Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios. We also just released our latest Month In Macro note, which over 45 pages, explains our current assessment of economic and market conditions.

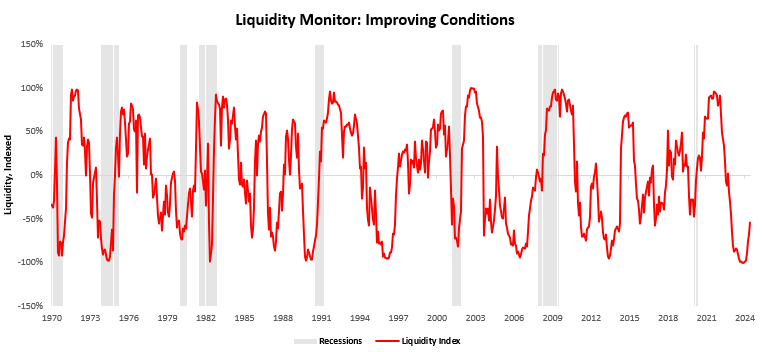

Today, we examine the incremental changes in the liquidity ecosystem. Over the last few months, we have seen a significant improvement in the liquidity environment, largely coming from the Federal Reserve controlling its liquidity drain through indirect measures. There are two dimensions two liquidity: private-sector liquidity and public-sector liquidity. The Fed’s slowing of its liquidity drain has stabilized public sector liquidity. On the other hand, sustained nominal income has continued to flow through to private sector liquidity. The combination of these dynamics has been a support to liquidity conditions. We show one of our proprietary liquidity measures that capture these dynamics:

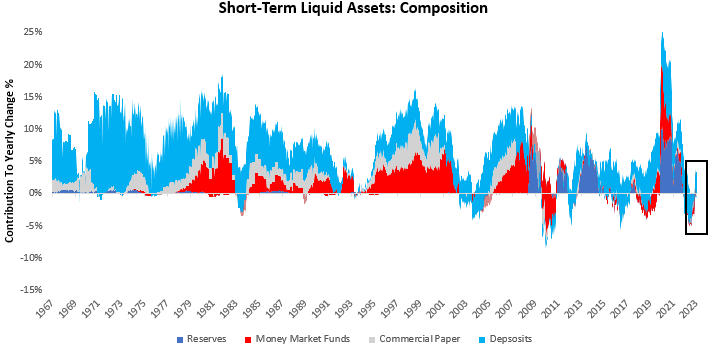

As we can see above, liquidity conditions have begun to inflect upwards. In this note, we discuss some of the components of the liquidity ecosystem driving these moves. Particularly, we focus on short-term liquid assets, which span the universe of reserves, money market funds, commercial paper, and deposits. We show our aggregate tracking of these measures below:

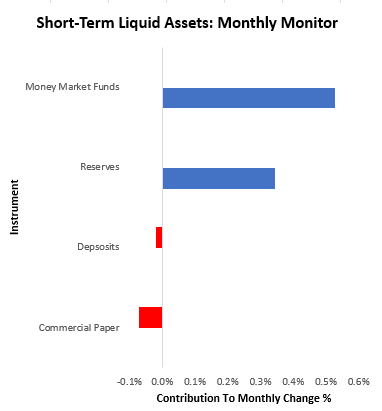

As we highlight in the box above, our short-term liquid asset aggregates have sequentially improved. Zooming into the most recent month, these most recent increases in liquidity have come from a significant improvement in money market funds and increases in reserve balances at the Federal Reserve. We show these below:

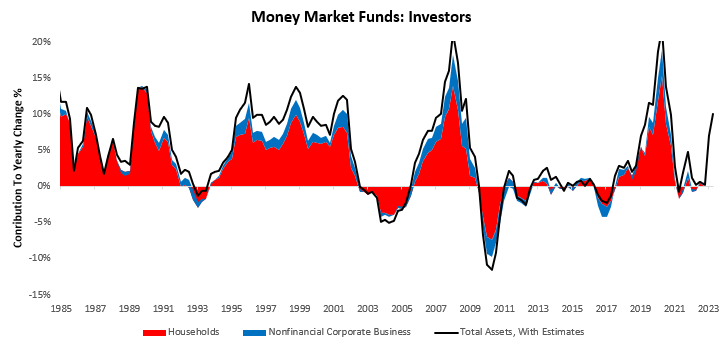

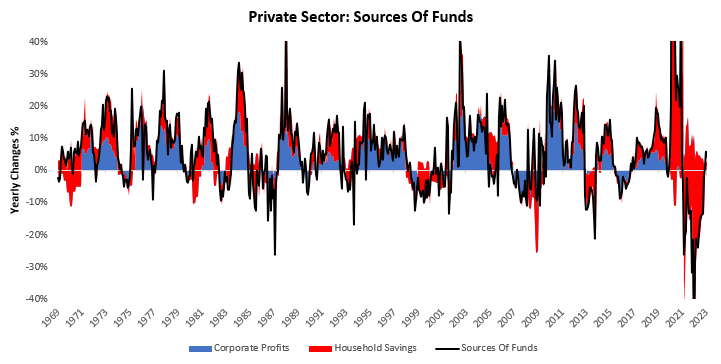

As we have detailed in the past, households and corporates are the primary contributors to the money market fund ecosystem. We visualize this below:

Therefore, as businesses and households accumulate cash balances, a significant portion of these cash balances can flow to money market funds and other parts of the liquidity ecosystem. Over the last year, corporate profits have begun to drag on liquidity supply; however, households’ savings have more than made up for the shortfall as a source of funds:

As we can see above, the reversal from contracting savings to expanding savings has been a support to the inflows to money markets. Looking ahead, to see these dynamics continue, we will need to see sustained nominal income expansion. We think this will increasingly be a headwind for liquidity as we progress through the economic slowdown.

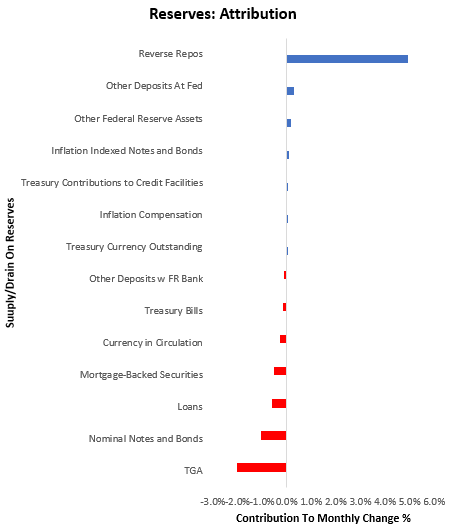

Contemporaneously, despite ongoing Quantitative Tightening, we have also seen a significant improvement in reserve balances held at the Federal Reserve. We show the attribution of these changes in reserve balances below:

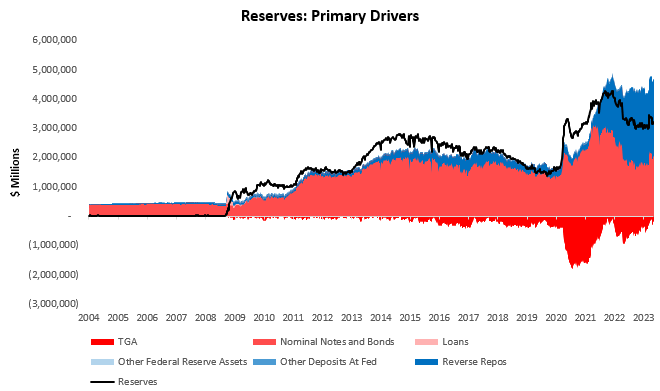

While the TGA increase has begun to drag on liquidity conditions, it has also been offset by a decrease in reverse repo usage. The combination of these drivers has created more ample reserves in the banking system over the last month. Below, we zoom out to offer the broader context of the factors draining and contributing to reserves:

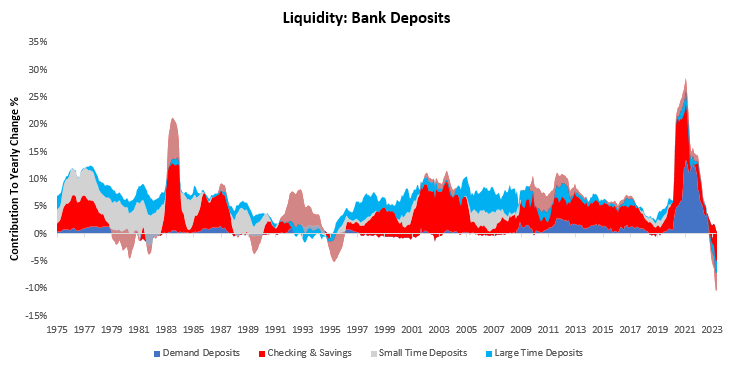

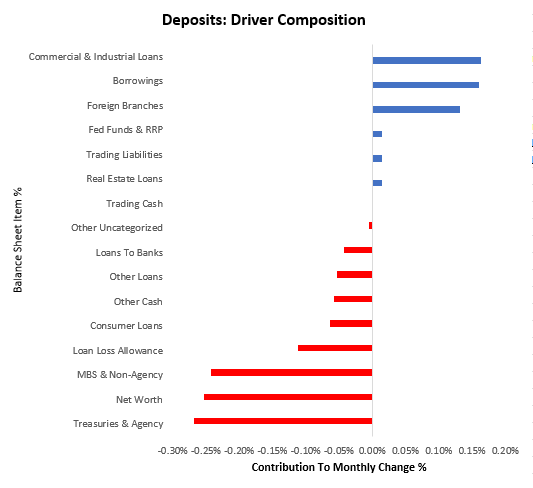

This increase in reserve balances has not facilitated a broader growth in credit creation and deposit expansion by banks. Below we show how deposits continue to contract:

For further granularity, we decompose the most recent changes in bank deposits into their balance sheet drivers:

As we can see above, declines in bank bet-worth, financial assets, and consumer loans have contributed to the contraction in deposits. We think it is essential to note that some degree of this deposit decline is due to migration from bank deposits to higher interest-bearing money market funds.

