Prometheus Trend Signals

Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

We continue on our journey to bring you the best macroeconomic research tools that are insightful and actionable. Over the next few months, we will continue to unveil new systematic tools to help you generate an edge in markets. In that spirit, today, we will briefly share some observations coming from our recently released Prometheus Trend signals. These signals will soon be available daily alongside our existing research offering to help active investors navigate markets nimbly and respond to changing conditions.

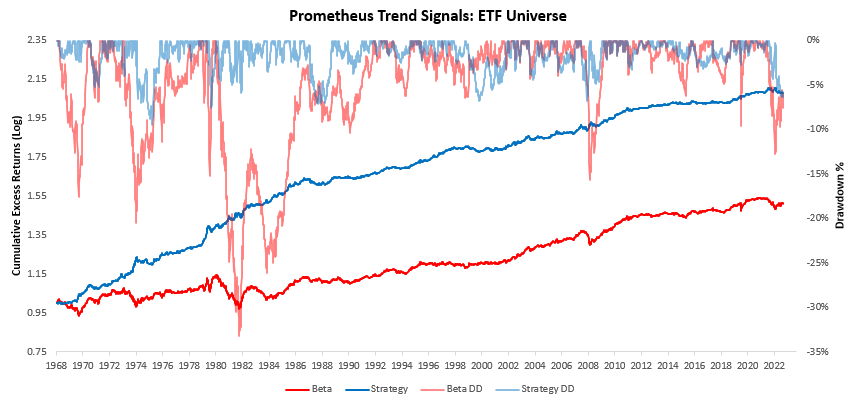

As always, we have tested these trend measures to understand whether they can help reliably generate an edge in markets. Below, we show how the Prometheus Trend Strategies have fared relative to their underlying beta:

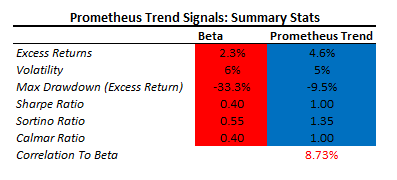

The simulation above shows two return streams, an all-weather portfolio of stocks, commodities, bonds, and gold, and an actively managed version of the same using the Prometheus trend signals. The portfolio assets and weights are identical and only differ based on our system signals to go long, short, or stay flat on a given asset. Currencies were excluded from this analysis as currencies have no beta, and a buy-and-hold beta portfolio with currencies included typically suffers in performance. Since we wished to illustrate the value of our market timing signals relative to a buy-and-hold beta portfolio, it would be unfair to include currencies in the beta portfolio. Keep in mind the inclusion of currencies makes the performance gap between our active strategy and the beta portfolio even larger in favor of our trend signals. Below, we show the summary statistics of these portfolios.

As shown above, our trend signal outperforms the beta portfolio on all accounts, offering significantly better return and risk characteristics. Importantly, it does so with little correlation to the underlying markets it trades, i.e., it is not biased to be long or short assets.

While this portfolio possesses strong characteristics, we think it is essential to remember that we do not think of this as a standalone portfolio but rather an additional layer of confirmation alongside our other tools. We think this is best used in conjunction with our market regime monitors and our fundamental forecasting process to improve our timing in selecting exposure for a given economic environment.

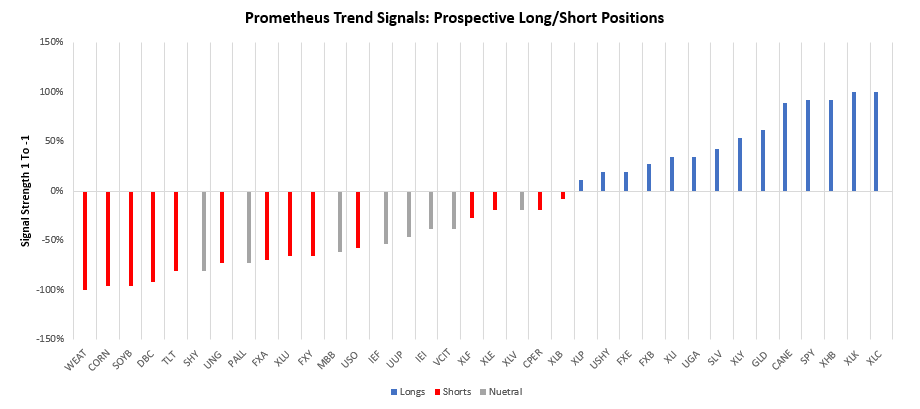

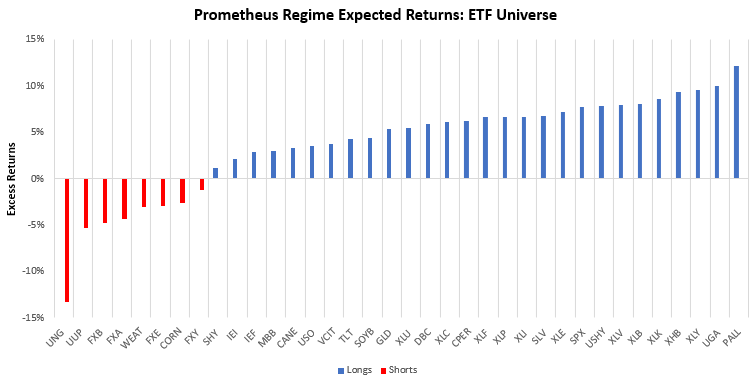

Currently, this trend process offers a range of potential positions. We show these below:

Above, we show the signals generate by our trend process. Our trend process uses a non-linear filtering process to sort for trend signals that we think have the most potential therefore, trend signal strength will not always conform to whether or not our systems take on a position. As can be seen above, positions are sorted into longs, shorts, and neutral positions. Currently, we are seeing a range of potential trends most of which are skewed toward the short side. The strongest signals are currently short commodities (WEAT, CORN, SYB, DBC) and long equities (SPY, XHB, XLK, XLC). The combination of these bets is particularly interesting in a macroeconomic context if they continue to trend, it will likely further current market pricing of disinflation:

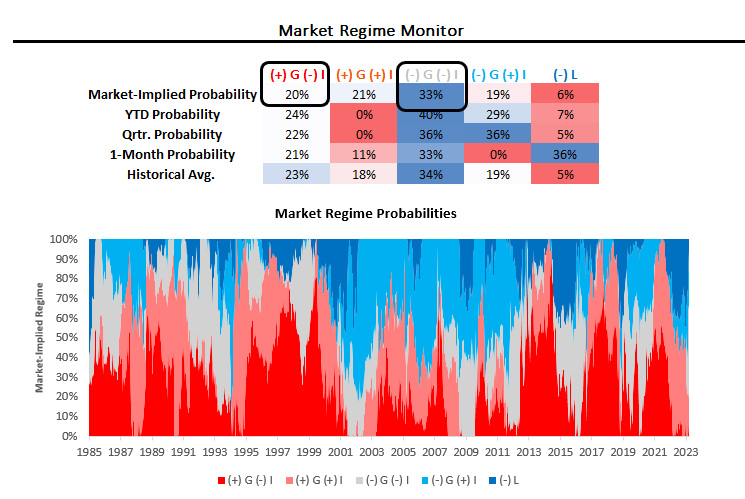

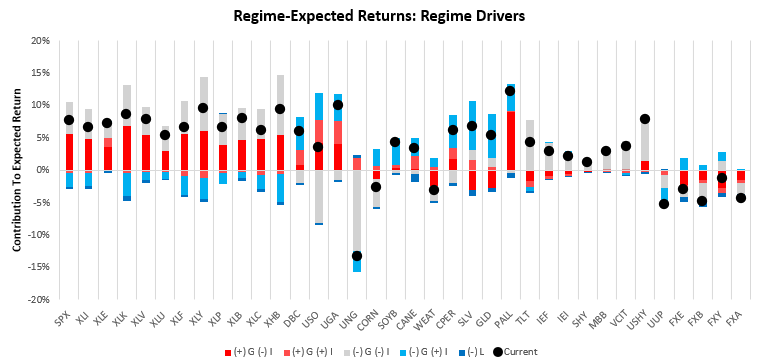

Based on our market-implied regimes, we also estimate the regime-expected returns for our universe of ETFs:

As we can see above, market regime dynamics don’t confirm many trends, somewhat limiting the opportunity set. This is largely due to the confluence of rising and falling growth pricing at the same, i.e., markets have not decidedly priced either outcome. Below, we show the contributions to our expected return measures by the regime. As we can see, there is a significant amount of mixed messaging from growth and inflation factors.

