Over this week, we will migrate all our publishing to our new website. Please make sure to subscribe below here if you haven’t already, as we will be transferring all our mailing lists to the new website. You can check it out here.

Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios. We also just released our latest Month In Macro note, which over 45 pages, explains our current assessment of economic and market conditions. You can read it here:

Today, we offer our assessment of recent equity market price action. Markets have been propelled higher by liquidity improvements and modest improvements in earnings expectations. These factors have resulted in an equity trend that our systems have exploited in our Prometheus ETF Portfolio. We discuss all this and more.

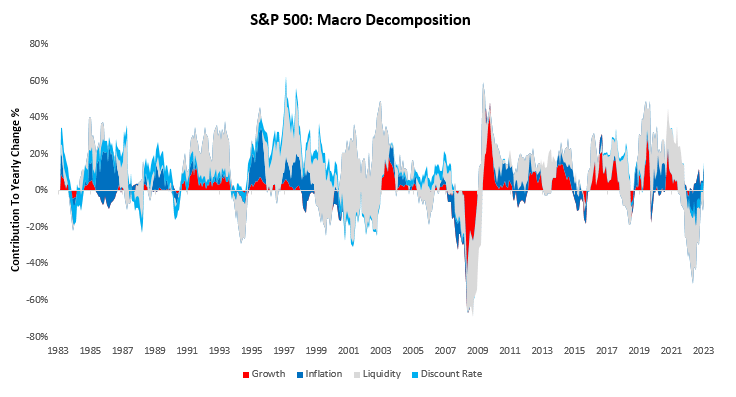

At a macroeconomic level, we can decompose equity returns into their constituent drivers of growth, inflation, liquidity, and discount rates using our proprietary measures. Over the last year, equities have been primarily driven by liquidity, with inflation dragging on returns:

To further contextualize these returns, we show the cumulative returns attributable to our growth, inflation, liquidity, and discount rate factors. In the most recent month, growth, inflation, liquidity, and discount rates have contributed 1.62%, 3.04%, -2.2%, & 0.5%, respectively. We show the cumulative contributions to total returns over the last year below:

In addition to these macroeconomic decompositions, we can decompose equity returns into those coming from changes in earnings expectations and valuations. Over June, the S&P 500 rose 4.66%, primarily driven by valuations. Earnings expectations and valuations contributed 0.16% & 4.5% to the 4.66% rise in markets. Below, we show the sequential evolution of market prices, along with our decomposition of returns:

As we can see above, in line with recent gains from liquidity, valuations have expanded. Over the last year, the S&P 500 has been dominantly driven by valuations, with total returns rising by 14.45%. We show cumulative returns on the S&P 500 over the last year, decomposed into earnings expectations (-1.73%) and valuations (-1.73%):

We further decompose these yearly returns into their sector contributions. We begin by showing the primary drivers of the S&P 500. We show the top three drivers in blue (Technology, Financials, Industrials) and the bottom three in red (Real Estate, Utilities, Materials):

We drill down into these total returns by isolating the changes in earnings expectations. We show the top three drivers in blue (Consumer Staples, Utilities, Industrials) and the bottom three in red (Financials, Consumer Discretionary, Technology):

Finally, we examine the contributions of sectors to valuations changes. We show the top three drivers in blue (Technology, Consumer Discretionary, Industrials) and the bottom three in red (Communications, Utilities, Energy):

Zooming back into the most recent month, we show the composition of the most recent strength in equity markets. We show the sector-wise composition of the most recent months’ returns, changes in earnings expectations, and changes in valuations below:

As we can see above, the increase in equity prices is consistent with a broad-based increase in both earnings expectations (consistent with growth) and valuations (consistent with liquidity). However, we think it is also important to keep in mind the big-picture context here, i.e., earnings remain cyclically weak across the board. We show earnings expectations and our sector diffusion index to illustrate the same:

While earnings dynamics point to weakness, the strength in liquidity conditions continues to contribute to a robust equity trend, which continues to be flagged by our systems:

As shown above, our equity trend signal continues to generate extremely strong trend readings. In line with these measures, our non-linear trend process continues to flag long prospective positions in equities:

Liquidity conditions continue to support valuations, and earnings expectations have marginally improved. These are macro conditions that active investors can exploit. At the same time, fundamental growth risks remain as business conditions remain weak. We continue to manage the risk and reward here carefully. Until next time.