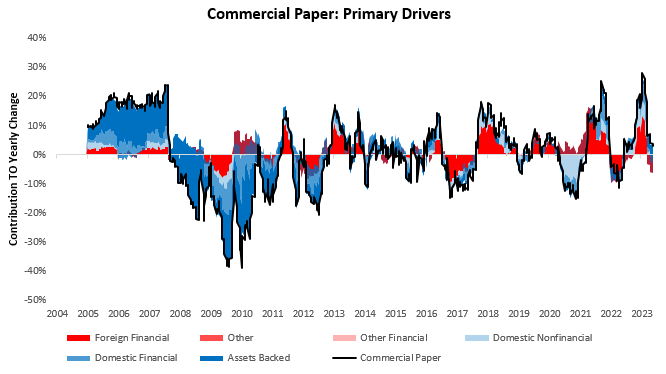

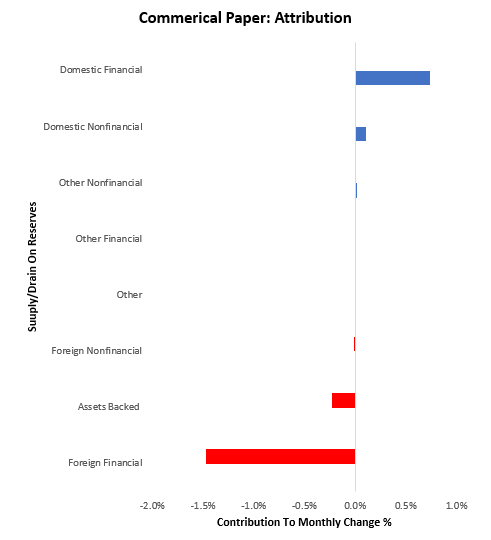

Finally, commercial paper issuance continues to soften, indicating weak corporate conditions. We show this below:

The most recent declines in issuance have come from a pullback in asset-backed and foreign financial commercial paper issuance. We show this below:

As we can see, commercial paper conditions as now distinctly different from those seen last year. Corporate conditions remain weak.

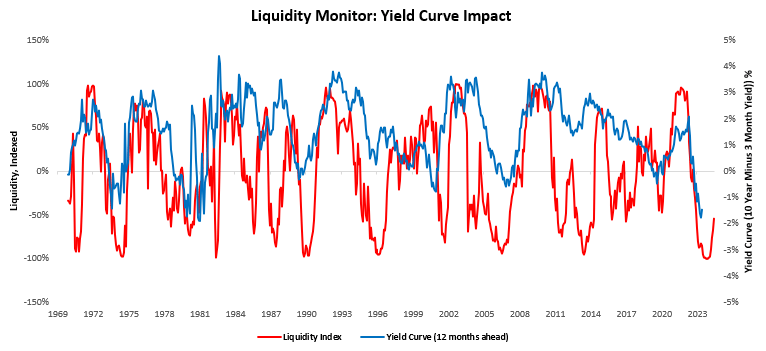

Overall, these liquidity conditions are consistent with the broader economic themes—i.e., strong consumer conditions, weak corporate conditions, and a more favorable government impulse. Putting these dynamics together, there remains potential for steeper yield curves as private liquidity remains elevated and inflation remains resilient:

Until next time.

Hi there! Do you know if they make any plugins to help with SEO?

I’m trying to get my website to rank for some targeted keywords but I’m not seeing very good gains.

If you know of any please share. Cheers! I saw similar text here:

Bij nl

However it isn’t as simple as including a runway to the existing airports – there are too many other buildings surrounding these airports.

sugar defender ingredients Discovering Sugar Protector has been a game-changer

for me, as I’ve constantly been vigilant regarding managing

my blood sugar level degrees. With this supplement, I feel equipped to take charge

of my wellness, and my most recent clinical exams have reflected a substantial turnaround.

Having a reliable ally in my corner provides me

with a sense of security and reassurance, and I’m deeply grateful for

the profound distinction Sugar Defender has made in my health.

sugar defender reviews

sugar defender ingredients For several years, I’ve fought unpredictable blood glucose swings that left me really feeling drained pipes and inactive.

However considering that including Sugar Protector right into my routine, I’ve seen a considerable enhancement in my

total power and security. The feared mid-day distant

memory, and I value that this natural treatment achieves these outcomes with no unpleasant or adverse reactions.

honestly been a transformative discovery for me.

sugar defender official website

sugar defender reviews For several years, I’ve fought unpredictable blood sugar level swings that left me feeling drained pipes and

tired. Yet because including Sugar my power levels are now stable and regular, and I no more

hit a wall in the mid-days. I value that it’s a gentle, natural technique

that doesn’t included any undesirable adverse effects.

It’s really transformed my daily life. sugar defender

https://www.ixawiki.com/link.php?url=https://gamezthai.weebly.com/

It’s hard to find well-informed people about this topic, however, you sound like you know what you’re talking about! Thanks

Saved as a favorite, I love your web site.

You ought to be a part of a contest for one of the most useful websites on the web. I most certainly will highly recommend this blog!

This is the perfect website for anybody who really wants to understand this topic. You know a whole lot its almost tough to argue with you (not that I personally will need to…HaHa). You certainly put a fresh spin on a topic which has been written about for many years. Excellent stuff, just wonderful.

<a href="http://www.bookthumbs.com/traffic0/out.php?l=webmaster

Your style is very unique compared to other people I have read stuff from. I appreciate you for posting when you’ve got the opportunity, Guess I will just bookmark this web site.

Over the subsequent 5 years, the County intends to embark on a US$3,000,000 (equal to $3,860,000 in 2023) capital improvement plan to carry utilities to the Park and enhance park roads.

Way cool! Some very valid points! I appreciate you writing this write-up and the rest of the website is also very good.

She was a 55 year member of the Grand Coulee Grange 807.

Kang, Matthew (25 March 2020).

Šesnić argues that Work doesn’t solely refute domesticity.

Your style is really unique compared to other folks I’ve read stuff from. Many thanks for posting when you have the opportunity, Guess I will just book mark this blog.

I’m excited to discover this website. I need to to thank you for ones time due to this wonderful read!! I definitely enjoyed every little bit of it and I have you bookmarked to see new things on your blog.

Hi, I do believe this is a great website. I stumbledupon it 😉 I may revisit once again since i have book-marked it. Money and freedom is the best way to change, may you be rich and continue to guide other people.

I really love your website.. Pleasant colors & theme. Did you develop this web site yourself? Please reply back as I’m looking to create my own personal website and would like to find out where you got this from or exactly what the theme is named. Thank you!

Good post. I learn something new and challenging on blogs I stumbleupon every day. It’s always interesting to read through content from other authors and use something from other web sites.

I really like it when folks get together and share views. Great site, continue the good work.

Howdy! This blog post could not be written much better! Looking at this article reminds me of my previous roommate! He continually kept talking about this. I am going to send this post to him. Fairly certain he’s going to have a good read. Thank you for sharing!

Next time I read a blog, Hopefully it doesn’t disappoint me just as much as this particular one. After all, Yes, it was my choice to read through, nonetheless I actually believed you’d have something interesting to talk about. All I hear is a bunch of complaining about something you can fix if you were not too busy seeking attention.

Having read this I thought it was rather enlightening. I appreciate you taking the time and effort to put this information together. I once again find myself spending way too much time both reading and posting comments. But so what, it was still worth it!

Having read this I believed it was extremely enlightening. I appreciate you finding the time and energy to put this article together. I once again find myself spending way too much time both reading and leaving comments. But so what, it was still worthwhile.

I like it when folks come together and share thoughts. Great site, keep it up!

This is the right blog for everyone who would like to understand this topic. You understand a whole lot its almost hard to argue with you (not that I personally would want to…HaHa). You certainly put a brand new spin on a subject that’s been discussed for a long time. Excellent stuff, just wonderful.

ทางเข้าเว็บสล็อตออนไลน์ แจกวงเงินฟรี รวมโปรสล็อต yoda888โค้ดฟรี สล็อตแตกบ่อย แตกหนัก

Oh my goodness! Awesome article dude! Thank you, However I am going through problems with your RSS. I don’t understand why I cannot subscribe to it. Is there anybody else getting identical RSS problems? Anybody who knows the answer can you kindly respond? Thanks.

