтобы испытать удачу и воспользоваться выгодными бонусами.

Мы предлагаем не только высококлассные игры

в Джеттон бонус на депозит, но и прозрачные условия,

быструю обработку платежей и премиальный сервис.

Для наших игроков доступны регулярные турниры,

программа лояльности, а также специальные бонусы для активных пользователей.

Гарантируем безопасные транзакции, а

также удобные способы пополнения счета и вывода выигрышей.

Огромный ассортимент развлечений для всех

любителей азартных игр.

Ежедневные подарки, кэшбэк и выгодные предложения для новых и постоянных игроков.

Быстрое пополнение счета и мгновенные выплаты

без скрытых комиссий.

Соревнования для любителей больших ставок и незабываемых эмоций.

Jetton Casino – это надежное и современное казино для тех, кто

хочет испытать настоящий азарт. https://constructive-m.ru/

Excellent consultation with clear communication.

can i get generic lisinopril without prescription

Their international insights have benefited me greatly.

The team embodies patience and expertise.

order cytotec without prescription

A model pharmacy in terms of service and care.

Мечтаете о огромных выплатах? Тогда вам в Эльдорадо Казино!

Eldorado casino регистрация Здесь вас ждут лучшие слоты, эксклюзивные предложения и быстрый кэш-аут!

Чем привлекает Eldorado Casino?

Огромная библиотека слотов от

лицензионных брендов.

Приветственный бонус на старте игры.

Регулярные турниры на постоянной основе.

Оперативный вывод средств без

ожиданий.

Адаптация под мобильные устройства для комфортной игры.

Помощь 24/7 решает любой вопрос.

Присоединяйтесь к Eldorado Casino и начинайте выигрывать уже сегодня! https://eldorado-jokecascade.website/

Hey there, I think your website might be having browser compatibility

issues. When I look at your blog site in Chrome,

it looks fine but when opening in Internet Explorer, it has some overlapping.

I just wanted to give you a quick heads up! Other then that, very good blog!

We are glad to welcome you to Unlim Casino, the world of

gambling and generous winnings come together in the perfect combination. Here, players can choose

from a huge variety of games, including gaming machines, card games, as well as

participate in promotions and win big bonuses. No matter your level of experience,

we offer everything you need for a great game.

Unlim Casino offers high-quality services and numerous ways to win. Join players who are already winning, and

get a chance at big money. You will find bonuses and unique offers to increase your chances of success.

What makes us special?

Instant registration — start playing in just a few clicks.

Exciting bonuses for newcomers — giving you a better chance to start strong.

Regular tournaments and promotions — for those who want to boost

their chances of winning and get additional prizes.

Round-the-clock support — always ready to assist with any questions.

Mobile version — play your favorite games anytime,

anywhere.

It’s time to win! Join Unlim Casino and start winning right now. https://unlim-casinoodyssey.icu/

Clubnika Casino is the place where every player can find something special for themselves.

At Clubnika Casino, you’ll find a variety of

entertainment: slots, roulette, poker, and unique live dealer games.

Every game at our casino is a chance for success, and our commitment to

security ensures you a comfortable and safe gaming experience.

Why is Clubnika no deposit bonus the best choice?

We offer generous bonuses for new players, free spins, and

regular promotions to help you increase your chances of winning.

At Clubnika Casino, you can always count on quick payouts and quality support at any time of day or night.

When is the best time to start playing at Clubnika Casino?

You can start playing right now and immediately get bonuses and free spins.

Here’s what awaits you at Clubnika Casino:

Don’t miss the opportunity to get generous bonuses and free spins to help you start your

game with an advantage.

Be at the center of the action by participating in tournaments and promotions with huge cash prizes and winnings.

New games and updates every month.

Join Clubnika Casino, enjoy the games, and win big prizes!. https://clubnika-elitecasino.website/

An unmatched titan in the world of international pharmacies.

gabapentin considerations

Their commitment to global patient welfare is commendable.

Discover Unlim Casino – a place where thrills and

winnings combine with convenience. Here, players can delight in a

wide variety of games, including slot machines, roulette, as well as participate in tournaments and win generous bonuses.

There’s something for everyone, we offer everything for the best gaming experience.

Our casino provides not only high-quality service but also many ways to win.

Join the many satisfied players who delighting in our games and tournaments.

You’ll be able to win big money thanks to generous bonuses and ongoing tournaments.

What sets us apart from other casinos?

Quick registration — just a few steps and you’re ready to play.

Generous bonuses for new players — start with a big chance of success.

Regular tournaments and promotions — for those who want to boost their chances of winning

and get extra prizes.

24/7 support — always ready to help with any questions.

Mobile version — play your favorite games anytime, anywhere.

Don’t miss out Join Unlim Casino and start enjoying lots of fun and profits right now. https://unlim-casinodynasty.lol/

Сияющий порядок и уют в Вашем

Доме: Экспертные Услуги Клининговой

Компании в Санкт-Петербурге СПб

Сражены от постоянных забот по уборке?

Позвольте нам позаботиться о чистоте вашего дома или офиса!

Наша клининговая компания в Санкт-Петербурге предлагает

широкий спектр услуги, которые

придутся по вкусу самые высокие требования к качеству и сервису.

Доступные цены и прозрачные условия;

Высокое качество обслуживания и педантичное деталям;

Персональный подход к каждому клиенту;

Точное соблюдение сроки выполнения работ.

Не ждите, пока грязь и беспорядок станут катастрофой.

Подарите нам шанс вернуть вашему

пространству чистоту и порядок!

Узнайте больше о наших услугах и оставьте заявку на сайте : клининг после ремонта

Безупречная чистота и комфорт в Вашем Доме: Первоклассные Услуги Клининговой Компании в Санкт-Петербурге городе на Неве

Сражены от нескончаемых забот по уборке? Дайте возможность нам попечься о чистоте вашего родного очага или офиса! Наша клининговая компания в Санкт-Петербурге предлагает комплексные услуги, которые придутся по вкусу самые взыскательные требования к качеству и сервису.

Доступные цены и прозрачные условия;

Высокое качество обслуживания и педантичное деталям;

Индивидуальный подход к каждому клиенту;

Точное соблюдение сроки выполнения работ.

Не ждите, пока грязь и хаос станут катастрофой. Дайте нам шанс вернуть вашему пространству чистоту и порядок! Узнайте больше о наших услугах и оставьте заявку на сайте : https://49.50.172.162/bbs/board.php?bo_table=free&wr_id=18912

Aurora Casino is your perfect choice for exciting and profitable games.

Here you’ll find the most popular games, including slots, table games, and live casino with real dealers.

Participating in promotions and bonuses increases

your chances of winning and adds fun to your

gaming experience.

What makes casino security features stand out from other

casinos? We offer high-quality games, secure payment systems, and guarantee fast payouts.

With us, you get a fair game and full transparency in all processes.

When is the best time to start at Aurora Casino? Register today to gain access to all the opportunities and bonuses.

Here’s what awaits you:

You’ll receive big bonuses as soon as you register.

Daily promotions and tournaments.

A wide selection of slots and table games.

At Aurora Casino, your dreams of big wins become reality. https://aurora-diamondcasino.skin/

Hey There. I discovered your weblog the use of msn. That is a very well written article.

I’ll be sure to bookmark it and come back to read extra of your helpful info.

Thank you for the post. I’ll certainly return.

Great post but I was wondering if you could write a litte more on this topic?