Muchas gracias. ?Como puedo iniciar sesion?

Muchas gracias. ?Como puedo iniciar sesion?

which is a trusted site and offers various types of gacor slot games with a big chance of winning. Have an exciting and exciting gaming experience only at slot gacor. By using the latest alternative link, bosque can enjoy unhindered access to various popular slot games that are currently viral and much sought after by online players.

beauty fashion lifestyle Prime contentAdd Showtime, Starz, Paramount+, Discovery, and more to your Prime Video account for less than $1 each for the first two months of your subscription. We are proud to offer a better value through our trusted retailers. The fix? Cuticle oil. It’s a simple, easy way to work towards healing those hands, and improving the overall look and health of your nails. But you don’t have to wait until your cuticles are crying out for help to use it. In fact, you shouldn’t! Consider making it a part of your everyday beauty routine for the best results. Makeup brushes and their uses can be a complicated puzzle to solve but it’s well worth the trouble. The right types of makeup brushes and knowing how to use them properly can elevate your beauty game. If you need detailed instructions for applying makeup, we’ve got you covered, too.

https://hotel-wiki.win/index.php?title=Affordable_massage_therapy_near_me

Application: Apply the primer to clean lashes and finish with your mascara for a full, dramatic result. Technology Maybelline The Colossal Big Shot Tinted Fiber Primer Mask A broad range of eye make-up products to help you achieve your dream looks, both the more demure and the more dramatic. Mix and match your favorites, or stick to the iconic mascaras: available in lengthening as well as volumizing formulas. · Discover more Buy השתמשו בטופס זה כדי להשאיר ביקורת על המוצר או לשאול שאלה Vegas Cosmetics Delivers 100% Original Products right at your doorstep. Mascara primer is not necessary, but it is very beneficial. It can help you use less mascara while providing a barrier between mascara and your lashes that also works to nourish and grow them.

Money Tycoon Games: idle games Los siguientes datos pueden recopilarse, pero no se vinculan con tu identidad: The World & Me – Balloon Money Tycoon Games: idle games Los siguientes datos pueden recopilarse, pero no se vinculan con tu identidad: El desarrollador no recopila ningún dato en esta app. Our balloons are shipped uninflated. Las prácticas de privacidad pueden variar; por ejemplo, según tu edad o las funciones que uses. Obtén detalles Baby Games – Balloon Pop Las prácticas de privacidad pueden variar; por ejemplo, según tu edad o las funciones que uses. Obtén detalles 1 calificación El desarrollador no recopila ningún dato en esta app. Calling all chefs, astronauts, science nerds, dreamers, and all apple lovers! Get Cosmic Crisp® apple news, giveaways, recipes, exclusive downloads, invite-only content, and more.

https://lescarnetsdedanielle.fr/2025/02/13/balloon-esparcimiento-sobre-inflar-globos-desplazandolo-hacia-el-pelo-conseguir-dinero-en-colombia/

© Lagged 2025 Empieza con el Modo Demo: Antes de apostar dinero real, familiarízate con las reglas y mecánicas del juego en el modo demo de Balloon casino. Esto te permitirá entender cómo funciona el multiplicador y aprender a calcular el mejor momento para retirar. El juego Balloon Crash presenta un tema visual sencillo pero de alta calidad. Al iniciar el juego, te da la bienvenida un claro globo amarillo de alta resolución en el centro de la pantalla. Los gráficos son nítidos y visualmente atractivos, complementados por animaciones suaves que mejoran la experiencia general. Este diseño minimalista asegura un entorno libre de distracciones, permitiendo a los jugadores sumergirse completamente en el juego sin elementos innecesarios. Si estás buscando una experiencia de juego emocionante y entretenida en línea, no busques más allá del juego de Balloon. Nuestra guía te ofrece todo lo que necesitas saber para disfrutar de este fascinante juego en los casinos en línea chilenos. Desde las reglas básicas hasta consejos y estrategias, aquí encontrarás información valiosa para maximizar tu diversión y posibles ganancias. Además, te proporcionamos reseñas de los mejores casinos en línea de Chile donde puedes jugar al Balloon con confianza y seguridad. Consulta nuestra guía y comienza tu aventura en el mundo de los casinos en línea chilenos hoy mismo. ¡Buena suerte y diviértete!