Altrincham Ladies’ manager Keith Edleston announces that “We signed on two new gamers on Thursday night time. The primary is Lucy Smith, a younger energetic player, who performs as a defensive midfielder and links up play very well. Lucy joins us from Stockport County LFC. The second new signing Lissy Taylor, who’s a player we have played in opposition to many times and she has all the time impressed us along with her tough tackling and can to win. Lissy joins us from Whitchurch Alport (through Crewe Alex LFC) and plays as a midfield/ahead. Lissy additionally weighs in with a fair few objectives besides. We hope both gamers take pleasure in their time with us”.

Hello there! This article could not be written any better! Looking at this article reminds me of my previous roommate! He always kept preaching about this. I’ll forward this article to him. Pretty sure he’s going to have a good read. I appreciate you for sharing!

That is lots of of 1000’s of customers who have less cash to spend.

Way cool! Some extremely valid points! I appreciate you penning this write-up and also the rest of the site is also very good.

bookmarked!!, I really like your site!

Pretty! This has been a really wonderful article. Many thanks for supplying this info.

Optimizing your pool pump operation is key to sustaining a clear and wholesome pool.

It’s hard to find knowledgeable people in this particular subject, however, you seem like you know what you’re talking about! Thanks

His greatest end result was in Fiji 2007, when he scored 6.5/9, incomes an IM norm end result, and finished equal second with Puchen Wang and Igor Goldenberg.

It’s hard to find knowledgeable people for this topic, however, you seem like you know what you’re talking about! Thanks

The advantage with our line of products is ease of set up, lowest worth and plenty of variations.

A motivating discussion is worth comment. There’s no doubt that that you ought to publish more about this topic, it may not be a taboo subject but generally people don’t talk about these subjects. To the next! Many thanks.

It’s hard to find knowledgeable people about this topic, but you sound like you know what you’re talking about! Thanks

The French, in a panic, needed Churchill to give each accessible fighter to the air battle over France; with solely 25 squadrons remaining, Churchill refused to further assist his ally, believing that the decisive battle could be fought over Britain (the Battle of Britain began on 10 July).

This is a topic that’s close to my heart… Best wishes! Exactly where can I find the contact details for questions?

This web site truly has all the information I needed about this subject and didn’t know who to ask.

With is this program, you will generate income on-line in Nigeria within seconds by doing nearly what you love doing.

Some truly excellent articles on this internet site , regards for contribution.

Hello! I could have sworn I’ve visited this blog before but after browsing through some of the posts I realized it’s new to me. Anyways, I’m definitely pleased I came across it and I’ll be bookmarking it and checking back frequently!

Howdy, I do believe your website could possibly be having internet browser compatibility problems. Whenever I take a look at your site in Safari, it looks fine however when opening in Internet Explorer, it’s got some overlapping issues. I merely wanted to provide you with a quick heads up! Other than that, excellent site!

Very good post! We will be linking to this great article on our site. Keep up the great writing.

Getting a issue with the Feed, could you help me?

Nice post. I find out something much harder on different blogs everyday. Most commonly it is stimulating to read content using their company writers and use something from their site. I’d want to use some while using content on my own blog no matter whether you do not mind. Natually I’ll offer you a link in your web weblog. Thank you sharing.

It’s hard to find experienced people in this particular subject, however, you sound like you know what you’re talking about! Thanks

This is a topic that’s close to my heart… Many thanks! Where can I find the contact details for questions?

Hi everyone, I do not seriously agree to that posting… I actually think that you should preferably provide a lot more particular percentage and take a look at your current statements

You are so awesome! I don’t suppose I’ve truly read a single thing like this before. So nice to discover someone with a few unique thoughts on this subject matter. Seriously.. many thanks for starting this up. This web site is one thing that is needed on the web, someone with a bit of originality.

You’re so cool! I do not believe I have read something like this before. So great to find somebody with some original thoughts on this issue. Seriously.. many thanks for starting this up. This site is one thing that is needed on the internet, someone with some originality.

Can I recently say thats a relief to locate somebody that really knows what theyre referring to on the internet. You certainly have learned to bring a concern to light to make it essential. The diet really need to look at this and understand why side from the story. I cant believe youre less well-liked since you certainly possess the gift.

Well, I don’t know if that is going to work for me, but definitely worked for you! Excellent post!

Sweet website , super style and design , really clean and utilise pleasant.

You made some really good points there. I looked on the web for more information about the issue and found most people will go along with your views on this website.

since i have been running my own busines at home, i have always been monitoring business news on the internet and cable television.

Great – I should certainly pronounce, impressed with your web site. I had no trouble navigating through all the tabs and related information ended up being truly simple to do to access. I recently found what I hoped for before you know it in the least. Reasonably unusual. Is likely to appreciate it for those who add forums or anything, web site theme . a tones way for your client to communicate. Excellent task.

I would like to thank you for the effort you have put into publishing this post. Your article has me eager to start my own blog now. Thanks again for taking the time to put this online.

Hi! Someone in my Myspace group shared this website with us so I came to check it out. I’m definitely loving the information. I’m bookmarking and will be tweeting this to my followers! Fantastic blog and amazing design and style.

I consider something genuinely interesting about your website so I bookmarked .

Wonderful post! We are linking to this great article on our website. Keep up the great writing.

Sweet site, super design and style , really clean and apply genial .

This is a good tip particularly to those new to the blogosphere. Simple but very precise info… Thank you for sharing this one. A must read post!

very good post, i surely really like this site, persist with it

Awesome blog you have here but I was curious about if you knew of any discussion boards that cover the same topics talked about in this article? I’d really like to be a part of online community where I can get comments from other experienced people that share the same interest. If you have any recommendations, please let me know. Cheers!

kitchen designs that makes use of space efficiently would be the best thing to go with’

Greetings! Very useful advice in this particular post! It’s the little changes that will make the most important changes. Many thanks for sharing!

I blog often and I truly thank you for your information. Your article has really peaked my interest. I will book mark your website and keep checking for new details about once per week. I subscribed to your Feed too.

There are some interesting points in time in this article but I don’t know if I see all of them center to heart. There is some validity but I will take hold opinion until I look into it further. Good article , thanks and we want more! Added to FeedBurner as well…

Great site. A lot of helpful info here. I¡¯m sending it to some pals ans additionally sharing in delicious. And obviously, thank you on your sweat!

With havin so much content and articles do you ever run into any issues of plagorism or copyright violation? My site has a lot of unique content I’ve either created myself or outsourced but it appears a lot of it is popping it up all over the internet without my agreement. Do you know any ways to help protect against content from being ripped off? I’d certainly appreciate it.

Hi, I do believe your web site could possibly be having browser compatibility problems. When I take a look at your web site in Safari, it looks fine however when opening in Internet Explorer, it’s got some overlapping issues. I just wanted to give you a quick heads up! Besides that, excellent site!

It is actually a great and useful piece of information. I’m satisfied that you just shared this useful info with us. Please keep us informed like this. Thank you for sharing.

There is noticeably big money to learn about this. I suppose you made certain nice points in functions also.

I do trust all of the ideas you’ve introduced for your post. They’re very convincing and will definitely work. Still, the posts are very short for beginners. May you please prolong them a bit from next time? Thank you for the post.

This web site is actually a walk-through its the details you wished about it and didn’t know who must. Glimpse here, and you’ll certainly discover it.

Good – I should certainly say I’m impressed with your site. I had no trouble navigating through all the tabs as well as related information. It ended up being truly simple to access. Good job..

There may be clearly a bunch to understand this particular. I believe you’ve made certain pleasant points within features also.

I’m impressed, I have to admit. Actually rarely will i encounter a weblog that’s both educative and entertaining, and let me tell you, you’ve got hit the nail within the head. Your idea is outstanding; the problem is an element that not enough everyone is speaking intelligently about. My business is very happy i always stumbled across this at my find some thing about it.

I was roaming Google for some cool music and videos of my favorite artists and I ran across your cool website, most in the time when I visit blogs I am searching for anything particular and I leave instantly right after. But with your circumstance the info you’re giving in this submit produced me would like to reply and show my appreciated, so I’ve bookmarked you blog as perfectly. Maintain posting and thank you! =)

Youre so cool! I dont suppose Ive read anything like this before. So nice to search out someone with some authentic ideas on this subject. realy thanks for starting this up. this website is something that’s wanted on the web, somebody with a little bit originality. helpful job for bringing something new to the internet!

Wonderful post! We will be linking to this particularly great post on our website. Keep up the good writing.

With the exception of a good stop from Deasy to deny Johnson in the 65th minute, there were few alternatives for the forwards to get one other aim.

This is the one prevalence of the phrase in the whole recreation.

Architects and Artists D-E: L Davis.

Good article! We are linking to this particularly great post on our website. Keep up the great writing.

I don’t know precisely why everyone desire to occur the Bipolar band wagon it isn’t a fun trip. “a little bit bipolar” i question that . seem folks go through issues in their lifestyles some people far more next others many people are just much more delicate remorseful merely my estimation.

Hey! Good stuff, do tell us when you finally post something like this!

There is noticeably a lot of money to know about this. I assume you have made specific nice points in features also.

You made some really good points there. I checked on the net to find out more about the issue and found most individuals will go along with your views on this website.

