Business Sales: Weakness Persists

Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

The next stage in this business cycle will be determined by whether the labor market can continue to support spending. The Fed is currently trying to tame inflation by creating a softer labor market. The tool they have to do so is interest rates. By increasing interest rates, they hope to facilitate higher interest burdens, which drags on profitability. When profitability contracts, businesses have typically responded by laying-off employees. While this approach works well to cut costs at the firm level, at the macroeconomic level, this reduces total employment, which reduces total spending. Reduced spending leads to lower revenues, which hurts profits further, causing further lay-offs, i.e., a self-reinforcing downward spiral. Therefore, the key variables to track today are business revenues relative to their costs. Yesterday, we received more incremental information on business revenues.

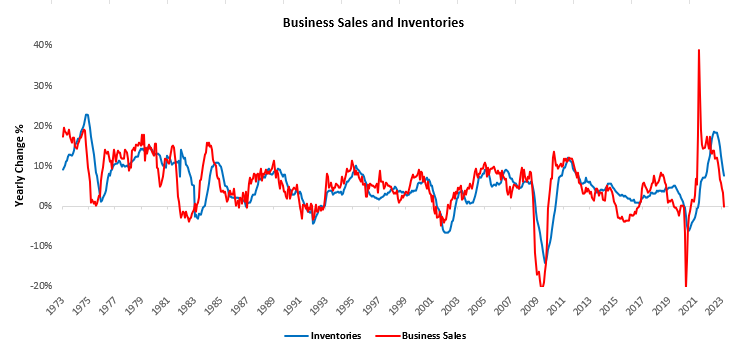

The latest data shows us that nominal business sales continued to slow down through March, now at 0% growth versus last year. Inventory growth continues to follow sales growth lower, as inventories are managed based on sales:

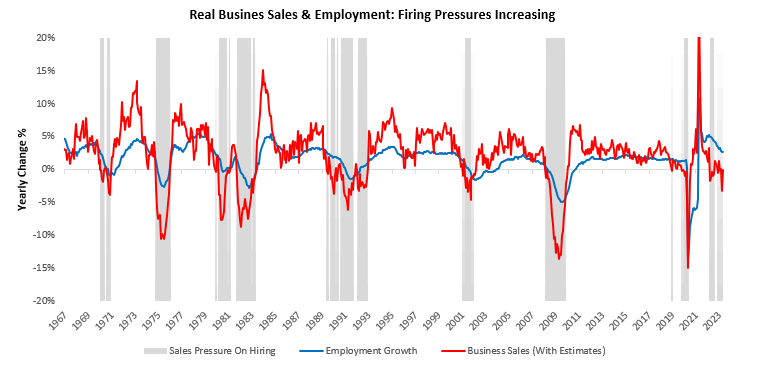

This decline in nominal sales will likely cause a further deterioration in inventory growth, which will flow through to GDP in the form of a further inventory drawdown. Additionally, real sales growth is currently below employment growth, suggesting downward pressures on future hiring. The divergence between sales & hiring is significant relative to history, suggesting strong downward pressure on future employment:

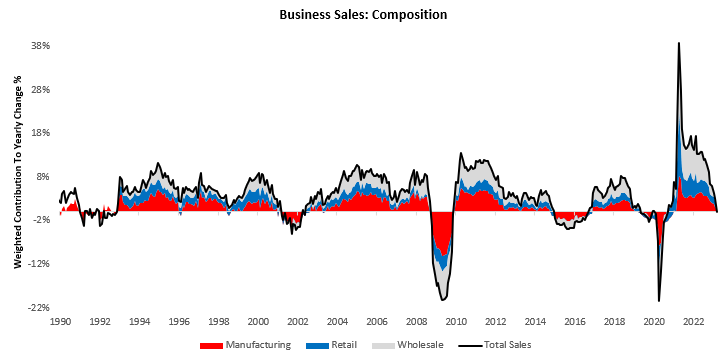

Specifically, we received new data in the form of wholesalers’ sales & revisions to their inventory numbers. The latest wholesale sales data disappointed expectations, with a monthly change of -2.1% versus the expected 0.4%. This data resulted in a -1.5% decrease in total nonfarm sales- with manufacturing, retail, and wholesale contributing -0.03%, -0.26%, and-0.77%, respectively. We show their relative contributions to sales activity over the last year:

Of these categories, wholesale sales remain the weakest link. As mentioned, wholesale sales weakened significantly in March (-2%), and the weakness remained broad-based. We show the major drivers of this change below:

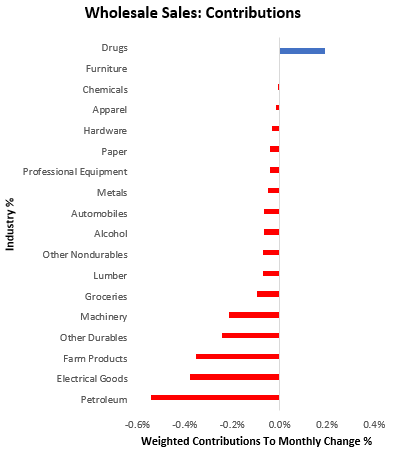

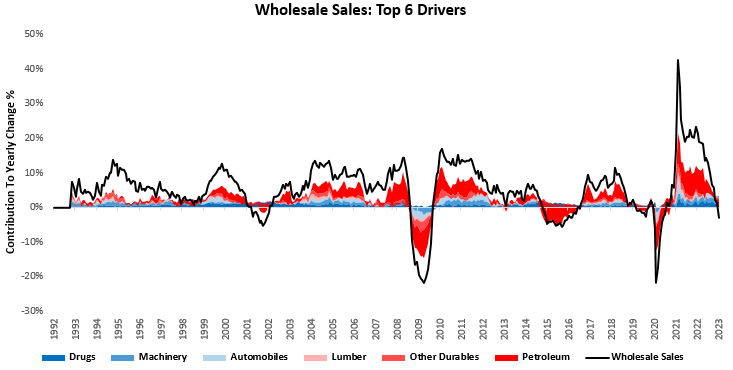

Below, we zoom out to show the 6 major drivers of strength in shades of blue and weakness in shades of red:

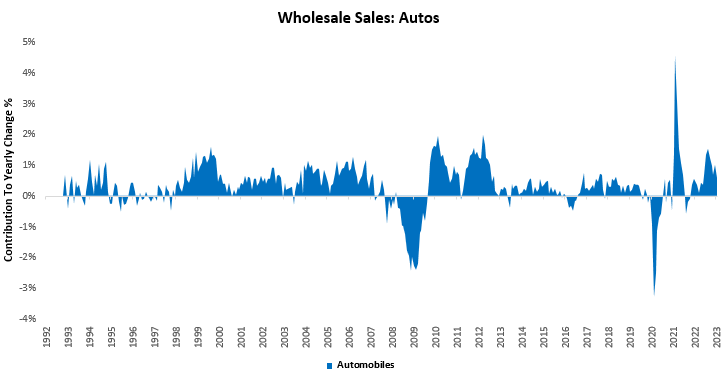

As we can see, wholesale sales of petroleum, durables, and lumber continue to weigh on business sales. Part of this decline is likely due to price declines in these segments. On the other hand, areas like automobiles continue to show strength. We zoom in on automobiles as it has typically more sensitive to changing credit conditions. We currently see little weakness in the yearly trend in wholesalers’ sales of automobiles:

Overall, the latest sale data continue to point to cyclical pressures on businesses. The breadth of weakness in the wholesale sector was telling in this report, implying weak business conditions. Labor conditions remain more steady than business conditions; eventually, these two will have to reconcile.

Hey! Do you know if they make any plugins to assist with Search Engine Optimization? I’m trying to get my

site to rank for some targeted keywords but I’m not seeing very good gains.

If you know of any please share. Thank you! You can read

similar art here: Eco product

Hello there! Do you know if they make any plugins to assist with Search Engine Optimization?

I’m trying to get my site to rank for some targeted keywords but I’m not seeing very good results.

If you know of any please share. Cheers! You can read similar article here: Change your life

I’m really inspired along with your writing skills as smartly as

with the structure on your weblog. Is that this a paid subject or did you modify

it your self? Either way stay up the excellent high quality writing,

it’s uncommon to look a nice weblog like this one nowadays.

Instagram Auto comment!

I am extremely inspired with your writing talents and also with the layout on your blog.

Is this a paid topic or did you customize it your

self? Either way stay up the nice high quality writing, it

is uncommon to see a great blog like this one nowadays.

Leonardo AI x Midjourney!

I am extremely inspired together with your writing abilities and also with the layout for your blog. Is this a paid subject matter or did you customize it your self? Either way keep up the excellent quality writing, it’s uncommon to look a nice weblog like this one today. I like prometheus-research.com ! My is: TikTok Algorithm

I am extremely inspired together with your writing talents as smartly as with the structure on your blog.

Is that this a paid topic or did you customize it

yourself? Either way keep up the nice high quality

writing, it is rare to peer a great weblog like this one nowadays.

Leonardo AI x Midjourney!

anabolika und hgh kaufen

steroid dealer