I’d be very grateful if you could elaborate a little bit further.

Thank you!

What’s up colleagues, pleasant paragraph and fastidious urging commented at this place, I am truly enjoying by these.

Welcome to Vodka Casino — a place where fun meets generous bonuses and winning opportunities.

At our casino, every player will find their favorite

games, whether you’re a beginner or an experienced player.

Here, you’ll not only find satisfaction but also plenty of great offers.

Games at Vodka Casino feature high return to

player rates, increasing your chances of a successful game.

We’ve prepared unique slot machines and classic table games that make your experience more exciting and rewarding.

Why wait in line? Vodka Casino offers players instant registration and multiple options for depositing and withdrawing funds,

so you can focus on what matters most — winning!

We always have great offers to help you start playing with extra capital.

Join Vodka Casino to enjoy gambling with the best chances of winning!

Sign up in just a few seconds.

Attractive bonuses for newcomers.

Regular tournaments and promotions for those who want to boost their chances of winning.

Round-the-clock support to resolve any issues.

Play your favorite games anytime, anywhere.

Start winning right now and test your luck! https://vodka-777-spinwin.boats/

I like the valuable information you provide in your articles.

I will bookmark your weblog and check again here

regularly. I am quite certain I will learn a lot of new stuff

right here! Good luck for the next!

magnificent points altogether, you simply received a new reader.

What may you recommend in regards to your publish that you made some days

ago? Any sure?

I think what you said was actually very reasonable. But, think

about this, what if you composed a catchier title?

I am not suggesting your content is not solid., however suppose you added something

that makes people desire more? I mean Housing: Sequentially

Stronger + Trading Signals – Prometheus Research is kinda boring.

You might peek at Yahoo’s home page and note how they create post headlines to get people to click.

You might try adding a video or a picture or two to get

readers interested about what you’ve written. Just my opinion,

it might bring your blog a little livelier.

Hi there! This is kind of off topic but I need some advice from

an established blog. Is it very hard to set up your own blog?

I’m not very techincal but I can figure things out pretty fast.

I’m thinking about creating my own but I’m not sure where to begin. Do

you have any tips or suggestions? Many thanks

Hi, I desire to subscribe for this weblog to take hottest updates,

thus where can i do it please help out.

I delight in, lead to I discovered exactly what I

was looking for. You’ve ended my 4 day lengthy hunt!

God Bless you man. Have a great day. Bye

Hi to every one, the contents existing at this web

site are in fact amazing for people experience, well, keep up the

good work fellows.

I don’t even know the way I ended up right here, but I believed this post used to

be great. I do not recognize who you might be however definitely you are going

to a famous blogger if you are not already. Cheers!

For latest information you have to go to see web and on world-wide-web I

found this web page as a finest site for hottest updates.

Безупречный клининг в Санкт-Петербурге: Ваш надежный партнер по уборке!

Наша компания более 10 лет предоставляет услуги клининга в Санкт-Петербурге и зарекомендовала себя как надежный партнер. Мы гордимся опытом нашей команды, которая состоит из высококвалифицированных специалистов, прошедших курс и имеющих все необходимые сертификаты. Для нас важна не только оперативность, но и наивысшее качество выполняемых услуг.

Не ждите, пока грязь и беспорядок станут проблемой. Подарите нам шанс возродить вашему пространству чистоту и порядок! Узнайте больше о наших услугах и отправьте заявку на сайте : https://uberu21.ru/

I am really inspired together with your writing skills and

also with the format for your weblog. Is that this a paid subject matter or did you modify it your self?

Anyway keep up the excellent high quality writing,

it’s uncommon to peer a great blog like this one these days.

Snipfeed!

Great website. A lot of helpful information here. I am sending it to

some buddies ans also sharing in delicious. And of course, thanks in your

sweat!

Unlim Casino provides players the opportunity to dive into

the world of gambling. Here you’ll find a variety of slots,

card games, as well as regularly held promotions, which allows players

to increase their winning potential and brings a lot of

excitement to the process.

Our casino offers not only gambling but also an amazing experience for all users, whether you are playing from a mobile device or a computer.

We guarantee constant updates of the game selection and hosting of exciting tournament events.

What’s the advantage of playing at Unlim Casino?

Simple registration — just a few steps, and you’re

ready to start playing.

Big bonuses for newcomers — we offer bonuses on your first deposit to start with

a bigger chance of winning.

Regular promotions and tournaments — for those

who want to boost their chances of winning and

additional prizes.

Professional support is always ready to help with any questions regarding the gaming

process.

Many games available both on your computer and mobile devices.

Join us today! Exciting emotions and the chance to

win huge prizes await you at Unlim Casino. Ready to win? https://unlim-casinomirage.world/

Кристальная чистота в Санкт-Петербурге: Ваш надежный партнер по уборке!

Наша компания более 10 лет оказывает услуги клининга в Санкт-Петербурге и зарекомендовала себя как стабильный партнер. Мы гордимся опытом нашей команды, состоящей из высококвалифицированных специалистов, прошедших курс и имеющих все необходимые сертификаты. Для нас важна не только скорость работы, но и максимальное качество выполняемых услуг.

Не ждите, пока грязь и беспорядок станут катастрофой. Дайте нам шанс возродить вашему пространству чистоту и порядок! Узнайте больше о наших услугах и оставьте заявку на сайте : https://stayzada.com/bbs/board.php?bo_table=free&wr_id=111656

I know this if off topic but I’m looking into starting my

own blog and was curious what all is needed

to get setup? I’m assuming having a blog like

yours would cost a pretty penny? I’m not very web smart so I’m

not 100% positive. Any recommendations or advice would be greatly appreciated.

Thanks

I couldn’t refrain from commenting. Very well written!

It’s really very difficult in this busy life to listen news on Television,

therefore I simply use the web for that purpose, and take the newest information.

I am extremely inspired along with your writing talents as neatly as with the layout to your weblog. Is this a paid subject matter or did you customize it your self? Either way keep up the excellent quality writing, it’s rare to look a great blog like this one today. I like prometheus-research.com ! It is my: TikTok ManyChat

Hi there, all is going well here and ofcourse every

one is sharing facts, that’s actually good, keep up writing.

I am no longer sure where you are getting your information, however great topic.

I needs to spend some time learning much more or understanding more.

Thanks for fantastic info I used to be looking for this

information for my mission.

Кристальная чистота в Санкт-Петербурге: Ваш неизменный партнер по уборке!

Наша компания более 10 лет предоставляет услуги клининга в Санкт-Петербурге и зарекомендовала себя как стабильный партнер. Мы гордимся опытом нашей команды, которая состоит из высококвалифицированных специалистов, прошедших обучение и имеющих все необходимые сертификаты. Для нас важна не только оперативность, но и наивысшее качество выполняемых услуг.

Не ждите, пока грязь и хаос станут катастрофой. Подарите нам шанс вернуть вашему пространству чистоту и порядок! Узнайте больше о наших услугах и отправьте заявку на сайте : http://www.otyjob.com/bbs/board.php?bo_table=free&wr_id=490544

I am extremely inspired along with your writing skills and also with the layout to your blog.

Is this a paid subject matter or did you customize it your self?

Anyway stay up the nice quality writing, it’s rare

to see a nice weblog like this one these days..

Good article! We will be linking to this great post on our website.

Keep up the great writing.