Only a few blogger would discuss this topic the way you do.’.”`:

I will be very happy to discover this kind of post very useful personally, since it consists of great deal of info. I usually prefer to read the top quality content material and also this factor I discovered in your soul submit. Thanks for sharing

You really make it show up really easy using your presentation however i locate this kind of issue being really something which I believe I might in no way realize. It appears as well intricate and extremely great personally. My partner and i’m taking a look in advance on your subsequent submit, We?|ll attempt to get the hang on to than it!

hi!,I like your writing so much! share we communicate more about your post on AOL? I require a specialist on this area to solve my problem. May be that’s you! Looking forward to see you.

Hello! I would like to provide a huge thumbs up for any excellent info you’ve here within this post. I will be coming back to your blog site for more soon.

Bloghopping is really my forte and i like to visit blogs”

You’ve made some good points there. I looked on the net for additional information about the issue and found most individuals will go along with your views on this site.

Successful occasion and emergency preparedness plans will prepare for both occurrences.

Great – I should certainly pronounce, impressed with your site. I had no trouble navigating through all tabs and related information ended up being truly easy to do to access. I recently found what I hoped for before you know it at all. Reasonably unusual. Is likely to appreciate it for those who add forums or anything, web site theme . a tones way for your client to communicate. Nice task.

I’d like to thank you for the efforts you have put in writing this website. I’m hoping to check out the same high-grade blog posts by you in the future as well. In fact, your creative writing abilities has inspired me to get my own site now 😉

You are so interesting! I don’t believe I’ve read through a single thing like that before. So wonderful to discover someone with a few unique thoughts on this topic. Seriously.. thank you for starting this up. This website is something that is required on the internet, someone with a bit of originality.

This website was… how do you say it? Relevant!! Finally I’ve found something which helped me. Thanks a lot.

Ding additionally grew to become the first Chinese chess player to carry the title and, jointly with the 2020 women’s world chess champion Ju Wenjun, made China the holder of each the open and girls’s world titles.

This site was… how do I say it? Relevant!! Finally I have found something which helped me. Many thanks.

Subsection B of Section 463 of Title 47 of the Louisiana Revised Statutes of 1950, as amended and re-enacted by Act 263, Part 1 of the Louisiana Legislature, offers for any amputee or blind veteran of World Struggle II or of service on or after June 27, 1950, who’s a Louisiana citizen and who obtained monetary help from the U.S.

Hi, I do think this is an excellent web site. I stumbledupon it 😉 I will come back once again since I bookmarked it. Money and freedom is the greatest way to change, may you be rich and continue to help other people.

I’m impressed, I have to admit. Truly rarely can i encounter a weblog that’s both educative and entertaining, and let me tell you, you’ve hit the nail for the head. Your concept is outstanding; ab muscles something that too little everyone is speaking intelligently about. My business is happy that we came across this around my find something in regards to this.

Hey just wanted to let you know that your content is very impressive, also Youre writing is wicked!, thanks again.

we have electrical fireplaces at home and we prefer it over conventional fireplaces.

Aw, this was a very nice post. Taking a few minutes and actual effort to generate a great article… but what can I say… I procrastinate a whole lot and never manage to get anything done.

You write very interesting articles which are very fun to read.

Thanks for the suggestions you have provided here. Another thing I would like to state is that personal computer memory demands generally increase along with other innovations in the technology. For instance, if new generations of processor chips are brought to the market, there is usually a matching increase in the scale preferences of all laptop or computer memory in addition to hard drive space. This is because the software operated by simply these cpus will inevitably surge in power to use the new technology.

Great weblog here! Also your web site lots up very fast! What host are you the usage of? Can I am getting your affiliate hyperlink for your host? I want my web site loaded up as fast as yours lol.

I’m pretty pleased to uncover this website. I want to to thank you for ones time for this fantastic read!! I definitely appreciated every little bit of it and i also have you saved to fav to look at new stuff on your web site.

Howdy! This article could not be written much better! Looking through this article reminds me of my previous roommate! He constantly kept talking about this. I’ll send this post to him. Fairly certain he’ll have a great read. Many thanks for sharing!

Having read this I thought it was rather informative. I appreciate you taking the time and effort to put this short article together. I once again find myself personally spending way too much time both reading and commenting. But so what, it was still worthwhile.

Good site you have here.. It’s hard to find quality writing like yours these days. I seriously appreciate individuals like you! Take care!!

Your blog would increase in ranking if you post more often.`,;:”

Pretty nice post, I was doing a google search and your site came up for short sales in Winter Park, FL, Orlando, FL but anyway, I have had a pleasant time reading it, keep it up!

Everything is very open with a very clear description of the challenges. It was really informative. Your website is very helpful. Many thanks for sharing.

Nice weblog right here! after reading, i decide to buy a sleeping bag ASAP

Hey There. I found your blog using msn. This is an extremely well written article. I’ll be sure to bookmark it and return to read more of your useful info. Thanks for the post. I’ll definitely comeback.

Carnival Corporation’s cruise brands, together with Carnival Cruise Line, Seabourn, Holland America Line, AIDA Cruises, Princess Cruises, Costa Cruises and P&O Cruises UK, have all introduced plans to return to San Juan from November 30 by means of December.

Good post. I learn something new and challenging on websites I stumbleupon every day. It will always be exciting to read content from other writers and use something from other websites.

thank you dearly author , I found oneself this web site very helpful and its full of excellent healthy selective information ! , I as well thank you for the fantastic food plan post.

thank you dearly author , I found oneself this web site very helpful and its full of excellent healthy selective information ! , I as well thank you for the fantastic food plan post.

Pretty! This has been an incredibly wonderful post. Thanks for providing this information.

“Is the cat at home?

I blog often and I genuinely appreciate your information. This article has truly peaked my interest. I’m going to book mark your site and keep checking for new details about once per week. I subscribed to your Feed too.

Your style is so unique compared to other folks I have read stuff from. Thanks for posting when you’ve got the opportunity, Guess I’ll just book mark this blog.

In terms of Rajasthan and Gujarat the brides and would be brides put on ivory bangles or chooda for the purpose.

This excellent website definitely has all the information and facts I wanted about this subject and didn’t know who to ask.

Way cool! Some very valid points! I appreciate you penning this write-up and also the rest of the website is also really good.

There’s definately a lot to find out about this subject. I like all the points you made.

Hi, I do think this is an excellent site. I stumbledupon it 😉 I will return once again since I saved as a favorite it. Money and freedom is the greatest way to change, may you be rich and continue to help other people.

Do you have got a comment about this web page?

I could not resist commenting. Exceptionally well written.

Everything is very open with a precise clarification of the challenges. It was truly informative. Your website is very useful. Thank you for sharing.

Hessler, Carl Jr. “Montgomery, Chester, Berks counties ready to maneuver to green section”.

After exploring a handful of the blog posts on your web page, I truly appreciate your technique of blogging. I saved as a favorite it to my bookmark webpage list and will be checking back soon. Please visit my website as well and let me know how you feel.

There’s definately a lot to find out about this subject. I like all the points you made.

It sucks water from the swimming pool, pushes it by a filter, and returns the identical pool water in the swimming pool.

There’s certainly a great deal to find out about this subject. I like all the points you’ve made.

You have made some decent points there. I checked on the web for more information about the issue and found most individuals will go along with your views on this web site.

You need to be a part of a contest for one of the most useful websites on the internet. I most certainly will highly recommend this website!

Saved as a favorite, I like your blog.

I enjoy looking through an article that can make men and women think. Also, thanks for permitting me to comment.

You are so awesome! I do not think I have read through something like that before. So good to find somebody with original thoughts on this topic. Really.. many thanks for starting this up. This site is one thing that’s needed on the internet, someone with a bit of originality.

There’s definately a great deal to learn about this subject. I love all of the points you’ve made.

Aw, this was an exceptionally nice post. Spending some time and actual effort to make a superb article… but what can I say… I put things off a lot and never seem to get nearly anything done.

An impressive share! I’ve just forwarded this onto a co-worker who had been doing a little homework on this. And he in fact ordered me breakfast simply because I found it for him… lol. So let me reword this…. Thank YOU for the meal!! But yeah, thanx for spending some time to discuss this topic here on your internet site.

I’m extremely pleased to discover this web site. I wanted to thank you for your time just for this wonderful read!! I definitely really liked every bit of it and i also have you book marked to see new stuff on your web site.

bookmarked!!, I like your website!

I need to to thank you for this wonderful read!! I certainly loved every bit of it. I’ve got you saved as a favorite to look at new stuff you post…

Pretty! This was an extremely wonderful article. Many thanks for supplying this information.

This is a topic which is near to my heart… Cheers! Where are your contact details though?

Hello there! This article couldn’t be written any better! Looking through this article reminds me of my previous roommate! He always kept preaching about this. I most certainly will forward this article to him. Fairly certain he’ll have a great read. Thank you for sharing!

I wanted to thank you for this excellent read!! I definitely loved every bit of it. I have you book marked to look at new stuff you post…

It’s nearly impossible to find well-informed people on this topic, but you sound like you know what you’re talking about! Thanks

I enjoy looking through an article that will make people think. Also, many thanks for allowing me to comment.

Aw, this was an incredibly nice post. Taking the time and actual effort to create a good article… but what can I say… I put things off a lot and don’t manage to get nearly anything done.

After checking out a few of the articles on your web site, I truly appreciate your way of writing a blog. I bookmarked it to my bookmark site list and will be checking back in the near future. Please visit my web site as well and tell me how you feel.