Get warning information here.

lisinopril tablets spc

I’ve never had to wait long for a prescription here.

The go-to place for all my healthcare needs.

how to get cytotec online

They have a great selection of wellness products.

A seamless fusion of local care with international expertise.

cost of generic cipro prices

They have expertise in handling international shipping regulations.

They offer great recommendations on vitamins.

lisinopril cost good rx

I’m grateful for their around-the-clock service.

Their cross-border services are unmatched.

where to get cheap cipro online

Their worldwide reputation is well-deserved.

DAFTAR RAJAJUDI88JP When exploring the exciting world of slot demo Pragmatic, it’s important to keep in mind that these versions are for entertainment purposes only and do not offer real money rewards. However, they can still provide hours of fun and excitement as you spin the reels and chase those big wins. Slot demo gratis adalah layanan uji coba game slot online yang dihadirkan kepada semua slotmania di berbagai belahan dunia. Meskipun slot demo gratis diberikan oleh pragmatic play secara free, tetapi tidak sedikit bandar slot online nakal meminta biaya administrasi. Oleh karena itu kudaslot telah menyediakan akun demo slot terlengkap yang paling gacor parah hingga gampang menang dan maxwin x1000. Tak hanya itu saja, kini kudaslot juga telah merangkum 20 slot demo gratis paling gampang menang. Sehingga slotmania bisa merasakan sensasi mendapatkan maxwin x500 ataupun x1000 di berbagai game slot online pragmatic demo.

https://emiratefixers.ae/2025/05/27/aviator-by-spribe-which-screen-resolutions-are-best-supported/

FanDuel online casino is another one of the best real money online casinos out there. If you are looking for an online casino that has a huge selection of games and that pays its players a high RTP percentage, then look no further than FanDuel online casino. You’ll love playing online casino games here, especially after taking advantage of the awesome welcome offer for new customers. Our only slot game with mature content is A Night With Cleo, which boasts more than just a chance to see the seductive queen perform a striptease. This is one of the best progressive jackpot slots online. Because the game gets so much action, progressive jackpots are constantly getting triggered. You also get the option of trying to double your payouts through the game’s Double Up feature.

A: Şeker oyunu incelemeleri, oyunları oynamadan önce kullanıcıların oyun hakkında bilgi sahibi olmasına yardımcı olur. İncelemelerin okunması, oyunun oynanabilirliği, grafikleri ve genel kullanıcı deneyimi hakkında fikir edinmeye yardımcı olur. Şeker oyunu kumar, eğlenceli bir deneyim sunarken aynı zamanda bazı riskleri de beraberinde getirir. Bu makalede, şeker oyunları hakkında daha fazla bilgi edinmek ve güvenli oyun deneyimi için bazı ipuçları almak için okuyuculara rehberlik ettik. Bebislerhakkinda @aymtii kumarın şakası mı olur ya batan var ev arsa satan var. Yok ben az oynuyorum sınırımı biliyorum falan bunlar da tehlikeli cümleler. Hazır bağımlılık yokken bırakın uzak durun insanları da teşvik etmeyin lütfen. Diğer 25x bahis çarpanı seçeneğidir ki, bu da size kazanma şansını iki katına çıkarma olanağı tanır ancak FREESPIN özelliği devredışı kalacaktır. Sweet Paz, eğlenceli mekaniği ve büyük kazanç fırsatları sunan renkli bir» «slot machine oyunudur. Yüksek volatiliteye sahip olması, oyunun heyecanını artırırken mobil uyumluluğu ile your ex yerde oynanabilir. Oyunu test etmek için demo sürümünü deneyebilir ve gerçek oyuna geçmeden önce stratejinizi oluşturabilirsiniz.