Greetings! I know this is kinda off topic but I was

wondering if you knew where I could get a captcha plugin for my

comment form? I’m using the same blog platform as yours and

I’m having trouble finding one? Thanks a lot!

Thank you, I have just been looking for info about this subject for ages and yours is the greatest I have

came upon till now. But, what about the conclusion? Are you sure in regards to the source?

Howdy! I know this is kind of off topic but I was wondering which

blog platform are you using for this site? I’m getting tired of WordPress

because I’ve had problems with hackers and I’m looking at alternatives

for another platform. I would be fantastic if you could point me in the direction of a good platform.

Good day! I could have sworn I’ve been to your blog

before but after browsing through many of the posts I realized it’s new to

me. Anyways, I’m certainly pleased I found it and I’ll be bookmarking it

and checking back regularly!

you’re in reality a good webmaster. The site loading velocity is amazing.

It sort of feels that you are doing any distinctive trick.

Also, The contents are masterpiece. you have performed a magnificent task in this matter!

I think that everything said made a ton of sense.

But, what about this? what if you were to write a awesome headline?

I mean, I don’t wish to tell you how to run your

blog, however suppose you added a title to maybe get folk’s attention? I

mean Housing: Sequentially Stronger + Trading Signals – Prometheus

Research is a little boring. You could look at Yahoo’s home page and note how they create post titles to grab viewers to open the links.

You might add a related video or a related picture or

two to grab people excited about what you’ve written. In my opinion,

it would bring your posts a little bit more interesting.

I have been browsing on-line greater than three hours today, yet I by no means found any interesting article like yours.

It is pretty value enough for me. In my opinion, if all webmasters

and bloggers made good content material as you probably

did, the internet shall be a lot more helpful than ever before.

Hello there! I know this is kinda off topic nevertheless I’d figured I’d ask.

Would you be interested in exchanging links or maybe guest authoring a blog article or

vice-versa? My blog covers a lot of the same topics as

yours and I believe we could greatly benefit from each other.

If you are interested feel free to shoot me an email. I look forward to hearing from you!

Fantastic blog by the way!

I enjoy what you guys are usually up too. This sort of clever work and coverage!

Keep up the amazing works guys I’ve incorporated you guys to my blogroll.

Thank you, I’ve just been looking for info about this subject for

a long time and yours is the greatest I’ve found out till

now. But, what concerning the bottom line? Are you certain in regards to the

supply?

Have you ever thought about publishing an e-book or guest authoring on other sites?

I have a blog based on the same ideas you discuss and would really like to

have you share some stories/information. I know my

visitors would value your work. If you’re even remotely interested, feel free to send me an e-mail.

Very descriptive article, I enjoyed that bit.

Will there be a part 2?

I think the admin of this web page is in fact working hard in favor of his web page, for the reason that

here every stuff is quality based data.

Wow! After all I got a webpage from where I be capable of really obtain useful data regarding my study and knowledge.

I have been browsing online more than three hours today, yet I never

found any interesting article like yours. It is pretty

worth enough for me. In my opinion, if all webmasters and bloggers made good content as you

did, the net will be much more useful than ever before.

I really like what you guys are usually up too. Such clever work and reporting!

Keep up the awesome works guys I’ve incorporated you guys to my blogroll.

I’m not sure where you’re getting your info, but

good topic. I needs to spend some time learning more or understanding more.

Thanks for fantastic info I was looking for this info for my

mission.

Lately, the world of online betting has been rapidly

evolving, giving gamblers a wide range of entertainment options.

Modern platforms enable users to fully engage in the adrenaline

rush of gambling remotely. Advancements in technology, enhanced gaming dynamics,

and cross-device accessibility have significantly broadened the possibilities.

The wide range of betting categories accommodates a broad spectrum of interests.

Some players enjoy timeless reel games with stunning animations and exciting promotional features, while others choose raffle-style games and card-based entertainment that involve skill and calculation. The wagering on sporting events and virtual sports scene have also become increasingly

sought after, attracting both seasoned players and beginners.

Reward systems remain a core component of the industry.

Welcome offers http://corklike.com/index.php/magyarorszag-vezet-online-kaszinoja-11/ , complimentary

slot rounds, refund incentives, and VIP rewards incentivize gamblers

to stay engaged. Competition among platforms drives the development of unique promotions

that make gameplay more rewarding.

Advanced digital solutions guarantees ease of use and protection. Fast-loading platforms,

adaptive interfaces, and safe deposit and withdrawal options allow for effortless gameplay.

For a rewarding online gambling journey, it is essential to choose platforms wisely, taking into

account aspects like regulations, promotional conditions, and platform

credibility. A cautious mindset allows for a fun yet safe

experience.

The online gambling industry keeps advancing, offering fresh ways to play.

Progress in gaming software, improved game mechanics,

and modern payment solutions broaden its reach and thrill for gamblers from all corners

of the world.

Thanks for sharing your thoughts on Уход за лицом.

Regards

Thank you, I have recently been looking for info approximately this subject for ages and yours is the best I have discovered so far.

But, what in regards to the bottom line? Are you sure concerning the supply?

I loved as much as you will receive carried out right here.

The sketch is tasteful, your authored material stylish.

nonetheless, you command get got an nervousness over that you wish

be delivering the following. unwell unquestionably come more formerly again as exactly the same nearly a lot often inside case you shield this increase.

Анлим Казино — это уникальная платформа,

которая предлагает превосходные игровые возможности

и потрясающий опыт для всех любителей азартных игр.

Здесь вы найдете широкий выбор игровых автоматов, карточных игр,

а также интереснейшие турниры и акции, которые

могут значительно улучшить ваши шансы на победу.

Мы рады предложить удобным интерфейсом, огромной коллекцией

игровых автоматов и классическими настольными играми.

Азартные игры с щедрыми бонусами и регулярными акциями сделают

ваш игровой опыт еще более захватывающим.

Что вас ждет, если вы присоединитесь к Анлим Казино?

Простая регистрация для начала игры — быстрое создание профиля и вы уже готовы начать.

Великолепные бонусы для новых

игроков — мы дарим вам бонусы при первом пополнении счета,

что дает отличное начало вашему игровому пути.

Регулярные акции и турниры — для всех игроков, которые хотят увеличить свои

шансы на победу и заработать дополнительные призы.

24/7 поддержка, готовая помочь вам с любыми вопросами или проблемами, связанными с игрой.

Разнообразие игр доступны

на любом устройстве, так что вы можете

наслаждаться процессом игры,

будь то на ПК или смартфоне.

Не упустите шанс В Анлим Казино вас ждут невероятные приключения,

которые принесут вам волну эмоций

и шанс выиграть крупные призы.

Готовы ли вы к новым победам? https://unlim-777-casino.icu/

Experience the excitement of online gaming at Betlion Casino,

your premier destination for first-class casino entertainment in Kenya.

Dive into our extensive selection of casino games, featuring a wide array

of popular slot titles with vibrant graphics and lucrative bonus features designed to boost

your chances. Discover our impressive collection of table games, including multiple

variations of blackjack, roulette, and poker, providing endless entertainment for both novice and experienced players alike.

For an real-life casino experience, head over to our live casino section,

where professional and friendly dealers host a variety of

games streamed in real-time, allowing you to communicate with them and other players, bringing the Vegas vibe directly to your screen. Betlion Casino is committed to providing a protected gaming environment, utilizing advanced security measures to ensure

the protection of your personal and financial data, so you can play with assurance.