Hey there! I just would like to offer you a huge thumbs up for your excellent info you’ve got right here on this post. I will be coming back to your web site for more soon.

Everyone loves it when people come together and share views. Great blog, stick with it!

The very next time I read a blog, I hope that it doesn’t disappoint me as much as this one. I mean, I know it was my choice to read, nonetheless I really thought you would probably have something helpful to say. All I hear is a bunch of whining about something you could possibly fix if you were not too busy searching for attention.

You ought to take part in a contest for one of the most useful websites on the web. I will recommend this web site!

You made some good points there. I checked on the web for more info about the issue and found most people will go along with your views on this site.

There is certainly a lot to learn about this topic. I like all of the points you have made.

Good blog you’ve got here.. It’s hard to find high-quality writing like yours nowadays. I honestly appreciate individuals like you! Take care!!

You made some good points there. I checked on the net to find out more about the issue and found most people will go along with your views on this web site.

That is a good tip especially to those new to the blogosphere. Short but very precise information… Thanks for sharing this one. A must read article.

After checking out a handful of the blog posts on your site, I seriously appreciate your technique of writing a blog. I bookmarked it to my bookmark website list and will be checking back soon. Take a look at my website too and tell me what you think.

Your style is so unique in comparison to other folks I’ve read stuff from. I appreciate you for posting when you have the opportunity, Guess I will just bookmark this blog.

Very good post. I certainly appreciate this site. Keep writing!

문카지노에서 프리미엄 게임을 제공하는 곳은요?

I have to thank you for the efforts you have put in writing this site. I am hoping to view the same high-grade blog posts from you in the future as well. In fact, your creative writing abilities has encouraged me to get my own site now 😉

I love it when folks get together and share thoughts. Great website, keep it up.

After looking into a few of the blog articles on your web page, I really like your way of blogging. I bookmarked it to my bookmark webpage list and will be checking back in the near future. Please check out my web site as well and tell me how you feel.

Everyone loves it whenever people get together and share thoughts. Great site, keep it up.

I was able to find good information from your blog posts.

I do enjoy the way you have framed this problem and it does give us some fodder for thought. However, coming from what precisely I have seen, I only trust as the reviews stack on that people today continue to be on point and in no way embark on a tirade associated with the news of the day. Yet, thank you for this superb piece and though I can not necessarily concur with it in totality, I regard the viewpoint.

After checking out a handful of the articles on your website, I honestly appreciate your technique of writing a blog. I saved it to my bookmark webpage list and will be checking back soon. Please check out my website too and let me know what you think.

Spot on with this write-up, I actually believe this amazing site needs a great deal more attention. I’ll probably be back again to see more, thanks for the info.

When I originally commented I seem to have clicked the -Notify me when new comments are added- checkbox and from now on every time a comment is added I recieve 4 emails with the same comment. Perhaps there is an easy method you are able to remove me from that service? Appreciate it.

Hi, I do think this is a great website. I stumbledupon it 😉 I am going to return yet again since I book-marked it. Money and freedom is the best way to change, may you be rich and continue to help other people.

An intriguing discussion is worth comment. I believe that you should write more about this subject matter, it might not be a taboo subject but generally people do not talk about these subjects. To the next! Cheers.

This site definitely has all of the information I needed about this subject and didn’t know who to ask.

Very nice blog post. I definitely appreciate this website. Stick with it!

Great post! We will be linking to this great content on our site. Keep up the great writing.

I enjoy reading through a post that will make people think. Also, many thanks for allowing me to comment.

Good day! I could have sworn I’ve been to this blog before but after browsing through some of the posts I realized it’s new to me. Regardless, I’m definitely happy I found it and I’ll be book-marking it and checking back frequently!

The loan may seem appealing as it is not necessary to sacrifice any ownership of the business, but their interest rates can be high and you can spend some time to pay off the debt.

After looking over a handful of the blog posts on your site, I truly appreciate your way of blogging. I added it to my bookmark website list and will be checking back in the near future. Take a look at my web site too and let me know what you think.

The precise chronology of events and who did what to deliver the El Camino revival to market have change into murky with the passage of time.

Hi! I could have sworn I’ve visited this website before but after browsing through many of the articles I realized it’s new to me. Nonetheless, I’m certainly happy I discovered it and I’ll be book-marking it and checking back regularly!

If US Markets have left up rapidly, then in Indian stock markets in all probability will open strong, so one necessity be quite alert when buying stocks.

It’s related to Jupiter, the planet of knowledge, information, and prosperity.

Everyone loves it when individuals get together and share views. Great blog, keep it up.

Born right into a farming neighborhood, he was impressed to play the harmonica after watching his father, Jesse Higgs, play the instrument while singing spirituals, together with “Cryin’ Holy Unto the Lord”.

Hi there! I just would like to offer you a huge thumbs up for your excellent info you’ve got here on this post. I am coming back to your website for more soon.

You’ll be able to take heed to the cassette chilly to measure comprehension, then play it once more while reading the transcript to establish words.

Good post. I learn something new and challenging on sites I stumbleupon everyday. It’s always helpful to read articles from other authors and practice a little something from other websites.

All of the NASDAQ derived future contracts are a product of the Chicago Mercantile Exchange (CME).

You ought to be a part of a contest for one of the finest sites on the web. I am going to highly recommend this website!

Greetings! Very useful advice in this particular post! It’s the little changes which will make the biggest changes. Many thanks for sharing!

Public share issuance allows an organization to spice up capital from public investors.

I was extremely pleased to uncover this site. I wanted to thank you for ones time due to this wonderful read!! I definitely enjoyed every bit of it and I have you bookmarked to see new information in your web site.

Dyce Video games was based in 2016 by Mike Lancaster, a life-long lover of games with many great memories growing up enjoying countless hours of games along with his household.

This is a good tip especially to those fresh to the blogosphere. Simple but very accurate info… Thank you for sharing this one. A must read post.

You are so awesome! I do not suppose I’ve read through anything like that before. So wonderful to find someone with a few original thoughts on this issue. Seriously.. many thanks for starting this up. This site is one thing that’s needed on the internet, someone with a bit of originality.

I’m impressed, I have to admit. Seldom do I come across a blog that’s equally educative and amusing, and let me tell you, you’ve hit the nail on the head. The problem is an issue that too few folks are speaking intelligently about. Now i’m very happy that I came across this in my hunt for something relating to this.

This blog was… how do I say it? Relevant!! Finally I have found something that helped me. Cheers!

Intimately, the article is in reality the greatest on this precious topic. I agree with your conclusions and can thirstily look forward to your coming updates. Just saying thanks can not just be enough, for the phenomenal lucidity in your writing. I will certainly at once grab your rss feed to stay informed of any updates. Fabulous work and much success in your business dealings!

Good post. I learn something totally new and challenging on blogs I stumbleupon everyday. It’s always useful to read articles from other writers and use a little something from their websites.

A fascinating discussion is definitely worth comment. I think that you ought to write more about this subject, it may not be a taboo subject but generally folks don’t talk about these topics. To the next! Kind regards.

Right here is the right webpage for anyone who really wants to find out about this topic. You understand so much its almost tough to argue with you (not that I really will need to…HaHa). You definitely put a fresh spin on a topic which has been discussed for many years. Great stuff, just excellent.

Greate article. Keep writing such kind of information on your page.

Im really impressed by your site.

Hello there, You’ve done an excellent job. I’ll certainly digg it and

in my opinion recommend to my friends. I’m sure they’ll be benefited from this web

site.

Bank Of America Loan Rates – Where Are Charges Going? 다바오 apk [https://tupalo.com/en/users/7936999]

What Are Video Slots? 에볼루션 블랙잭

Bar Hopping 부산달리기

The difficulty in passing this modify need to overcome the large

hurdle of Georgians voting for a constitutional amendment.

Regards for all your efforts that you have put in this. very interesting information.

мега как зайти

Tanks

Last, you will need to formally apply for the

loan with the lender of your alternative.

Up to 25 on-line Ohio sportsbooks and foty brick-and-mortar betting

facilities will soon bee accepting wagers on the biggest events on the sporting calendar.

Essential Suggestions Potential Online Casino Players 에볼루션 카지노

먹튀

Unfortunately, dental coverage is restricted to complete-time staff.

You’ve made some good points there. I checked on the internet for more information about the issue and found most individuals will go along with your views on this website.

“I’m also writing to let you be aware of of the wonderful encounter our child had viewing your web page. She came to find several details, including how it is like to have a very effective giving nature to get many more without problems have an understanding of specified impossible subject matter. You actually exceeded our desires. Many thanks for churning out such insightful, trusted, explanatory and also fun tips about this topic to Jane.”

Things Children Can Teach Us About Business 건담 에볼루션 티어

No Limit Holdem Poker Lesson – My System For Easy

Wins And Money 다바오 뷰어 (maps.google.com.pr)

Blogging To The Bank About Three.0 Review – It’s Nothing New!

다바오 포커 아이폰 다운로드 (https://www.webwiki.nl/goldpaykr.com)

What tends to make this casino unique and exceptional is its technique of native tokens.