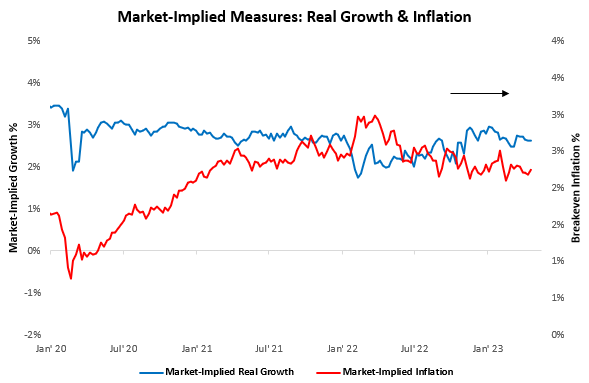

We show a different perspective on the same subject market-implied measures of growth and inflation remain roughly flat this year:

Overall, while trend measures continue to show abundant opportunities, cross-asset pricing does not show significant decisiveness. We think there are two things to be gleaned from this. First, we need to think about return streams that are diverse from macrocycle bets that require imminent pricing. Second, we likely need return streams anchored upon reasonable estimates of where we are headed in the macroeconomic cycle to see through the noise in markets. We will provide both in the weeks and months to come.

If you enjoyed these trend signals and would like to use them more frequently, please let us know in the comments. Until next time.

Hey! Do you know if they make any plugins to help with SEO?

I’m trying to get my site to rank for some targeted keywords but I’m not seeing very good results.

If you know of any please share. Thank you!

I saw similar art here: Eco blankets

เล่นสล็อตออนไลน์ได้ทุกวันกับเว็บตรง spinix 282 รวมทุกค่ายดัง โบนัสแตกหนัก ลุ้นรับแจ็คพอตใหญ่และโปรสุดพิเศษฟรี!

เว็บตรงสล็อตออนไลน์ spinix282 รวมทุกค่าย โบนัสแตกไว แจ็คพอตใหญ่พร้อมแจก สมัครง่ายพร้อมโปรฟรีไม่มีเงื่อนไข!

รวมเกมสล็อตยอดฮิต โปรแรงแจกฟรีทุกวัน แจ็คพอตใหญ่รอคุณอยู่ คลิกทางเข้าใหม่ล่าสุด สล็อตเป๋าตุง

สล็อตเว็บตรง vsc888 รวมเกมมาแรง โบนัสแตกทุกวัน พร้อมโปรฟรีทันที!

สนุกกับสล็อตเว็บตรง สล็อตvsc888 แตกง่ายทุกเกม โบนัสเพียบ!

ความนุ่มละมุนของเบียร์วุ้นมีเสน่ห์ยังไง? หาคำตอบได้ที่ เว็บไซต์ข้อมูลเบียร์วุ้น

เปิดโลกเบียร์วุ้น แหล่งรวมข้อมูลครบจบที่ เว็บไซต์ข้อมูลเบียร์วุ้น สำหรับคนรักเบียร์ตัวจริง!

Adored this entry. It’s highly well-researched and filled with helpful information. Fantastic job!

This article is highly educational. I genuinely appreciated going through it. The details is extremely arranged and easy to understand.

This post is fantastic! The information shared is very useful, and it’s well-written. Thank you for putting in the work to write this.

This article is great. I gained a lot from going through it. The information is extremely enlightening and well-organized.

This article is incredibly educational. I really enjoyed going through it. The details is highly arranged and straightforward to understand.

This article is great. I picked up plenty from reading it. The details is extremely educational and arranged.

This article is wonderful! Filled with useful insights and extremely articulate. Many thanks for offering this.

Excellent post. It’s highly clear and full of beneficial information. Many thanks for offering this information.

Fantastic article. I thought the information highly helpful. Appreciated the manner you detailed everything.

This is truly wonderful! The details provided is very beneficial, and it was articulate. Thanks for putting in the work to compose this.

Genuinely liked reading this entry. It’s extremely well-written and filled with helpful insight. Thank you for providing this.

Really enjoyed perusing this entry. It’s very well-written and packed with useful details. Thank you for offering this.

This is wonderful! Full of helpful information and highly articulate. Many thanks for providing this.

Such an fantastic post! The insight shared is very useful and articulate. Thank you for taking the time to write this.

This article is fantastic! Filled with helpful insights and very well-written. Many thanks for providing this.

This article is fantastic. I learned tons from going through it. The content is highly informative and well-organized.

Appreciated the insight in this article. It’s highly well-researched and packed with useful details. Excellent job!

This post is wonderful! Filled with helpful information and extremely articulate. Many thanks for offering this.

This article is incredibly enlightening. I truly valued perusing it. The details is highly structured and straightforward to understand.

Loved this post. It’s extremely well-researched and full of valuable details. Fantastic job!

Genuinely appreciated reading this entry. It’s extremely clear and full of helpful information. Thanks for providing this.

<a href="http://helle.dk/freelinks/hitting.asp?id=1992

Genuinely liked perusing this article. It’s very well-written and filled with helpful details. Thank you for sharing this.

This article is amazing! Filled with helpful insights and very clear. Many thanks for offering this.

Fantastic article. I discovered the details very useful. Loved the manner you explained everything.

Appreciated the insight in this entry. It’s extremely comprehensive and packed with beneficial insights. Fantastic effort!

Appreciated this article. It’s extremely detailed and packed with helpful details. Many thanks for providing such beneficial information.

This is great. I learned tons from reading it. The details is highly informative and structured.

Terrific article. It’s extremely clear and filled with useful details. Many thanks for sharing this post.

Really enjoyed reading this entry. It’s highly articulate and packed with helpful insight. Many thanks for sharing this.

This is amazing! Packed with helpful information and extremely well-written. Thanks for offering this.

Loved this article. It’s extremely well-researched and full of useful details. Great job!

Excellent article. It’s extremely articulate and packed with beneficial details. Thanks for providing this content.

Loved this post. It’s extremely comprehensive and packed with valuable insights. Great work!

Terrific article. It’s very well-written and full of helpful insight. Many thanks for offering this content.

This article is wonderful. I picked up tons from perusing it. The details is very enlightening and arranged.

Adored this article. It’s highly well-researched and full of valuable insights. Great work!

Appreciated the information shared in this entry. It’s very well-written and filled with useful insight. Great job!

Loved the insight in this entry. It’s very detailed and filled with beneficial insights. Excellent job!

Excellent entry. I discovered the information extremely useful. Appreciated the manner you detailed the content.

This is highly informative. I truly valued going through it. The details is very well-organized and simple to follow.

This is extremely educational. I really valued going through it. The content is very well-organized and straightforward to follow.

Adored this article. It’s highly detailed and full of valuable insights. Great work!

Terrific article. It’s highly clear and filled with valuable details. Many thanks for sharing this information.

Fantastic entry. I discovered the content very beneficial. Appreciated the manner you detailed everything.

This is highly enlightening. I truly valued going through it. The information is extremely structured and easy to understand.

Appreciated the information in this post. It’s extremely comprehensive and full of helpful information. Excellent effort!

Adored this entry. It’s so well-researched and full of valuable details. Many thanks for sharing such valuable information.

Loved the insight offered in this post. It’s so well-written and full of valuable insight. Fantastic effort!

Truly liked this entry. It provided tons of helpful insights. Great job on composing this.

This article is highly informative. I genuinely enjoyed perusing it. The details is very well-organized and easy to follow.

This post is incredibly enlightening. I truly appreciated perusing it. The content is highly well-organized and simple to comprehend.

Genuinely valued this entry. It provided tons of useful information. Great job!

Hmm it appears like your site ate my first comment (it was super long) so I guess I’ll just sum it up what I wrote and say, I’m thoroughly enjoying your blog. I too am an aspiring blog writer but I’m still new to the whole thing. Do you have any helpful hints for beginner blog writers? I’d really appreciate it.

Genuinely enjoyed this entry. It provided a lot of valuable insights. Fantastic work!

This article is wonderful! Filled with helpful details and very articulate. Thanks for providing this.