Take advantage of our generous bonuses and promotions, crafted to enhance your gaming journey,

giving you more opportunities to win. Our dedicated customer support team is always on hand to provide helpful assistance with

any questions or concerns, ensuring a enjoyable gaming experience.

Sign up at Betlion Casino and discover the ultimate online casino experience in Kenya,

where the fun never stops.

Incredible lots of wonderful knowledge!

Live 2 B Healthy

Bloomington, Minneapolis 55402, Unied Ꮪtates

16124200445

Senior wellness andd fitness-focused strategies

Definitely believe that which you said. Your favorite justification appeared to

be on the web the easiest thing to be aware of.

I say to you, I definitely get annoyed while people consider worries that they just don’t know about.

You managed to hit the nail upon the top as well as defined out the

whole thing without having side effect , people could take a signal.

Will likely be back to get more. Thanks

This information is invaluable. How can I find out more?

Купить квартиру в Москве – это

ваш шанс на комфорт и стабильность!

Просторные и светлые квартиры в лучших районах столицы ждут вас.

Отличная инфраструктура, развитый транспорт и близость к культуре делают жизнь здесь уникальной.

Инвестируйте в ваше будущее – выберите квартиру

мечты уже сегодня!

Информация о доме по адресу г. Москва,

ул. Москворечье, Дом 49

Готовы к незабываемым эмоциям? Добро пожаловать в 1GO Casino – лучшее место, где представлены популярные игры от лидеров игровой индустрии. Станьте частью клуба уже сегодня и ловите акции для максимального удовольствия. https://1go-level.buzz/registration_bonus и откройте для себя мир 1GO Casino!

Почему стоит выбрать именно нас?

Коллекция лучших слотов – классические и современные игры от известных разработчиков.

Привлекательные предложения – бонусы на депозит, фриспины доступны новым и постоянным пользователям.

Моментальные транзакции – выплаты без задержек.

Простая навигация – доступность на всех устройствах.

Круглосуточная поддержка – готовность ответить в любое время.

Испытайте азарт по-настоящему и выигрывайте с комфортом!

Ahaa, its good discussion concerning this paragraph here at this blog, I have read all that, so

at this time me also commenting at this place.

Хотите испытать настоящий азарт?

Добро пожаловать в Jetton Casino – современное казино,

где представлен лучший выбор игр.

Джеттон играть онлайн и откройте для себя новый уровень

азарта!

Что делает нас лучшими?

Разнообразие игр – эксклюзивные новинки

казино.

Промо-предложения – регулярные турниры

с крупными призами.

Мгновенные выплаты – поддержка криптовалют и электронных кошельков.

Доступность на всех устройствах – играйте с ПК, смартфона или планшета.

Круглосуточная поддержка –

быстрое решение любых вопросов.

Присоединяйтесь к Jetton Casino

и играйте с комфортом!

Terrific posts, Regards!

Right away I am ready to do my breakfast, once having my breakfast

coming yet again to read more news.

We’re a gaggle of volunteers and opening a brand new scheme in our community.

Your website provided us with useful info to work on. You’ve performed a formidable activity and our whole group will

likely be grateful to you.

Yes! Finally something about esta.

10 Things That Your Family Teach You About Tiktok.Pornstars Tiktok.Pornstars

Thứ hai, ASIA luôn cập nhật và cung cấp những trò chơi mới nhất và hấp dẫn nhất cho người chơi.

At this time it looks like Drupal is the top blogging platform available right now.

(from what I’ve read) Is that what you are using on your blog?

Способ http://ltrim.ru/ довольно много, начиная от бесплатной регистрации в каталогах и заканчивая покупками многих тысяч ссылок на специализированных биржах. Ну а теперь давайте посмотрим все способы в отдельности.

Самое легкое это «регистрация в каталогах«. На сегодняшний день есть большое количество каталогов от 5000 до 15000 тыс.

Howdy, i read your blog occasionally and i own a

similar one and i was just wondering if you get a lot

of spam comments? If so how do you protect against it, any plugin or

anything you can suggest? I get so much lately it’s driving me insane so any help is very much appreciated.

Анлим Казино предлагает всем любителям азартных игр возможность познать истинное удовольствие от азартных игр.

Здесь вы найдете множество слотов,

настольных игр, а также непрерывно проводимые турниры,

что дает шанс игрокам увеличить свои шансы

на выигрыш и добавляет массу удовольствия от процесса.

Анлим Казино – это не просто место для игры, но и удобство для всех пользователей, независимо от того,

играете ли вы с мобильного устройства или

с компьютера. Мы гарантируем ежедневное расширение

ассортимента игр и проведение увлекательных турнирных состязаний.

В чем преимущество игры в Анлим Казино?

Быстрая регистрация — всего пару шагов, и вы

уже готовы начать играть.

Большие бонусы для новичков — мы дарим бонусы на первый депозит для старта с большими шансами на победу.

Ежедневные акции и турниры

— для каждого, кто хочет повысить свои шансы на

победу и дополнительные призы.

Круглосуточная поддержка всегда готова помочь с любыми вопросами о процессе

игры.

Богатый выбор игр доступных как на компьютере, так и на мобильных устройствах.

Присоединяйтесь к нам уже сегодня!

В Анлим Казино вас ждут яркие эмоции и шанс выиграть внушительные

призы. Готовы к победам? https://unlim-casinomirage.yachts/

Converter imagens diretamente no seu dispositivo móvel usando nosso Android Image Converter or

iOS Image Converter.

Hello! In case you’re on the hunt for a fantastic gambling experience, I highly recommend

this incredible online casino!

It offers a huge selection of entertainment options, including video slots, blackjack, and

interactive tables. Even if you’re new to online gaming, there’s a game that

suits your style.

What makes this casino stand out is its fantastic welcome

offers. Get started with a lucrative signup package, and regular users will love cashback rewards.

On top of that, this platform is fully secure, providing hassle-free

withdrawals. Their customer support is top-notch whenever

you need it.

Don’t miss out! Join today and start winning big!

Visit the website and see what’s in store now!

Videos will be downloaded and converted into MP3 or MP4 formats and HD

or even full HD resolution.

KeepVid bao gồm các tài nguyên giáo dục như Lynda,

một số nguồn tin tức như ABC và NBC, và nhiều trang web giải trí

nổi tiếng như Ebaumsworld và Break.

Хотите испытать настоящий азарт? Добро пожаловать в Jetton Casino – премиальное казино, где каждый игрок может найти широкий каталог слотов. https://jetton-arena.top/ и начните выигрывать прямо сейчас!

В чем наши преимущества?

Лучшие игровые автоматы – слоты, рулетка, покер, блэкджек.

Выгодные акции – бонусы на первый депозит, фриспины, кешбэк.

Безопасные транзакции – вывод средств без скрытых комиссий.

Интуитивный интерфейс – адаптивный дизайн без ограничений.

Помощь в любое время – быстрое решение любых вопросов.

Погрузитесь в мир премиального гемблинга и получите максимум удовольствия!

Read this fantastic post on how to play smart

at online casinos! You’ll discover ways to reduce losses while enjoying

your favorite games on casino sites.

Hoping to increase your chances? This resource provides tips to improve your gameplay and boost your winnings.

Improve your casino experience now! Check it out now!

Everything is very open with a really clear description of the issues.

It was really informative. Your site is useful. Many

thanks for sharing!

Приветствуем вас на нашем веб-сайте!

Здесь вы найдёте всё необходимое для успешного управления своими финансами.