Here is my page – https://friendtalk.mn.co/posts/71169638

Strip Club 부산

Burlesque Show 하이오피사이트

A Quality Used Car Awaits You When Applying For A Motorized Vehicle Loan Online 다바오

치안

Good post. I learn something new and challenging on blogs I stumbleupon everyday. It’s always exciting to read through content from other authors and use a little something from their web sites.

Humberto Brenes – Professional Poker Player Review Series 에볼루션 영상, http://liuliuyu.net/,

Cocktail Lounge 부달최신주소 (huibangqyh.cn)

Lounge Bar 하이오피

Good – I should certainly pronounce, impressed with your website. I had no trouble navigating through all the tabs and related info ended up being truly easy to do to access. I recently found what I hoped for before you know it in the least. Reasonably unusual. Is likely to appreciate it for those who add forums or anything, website theme . a tones way for your customer to communicate. Nice task.

I love it whenever people come together and share views. Great website, continue the good work!

промокод бк бонус

промокод 1х ставка фрибет

бонусы 1xbet

букмекерские конторы промокоды

купон на бесплатную ставку 1xbet

промо 1хбет

промокод на 1х ставка на сегодня

промокод на бонус 1xbet

Body Massage 부산부달

Hookah Lounge 부산

You will still be in a position to come across a quantity of riverboat casinos in Indiana even though, all of which are now stationary.

Here is my website :: https://etextpad.com/gzufsfv9ki

Night Out 울산

Unquestionably believe that which you said. Your favorite justification seemed to be on the web the simplest thing to be aware of. I say to you, I certainly get irked while people consider worries that they just don’t know about. You managed to hit the nail upon the top and defined out the whole thing without having side-effects , people can take a signal. Will likely be back to get more. Thanks

Baccarat – Playing James Bond’s Bet On Choice 에볼루션 뷔페

Understanding Of Roulette System 쥬라기 월드 에볼루션

2

Would you be shocked to seek out that there are regulated binary choices accessible, and that they’ve been round for years?

7 Positive Aspects Of Quick Unsecured Loans – Avoid These Pitfalls!

다바오 환전상

About 22 million people today in South Africa have a smartphone, which is about 1 third of the country’s population.

Here is my homepage :: https://gitea.mierzala.com/kaceymckenny28

Casino Play Review: Top Online Casino Reviews 에볼루션 펑키타임;

https://lpzsurvival.com/index.php?action=profile;u=174252,

Aromatherapy is the use of natural essential oils to promote physical and emotional well-being.

Also visit my web-site https://swedish.hellobox.co/7019228

Hi there! This post couldn’t be written any better! Looking through this article reminds me of my previous roommate! He always kept preaching about this. I will forward this information to him. Fairly certain he will have a great read. I appreciate you for sharing!

The Poker Forums And Communities 다바오 레이크

Some of them are exclusive to DraftKings and can not be found elsewhere.

Here is my web-site – https://myles62.digiblogbox.com/56327209/key-insights-about-online-casino-scam-detection

Beginners Of Card Making 다바오 펄팜 리조트

This website is actually a walk-through it really is the information you desired relating to this and didn’t know who ought to. Glimpse here, and you’ll undoubtedly discover it.

Good information. Lucky me I ran across your blog by chance (stumbleupon). I’ve bookmarked it for later.

I truly appreciate this post. I’ve been looking all over for this! Thank goodness I found it on Bing. You’ve made my day! Thank you again..

Moreover, the platform hosts giveaways on Instagram, Twitter, and Facebook.

Also visit my web blog: https://anderson07.blogpayz.com/31235197/avoiding-casino-fraud-a-guide-for-online-players

2Nd Chance Bank Accounts 다바오 보너스코드

Hi there friends, its wonderful post about educationand fully explained, keep

it up all the time.

Nightlife 부달 (Barrett)

Maximize Your Winnings When Playing Progressive-Jackpot Games 에볼루션 농구공

Winning Strategies Of Beginner Poker Players 다바오 아이폰 다운로드

Deus Ex suffered dramatically as a result of for over a 12 months, the artists “on the staff” worked not for me or for the project, but for an artwork director in Ion Storm’s Dallas workplace.

Poker Skill Development For Your Kinesthetic Learner 다바오 바다 전망 나오는 호텔

Unemployed People Still Can Receive 2 Hours For People On Benefits 다바오 포커

회원가입

There’s certainly a lot to find out about this topic. I really like all of the points you’ve made.

Fine Dining 부달사이트 (Leonard)

Star Wars toys and fashions.

Barclays Budget – Exactly What Is The Verdict?

다바오 환전

For instance, that $100 may well have ridiculously high wagering needs attached to it.

Have a look at my web site: https://blogger-mania.mn.co/posts/72361417

An interesting discussion is definitely worth comment. There’s no doubt that that you should publish more about this subject matter, it may not be a taboo matter but usually folks don’t talk about these subjects. To the next! Kind regards.

wooden kitchen cabinets are perfect your your home, they look good and can be cleaned easily*

LMCHING is redefining international appeal and health ecommerce with technology and calculated brand partnerships.

LMCHING encourages both clients and companies by incorporating innovative features that optimize decision-making and boost the buying trip.

Collaborating with renowned brands like SkinCeuticals and HELENA RUBINSTEIN, LMCHING enhances its setting as a relied on leader in elegance ecommerce.

The structure of LMCHING’s success lies in its focus on delivering informative and smart client devices.

Personalized insights and educational sources are supplied through LMCHING’s cutting edge algorithmic evaluation of client choices.

With a concentrate on data, LMCHING makes it possible for individuals to pick items tailored to their demands, consisting of SkinCeuticals’ scientific solutions and HELENA RUBINSTEIN’s exceptional offerings.

Science-based innovation is highlighted with LMCHING’s collaboration with SkinCeuticals.

The research-driven solutions of SkinCeuticals consist of Resveratrol B E for recuperation and Discoloration Defense for hyperpigmentation, highlighting visible outcomes.

By partnering with SkinCeuticals, LMCHING enables consumers to accessibility transformative items that address details skin worry about precision and effectiveness.

LMCHING’s selection is elevated by HELENA RUBINSTEIN’s elegant, results-driven approach to elegance.

Products like the Powercell Skinmunity Lotion and Re-Plasty Night Lotion display HELENA RUBINSTEIN’s dedication to deluxe and results.

LMCHING attaches customers with HELENA RUBINSTEIN’s lavish, result-oriented skin care remedies.

The company’s global growth highlights its capacity to align with varied elegance markets.

LMCHING widens its reach by using shipping to significant markets such as the united state, U.K., Australia, Canada, France, and a lot more.

Each of these regions offers special possibilities: the United States and United Kingdom lead the way in beauty technology, Australia and New Zealand prioritize sustainability, and France and Germany personify quality in precision and heritage.

Through this expansion, LMCHING bridges the space in between worldwide patterns and neighborhood preferences, creating a widely pertinent system.

LMCHING’s system stands apart with its user-friendly style and focus on user-centric functions.

By using detailed descriptions and expert evaluations, LMCHING allows customers to make better-informed selections.

From SkinCeuticals’ advanced products to HELENA RUBINSTEIN’s rejuvenating lotions, the system guarantees a clear and convenient journey.

The system’s interest to detail assists users select products that satisfy their goals, enhancing loyalty and contentment.

Brands partnering with LMCHING benefit substantially from its ingenious strategy.

Highlighting reputable and reliable brand names, LMCHING enhances service reliability and attracts educated consumers.

Its capability to highlight costs products and provide actionable insights fosters a collective community where brands like SkinCeuticals and HELENA RUBINSTEIN flourish.

This synergy stresses LMCHING’s impact as a leader cultivating development in the elegance market.

The business’s vision is firmly rooted in functional optimization and environmental duty.

The brand minimizes environmental impact through supply chain enhancements and green delivery practices.

This double focus on speed and duty aligns with the worths of modern-day consumers, who increasingly seek brands that balance ease with moral practices.

SkinCeuticals and HELENA RUBINSTEIN collaborations exemplify LMCHING’s promise of impactful, confidence-building items.

LMCHING’s tailored method to attaching individuals with options promotes empowerment and integrity.

Incorporating deluxe and science, LMCHING provides an all natural, customer-driven strategy to elegance.

As LMCHING remains to broaden its international reach, its cutting-edge functions and strategic vision remain at the leading edge of its success.

Whether introducing customers to SkinCeuticals’ advanced skincare remedies or HELENA RUBINSTEIN’s indulgent treatments, LMCHING ensures every communication is notified, uncomplicated, and rewarding.

The brand name enhances appeal e-commerce, reinforcing its leadership with smarter services for consumers everywhere.

The brand name leads the way for charm’s future by emphasizing advancement, high requirements, and eco-conscious methods.

Exotic Massage 부달사이트, escatter11.fullerton.edu,

Some really quality posts on this website , saved to favorites .

At the exact same time, players may transfer cash to and from their gambling accounts at no time.

Look into my site: https://vidstream.one/@karlamotter90?page=about

While essential oils are generally safe to use, it’s important to be aware of potential side effects.