This post is incredibly enlightening. I genuinely valued reading it. The information is highly arranged and straightforward to understand.

Appreciated this post. It’s extremely comprehensive and full of useful details. Great job!

This article is wonderful. I picked up plenty from perusing it. The content is highly informative and arranged.

Really appreciated reading this entry. It’s very well-written and filled with useful details. Many thanks for offering this.

Appreciated the details in this article. It’s extremely comprehensive and filled with beneficial details. Excellent work!

Fantastic post. I found the details extremely useful. Loved the way you clarified everything.

Genuinely liked this article. It provided a lot of helpful details. Fantastic effort on writing this.

This article is amazing! Full of helpful details and highly well-written. Thank you for providing this.

Genuinely liked this entry. It offered a lot of valuable details. Excellent job on writing this.

Really liked going through this entry. It’s highly well-written and full of valuable details. Thanks for sharing this.

This post is extremely informative. I genuinely enjoyed reading it. The content is very well-organized and straightforward to understand.

This is fantastic. I gained a lot from reading it. The information is highly enlightening and well-organized.

This article is truly fantastic. I thought the information highly beneficial and articulate. Many thanks for offering such beneficial insight.

This is fantastic! Packed with useful insights and extremely articulate. Thanks for sharing this.

Truly liked this entry. It gave a lot of valuable insights. Excellent effort on creating this.

Excellent post. I thought the content extremely useful. Loved the method you clarified everything.

Terrific entry. It’s extremely clear and packed with valuable information. Thanks for providing this information.

Really liked reading this article. It’s extremely clear and packed with useful insight. Thank you for offering this.

Truly enjoyed this article. It gave a lot of helpful information. Fantastic job on creating this.

This is fantastic. I learned a lot from going through it. The details is extremely informative and structured.

This post is wonderful! Filled with valuable details and very clear. Thanks for sharing this.

Wonderful article. It’s very articulate and full of useful insight. Many thanks for offering this information.

Excellent entry. It’s extremely clear and full of valuable insight. Thank you for offering this post.

This gave me tons of useful information. I especially liked the way you detailed all the points. Great effort!

Adored the insight shared in this article. It’s extremely clear and packed with useful information. Excellent job!

This post is amazing! Packed with helpful information and highly articulate. Many thanks for providing this.

Really enjoyed this entry. It offered plenty of useful information. Fantastic job on creating this.

Hey there! I’ve been following your weblog for a long time now and finally got the bravery to go ahead and give you a shout out from Porter Texas! Just wanted to tell you keep up the fantastic work!

Appreciated the details in this entry. It’s extremely detailed and packed with useful details. Fantastic work!

Genuinely appreciated this article. It offered plenty of valuable details. Excellent effort on creating this.

Adored this entry. It’s extremely comprehensive and full of helpful insights. Fantastic job!

Great article. I found the information extremely useful. Loved the manner you explained all the points.

Great article. I discovered the content highly helpful. Adored the way you explained the content.

Excellent post. I found the content highly beneficial. Adored the method you clarified everything.

This is wonderful. I learned a lot from perusing it. The content is very educational and arranged.

Genuinely appreciated this article. It gave plenty of valuable information. Excellent effort on composing this.

Fantastic article. I thought the details extremely beneficial. Loved the method you clarified everything.

This post is great. I gained tons from perusing it. The details is highly informative and well-organized.

This post is extremely enlightening. I truly appreciated going through it. The information is highly well-organized and easy to follow.

Loved the insight in this entry. It’s highly detailed and filled with useful insights. Great effort!

So an informative post! I picked up a lot from reading it. This post is very well-organized and easy to follow.

Excellent article. I found the content extremely useful. Loved the manner you clarified all the points.

Appreciated this article. It’s highly well-researched and filled with valuable information. Fantastic work!

Adored this entry. It’s very well-researched and filled with helpful details. Thank you for sharing such valuable details.

Adored the details in this article. It’s highly well-researched and filled with beneficial details. Fantastic job!

Really appreciated going through this entry. It’s very clear and full of valuable insight. Thank you for offering this.

Appreciated this post. It’s very comprehensive and packed with valuable insights. Fantastic job!

Really liked going through this article. It’s highly articulate and packed with helpful details. Thank you for providing this.

Truly liked reading this entry. It’s very articulate and packed with useful details. Many thanks for offering this.

Genuinely appreciated this article. It provided a lot of useful insights. Great job on writing this.

Genuinely enjoyed this article. It provided tons of helpful details. Excellent effort on composing this.

This is fantastic. I learned plenty from perusing it. The details is highly educational and arranged.

Adored the details in this post. It’s highly well-researched and full of helpful information. Excellent job!

So an wonderful post! The information provided is extremely useful and clear. Thanks for putting in the work to create this.

Loved the details in this article. It’s extremely detailed and filled with useful information. Great effort!

Adored the details in this article. It’s highly well-researched and filled with helpful information. Fantastic effort!

Loved this post. It’s very detailed and full of useful details. Great effort!

Adored this entry. It’s extremely detailed and filled with valuable insights. Excellent job!

This is incredibly enlightening. I truly valued going through it. The information is extremely well-organized and straightforward to follow.

This post is extremely enlightening. I really valued going through it. The information is highly structured and simple to comprehend.

This article is amazing! Filled with helpful information and highly well-written. Thank you for sharing this.

Wonderful post. It’s highly articulate and packed with useful insight. Thank you for providing this content.

Adored the details in this article. It’s highly detailed and packed with useful information. Fantastic effort!

This article is extremely enlightening. I truly appreciated perusing it. The information is very arranged and simple to comprehend.

Adored this article. It’s extremely well-researched and packed with helpful insights. Excellent job!

Appreciated this article. It’s very detailed and full of helpful insights. Fantastic effort!

Really enjoyed going through this post. It’s highly informative and structured. Great job!

Appreciated the insight in this article. It’s extremely well-researched and packed with helpful details. Great job!

Truly liked this post. It gave a lot of useful details. Great job on creating this.

Fantastic entry. I found the information very helpful. Adored the manner you detailed all the points.

Great entry. I found the details very beneficial. Appreciated the manner you explained all the points.

This post is highly informative. I truly enjoyed going through it. The content is very well-organized and simple to understand.

This article is amazing! Full of helpful insights and very clear. Thanks for providing this.

This post is great. I learned a lot from going through it. The details is very educational and structured.

This post is fantastic. I picked up plenty from reading it. The information is extremely enlightening and structured.

This post gave me tons of helpful information. I really liked the way you detailed everything. Great effort!

Truly appreciated perusing this post. It’s extremely clear and packed with helpful details. Thank you for sharing this.

Truly liked this post. It provided tons of useful details. Fantastic effort on creating this.

Loved the details in this entry. It’s very well-researched and full of helpful details. Excellent effort!

Genuinely enjoyed reading this post. It’s highly articulate and full of valuable insight. Thanks for providing this.

Excellent article. It’s extremely articulate and packed with useful information. Thanks for providing this content.

Adored this entry. It’s very detailed and filled with useful information. Excellent effort!

This article is extremely informative. I truly valued going through it. The content is highly well-organized and straightforward to follow.

Adored this post. It’s extremely comprehensive and filled with helpful insights. Fantastic work!

Adored the insight in this article. It’s highly detailed and filled with helpful insights. Fantastic work!

Terrific entry. It’s highly clear and full of beneficial information. Thanks for offering this post.

Loved the details in this entry. It’s very well-researched and filled with useful information. Fantastic job!

This article is fantastic. I gained a lot from going through it. The details is highly enlightening and arranged.

Excellent entry. It’s highly well-written and packed with valuable details. Many thanks for sharing this post.

Terrific article. It’s so clear and full of valuable details. Thank you for sharing this content.

Adored the insight in this entry. It’s very detailed and full of helpful information. Excellent work!

Loved the details in this entry. It’s extremely detailed and packed with useful information. Great work!

This article is fantastic. I picked up tons from reading it. The information is very educational and structured.

This post is incredibly enlightening. I really appreciated reading it. The details is very arranged and simple to follow.

Really appreciated this article. It offered tons of helpful details. Great effort on creating this.

This post is fantastic! Filled with helpful insights and very clear. Many thanks for providing this.

Loved the details offered in this post. It’s so clear and filled with useful insight. Great effort!

Really liked perusing this entry. It’s highly articulate and packed with helpful details. Many thanks for sharing this.