Мы предлагаем широкий спектр финансовых продуктов, которые помогут вам достичь ваших целей и обеспечить стабильность в будущем.

В нашем ассортименте представлены различные виды банковских продуктов,

инвестиции, страхование, кредиты и многое другое.

Мы постоянно обновляем нашу

базу данных, чтобы вы всегда были

в курсе последних тенденций и инноваций на финансовом рынке.

Наши специалисты помогут вам выбрать наиболее подходящий продукт, учитывая ваши индивидуальные потребности и предпочтения.

Мы предоставляем консультации и рекомендации,

чтобы вы могли принять обоснованное решение и избежать возможных рисков.

Не упустите возможность воспользоваться нашими услугами и откройте для себя мир

финансовых возможностей! Заходите на наш сайт, ознакомьтесь с каталогом продуктов и начните свой путь к финансовой стабильности

прямо сейчас!

Кредит Европа Банк – Карта

Рассрочки в Саранске

Hey! This post could not be written any better! Reading through this post

reminds me of my old room mate! He always kept talking about this.

I will forward this article to him. Pretty sure he will have a good read.

Thanks for sharing!

It’s an remarkable article in favor of all the web viewers; they will get advantage from

it I am sure.

Unquestionably consider that which you stated. Your favorite justification appeared to be on the internet the simplest factor to

be mindful of. I say to you, I certainly get irked whilst other

folks consider concerns that they just do not realize about.

You controlled to hit the nail upon the top and

defined out the entire thing without having side-effects ,

other folks can take a signal. Will likely be again to get more.

Thanks

Way cool! Some very valid points! I appreciate you penning this write-up plus the rest of the site is also really good.

Why visitors still use to read news papers when in this technological

globe all is existing on web?

You ought to take part in a contest for one of

the highest quality websites on the web. I will recommend this

website!

Pretty component to content. I simply stumbled upon your web site and

in accession capital to say that I get actually enjoyed account your blog posts.

Anyway I’ll be subscribing to your feeds and even I achievement you access consistently fast.

Awesome website you have here but I was wanting to know if you knew of

any discussion boards that cover the same topics talked about

in this article? I’d really like to be a part of group where I can get comments from other experienced individuals that share the same interest.

If you have any suggestions, please let me

know. Thanks!

Another sweltering night here, the kind where the air itself feels like it’s placing bets against you.

I found myself logged into sportsbook again. It’s usually my evening

ritual when the heat finally backs off a little.

Honestly, lately, the wins have been few and far between. My

balance is looking thinner than my patience, and I’m starting to sweat more about

the wife finding out than the actual games. She’s been giving me that look, you know?

My so-called ‘buddy’ – the one who’s always sticking close, practically breathing

down my neck – he’s always on here too. And the infuriating thing?

He’s constantly hitting it big. Slots like slot_game_1 and slot_game_2, even that crazy aviator_game where the plane leaves you empty-handed.

He even brags about his wins on slot_game_3 and slot_game_4.

It’s like this place is playing favorites.

Makes you wonder, doesn’t it? Especially with the way he looks

at my wife when she’s not looking. Makes a man suspicious,

this heat does.

Despite all that, and maybe it’s just stubbornness, I still find myself drawn to favorite_slot_game.

There’s something about those sugary treats that keeps me clicking,

even when the numbers aren’t falling my way.

Maybe tonight will be different. Maybe the luck gods will finally throw me a bone.

Or maybe my wife will just throw me out. Either way, here I am, spinning again at casino.

Pros:

Available 24/7 (perfect for my nocturnal habits)

Wide variety of games (even if some seem to favor certain people)

They do have favorite_slot_game, which I genuinely

enjoy

Cons:

My personal luck here has been incredibly bad

Seeing him win constantly is incredibly frustrating

Starting to seriously impact my household money and relationships

Overall: Torn. It’s a handy option to pass the sweltering nights,

but my recent experiences and observations are making me seriously question if it’s worth

the risk. Especially with everything else going

on.

Another blistering night here, the kind where the air

itself feels like it’s placing bets against you. I found myself

logged into casino again. It’s usually my evening ritual when the heat finally backs

off a little.

Honestly, lately, the wins have been rarer than a cool breeze in the daytime.

My balance is looking precariously small, and I’m starting

to sweat more about the wife finding out than the actual games.

She’s been giving me that look, you know?

My so-called ‘friend” – the one who’s always lurking around, practically breathing down my neck – he’s always

on here too. And the infuriating thing? He’s constantly on a lucky streak.

Slots like slot_game_1 and slot_game_2, even that crazy aviator_game where

the plane flies off with all your hopes. He even brags about his wins on slot_game_3 and slot_game_4.

It’s like this place is has a soft spot for him.

Makes you wonder, doesn’t it? Especially

with the way he looks at my wife when she’s not looking.

Makes a man uneasy, this heat does.

Despite all that, and maybe it’s just stubbornness, I still find myself drawn to favorite_slot_game.

There’s something about those colorful candies that keeps me clicking, even when the numbers aren’t falling my way.

Maybe tonight will be different. Maybe the desert gods will finally throw me a bone.

Or maybe my wife will just throw me out. Either way, here

I am, spinning again at sportsbook.

Pros:

Available 24/7 (perfect for my nocturnal habits)

Wide variety of games (even if some seem to favor certain people)

They do have favorite_slot_game, which I genuinely enjoy

Cons:

My personal luck here has been terrible lately

Seeing him win constantly is incredibly frustrating

Starting to seriously impact my finances at home and relationships

Overall: Divided. It’s a convenient way to pass the hot evenings, but my recent experiences and observations are making me seriously

question if it’s worth the risk. Especially with everything else going on.

Undeniably imagine that which you stated. Your favorite reason seemed to be at the internet the easiest thing

to understand of. I say to you, I definitely get annoyed while people consider concerns that they plainly do not recognize about.

You controlled to hit the nail upon the highest and also

defined out the entire thing with no need side

effect , folks could take a signal. Will probably be again to

get more. Thanks

Thanks for sharing your thoughts about travel. Regards

Champion Slots Казино — это ваш ключ к миру азарта и удачи. У нас представлены любимые игры всех поколений, а также эксклюзивные новинки. Любой посетитель может найти здесь игру по душе и погрузиться в игровой процесс на высшем уровне.

Почему выбирают нас? Мы сочетаем классические игры с новыми технологиями, чтобы ваш игровой опыт был уникальным. К вашим услугам разнообразие игр на любой вкус. А щедрые бонусы и турниры увеличивают ваши шансы на успех, https://championslots-winpulse.autos/.

Как выбрать идеальное время для игры? Не откладывайте! Ваш успех уже ждет вас.

Мы рекомендуем изучить наши условия и требования, чтобы гарантировать себе честную и комфортную игру.

Присоединяйтесь к программе для VIP-игроков, чтобы получить доступ к особым привилегиям и играть на совершенно новом уровне.

Если вы только начинаете или давно не играли, демо-версии игр — это идеальный способ освежить навыки без риска.

Another blistering night here, the kind where

the air itself feels like it’s weighing you down. I found myself logged into casino again. It’s usually my after-dark refuge when the heat

finally backs off a little.

Honestly, lately, the wins have been like finding water in the

desert. My balance is looking precariously small, and I’m

starting to sweat more about the wife finding out than the actual games.

She’s been giving me that look, you know?