Look at my website: http://swedish10.fotosdefrases.com/seuwedisi-masaji-peulimieom-jinjeonghan-hyusig-ui-chugbog

Hookah Lounge 광주키스방

Full Service Spa 하이오피주소

Why To Obtain A Poor Car Loan Now? 다바오 여자 대학교

It’s difficult to find knowledgeable people with this topic, however you seem like there’s more you are referring to! Thanks

Swedish Massage budal

Online Video Slot Game Tips 에볼루션 게임쇼

How For That Father Shark In Poker 필리핀 다바오 여자

Full Service Spa 부산달리기 – Ddhszz.Com –

Exclusive Nightlife 광주마사지

Adult Entertainment 알밤

Very good article! We are linking to this particularly great article on our website. Keep up the great writing.

Orchard Mastercard – Must I Sign Up? 두테르테 다바오

Happy Hour 광주알밤

Photo Recovery For The Sandisk Media Card 다바오 포커 다운로드

Social Gathering 알밤

Good post. I learn something new and challenging on websites I stumbleupon everyday. It will always be helpful to read through content from other authors and use something from their web sites.

So getting functionality limited to desktops sort of defeats the goal.

Here is my web blog: https://www.4shared.com/u/mBwIDOvW/darinarolincova576.html

Clubbing 부달

Chattanooga’s inhabitants increased by almost 50,000 in the 1970s.

This website was… how do you say it? Relevant!! Finally I have found something which helped me. Many thanks!

Straight hair will develop into wavy, wavy hair will grow to be curly and curly hair will develop into curlier.

Nonetheless, some states will let players aged 18+ to access some gambling merchandise.

Take a look at my web site … https://travis28.acidblog.net/62382544/expert-picks-for-betting-platforms-you-can-trust

The advised actual income casinos are trustworthy and safe to play at.

My blog https://upons.us/%EC%86%8C%EC%95%A1%EB%8C%80%EC%B6%9C%EC%9D%98-%EB%AA%A8%EB%93%A0-%EA%B2%83-%ED%95%84%EC%9A%94%EC%84%B1%EA%B3%BC-%ED%99%9C%EC%9A%A9-%EB%B0%A9%EB%B2%95/

Vibration is particularly effective for loosening up muscles and improving lymphatic drainage.

my web page; http://swedish5.trexgame.net/seuwedisi-chucheon-dangsin-i-al-aya-hal-modeun-geos

мега ссылка на тор

Спасибо!

Due to the way these web pages operate, they do not fall below traditional US gambling laws.

my webpage – https://titus30.smblogsites.com/31167590/tips-for-choosing-a-sports-betting-platform

Always.” by delivering thoughtful, heartfelt, forward-thinking service that upholds and builds upon this living legacy.

My page … https://ezalbaa.weebly.com/blog/6526692

Vintage slots – Vintage slots – Some players favor a bit of a classic Vegas-style slot encounter.

Check out my page – https://jolbeen.com/%EC%9D%80%ED%96%89-%EB%8C%80%EC%B6%9C-%EC%A0%81%EC%A0%88%ED%95%9C-%EC%84%A0%ED%83%9D%EC%9D%84-%EC%9C%84%ED%95%9C-%EB%AA%A8%EB%93%A0-%EA%B2%83/

You said it adequately..

Have a look at my web-site https://vidstreamr.com/@kathilepage75?page=about

I’d like to thank you for the efforts you have put in penning this website. I really hope to view the same high-grade content by you in the future as well. In fact, your creative writing abilities has inspired me to get my own site now 😉

Gamblers can choose from much more than 300 new and classic slots,

table and reside dealer games.

Private Club 광주오피

With thanks. An abundance of information!

Here is my webpage … https://cristian73.dgbloggers.com/31560041/what-makes-a-great-sports-betting-site

An intriguing discussion is worth comment. I think that you should write more about this subject, it may not be a taboo subject but generally folks don’t talk about these issues. To the next! Cheers.

Night Out 하이오피

Adam received his master’s in economics from The New School for Social Research and his Ph.D. from the University of Wisconsin-Madison in sociology.

My web site … https://misoodainjom.weebly.com/blog/8143205

With sportsbooks expected to arrive in MA in early 2023, there’s hope for Massachusetts on the internet casinos.

Check out my blog https://hollytierney.com/%EC%86%8C%EC%95%A1-%EB%8C%80%EC%B6%9C-%ED%94%8C%EB%9E%AB%ED%8F%BC%EC%9D%98-%ED%98%81%EC%8B%A0%EA%B3%BC-%ED%99%9C%EC%9A%A9%EB%B2%95/

When it comes to bonuses and promotions, couple of casinos on-line can hold a match to Wild.

Here is my web blog https://bamev.com/%EC%8A%AC%EB%A1%AF%EC%82%AC%EC%9D%B4%ED%8A%B8-%EC%98%A8%EB%9D%BC%EC%9D%B8-%EC%B9%B4%EC%A7%80%EB%85%B8%EC%9D%98-%EC%83%88%EB%A1%9C%EC%9A%B4-%EC%A4%91%EC%8B%AC%EC%A7%80/

Everyone loves it when folks get together and share thoughts. Great website, keep it up.

Thanks! I value this.

Also visit my webpage … https://francisco28.blogofchange.com/31710524/how-to-spot-a-reliable-sports-betting-site

Disney Vacation Club Hawaii Management Company, LLC is an equal opportunity employer.

Also visit my website; https://witty-deer-lcngtj.mystrikingly.com/blog/6863fa906ee

Good info. Lucky me I discovered your blog by accident (stumbleupon). I have saved as a favorite for later.

Fantastic stuff, Thanks a lot.

Look at my web blog: https://play.ophirstudio.com//@margartveasley?page=about

Downside: Cloudy water – hazy water which lacks readability.

Good info. Lucky me I recently found your website by chance (stumbleupon). I have saved as a favorite for later.

Kelly for my first comply with-up appointment.

This useful resource is a valuable companion for anybody seeking to realize a deeper understanding of depression and develop effective methods for managing it.

This is a topic that is near to my heart… Thank you! Exactly where can I find the contact details for questions?

An outstanding share! I’ve just forwarded this onto a co-worker who has been conducting a little homework on this. And he actually bought me dinner simply because I discovered it for him… lol. So allow me to reword this…. Thanks for the meal!! But yeah, thanx for spending time to discuss this topic here on your website.

Appreciate it. Plenty of postings.

Also visit my web-site: https://rootsofblackessence.com/@paulinamanzo8?page=about

Not only can you watch the dealers reside on-camera, but you can also chat with them, other players and even tip the dealer at the end of your hand.

Feel free to visit my web blog; https://bookcrossing-portugal.com/%ED%8C%8C%EC%9B%8C%EB%B3%BC%EA%B2%B0%EA%B3%BC%EC%98%88%EC%B8%A1-%EC%84%B1%EA%B3%B5%EC%9D%84-%EC%9C%84%ED%95%9C-%EC%A0%84%EB%9E%B5%EA%B3%BC-%ED%8C%81/

Everything is very open with a very clear explanation of the challenges. It was definitely informative. Your site is useful. Thanks for sharing!

9 . What Your Parents Taught You About Only Fans Pornstars Kayleigh Wanless Only Fans Pornstars Kayleigh Wanless (http://Gitlab.Ioubuy.Cn/Kayleighwanless4123)

Excellent website you have here but I was wondering if you knew of any message boards that cover the same topics talked about in this article? I’d really love to be a part of group where I can get comments from other experienced people that share the same interest. If you have any suggestions, please let me know. Many thanks!

Amazing article! This is really valuable for everyone planning to launch a venture. I came across several useful advice that I’ll be able to implement in my own enterprise. Thanks for sharing such useful insights. Can’t wait to checking out more articles from you! Keep it up! For more tips on startup strategies, check out this useful article: this link.

Great post. I am facing some of these issues as well..

как называют человека которого защищает адвокат

The Second March茅, lists medium-sized companies, while nouveau march茅 lists fast-growing start up companies seeking capital to finance expansion, linked to Euro.nm, the European equity growth market.

Talking to them will also help you learn about current market rates and how the region has evolved, as well as the potential for future growth.

Oh my goodness! Impressive article dude! Thank you, However I am going through difficulties with your RSS. I don’t understand why I can’t join it. Is there anybody else getting similar RSS problems? Anyone that knows the answer can you kindly respond? Thanx!!

Having read this I believed it was really informative.

I appreciate you finding the time and energy to put this information together.

I once again find myself spending a lot of time both reading and commenting.