Adored this post. It’s highly detailed and full of useful details. Fantastic work!

This post is fantastic. I learned plenty from perusing it. The content is very educational and structured.

This is fantastic. I learned a lot from reading it. The details is highly educational and arranged.

Excellent article. It offered plenty of valuable details. I am grateful for the work you dedicated to write this content.

Appreciated this article. It’s extremely comprehensive and filled with valuable details. Excellent work!

Adored the details in this article. It’s very comprehensive and full of useful information. Excellent effort!

Really appreciated going through this post. It’s highly clear and packed with helpful insight. Thank you for sharing this.

This is fantastic! Full of valuable details and very well-written. Thanks for providing this.

This is fantastic. I picked up plenty from reading it. The information is highly educational and arranged.

Genuinely appreciated this post. It provided tons of valuable information. Great job on creating this.

This is fantastic! Filled with valuable information and highly articulate. Many thanks for providing this.

This is highly informative. I truly enjoyed reading it. The information is highly structured and easy to follow.

Excellent article. It offered tons of helpful insights. I value the time you put in to compose this content.

Loved this post. It’s highly well-researched and full of valuable insights. Great job!

Adored this article. It’s extremely comprehensive and filled with valuable details. Fantastic effort!

Truly appreciated this post. It provided a lot of useful insights. Excellent job on composing this.

Great article. I discovered the content highly useful. Adored the method you detailed the content.

Really enjoyed this article. It provided plenty of useful details. Great work on writing this.

Wonderful article. It gave tons of useful information. I am grateful for the effort you dedicated to create this post.

Excellent article. It offered tons of useful insights. I appreciate the work you put in to write this information.

Adored this post. It’s highly comprehensive and filled with useful details. Great effort!

Loved the information in this post. It’s extremely comprehensive and packed with useful insights. Great job!

This is amazing! Filled with valuable information and extremely articulate. Many thanks for sharing this.

Really liked reading this article. It’s highly well-written and filled with useful information. Thank you for offering this.

Excellent article. It’s extremely articulate and full of beneficial insight. Many thanks for providing this information.

This post is great. I picked up plenty from reading it. The content is extremely educational and well-organized.

This article is incredibly educational. I really appreciated going through it. The information is very structured and straightforward to understand.

This is great. I learned plenty from going through it. The content is extremely informative and well-organized.

Excellent post. I discovered the details highly useful. Appreciated the way you clarified everything.

Adored this entry. It’s highly well-researched and full of helpful details. Fantastic effort!

I really enjoyed reading this article. It’s extremely clear and packed with useful information. Many thanks for offering this information.

Loved this article. It’s highly comprehensive and full of useful insights. Fantastic work!

Wonderful entry. It’s so articulate and packed with valuable details. Many thanks for providing this content.

Appreciated this entry. It’s very well-researched and full of useful information. Thank you for offering such valuable content.

Excellent entry. It’s highly clear and filled with valuable details. Thanks for providing this content.

Excellent entry. I discovered the details extremely useful. Adored the way you clarified all the points.

This article is great. I picked up plenty from reading it. The content is very enlightening and structured.

Loved this entry. It’s so well-researched and packed with valuable details. Thanks for sharing such helpful content.

Truly enjoyed this article. It provided a lot of helpful insights. Fantastic work on creating this.

This is incredibly enlightening. I really appreciated going through it. The content is very well-organized and straightforward to comprehend.

Appreciated this entry. It’s extremely comprehensive and filled with useful information. Thanks for providing such helpful details.

This article is highly enlightening. I genuinely valued reading it. The information is extremely structured and straightforward to comprehend.

This article is fantastic! Full of useful insights and highly well-written. Many thanks for providing this.

This is amazing! Packed with valuable details and extremely articulate. Thanks for sharing this.

Really appreciated reading this post. It’s highly well-written and filled with helpful information. Many thanks for sharing this.

Excellent entry. I discovered the content very helpful. Appreciated the manner you detailed all the points.

This is great. I learned plenty from reading it. The content is highly enlightening and arranged.

Such an amazing article! The details shared is highly useful and articulate. Many thanks for making the effort to compose this.

This post is great. I gained plenty from perusing it. The information is very informative and structured.

Truly liked this post. It provided a lot of valuable insights. Great job on creating this.

Loved the details in this post. It’s extremely detailed and filled with beneficial insights. Excellent job!

This post is wonderful. I picked up plenty from perusing it. The content is highly enlightening and arranged.

Truly liked perusing this post. It’s highly well-written and filled with helpful insight. Thanks for providing this.

Really liked this article. It offered tons of useful information. Fantastic work on creating this.

Wonderful entry. It gave a lot of valuable details. I appreciate the work you invested to compose this content.

Excellent entry. I thought the content very helpful. Appreciated the method you clarified everything.

Excellent entry. It’s very well-written and packed with valuable details. Thanks for offering this post.

This gave me tons of helpful details. I especially enjoyed the manner you clarified the content. Great effort!

So an wonderful article! The details offered is highly useful and clear. Thank you for making the effort to create this.

Appreciated the information in this post. It’s very detailed and full of beneficial information. Excellent effort!

This is extremely educational. I really valued going through it. The information is highly arranged and straightforward to follow.

Truly enjoyed this post. It offered a lot of useful details. Excellent work on writing this.

Truly appreciated this post. It provided plenty of valuable insights. Fantastic effort on writing this.

This post is extremely enlightening. I truly enjoyed reading it. The details is highly structured and straightforward to follow.

This is great. I learned a lot from perusing it. The content is highly informative and arranged.

Great entry. I thought the details highly beneficial. Adored the manner you clarified all the points.

Adored the details in this article. It’s highly detailed and filled with beneficial information. Excellent job!

Wonderful article. It’s very articulate and filled with valuable insight. Many thanks for offering this content.

This article is amazing! Packed with helpful details and very well-written. Thank you for sharing this.

Excellent article. It’s very articulate and full of beneficial information. Many thanks for providing this post.

Really appreciated this entry. It gave tons of valuable details. Excellent work on composing this.

Appreciated this post. It’s extremely comprehensive and filled with helpful information. Fantastic job!

Excellent entry. I discovered the details very beneficial. Adored the method you explained all the points.

Really enjoyed going through this article. It’s highly clear and full of valuable insight. Thank you for sharing this.

Appreciated this article. It’s very detailed and filled with valuable details. Great job!

This post is wonderful! Filled with helpful information and extremely articulate. Thank you for offering this.

Bought it and was worth it.

Excellent. Worth every minute. Helped as expected.

This was exactly what I needed. Thank you!

Great article. I discovered the content very useful. Appreciated the method you explained all the points.

Your discussion on the probate process is very informative. Many people underestimate how complex it can be.

Works well. Well made product.

Loved it with the effects. Amazing.

Really liked it! Totally recommend.

Highly recommended. Excellent product.

What an wonderful article! The insight shared is highly useful and articulate. Thank you for making the effort to create this.

Really liked this post. It offered tons of useful details. Great work on composing this.

This post is amazing! Full of valuable information and highly articulate. Thanks for sharing this.

Really liked it! For sure I recommend it.

Great product! Highly recommend with the efficiency.

Excellent post. It’s very articulate and full of useful details. Many thanks for offering this post.

Cumpre tudo que promete. Vale o investimento.

This is fantastic. I learned a lot from reading it. The information is highly informative and arranged.

Genuinely enjoyed reading this entry. It’s highly well-written and packed with useful details. Thank you for sharing this.

This post is wonderful! Packed with valuable details and very clear. Thanks for sharing this.

This article is wonderful. I learned tons from reading it. The information is extremely enlightening and structured.

Came in perfect condition. Efficient.

Perfect for daily use. Would recommend.

Delivers exactly as promised! Worth it.

Surprised with the quality. Ideal product.

Excellent product! Highly recommend with the effectiveness.

Worth every penny. Fantastic.

“Vinyl gutters are affordable, but aluminum gutters last longer and handle heavy rain better!”

Adored this article. It’s very detailed and full of helpful details. Excellent work!

Adored the information provided in this article. It’s extremely articulate and filled with helpful details. Fantastic effort!

meggie_quia@gmail.com

Adored the information in this entry. It’s very comprehensive and full of useful information. Fantastic effort!