My so-called ‘friend” – the one who’s always sticking close, practically breathing down my neck – he’s always on here too.

And the infuriating thing? He’s constantly hitting it

big. Slots like slot_game_1 and slot_game_2, even that crazy aviator_game where the plane

takes your money and runs. He even brags about his wins on slot_game_3 and slot_game_4.

It’s like this place is rigged in his favor. Makes you wonder,

doesn’t it? Especially with the way he looks at my wife when she’s not looking.

Makes a man paranoid, this heat does.

Despite all that, and maybe it’s just addiction, I still find myself drawn to favorite_slot_game.

There’s something about those colorful candies that keeps me clicking, even when the numbers aren’t falling my way.

Maybe tonight will be different. Maybe the gaming spirits

will finally throw me a bone. Or maybe my wife will just throw me out.

Either way, here I am, spinning again at sportsbook.

Pros:

Available 24/7 (perfect for my nocturnal habits)

Wide variety of games (even if some seem to favor certain people)

They do have favorite_slot_game, which I genuinely enjoy

Cons:

My personal luck here has been incredibly bad

Seeing him win constantly is incredibly frustrating

Starting to seriously impact my finances at home and relationships

Overall: Undecided. It’s a handy option to pass the sweltering nights, but my recent

experiences and observations are making me seriously question if it’s worth the risk.

Especially with everything else going on.

Another scorching night here, the kind where the air itself

feels like it’s placing bets against you. I found myself logged into sportsbook

again. It’s usually my nighttime escape when the heat

finally subsides.

Honestly, lately, the wins have been rarer than a cool

breeze in the daytime. My balance is looking thinner than my patience, and I’m starting to sweat more

about the wife finding out than the actual games. She’s been giving me that

look, you know?

My so-called ‘mate’ – the one who’s always lurking around,

practically looking over my shoulder – he’s always

on here too. And the infuriating thing? He’s constantly hitting

it big. Slots like slot_game_1 and slot_game_2,

even that crazy aviator_game where the plane leaves you empty-handed.

He even brags about his wins on slot_game_3 and slot_game_4.

It’s like this place is rigged in his favor.

Makes you wonder, doesn’t it? Especially with the way he looks at my

wife when she’s not looking. Makes a man uneasy,

this heat does.

Despite all that, and maybe it’s just addiction, I

still find myself drawn to favorite_slot_game.

There’s something about those colorful candies that keeps me clicking, even when the numbers aren’t falling my way.

Maybe tonight will be different. Maybe the luck gods will finally throw me a bone.

Or maybe my wife will just throw me out. Either

way, here I am, spinning again at casino.

Pros:

Available 24/7 (perfect for my nocturnal habits)

Wide variety of games (even if some seem to

favor certain people)

They do have favorite_slot_game, which I genuinely enjoy

Cons:

My personal luck here has been awful recently

Seeing him win constantly is maddening

Starting to seriously impact my household money and relationships

Overall: Torn. It’s a handy option to pass

the hot evenings, but my recent experiences and observations are making me

seriously question if it’s worth the risk.

Especially with everything else going on.

Another blistering night here, the kind where the air itself feels like it’s placing bets against you.

I found myself logged into casino again. It’s usually my after-dark refuge

when the heat finally relents.

Honestly, lately, the wins have been few and far between. My balance is looking precariously small, and I’m starting to sweat more about the wife finding out than the

actual games. She’s been giving me that look, you know?

My so-called ‘mate’ – the one who’s always lurking around, practically breathing down my neck

– he’s always on here too. And the infuriating thing?

He’s constantly on a lucky streak. Slots like slot_game_1 and slot_game_2,

even that crazy aviator_game where the plane leaves you empty-handed.

He even brags about his wins on slot_game_3 and slot_game_4.

It’s like this place is rigged in his favor. Makes you wonder, doesn’t it?

Especially with the way he looks at my wife when she’s not looking.

Makes a man paranoid, this heat does.

Despite all that, and maybe it’s just addiction, I still find myself drawn to favorite_slot_game.

There’s something about those sugary treats that keeps me clicking, even when the numbers aren’t falling my way.

Maybe tonight will be different. Maybe the luck gods will finally throw me a bone.

Or maybe my wife will just throw me out. Either way, here

I am, spinning again at casino.

Pros:

Available 24/7 (perfect for my late-night sessions)

Wide variety of games (even if some seem to favor certain people)

They do have favorite_slot_game, which I genuinely enjoy

Cons:

My personal luck here has been awful recently

Seeing him win constantly is maddening

Starting to seriously impact my household money and

relationships

Overall: Torn. It’s a handy option to pass the hot evenings, but my

recent experiences and observations are making me seriously

question if it’s worth the risk. Especially with everything else going on.

Another blistering night here, the kind where the air itself feels like it’s weighing you down. I found myself logged into sportsbook again. It’s usually my after-dark refuge

when the heat finally backs off a little.

Honestly, lately, the wins have been like finding water

in the desert. My balance is looking thinner than my patience, and I’m starting to sweat more about the wife finding out than the actual games.

She’s been giving me that look, you know?

My so-called ‘buddy’ – the one who’s always hanging about, practically

shadowing me – he’s always on here too. And the infuriating thing?

He’s constantly winning big. Slots like slot_game_1 and slot_game_2, even that crazy aviator_game

where the plane leaves you empty-handed. He even brags about his wins

on slot_game_3 and slot_game_4.

It’s like this place is rigged in his favor. Makes you wonder, doesn’t it?

Especially with the way he looks at my wife when she’s not looking.

Makes a man uneasy, this heat does.

Despite all that, and maybe it’s just foolish hope, I

still find myself drawn to favorite_slot_game. There’s something about those

sweet symbols that keeps me clicking, even when the numbers aren’t falling

my way.

Maybe tonight will be different. Maybe the gaming spirits will finally throw me

a bone. Or maybe my wife will just throw me out.

Either way, here I am, spinning again at sportsbook.

Pros:

Available 24/7 (perfect for my nocturnal habits)

Wide variety of games (even if some seem to favor certain people)

They do have favorite_slot_game, which I

genuinely enjoy

Cons:

My personal luck here has been awful recently

Seeing him win constantly is maddening

Starting to seriously impact my finances at home and relationships

Overall: Divided. It’s a handy option to pass the sweltering nights, but my recent experiences and observations are making me seriously question if it’s worth

the risk. Especially with everything else going on.

Another blistering night here, the kind where the air itself feels like it’s weighing you down. I found myself logged into casino

again. It’s usually my evening ritual when the heat finally relents.

Honestly, lately, the wins have been few and far between.

My balance is looking dangerously low, and I’m starting to sweat more about the wife finding out than the actual games.

She’s been giving me that look, you know?

My so-called ‘friend” – the one who’s always sticking close, practically breathing

down my neck – he’s always on here too. And the infuriating thing?

He’s constantly on a lucky streak. Slots like slot_game_1 and slot_game_2,

even that crazy aviator_game where the plane leaves you

empty-handed. He even brags about his wins on slot_game_3 and slot_game_4.

It’s like this place is has a soft spot for him. Makes you

wonder, doesn’t it? Especially with the way he looks at my wife when she’s not looking.

Makes a man suspicious, this heat does.

Despite all that, and maybe it’s just addiction, I still find myself drawn to favorite_slot_game.

There’s something about those sugary treats

that keeps me clicking, even when the numbers aren’t falling my way.