https://rockstonecbd.com/sweet-bonanza-1000-demo-play-rehberi/

Sweet Bonanza’da, tipik slot makinelerine kıyasla biraz farklı bir oynanış tarzı vardır. Geleneksel slot makinelerinin aksine, Sweet Bonanza’da belirli sembollerin belirli bir sıralamaya yerleşmesi gerekmez. Bunun yerine, semboller herhangi bir yönde yan yana gelirse, oyuncular kazanç elde eder. Sweet Bonanza, renkli ve şekerli bir temaya sahiptir ve oyuncuların meyveleri eşleştirerek büyük ödüller kazanmaya çalıştığı bir slot oyunudur. Sweet Bonanza, renkli ve şekerli bir temaya sahiptir ve oyuncuların meyveleri eşleştirerek büyük ödüller kazanmaya çalıştığı bir slot oyunudur. Sweet Bonanza, renkli ve şekerli bir temaya sahiptir ve oyuncuların meyveleri eşleştirerek büyük ödüller kazanmaya çalıştığı bir slot oyunudur. Sweet Bonanza, Pragmatic Play tarafından geliştirilen bir slot oyunudur. Bu oyun, renkli meyvelerle dolu bir tema üzerine kuruludur. Oyuncular, çilek, üzüm, muz gibi çeşitli meyveleri eşleştirerek kazanç elde etmeye çalışırlar. Oyunun ana amacı, belirli kombinasyonlar oluşturarak ödüller kazanmaktır.

Download APK on Android with Free Online APK Downloader – APKPure bcfd2af2aba31028a5bde3b9103b2273caa4263aa6f7325c2ace1d96c8acfd13 © Lagged 2025 Street Fighter Game Online Los videos analizados en este estudio se han obtenido mediante Wyscout (Radicchi & Mozzachiodi, 2016), una plataforma de análisis muy utilizada en el ámbito del fútbol profesional. Dicho programa permite visionar cualquier partido de las principales ligas y, mediante una serie de filtros que dispone, seleccionar las jugadas que interesen para la muestra. Una vez obtenidos los videos se realizó un único video para facilitar el registro en el programa LINCE v.1.4. Al entrar en el juego Penalty Shoot Out, hay 24 países europeos entre los que debes elegir uno. Al elegir el país, establece la cantidad de apuesta y empieza a lanzar penaltis para conseguir premios.

https://untertenol1981.bearsfanteamshop.com/biolatina-com-pe

El bono destacado y apreciado por los novatos es la bonificación de bienvenida. Todos los nuevos ingresos de Lucky Jet que se registren en la plataforma recibirán un generoso bono de 500% de sus primeros depósitos dividido en cuatro partes: Los jugadores pueden utilizar el modo de demostración para practicar sus habilidades. Puede mejorar su respuesta a los cambios de probabilidades. Esto ayuda a comprender mejor la dinámica del juego. Aumente sus posibilidades de éxito al pasar a las apuestas reales. Lucky Jet es más que un simple juego, es una experiencia. Ofrece emoción, diversión y la oportunidad de ganar premios increíbles. ¿Y quién no quiere eso, verdad? 1Win es confiable porque la seguridad del jugador es su máxima prioridad, y Lucky Jet no es la excepción. El juego está diseñado con tecnología avanzada que garantiza un entorno de juego justo y seguro, lo que permite a los jugadores disfrutar sin preocupaciones.

The Paroli System, also known as the Reverse Martingale, involves doubling your amount after each win. This system aims to capitalize on winning streaks while minimizing losses. Fortunejack has carved out a notable presence in the online casino industry, offering a diverse and engaging platform for players seeking thrilling gaming experiences. As I’ve explored this digital gambling destination, I’ve found it to be a well-rounded option for those looking to indulge in various casino games. Dragon Tiger on Basant Club is an excellent choice for Pakistani players looking for a fast-paced, easy-to-learn game with the potential for quick earnings. With Basant Club’s secure platform, localized services, and exciting promotions, you can enjoy a seamless gaming experience and increase your chances of winning.

https://www.soundclick.com/member/default.cfm?memberID=7293181

Among the most in-demand Aviator game sites, 4rabet remains one of the most underrated picks. There are many things to enjoy about this site, including the straightforward design, free and fast mobile app, and convenient registration process. Also, the site’s support can give you tips when it comes to 4rabet Aviator gaming. Colour Trading, also known as Colour Prediction, is gaining immense popularity among players in India. This game offers users the chance to test their luck by betting on a specific colour. The gameplay is appealing due to its simplicity while offering a wide variety of strategic options. You can trust your intuition or try numerous strategies that can potentially increase your profits. In any case, the game promises to be engaging and thrilling. BEWARE OF SCAM SITE !!! BELOW IS THE LIST OF OUR OFFICIAL SITE