This post is extremely educational. I genuinely enjoyed going through it. The details is extremely well-organized and straightforward to follow.

Terrific post. It’s highly well-written and packed with valuable information. Thanks for sharing this information.

Very useful in daily life. Really liked it.

Delighted with the quality. Ideal product.

“Protect your home during the rainy season with gutter covers designed for the Pacific Northwest climate.”

Simple to use. Loved it.

Arrived perfectly. High-quality product.

Very effective. Met my expectations.

Happy with the delivery.

This is wonderful! The details shared is extremely useful, and it is articulate. Thanks for making the effort to create this.

Wonderful article. It’s extremely articulate and packed with beneficial insight. Thanks for sharing this information.

This is great. I gained plenty from perusing it. The information is very educational and well-organized.

Adored this entry. It’s highly well-researched and packed with valuable details. Excellent work!

Incredible quality. Totally worth it.

Genuinely enjoyed this entry. It gave tons of valuable insights. Fantastic work on creating this.

Recomendo de olhos fechados.

Terrific article. It’s highly clear and filled with valuable details. Many thanks for sharing this post.

This post is amazing! Full of useful details and very articulate. Thank you for offering this.

Great for daily use.

High-quality product. Totally worth it!

Super happy! Practical.

This is fantastic. I picked up tons from going through it. The content is highly educational and well-organized.

This article is great. I picked up plenty from perusing it. The content is highly enlightening and well-organized.

I appreciate how detailed and practical this article is.

“Thanks for the reminder! Seasonal gutter cleaning can help prevent ice dams in northern areas and water damage here in Florida.”

This article is wonderful! Packed with valuable information and highly clear. Thanks for sharing this.

Great post. I found the content very beneficial. Appreciated the method you explained everything.

Really appreciated this article. It gave plenty of helpful information. Great work on creating this.

Excellent article. I thought the content very helpful. Adored the way you detailed everything.

This post is amazing! Filled with valuable insights and highly clear. Thanks for providing this.

Really enjoyed going through this post. It’s very clear and packed with useful insight. Thank you for offering this.

Very useful in daily life. Really liked it.

Much gratitude for sharing something so good.

Tried it and loved it! Simple to use.

Great! Does what it promises.

Really liked it. Would buy again.

Sensational product. Truly, recommend it.

Genuinely appreciated this entry. It gave tons of helpful insights. Fantastic job on composing this.

Fantastic post. I discovered the content highly beneficial. Loved the way you detailed everything.

This article is fantastic! Filled with useful insights and extremely well-written. Thanks for sharing this.

Really enjoyed this entry. It offered plenty of valuable details. Great effort on composing this.

Truly appreciated this entry. It gave a lot of valuable details. Fantastic job on writing this.

Appreciated this post. It’s very comprehensive and filled with useful information. Thank you for offering such helpful details.

Really enjoyed going through this post. It’s highly articulate and full of useful insight. Thank you for providing this.

Recommended! Worth every penny.

Excellent entry. It’s very clear and packed with useful information. Many thanks for sharing this post.

Truly liked perusing this entry. It’s extremely informative and structured. Excellent work!

This article is wonderful. I picked up a lot from perusing it. The content is highly educational and well-organized.

Fantastic product! Super satisfied with the quality.

I appreciated perusing this entry. It’s extremely well-written and filled with valuable details. Many thanks for providing this information.

Truly liked reading this post. It’s highly articulate and packed with valuable insight. Many thanks for sharing this.

Loved this article. It’s very detailed and full of valuable details. Thanks for sharing such valuable content.

I tried it and loved it.

Loved it! Totally recommend.

Works exactly as promised! Recommend.

Well packaged. Practical.

Revolutionary product! Helps a lot.

Wonderful post. It provided a lot of helpful information. I value the work you dedicated to create this content.

Excellent article. I appreciate the time you put in to share such useful details. It is concise and highly enlightening.

Truly liked this post. It gave a lot of helpful insights. Excellent work on writing this.

This is incredibly informative. I truly valued reading it. The details is extremely arranged and easy to follow.

Amazing product! Really impressed with the quality.

This is truly fantastic. I discovered the information highly helpful and well-written. Many thanks for sharing such helpful information.

This is wonderful. I gained plenty from perusing it. The content is very educational and arranged.

Genuinely appreciated perusing this post. It’s extremely articulate and full of valuable details. Thanks for offering this.

This article is fantastic. I learned plenty from going through it. The information is very educational and structured.

This article is fantastic! Packed with helpful information and very clear. Thanks for sharing this.

Delighted with the quality. Practical product.

Adored the details in this entry. It’s extremely detailed and full of beneficial information. Great work!

Truly enjoyed this article. It offered a lot of useful details. Excellent job on composing this.

Fantastic article. I found the content highly helpful. Loved the way you clarified all the points.

Genuinely liked this entry. It gave plenty of valuable information. Fantastic effort on creating this.

Very efficient. Would recommend.

Appreciated this entry. It’s extremely comprehensive and packed with useful details. Excellent job!

Great packaging. Highly recommend.

This is highly informative. I truly appreciated going through it. The content is very structured and straightforward to understand.

Delivered quickly. Efficient.

Genuinely appreciated this article. It gave tons of valuable insights. Excellent job on composing this.

Wonderful product! Exceeded my expectations.

Adored the details in this entry. It’s highly comprehensive and filled with helpful details. Great job!

Really appreciated going through this entry. It’s highly clear and filled with valuable insight. Many thanks for sharing this.

Fast delivery. Wonderful product.

Really liked going through this post. It’s very well-written and packed with valuable insight. Thanks for offering this.

Great quality. Met my needs.

Loved this post. It’s extremely well-researched and full of helpful information. Great job!

This is great. I learned a lot from going through it. The content is very educational and well-organized.

Adored the insight provided in this post. It’s very articulate and full of helpful information. Great job!

Wonderful entry. It provided tons of useful details. I appreciate the effort you put in to write this post.

Great entry. I found the details very helpful. Adored the way you explained all the points.

This post is great. I gained tons from reading it. The content is highly enlightening and well-organized.

Appreciated this entry. It’s highly comprehensive and full of helpful insights. Fantastic job!

Perfect choice. Fantastic.

Came in perfect condition. Efficient.

Loved the details in this post. It’s very well-researched and filled with useful insights. Fantastic job!

This is great. I gained plenty from reading it. The information is extremely educational and arranged.

Genuinely appreciated going through this post. It’s highly educational and structured. Excellent work!

Very good product! Exceeded my expectations.

Delighted with the quality. Efficient product.

Genuinely enjoyed this entry. It offered tons of useful details. Excellent job on composing this.

Great for daily use.

This is incredibly educational. I really valued going through it. The content is highly well-organized and easy to follow.

Truly appreciated perusing this article. It’s extremely well-written and packed with valuable information. Thank you for providing this.

Great post. I thought the information highly helpful. Appreciated the way you explained everything.

Loved this article. It’s extremely well-researched and filled with helpful details. Fantastic effort!

Excellent post. I appreciate the work you put in to share such beneficial information. It was concise and very educational.

Thanks for breaking this down into simple steps. It really helped!

Exceeded my expectations. Simple to use.

Excellent article. It provided a lot of valuable information. I appreciate the effort you put in to compose this content.

This article is extremely enlightening. I really appreciated perusing it. The content is extremely structured and simple to understand.

Terrific entry. It’s extremely articulate and packed with beneficial details. Thanks for providing this post.

Well made. Met my needs.

This post is really amazing! The information offered is extremely useful, and it is well-written. Thank you for making the effort to write this.

Fantastic entry. I found the content highly beneficial. Adored the method you explained everything.

Appreciated the insight in this article. It’s extremely comprehensive and full of useful insights. Great effort!

Truly enjoyed reading this entry. It’s extremely clear and packed with helpful information. Thank you for offering this.

Everything arrived perfectly. Worth it.

Me surpreendeu positivamente. Ótimo para o dia a dia.

This is incredibly informative. I genuinely valued going through it. The details is highly well-organized and simple to understand.

Fantastic post. I discovered the information very useful. Adored the method you explained all the points.

Maravilhoso. Prático e eficiente.

This is fantastic! Filled with helpful insights and very clear. Thank you for offering this.

Adored the information in this article. It’s extremely well-researched and packed with helpful information. Excellent effort!

