CPI: It’s All About Housing

Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

This week, all eyes will again be on CPI data to assess how the Fed will likely move policy. So far this year, we have experienced a significant bout of disinflation amidst an elevated inflation trend. We think there is still some of this disinflation ahead of us; however, the speed of disinflation is likely to slow, and we will start getting clarity on what kind of inflation average we will settle at. We have done well so far in riding this wave thus far. However, we think what lies ahead will likely differ from what has recently passed. We have explained our thinking in-depth in our latest Month In Macro report:

Summarily: We think that to get inflation down in a manner consistent with 2% inflation or less, the Fed will need to induce a recession. Only after several months of recessionary numbers will real GDP be hurt enough to bring down nominal spending to contain inflation.

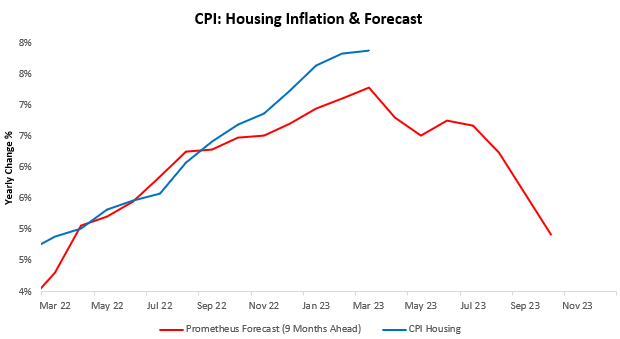

It is in this context that we turn to the upcoming CPI print. Our systems imply a range of 0.24% to 0.39% in month-on-month CPI. This is a relatively large range, largely due to the potential for housing decelerations. As we have documented previously, there is a lagged pass-through from home price to CPI housing and by our estimates, the window for the pass-through of declining home prices has likely begun:

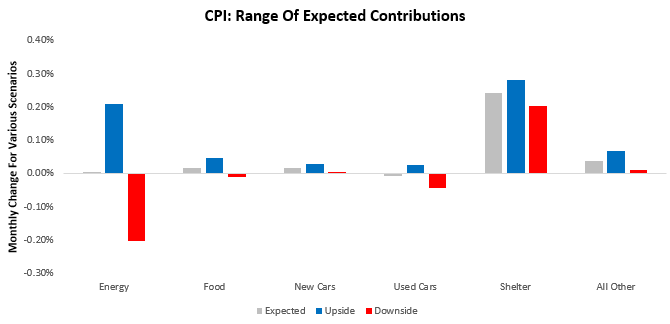

However, we think it is essential to recognize that this is a slow-moving cyclical force, and it is hard to time this pass through with a high degree of accuracy in monthly prints. Nonetheless, we must keep in mind this is a significant headwind for inflation and that odds increasingly favor disinflationary forces from this as months carry on. Below, we show our range of expected contributions to headline CPI broken into 6 categories that we believe to be dominant drivers at this junction: energy, food, new & used vehicles, shelter, ad all other components. We the range of our expectations on the upside and downside.

As we can see above, shelter is likely to be the dominant driver of this print (as always), with energy showing the potential to disrupt headline CPI. However, we judge energy as unlikely to be a very meaningful surprise as the breath of energy price changes is not very supportive. We expect motor fuel and electricity prices to rise and fuel oil and electricity to fall. Given recent energy trends, we expect any smoothing factors from the BLS to favor downside versus upside.

Additionally, we see some potential for used car prices to surprise to the upside; this could, at the extreme, add about 0.07% to headline CPI, resulting in a surprise if all other components come in in-line with consensus expectations. Below, we show our recently upgraded CPI forecasts over time:

Overall, this is a report to digest to understand if housing inflation has begun to slow and whether used car prices have stabilized.