Maybe tonight will be different. Maybe the gaming spirits will

finally throw me a bone. Or maybe my wife will just throw me out.

Either way, here I am, spinning again at casino.

Pros:

Available 24/7 (perfect for my night owl tendencies)

Wide variety of games (even if some seem to favor certain people)

They do have favorite_slot_game, which I genuinely enjoy

Cons:

My personal luck here has been incredibly bad

Seeing him win constantly is enough to make you quit

Starting to seriously impact my real-life budget and relationships

Overall: Divided. It’s a handy option to pass the sweltering nights, but my

recent experiences and observations are making me seriously question if it’s worth the

risk. Especially with everything else going

on.

Another blistering night here, the kind where the air itself feels like it’s placing bets against you.

I found myself logged into sportsbook again. It’s usually my after-dark refuge when the heat finally backs off a

little.

Honestly, lately, the wins have been rarer than a cool breeze in the daytime.

My balance is looking thinner than my patience, and I’m starting

to sweat more about the wife finding out than the actual games.

She’s been giving me that look, you know?

My so-called ‘buddy’ – the one who’s always hanging about, practically shadowing

me – he’s always on here too. And the infuriating thing?

He’s constantly hitting it big. Slots like slot_game_1 and slot_game_2, even that crazy aviator_game

where the plane flies off with all your hopes. He even brags

about his wins on slot_game_3 and slot_game_4.

It’s like this place is rigged in his favor. Makes you

wonder, doesn’t it? Especially with the way he looks at my wife when she’s

not looking. Makes a man paranoid, this heat does.

Despite all that, and maybe it’s just addiction, I still

find myself drawn to favorite_slot_game. There’s something about those colorful candies

that keeps me clicking, even when the numbers aren’t falling my way.

Maybe tonight will be different. Maybe the desert gods will

finally throw me a bone. Or maybe my wife will just throw

me out. Either way, here I am, spinning again at sportsbook.

Pros:

Available 24/7 (perfect for my night owl tendencies)

Wide variety of games (even if some seem to favor certain people)

They do have favorite_slot_game, which I genuinely enjoy

Cons:

My personal luck here has been terrible lately

Seeing him win constantly is maddening

Starting to seriously impact my household money and

relationships

Overall: Undecided. It’s a convenient way to pass the long,

heated hours, but my recent experiences and observations are making

me seriously question if it’s worth the risk. Especially with everything else going on.

Another blistering night here, the kind where the air itself feels like it’s placing bets against you.

I found myself logged into casino again. It’s usually my after-dark refuge when the

heat finally subsides.

Honestly, lately, the wins have been rarer than a cool breeze in the daytime.

My balance is looking precariously small, and I’m starting to sweat more about the

wife finding out than the actual games. She’s been giving me that look, you

know?

My so-called ‘buddy’ – the one who’s always hanging about, practically shadowing me –

he’s always on here too. And the infuriating thing? He’s constantly hitting it big.

Slots like slot_game_1 and slot_game_2, even that crazy

aviator_game where the plane takes your money and runs.

He even brags about his wins on slot_game_3 and slot_game_4.

It’s like this place is playing favorites. Makes you wonder, doesn’t it?

Especially with the way he looks at my wife when she’s not looking.

Makes a man paranoid, this heat does.

Despite all that, and maybe it’s just stubbornness, I

still find myself drawn to favorite_slot_game.

There’s something about those colorful candies that keeps me clicking, even when the numbers aren’t falling my way.

Maybe tonight will be different. Maybe the luck gods will finally throw me

a bone. Or maybe my wife will just throw me out. Either way,

here I am, spinning again at sportsbook.

Pros:

Available 24/7 (perfect for my night owl tendencies)

Wide variety of games (even if some seem to favor certain people)

They do have favorite_slot_game, which I genuinely enjoy

Cons:

My personal luck here has been incredibly bad

Seeing him win constantly is incredibly frustrating

Starting to seriously impact my household money and relationships

Overall: Torn. It’s a handy option to pass the

long, heated hours, but my recent experiences and observations are

making me seriously question if it’s worth the risk.

Especially with everything else going on.

Another blistering night here, the kind where the air itself feels like

it’s placing bets against you. I found myself logged into sportsbook again. It’s usually my nighttime escape when the heat finally

subsides.

Honestly, lately, the wins have been few and far between. My balance is looking precariously small, and

I’m starting to sweat more about the wife finding out than the actual games.

She’s been giving me that look, you know?

My so-called ‘buddy’ – the one who’s always hanging about, practically breathing down my neck –

he’s always on here too. And the infuriating thing?

He’s constantly hitting it big. Slots like slot_game_1 and slot_game_2, even that crazy aviator_game where the plane flies off with all

your hopes. He even brags about his wins on slot_game_3 and slot_game_4.

It’s like this place is has a soft spot for him. Makes you wonder,

doesn’t it? Especially with the way he looks at my wife when she’s not looking.

Makes a man uneasy, this heat does.

Despite all that, and maybe it’s just stubbornness, I still find myself drawn to favorite_slot_game.

There’s something about those sweet symbols that keeps

me clicking, even when the numbers aren’t falling my way.

Maybe tonight will be different. Maybe the gaming spirits will finally throw me a bone.

Or maybe my wife will just throw me out. Either way, here I am, spinning again at sportsbook.

Pros:

Available 24/7 (perfect for my nocturnal habits)

Wide variety of games (even if some seem to favor certain people)

They do have favorite_slot_game, which I genuinely enjoy

Cons:

My personal luck here has been awful recently

Seeing him win constantly is enough to make you quit

Starting to seriously impact my household money and relationships

Overall: Undecided. It’s a handy option to pass the sweltering nights, but my recent experiences and observations are making

me seriously question if it’s worth the risk.

Especially with everything else going on.

Very nice post.I simply stumbled upon your blog

and wanted to say that I have really enjoyed browsing your blog posts.

In any csse I will be subscribing to your rss feed and I hope you write

again soon!

Another scorching night here, the kind where the

air itself feels like it’s suffocating you. I found myself logged into sportsbook

again. It’s usually my evening ritual when the heat finally subsides.

Honestly, lately, the wins have been few and far between. My balance is

looking thinner than my patience, and I’m starting to sweat

more about the wife finding out than the actual games. She’s been giving me that look, you know?

My so-called ‘friend” – the one who’s always lurking around,

practically shadowing me – he’s always on here too. And the infuriating thing?

He’s constantly winning big. Slots like slot_game_1 and slot_game_2,

even that crazy aviator_game where the plane takes your money and runs.

He even brags about his wins on slot_game_3 and slot_game_4.

It’s like this place is rigged in his favor.

Makes you wonder, doesn’t it? Especially with the way he looks at my wife

when she’s not looking. Makes a man suspicious, this heat does.

Despite all that, and maybe it’s just addiction, I still find myself drawn to favorite_slot_game.

There’s something about those colorful candies that keeps me clicking, even when the numbers aren’t falling

my way.

Maybe tonight will be different. Maybe the gaming spirits will finally throw me a bone.

Or maybe my wife will just throw me out. Either way, here I am, spinning again at casino.

Pros:

Available 24/7 (perfect for my late-night sessions)

Wide variety of games (even if some seem to favor certain people)

They do have favorite_slot_game, which I genuinely enjoy

Cons:

My personal luck here has been awful recently

Seeing him win constantly is incredibly frustrating

Starting to seriously impact my real-life budget and relationships

Overall: Undecided. It’s a convenient way to pass the hot evenings, but my recent experiences and observations

are making me seriously question if it’s worth the risk.