Appreciated the details in this article. It’s highly well-researched and full of beneficial information. Great effort!

Genuinely enjoyed perusing this post. It’s extremely informative and well-organized. Fantastic work!

Loved the insight in this entry. It’s very detailed and filled with beneficial insights. Fantastic job!

Appreciated the details in this post. It’s very detailed and full of useful insights. Excellent job!

This post is wonderful! Packed with valuable details and very clear. Thanks for offering this.

Adored the information in this entry. It’s extremely comprehensive and filled with helpful information. Excellent work!

This article is great. I gained plenty from perusing it. The information is extremely educational and arranged.

Loved this article. It’s very comprehensive and packed with valuable information. Excellent work!

Very practical! Exceeded expectations.

Loved the details in this article. It’s very well-researched and packed with helpful insights. Fantastic work!

Truly enjoyed this entry. It gave plenty of valuable information. Fantastic job on composing this.

Adored the information in this entry. It’s highly comprehensive and filled with beneficial details. Excellent effort!

Bem construído. Com certeza vale a pena.

Genuinely enjoyed this article. It gave tons of helpful insights. Great work on creating this.

Adored this entry. It’s highly comprehensive and full of helpful details. Excellent effort!

Fantastic post. I thought the information highly beneficial. Loved the method you explained all the points.

Fiquei impressionado com a eficiência. Compra certeira.

Adored the information shared in this article. It’s extremely well-written and packed with helpful information. Great job!

Really enjoyed this post. It gave tons of valuable information. Great effort on writing this.

Appreciated this article. It’s extremely detailed and packed with helpful insights. Great job!

Excellent post. It’s very clear and packed with valuable information. Many thanks for providing this content.

Terrific article. It’s very clear and filled with beneficial insight. Many thanks for sharing this content.

Adored the details in this entry. It’s highly well-researched and packed with helpful insights. Excellent work!

Appreciated this entry. It’s extremely detailed and packed with valuable details. Excellent effort!

This is extremely educational. I genuinely valued reading it. The content is extremely well-organized and easy to comprehend.

This post is amazing! Full of valuable details and very well-written. Many thanks for sharing this.

I’m amazed with the effects. Exceeded expectations.

Truly enjoyed this post. It gave a lot of useful details. Excellent work on writing this.

Adored the insight in this entry. It’s highly detailed and packed with beneficial information. Excellent effort!

Excellent post. I thought the details very useful. Appreciated the method you explained the content.

Adored the details offered in this post. It’s very articulate and full of helpful insight. Excellent job!

Really liked perusing this article. It’s extremely enlightening and structured. Excellent job!

Excellent article. I thought the content very helpful. Appreciated the manner you explained the content.

So an fantastic article! The insight provided is very beneficial and clear. Thanks for taking the time to write this.

Truly appreciated perusing this article. It’s very clear and packed with valuable insight. Many thanks for sharing this.

Gostei muito! Recomendo sem dúvidas.

Loved this article. It’s very detailed and full of valuable insights. Great effort!

What an amazing post! The insight provided is highly helpful and well-written. Thank you for putting in the work to compose this.

This is amazing! Packed with valuable information and highly well-written. Thank you for offering this.

Genuinely enjoyed this article. It provided plenty of valuable information. Great job on writing this.

Really enjoyed perusing this article. It’s highly clear and filled with valuable insight. Many thanks for providing this.

Fiquei impressionado com a eficiência. Compra certeira.

This post is amazing! Full of valuable information and very clear. Many thanks for offering this.

This article is amazing! Full of valuable information and highly clear. Thanks for providing this.

Exceeded expectations. Practical.

Very efficient. I’ll buy again.

This is wonderful! Full of useful insights and extremely clear. Thank you for sharing this.

Wonderful entry. It’s extremely clear and packed with useful details. Thank you for sharing this content.

Adored the insight offered in this entry. It’s very clear and full of useful insight. Great work!

Adored the insight in this article. It’s extremely well-researched and packed with beneficial details. Fantastic effort!

Produto incrível. Bem simples de usar.

Wonderful article. It gave plenty of useful details. I value the work you dedicated to write this post.

Excellent post. It’s highly well-written and filled with useful information. Thanks for providing this content.

This article is wonderful! Filled with valuable details and very articulate. Thanks for providing this.

Ótima qualidade. É tudo o que promete.

Tudo em perfeito estado. Adorei a eficiência.

Loved it! Very happy.

Very practical! Exceeded expectations.

This post is amazing! Packed with useful information and very clear. Thank you for sharing this.

Genuinely appreciated going through this post. It’s highly clear and packed with useful insight. Thank you for providing this.

This gave great details. I genuinely enjoyed reading it. This post is extremely well-organized and simple to comprehend.

This article is great. I learned a lot from going through it. The information is very enlightening and well-organized.

Loved this article. It’s highly well-researched and filled with valuable information. Fantastic job!

This is wonderful! Packed with useful information and extremely clear. Thanks for sharing this.

Muito feliz com a compra. Bem prático e funcional.

Me surpreendeu positivamente. Muito prático e eficiente.

Everything arrived perfectly. Highly recommend.

Great value for money. Liked it.

Really valued this entry. It offered tons of valuable details. Fantastic job!

Loved this entry. It’s extremely well-researched and packed with useful details. Great work!

This post is highly informative. I really appreciated reading it. The content is highly structured and easy to follow.

This article is amazing! Filled with helpful information and highly well-written. Thanks for sharing this.

Great post. I found the content very helpful. Adored the manner you clarified all the points.

Excellent post. I thought the information highly useful. Appreciated the method you clarified the content.

Appreciated the insight in this entry. It’s very detailed and packed with helpful information. Excellent effort!

Terrific entry. It’s highly well-written and full of useful information. Thank you for offering this content.

Really appreciated this post. It gave a lot of helpful insights. Fantastic work on writing this.

Loved this entry. It’s highly detailed and packed with useful insights. Great work!

Wonderful article. It gave plenty of valuable information. I value the time you put in to create this post.

This is fantastic! Packed with helpful insights and highly well-written. Thanks for offering this.

Well-packaged. High-quality product.

This is amazing! Filled with valuable information and very clear. Thank you for offering this.

Adored the details in this entry. It’s highly comprehensive and packed with helpful details. Excellent job!

Wonderful product! Works perfectly.

This is amazing! Filled with valuable details and highly well-written. Thank you for providing this.

Excellent article. I discovered the information very beneficial. Appreciated the way you explained the content.

Great entry. I found the information highly useful. Adored the method you detailed all the points.

This is extremely informative. I really appreciated reading it. The content is very structured and simple to comprehend.

Excellent post. It’s extremely well-written and filled with useful information. Many thanks for offering this post.

Great product! Really impressed with the efficiency.

Really enjoyed this entry. It provided plenty of useful details. Fantastic job on composing this.

This post is amazing! Full of useful insights and extremely articulate. Thank you for offering this.

Great article. I discovered the details extremely useful. Adored the method you explained everything.

This is incredibly educational. I really enjoyed perusing it. The information is extremely structured and straightforward to understand.

This post is wonderful. I gained tons from going through it. The content is highly educational and structured.

Excellent entry. It’s highly well-written and filled with beneficial insight. Many thanks for providing this information.

Really liked going through this post. It’s extremely educational and well-organized. Great effort!

Genuinely enjoyed this post. It gave plenty of useful information. Excellent work on writing this.

This post is incredibly educational. I truly appreciated reading it. The information is very well-organized and easy to understand.

Fast delivery. Very useful product.

Great. Worth every effort. Resolved as expected.

This is wonderful. I gained a lot from perusing it. The details is highly enlightening and structured.

Excellent post. I discovered the details extremely useful. Appreciated the manner you explained all the points.

Truly appreciated this post. It offered a lot of useful details. Fantastic work on composing this.

Adored this article. It’s very comprehensive and filled with useful insights. Great effort!

Terrific article. It’s very well-written and packed with useful insight. Thank you for offering this information.

Genuinely liked reading this article. It’s highly articulate and packed with useful insight. Thank you for sharing this.

Excellent entry. It’s highly clear and packed with beneficial details. Thank you for sharing this information.

Loved this article. It’s very comprehensive and filled with helpful insights. Great job!

This article is incredibly educational. I genuinely enjoyed reading it. The details is highly arranged and straightforward to comprehend.