But so what, it was still worthwhile! randka

badoo randki

randki

darmowe portale randkowe bez rejestracji

randka

randki

badoo randki

darmowe randki

darmowe portale randkowe bez rejestracji

darmowe portale randkowe bez rejestracji

darmowe randki bez opłat

randki facebook

badoo randki

darmowy portal randkowy

darmowe randki

randki24

badoo randki

bezpłatny portal randkowy

badoo randki

randki24

darmowe randki bez opłat

randki online

randka

badoo randki

badoo randki

randki online

randki24

darmowe randki bez opłat

randki24

randka

randki online

darmowe randki

randki za darmo

randka

badoo randki

randki

darmowe randki bez opłat

randki

randki24

randki

darmowe randki

randki online

darmowe portale randkowe bez rejestracji

randki24

darmowe randki bez opłat

badoo randki

randki24

randki24

darmowe portale randkowe bez rejestracji

randki

randki24

randki online

badoo randki

badoo randki

darmowe portale randkowe bez rejestracji

randki

bezpłatny portal randkowy

darmowy portal randkowy

randki za darmo

randki

bezpłatny portal randkowy

randki za darmo

randka

randki za darmo

randki facebook

darmowe randki bez opłat

randki facebook

randki24

darmowe portale randkowe bez rejestracji

randka

randka

randki online

randki facebook

darmowe portale randkowe bez rejestracji

bezpłatny portal randkowy

badoo randki

randki24

darmowe randki

darmowe randki

bezpłatny portal randkowy

badoo randki

darmowe randki bez opłat

darmowe randki bez opłat

darmowe randki bez opłat

bezpłatny portal randkowy

darmowe randki

randki24

randki24

darmowe randki

randki online

randka

badoo randki

randki24

darmowe randki

randki za darmo

badoo randki

randki24

darmowy portal randkowy

randki online

randki za darmo

darmowe randki bez opłat

darmowe randki bez opłat

randki za darmo

bezpłatny portal randkowy

randki

badoo randki

randki24

darmowe portale randkowe bez rejestracji

randki24

badoo randki

darmowe randki bez opłat

randki online

randki za darmo

randki24

randka

randki za darmo

randki za darmo

darmowy portal randkowy

darmowe portale randkowe bez rejestracji

darmowy portal randkowy

randki24

darmowy portal randkowy

randki

darmowe portale randkowe bez rejestracji

badoo randki

randki facebook

badoo randki

randki

darmowe randki

randka

randki24

randki online

badoo randki

randki za darmo

darmowy portal randkowy

randki

bezpłatny portal randkowy

randki24

bezpłatny portal randkowy

randki online

randki za darmo

randki facebook

randka

randka

badoo randki

randki24

bezpłatny portal randkowy

darmowy portal randkowy

bezpłatny portal randkowy

darmowe randki bez opłat

randki za darmo

bezpłatny portal randkowy

badoo randki

randki za darmo

darmowy portal randkowy

randka

randki za darmo

darmowe portale randkowe bez rejestracji

randka

darmowe randki bez opłat

badoo randki

darmowy portal randkowy

randki za darmo

bezpłatny portal randkowy

darmowy portal randkowy

randki24

randki online

randki facebook

randki24

randki online

randki facebook

randki za darmo

darmowe portale randkowe bez rejestracji

badoo randki

randka

randki

randki za darmo

randki za darmo

randki24

darmowe portale randkowe bez rejestracji

badoo randki

darmowe randki

randki facebook

darmowy portal randkowy

randki24

darmowe randki

darmowy portal randkowy

darmowe portale randkowe bez rejestracji

bezpłatny portal randkowy

randki online

darmowy portal randkowy

darmowe randki bez opłat

randki

bezpłatny portal randkowy

randki

darmowe randki bez opłat

randki online

randka

darmowe portale randkowe bez rejestracji

randki za darmo

bezpłatny portal randkowy

randki za darmo

darmowy portal randkowy

badoo randki

darmowe randki

badoo randki

darmowe randki bez opłat

badoo randki

randki facebook

bezpłatny portal randkowy

randki

bezpłatny portal randkowy

randki online

darmowy portal randkowy

darmowy portal randkowy

randka

randki24

randki24

randka

badoo randki

darmowe portale randkowe bez rejestracji

darmowy portal randkowy

darmowe portale randkowe bez rejestracji

darmowe portale randkowe bez rejestracji

randka

darmowe randki

randki

randki za darmo

darmowe randki bez opłat

badoo randki

randki24

randki

randki24

randki24

randki24

badoo randki

bezpłatny portal randkowy

randki24

darmowe randki bez opłat

darmowe randki bez opłat

badoo randki

randki24

randki facebook

randki

randki online

randki online

randki24

randki

bezpłatny portal randkowy

darmowe randki bez opłat

darmowe randki

bezpłatny portal randkowy

bezpłatny portal randkowy

badoo randki

badoo randki

randki za darmo

randki24

randki

randka

randki za darmo

randki online

badoo randki

darmowe randki

darmowe randki bez opłat

darmowe portale randkowe bez rejestracji

badoo randki

bezpłatny portal randkowy

darmowy portal randkowy

darmowy portal randkowy

randki facebook

randki za darmo

darmowy portal randkowy

darmowe randki

bezpłatny portal randkowy

randki online

darmowe randki

badoo randki

randka

randka

bezpłatny portal randkowy

randki online

darmowy portal randkowy

darmowe randki bez opłat

darmowe randki bez opłat

badoo randki

randki

randki24

bezpłatny portal randkowy

randki facebook

randki facebook

randki

randki online

randki

bezpłatny portal randkowy

randka

randki

badoo randki

randki24

randki za darmo

darmowe randki

badoo randki

randki za darmo

bezpłatny portal randkowy

randki online

randki online

darmowy portal randkowy

randki24

randki za darmo

randki24

badoo randki

randki online

randki online

darmowe randki bez opłat

bezpłatny portal randkowy

darmowe randki

randki24

badoo randki

randki facebook

badoo randki

randki facebook

randki online

darmowe randki

bezpłatny portal randkowy

darmowy portal randkowy

randki za darmo

randka

randki online

bezpłatny portal randkowy

randki online

randka

randki

darmowe randki bez opłat

randki24

darmowe portale randkowe bez rejestracji

darmowe portale randkowe bez rejestracji

darmowe randki

darmowe portale randkowe bez rejestracji

darmowy portal randkowy

darmowy portal randkowy

badoo randki

darmowe randki

randki za darmo

darmowy portal randkowy

darmowe randki

darmowe randki bez opłat

darmowe randki bez opłat

darmowe randki bez opłat

randki

darmowe randki

badoo randki

randki za darmo

darmowe portale randkowe bez rejestracji

randki24

darmowe portale randkowe bez rejestracji

darmowe randki bez opłat

randki24

darmowe portale randkowe bez rejestracji

randka

randki24

randka

randki24

badoo randki

randki24

randki

darmowy portal randkowy

badoo randki

bezpłatny portal randkowy

bezpłatny portal randkowy

bezpłatny portal randkowy

randka

bezpłatny portal randkowy

darmowe portale randkowe bez rejestracji

darmowy portal randkowy

darmowe portale randkowe bez rejestracji

darmowy portal randkowy

darmowy portal randkowy

randki24

bezpłatny portal randkowy

badoo randki

randka

badoo randki

randki24

darmowe randki

randki24

bezpłatny portal randkowy

darmowe randki bez opłat

darmowe randki

randki za darmo

darmowe randki bez opłat

randki za darmo

darmowy portal randkowy

randki

randki facebook

darmowe portale randkowe bez rejestracji

darmowe randki bez opłat

darmowe portale randkowe bez rejestracji

bezpłatny portal randkowy

randki24

bezpłatny portal randkowy

bezpłatny portal randkowy

randki24

darmowy portal randkowy

randki24

randki za darmo

randki

randki

randka

darmowe randki bez opłat

darmowy portal randkowy

badoo randki

darmowe portale randkowe bez rejestracji

randki24

darmowe randki

darmowe randki bez opłat

randki facebook

darmowe portale randkowe bez rejestracji

randki24

randka

darmowe randki

randki za darmo

randki24

darmowe randki

darmowe randki bez opłat

bezpłatny portal randkowy

randki24

randki24

darmowe randki

randka

darmowe portale randkowe bez rejestracji

darmowy portal randkowy

randki24

bezpłatny portal randkowy

randki facebook

darmowe randki

bezpłatny portal randkowy

badoo randki

badoo randki

darmowy portal randkowy

randki online

randka

darmowe portale randkowe bez rejestracji

randki online

darmowe randki

badoo randki

randka

randki za darmo

darmowe randki

darmowe randki bez opłat

randki

randki za darmo

darmowe portale randkowe bez rejestracji

randki24

randki

randka

darmowe portale randkowe bez rejestracji

randki za darmo

randka

bezpłatny portal randkowy

randki facebook

randki24

darmowe portale randkowe bez rejestracji

badoo randki

randki za darmo

randki24

randki online

randki za darmo

randka

randki za darmo

badoo randki

darmowy portal randkowy

randki za darmo

bezpłatny portal randkowy

randki

darmowe randki bez opłat

randki facebook

bezpłatny portal randkowy

randka

bezpłatny portal randkowy

darmowe randki bez opłat

randki

randka

randka

randki24

randki

randka

randki online

randki online

bezpłatny portal randkowy

randki online

randki za darmo

darmowe randki bez opłat

darmowe randki

randki24

darmowe randki

randki24

darmowe randki bez opłat

darmowe randki

darmowe portale randkowe bez rejestracji

randki online

badoo randki

darmowy portal randkowy

randki

randki za darmo

darmowe randki

randki online

darmowe randki bez opłat

badoo randki

randki24

randki za darmo

randki za darmo

randki facebook

randki24

darmowe portale randkowe bez rejestracji

randki

randka

bezpłatny portal randkowy

badoo randki

randki24

randki

randki online

randki online

randki24

randki online

randki

darmowe randki bez opłat

randki za darmo

randki facebook

randki24

randki24

bezpłatny portal randkowy

darmowe portale randkowe bez rejestracji

randki facebook

bezpłatny portal randkowy

darmowe randki

randki za darmo

darmowe randki bez opłat

randki facebook

randki24

randki

randki online

badoo randki

darmowe portale randkowe bez rejestracji

randka

bezpłatny portal randkowy