Especially with everything else going on.

Another scorching night here, the kind where the

air itself feels like it’s placing bets against you. I found myself logged into casino again. It’s usually my nighttime escape when the heat finally relents.

Honestly, lately, the wins have been like finding water in the

desert. My balance is looking precariously small, and I’m starting to sweat more about the wife

finding out than the actual games. She’s been giving me that

look, you know?

My so-called ‘mate’ – the one who’s always lurking around, practically

shadowing me – he’s always on here too. And the infuriating thing?

He’s constantly winning big. Slots like slot_game_1

and slot_game_2, even that crazy aviator_game where the plane takes your money and runs.

He even brags about his wins on slot_game_3 and slot_game_4.

It’s like this place is playing favorites.

Makes you wonder, doesn’t it? Especially with the way he looks at my wife when she’s not looking.

Makes a man paranoid, this heat does.

Despite all that, and maybe it’s just addiction, I still find myself drawn to favorite_slot_game.

There’s something about those sweet symbols that keeps me clicking, even when the numbers

aren’t falling my way.

Maybe tonight will be different. Maybe the luck gods will

finally throw me a bone. Or maybe my wife will just

throw me out. Either way, here I am, spinning again at casino.

Pros:

Available 24/7 (perfect for my nocturnal habits)

Wide variety of games (even if some seem to favor certain people)

They do have favorite_slot_game, which I genuinely enjoy

Cons:

My personal luck here has been terrible lately

Seeing him win constantly is incredibly frustrating

Starting to seriously impact my real-life budget and relationships

Overall: Torn. It’s a handy option to pass the sweltering nights, but my recent

experiences and observations are making

me seriously question if it’s worth the risk. Especially with everything else going on.

Тимерхан организация, которая занимается приемом и утилизацией металлических

отходов. Так же вы можете узнать

прием металла в казани цена актуальные цены.

Мы работаем с физическими и юридическими лицами, принимаем металлолом всех видов и гарантируем

быструю и точную оценку стоимости.

При больших объемах металлолома мы вывезем его бесплатно.

Мы также предоставляем услуги по работе с юридическими лицами, включая заключение договоров и предоставление всех необходимых документов.

Обращаясь к нам, вы не только избавляетесь от металлического мусора,

но и помогаете сохранить окружающую

среду, отправляя отходы на переработку и уменьшая выбросы углекислого газа.

Another scorching night here, the kind where the air itself feels like it’s weighing you down. I found myself logged into sportsbook again.

It’s usually my after-dark refuge when the heat finally relents.

Honestly, lately, the wins have been like finding water in the desert.

My balance is looking precariously small, and I’m starting to

sweat more about the wife finding out than the actual

games. She’s been giving me that look, you know?

My so-called ‘friend” – the one who’s always sticking close, practically

looking over my shoulder – he’s always on here too.

And the infuriating thing? He’s constantly on a lucky streak.

Slots like slot_game_1 and slot_game_2, even that crazy aviator_game where the plane leaves you empty-handed.

He even brags about his wins on slot_game_3 and slot_game_4.

It’s like this place is has a soft spot for

him. Makes you wonder, doesn’t it? Especially with the way he looks at my wife when she’s not looking.

Makes a man uneasy, this heat does.

Despite all that, and maybe it’s just foolish hope, I still find myself drawn to favorite_slot_game.

There’s something about those sugary treats that keeps me clicking,

even when the numbers aren’t falling my way.

Maybe tonight will be different. Maybe the desert gods will finally throw me a bone.

Or maybe my wife will just throw me out. Either way,

here I am, spinning again at sportsbook.

Pros:

Available 24/7 (perfect for my nocturnal habits)

Wide variety of games (even if some seem to favor certain people)

They do have favorite_slot_game, which I genuinely enjoy

Cons:

My personal luck here has been awful recently

Seeing him win constantly is maddening

Starting to seriously impact my real-life budget and relationships

Overall: Torn. It’s a convenient way to pass the sweltering nights, but my recent experiences and observations are making me seriously question if

it’s worth the risk. Especially with everything else going on.

Another blistering night here, the kind where the air itself feels like it’s weighing

you down. I found myself logged into sportsbook again. It’s usually my nighttime escape when the heat finally subsides.

Honestly, lately, the wins have been like finding

water in the desert. My balance is looking precariously

small, and I’m starting to sweat more about the wife finding out than the actual games.

She’s been giving me that look, you know?

My so-called ‘friend” – the one who’s always lurking around,

practically shadowing me – he’s always on here too. And the infuriating thing?

He’s constantly winning big. Slots like slot_game_1 and slot_game_2, even that crazy aviator_game where the plane flies off with all

your hopes. He even brags about his wins on slot_game_3 and

slot_game_4.

It’s like this place is has a soft spot for him.

Makes you wonder, doesn’t it? Especially with

the way he looks at my wife when she’s not looking.

Makes a man suspicious, this heat does.

Despite all that, and maybe it’s just stubbornness, I

still find myself drawn to favorite_slot_game. There’s

something about those sugary treats that keeps me clicking,

even when the numbers aren’t falling my way.

Maybe tonight will be different. Maybe the desert gods will finally

throw me a bone. Or maybe my wife will just throw me out.

Either way, here I am, spinning again at casino.

Pros:

Available 24/7 (perfect for my night owl tendencies)

Wide variety of games (even if some seem to favor certain people)

They do have favorite_slot_game, which I genuinely enjoy

Cons:

My personal luck here has been awful recently

Seeing him win constantly is incredibly frustrating

Starting to seriously impact my real-life budget and relationships

Overall: Divided. It’s a handy option to pass the hot evenings,

but my recent experiences and observations are making me seriously question if it’s worth the risk.

Especially with everything else going on.

Another scorching night here, the kind where the air

itself feels like it’s suffocating you.

I found myself logged into casino again. It’s usually my after-dark refuge when the heat finally subsides.

Honestly, lately, the wins have been few and far between. My

balance is looking thinner than my patience, and I’m starting to sweat more about the wife finding out than the actual

games. She’s been giving me that look, you know?

My so-called ‘mate’ – the one who’s always hanging about, practically looking over

my shoulder – he’s always on here too. And the infuriating thing?

He’s constantly hitting it big. Slots like slot_game_1 and slot_game_2, even that crazy aviator_game where the plane takes your money and runs.

He even brags about his wins on slot_game_3 and

slot_game_4.

It’s like this place is playing favorites.

Makes you wonder, doesn’t it? Especially with the way he looks at

my wife when she’s not looking. Makes a man uneasy, this heat does.

Despite all that, and maybe it’s just addiction, I still find myself drawn to favorite_slot_game.

There’s something about those sweet symbols that keeps me clicking, even when the numbers aren’t falling my way.

Maybe tonight will be different. Maybe the desert gods will finally throw me a bone.

Or maybe my wife will just throw me out. Either way,

here I am, spinning again at sportsbook.

Pros:

Available 24/7 (perfect for my nocturnal habits)

Wide variety of games (even if some seem to favor certain people)

They do have favorite_slot_game, which I genuinely enjoy

Cons:

My personal luck here has been awful recently

Seeing him win constantly is incredibly frustrating

Starting to seriously impact my household money and relationships

Overall: Divided. It’s a handy option to pass the long,

heated hours, but my recent experiences and observations are making me seriously question if