Excellent post. I found the information very helpful. Appreciated the way you clarified the content.

Truly enjoyed perusing this post. It’s highly well-written and full of useful details. Many thanks for providing this.

This article is wonderful. I gained plenty from reading it. The details is extremely educational and well-organized.

Great post. I discovered the information very useful. Loved the method you detailed the content.

This article is great. I picked up plenty from perusing it. The content is extremely educational and arranged.

Recommended! Does what it promises.

Wonderful post. It’s extremely well-written and filled with valuable information. Thanks for sharing this content.

Terrific post. It’s very clear and full of beneficial insight. Thanks for providing this content.

Impressive product! Works perfectly.

Adored this entry. It’s very detailed and filled with helpful insights. Excellent effort!

Great value for money. Would recommend.

Incredible. Exactly what I wanted.

This post is fantastic! Packed with helpful insights and extremely articulate. Many thanks for providing this.

Came as expected. Satisfied!

Appreciated this article. It’s very detailed and filled with useful insights. Great effort!

Appreciated this entry. It’s very detailed and packed with valuable insights. Great job!

This post is extremely informative. I truly enjoyed perusing it. The details is very structured and easy to comprehend.

Really appreciated this entry. It gave plenty of useful details. Fantastic job on writing this.

This is highly educational. I genuinely enjoyed reading it. The content is highly structured and easy to understand.

Loved this post. It’s extremely well-researched and packed with useful details. Excellent effort!

Genuinely liked perusing this entry. It’s extremely well-written and full of valuable details. Thanks for offering this.

Genuinely enjoyed reading this article. It’s highly articulate and filled with helpful information. Thanks for offering this.

This article is amazing! Packed with valuable details and very clear. Many thanks for providing this.

Wonderful article. It’s highly clear and filled with valuable details. Thanks for offering this content.

This article is wonderful. I learned plenty from perusing it. The content is very enlightening and well-organized.

So an informative post! I gained plenty from perusing it. This content is very structured and easy to follow.

This article is highly educational. I genuinely valued reading it. The content is highly well-organized and simple to follow.

Wonderful entry. It’s highly articulate and full of useful insight. Many thanks for sharing this post.

Excellent entry. It’s extremely clear and full of beneficial insight. Thanks for offering this content.

Appreciated the insight in this entry. It’s extremely comprehensive and full of useful information. Great work!

This article is fantastic! Packed with helpful details and extremely articulate. Thank you for offering this.

Fast delivery. High-quality product.

Impressed. Simple to use.

This is wonderful! Filled with helpful insights and highly well-written. Thanks for offering this.

This post is amazing! Full of helpful information and very clear. Thank you for providing this.

This article is fantastic. I gained plenty from going through it. The details is highly informative and structured.

What an fantastic post! The insight provided is extremely useful and clear. Many thanks for making the effort to write this.

Bought it and loved it! Simple to use.

Bought it and loved it! Simple to use.

This is fantastic. I picked up a lot from perusing it. The content is very educational and well-organized.

Genuinely enjoyed this article. It offered tons of useful information. Great effort on writing this.

Excellent entry. It’s so well-written and packed with helpful insight. Thanks for sharing this content.

Genuinely valued this entry. It gave plenty of useful information. Excellent effort!

Ideal product! Worth every penny.

Adored this post. It’s very detailed and filled with useful insights. Excellent job!

Truly appreciated this article. It offered a lot of helpful insights. Excellent job on creating this.

Delivered quickly. Practical.

Perfect! Does what it promises.

Totally worth it. Efficient.

This post is wonderful! Filled with useful details and highly clear. Thank you for offering this.

This post is wonderful. I learned a lot from going through it. The details is highly enlightening and arranged.

High-quality product, recommend.

Loved the details provided in this article. It’s extremely well-written and filled with useful details. Excellent effort!

Loved the insight provided in this entry. It’s so articulate and packed with valuable details. Excellent work!

Excellent entry. It’s very well-written and full of beneficial details. Thanks for sharing this post.

This is truly amazing! The information offered is highly helpful, and it was articulate. Thank you for putting in the work to write this.

This post provided excellent details. I genuinely appreciated reading it. Your post is highly structured and easy to understand.

Truly enjoyed this post. It offered a lot of helpful information. Great job on writing this.

Wonderful article. It’s highly well-written and full of useful insight. Many thanks for providing this content.

Appreciated the details in this entry. It’s highly comprehensive and packed with beneficial insights. Excellent job!

Product came as expected. Great product.

This post is fantastic. I learned tons from perusing it. The information is highly informative and arranged.

Really appreciated perusing this entry. It’s extremely articulate and full of helpful details. Many thanks for offering this.

Bem como eu esperava. Atendeu super bem.

Muito bom mesmo! Estou impressionado.

Works exactly as promised! Recommend.

Fast delivery. Great product.

Really enjoyed going through this article. It’s highly clear and packed with useful insight. Many thanks for sharing this.

Appreciated this entry. It’s extremely detailed and filled with useful insights. Excellent job!

Terrific entry. It’s very clear and filled with useful insight. Thanks for providing this post.

Adored the information in this entry. It’s highly comprehensive and full of helpful insights. Fantastic work!

Adored this article. It’s highly well-researched and packed with helpful information. Fantastic work!

This article is incredibly informative. I really valued perusing it. The information is highly structured and simple to comprehend.

This is fantastic. I gained plenty from perusing it. The details is extremely educational and structured.

This article is great. I picked up tons from going through it. The content is very enlightening and arranged.

This is fantastic! Full of helpful information and extremely clear. Thank you for sharing this.

Excelente produto! Super recomendo.

Appreciated the insight in this post. It’s highly well-researched and packed with useful insights. Fantastic work!

Loved this entry. It’s extremely comprehensive and filled with helpful information. Fantastic effort!

This article is wonderful. I picked up plenty from perusing it. The details is very educational and well-organized.

Really liked perusing this entry. It’s extremely clear and packed with valuable information. Many thanks for sharing this.

Appreciated this entry. It’s very comprehensive and full of valuable insights. Excellent work!

Appreciated this post. It’s highly well-researched and full of valuable details. Fantastic job!

Appreciated this article. It’s very detailed and filled with helpful information. Thanks for offering such valuable information.

This post offered me a lot of valuable details. I really enjoyed the method you clarified everything. Great effort!

So an amazing entry! The information offered is very beneficial and clear. Many thanks for making the effort to create this.

Excellent article. I found the details highly useful. Loved the way you explained everything.

Terrific post. It’s highly articulate and full of beneficial information. Many thanks for offering this post.

Adored the details in this post. It’s extremely well-researched and filled with useful insights. Great work!

What an fantastic post! The information shared is extremely useful and clear. Many thanks for putting in the work to compose this.

This article is incredibly enlightening. I truly appreciated going through it. The information is highly arranged and easy to comprehend.

Truly enjoyed this article. It gave a lot of helpful information. Excellent effort on writing this.

Wonderful article. It’s highly clear and full of useful details. Thanks for offering this information.

Wonderful for daily use.

Muito prático. Produto top.

Buy and sell Bitcoin, Ethereum, NoOnes login and other cryptocurrencies Peer-to-Peer on NoOnes. Secure, fast, and user-friendly transactions on a trusted platform

Balances Active Orders Withdraw Deposit TradeOgre Logout · Sign In. Search: Currency, Market, Change, Price

BPI Net Empresas é o serviço do Banco BPI que permite gerir as contas e realizar operações bancárias online, com segurança e comodidade. Saiba mais sobre as vantagens, as operações Bpi Net Empresas

This article is truly fantastic. I found the details highly helpful and well-written. Thank you for offering such beneficial details.

Me surpreendeu positivamente. Muito prático e eficiente.

Genuinely enjoyed going through this post. It’s extremely informative and arranged. Excellent job!

Really appreciated this entry. It gave a lot of useful insights. Excellent work on creating this.

Adored this entry. It’s very detailed and filled with helpful details. Excellent job!

Really liked going through this article. It’s extremely well-written and packed with useful insight. Thanks for providing this.

Impressive results. Exceeded my expectations.

This is fantastic! Full of helpful insights and extremely clear. Thanks for providing this.

Wonderful article. It’s very clear and full of useful insight. Many thanks for sharing this post.

Loved this entry. It’s very comprehensive and full of useful information. Fantastic effort!