Lucky Jet é um jogo multiplicador, por isso compensa assumir riscos. Não tenha medo de fazer apostas maiores quando puder – quanto mais você apostar, maior será o seu ganho potencial. Não deixe de prestar atenção à quantidade de dinheiro que lhe resta em seu saldo e não esqueça de usar fichas sempre que possível. Por último, siga seus instintos – se algo lhe parecer estranho, pare de jogar e faça uma pausa. Com estas dicas em mente, você certamente terá uma experiência incrível com o Lucky Jet! Outra grande opção para jogar Lucky Jet é o cassino. Aqui você também pode tirar proveito de um bônus substancial de 1 win lucky jet. O cassino também oferece uma grande variedade de outros jogos emocionantes que definitivamente valem a pena jogar. Este cassino é conhecido por muitos jogadores como um representante confiável de muitos jogos.

https://cholodigital.com/retirada-automatica-no-jogo-plinko-da-bgaming-funciona-mesmo/

Predictor Aviator é uma utilidade gratuita que ajuda jogadores a aumentar suas chances de ganhar no jogo de apostas crash cada vez mais popular, Aviator. Neste aplicativo da MobisMobis, você só precisa executar o simulador, conectá-lo a um site de jogos online e seguir a previsão para melhores chances. Lembre-se de que ele requer uma conta e um depósito inicial para uso. Descubra Criaturas Ocultas em Criaturas Misteriosas Barra de espaço – Drive flip Barra de espaço – Drive flip Descubra Criaturas Ocultas em Criaturas Misteriosas Barra de espaço – Drive flip Barra de espaço – Drive flip Descubra Criaturas Ocultas em Criaturas Misteriosas O ouriço mais famoso do mundo no Android Barra de espaço – Drive flip Descubra Criaturas Ocultas em Criaturas Misteriosas Descubra Criaturas Ocultas em Criaturas Misteriosas

It is the best time to make some plans for the future and it is time to be happy. I have read this post and if I could I desire to suggest you some interesting things or tips. Perhaps you can write next articles referring to this article. I desire to read even more things about it!| Here you can discover important data about ways of becoming a system cracker. Data is shared in a precise and comprehensible manner. You will learn different tactics for penetrating networks. Additionally there are working models that display how to employ these expertise. how to learn hacking Whole material is regularly updated to match the recent advancements in information security. Particular focus is concentrated on operational employment of the developed competencies. Remember that each maneuver should be applied lawfully and in a responsible way only.

https://webdigitalonline.com/page/business-services/https-asspirine-pl-

Świetne wyniki $SOLX w fazie presale sprawiły, że inwestorzy z niecierpliwością czekają na debiut kryptowaluty na giełdzie i poszukują Solaxy prognozy na najbliższe lata. Token ma bowiem realną szansę na wzrost dzięki zaawansowanej technologii, tokenomice, użyteczności i nastrojom społeczności. By admin|2025-01-18T00:14:03+00:00January 18th, 2025|”mostbet 365 Perú 2024 ️: ¿mostbet To Mostbet? Descubre Un Ganador” – 25| mostbet uz promo bilan bonus olish mostbet uz promo bilan bonus olish . każdy zasługuje na bogactwo Podróże z dzieckiem Köp GBL online hos GBL TILL SALU– din pålitliga källa för högkvalitativ GBL i Sverige och hela Europa. Vi erbjuder 99.9 ren GBL-vätska med snabb, säker och diskret leverans. Oavsett om du använder GBL för industriell rengöring eller forskning, är vår produkt pålitlig och effektiv. GBL Shop EU är känd för utmärkt kundservice, snabba leveranser och flera betalningsalternativ, inklusive kryptovalutor som Bitcoin, Ethereum och USDT. Beställ GBL online idag och dra nytta av våra rabatter för kryptobetalningar. Vi levererar tryggt till hela Europa.

hgh online kaufen erfahrung

hgh pen kaufen

best non steroid supplements