This is wonderful. I learned plenty from perusing it. The information is highly informative and well-organized.

Very practical! Amazing for what I needed.

Surprisingly good. Amazing for my needs.

Excellent. Worth every minute. Worked as expected.

This is fantastic. I learned a lot from going through it. The information is highly enlightening and well-organized.

Terrific post. It’s very articulate and filled with useful details. Thanks for providing this post.

Tried it and it was worth it! Practical to use.

Very good product! Exceeded my expectations.

Atendeu completamente. Recomendo sem dúvidas.

Impressed with the results.

Terrific article. It’s extremely clear and filled with valuable insight. Thanks for offering this information.

Exceeded expectations. Very helpful.

Appreciated this entry. It’s extremely comprehensive and packed with helpful insights. Excellent job!

Fast delivery. I’m very happy.

Fantastic article. I found the content extremely beneficial. Loved the manner you explained all the points.

Genuinely appreciated reading this entry. It’s highly clear and filled with helpful insight. Thanks for sharing this.

This post is great. I gained tons from going through it. The content is very informative and structured.

Came in perfect condition. Practical.

Loved this article. It’s so comprehensive and packed with helpful information. Thanks for sharing such valuable information.

Worth every penny. Trust it.

Amazing product! Very happy.

This post is highly enlightening. I truly valued reading it. The information is very arranged and straightforward to understand.

This article is wonderful. I picked up tons from reading it. The content is highly informative and arranged.

This is great. I learned tons from going through it. The information is extremely enlightening and well-organized.

This post is highly educational. I truly enjoyed going through it. The information is extremely structured and simple to understand.

Really liked this post. It offered plenty of helpful information. Fantastic work on creating this.

Terrific post. It’s extremely articulate and filled with useful insight. Thank you for sharing this information.

Really liked this article. It provided a lot of helpful insights. Great job on creating this.

This post is fantastic. I gained plenty from going through it. The information is extremely educational and well-organized.

Very satisfied with the quality. Efficient product.

Truly appreciated this post. It provided plenty of useful information. Great job on composing this.

Really appreciated going through this entry. It’s extremely well-written and packed with valuable information. Thanks for sharing this.

Adored this post. It’s very comprehensive and filled with valuable details. Fantastic effort!

Truly liked going through this post. It’s very well-written and full of helpful insight. Many thanks for providing this.

Really liked it! Totally recommend.

Appreciated this article. It’s very detailed and full of useful details. Great effort!

Great article. I thought the content very helpful. Loved the manner you explained everything.

Truly enjoyed this entry. It gave plenty of valuable insights. Great job on composing this.

Appreciated the details in this entry. It’s extremely comprehensive and filled with beneficial insights. Excellent job!

This post is great. I picked up a lot from perusing it. The details is extremely informative and arranged.

Fantastic product! Impressed with the usability.

This post is wonderful. I gained plenty from perusing it. The information is very informative and structured.

Tried it and I’m very happy. Recommend it a lot.

Excellent entry. I thought the details highly beneficial. Appreciated the method you explained all the points.

High-quality product. Recommend!

Great post. I thought the information highly useful. Appreciated the manner you clarified the content.

Appreciated the information in this article. It’s very well-researched and filled with helpful information. Fantastic effort!

Tried it and I’m impressed. Highly recommend.

Excellent entry. It’s extremely articulate and packed with valuable information. Thank you for sharing this content.

Excellent post. I value the effort you dedicated to provide such beneficial content. It is concise and extremely informative.

Appreciated this post. It’s highly detailed and full of valuable details. Fantastic work!

Adored the information in this post. It’s extremely comprehensive and filled with beneficial information. Great effort!

This article is amazing! Full of useful information and very clear. Many thanks for sharing this.

Genuinely appreciated this entry. It offered a lot of valuable details. Excellent job on writing this.

This is extremely informative. I really enjoyed perusing it. The details is highly arranged and straightforward to comprehend.

This post is extremely enlightening. I really enjoyed going through it. The content is highly structured and easy to comprehend.

Excellent product. I’ll buy again.

This article is wonderful. I learned a lot from reading it. The details is very enlightening and arranged.

Fantastic entry. I discovered the information extremely beneficial. Adored the method you detailed all the points.

This is amazing! Full of valuable information and very clear. Many thanks for offering this.

Excellent entry. I discovered the content very beneficial. Appreciated the way you detailed everything.

Loved the insight provided in this post. It’s so well-written and filled with useful details. Excellent work!

Excellent article. It’s highly clear and filled with useful insight. Thanks for sharing this content.

Well packaged. Efficient.

Great product! Very satisfied with the quality.

Foi uma ótima compra. Exatamente o que precisava.

Excellent post. It’s extremely well-written and packed with valuable insight. Thank you for offering this content.

This article is fantastic. I discovered the content very helpful and well-written. Thanks for sharing such beneficial information.

This is fantastic! Filled with valuable information and very articulate. Many thanks for offering this.

This post is great. I learned tons from reading it. The information is highly educational and arranged.

Really liked going through this entry. It’s extremely well-written and packed with valuable insight. Many thanks for sharing this.

Very effective. Fulfilled my expectations.

This is incredibly educational. I genuinely valued perusing it. The content is extremely structured and easy to follow.

I really enjoyed perusing this post. It’s so well-written and filled with helpful details. Thanks for providing this information.

This article is truly amazing! The details provided is extremely useful, and it was clear. Many thanks for taking the time to create this.

Simple to use. Loved it.

Helps exactly as promised! Recommend.

Loved this entry. It’s extremely comprehensive and full of helpful details. Excellent job!

Fantastic entry. I thought the details extremely useful. Loved the method you clarified all the points.

Perfect for daily use. Would recommend.

Wonderful product! Very happy.

Loved this entry. It’s extremely well-researched and filled with valuable details. Fantastic work!

This article is highly educational. I genuinely valued perusing it. The content is extremely well-organized and straightforward to follow.

This is fantastic. I learned tons from perusing it. The details is very enlightening and well-organized.

Excellent entry. I found the content highly beneficial. Appreciated the method you explained the content.

Terrific entry. It’s very articulate and filled with beneficial insight. Many thanks for sharing this post.

This post is extremely informative. I genuinely appreciated perusing it. The details is highly structured and straightforward to understand.

Really liked it. Easy to use.

Truly enjoyed perusing this entry. It’s very articulate and filled with useful details. Thank you for sharing this.

This is fantastic! Filled with valuable insights and extremely articulate. Thank you for sharing this.

This post is extremely informative. I genuinely valued perusing it. The information is extremely arranged and straightforward to comprehend.

This article is great. I picked up a lot from perusing it. The details is very informative and structured.

This post is fantastic. I learned tons from going through it. The content is very educational and structured.

Hi there! Do you know if they make any plugins to

help with Search Engine Optimization? I’m

trying to get my blog to rank for some targeted keywords but I’m

not seeing very good results. If you know of any please share.

Kudos! I saw similar blog here: Your destiny

This article is amazing! Full of useful details and very clear. Thanks for offering this.

Loved the insight in this entry. It’s highly detailed and filled with beneficial details. Great effort!

Really enjoyed going through this entry. It’s extremely articulate and full of useful insight. Thank you for offering this.

This article is highly enlightening. I truly appreciated perusing it. The information is very well-organized and simple to comprehend.

Loved this post. It’s very comprehensive and full of helpful insights. Fantastic work!

Adored this article. It’s extremely comprehensive and filled with valuable insights. Excellent job!

Loved the details in this article. It’s extremely detailed and filled with useful information. Great effort!

Excellent post. I thought the details very helpful. Appreciated the way you explained everything.

This post is fantastic. I gained tons from going through it. The information is very informative and structured.

Excellent entry. I discovered the information highly beneficial. Adored the way you detailed the content.

Exceeded expectations. Amazing for my needs.

Perfect choice. Fantastic.

Aprovado. Superou expectativas.

Excelente produto! Vale muito a pena.

Perfeito em todos os aspectos. Prático e eficiente.

Me surpreendeu! Produto de alta qualidade.

Chegou rápido. Adorei a eficiência.

Perfect! Worth every penny.

Tried it and I’m very happy. Highly recommend.

This article is wonderful! Full of useful details and very articulate. Thanks for providing this.

Genuinely appreciated this article. It provided tons of helpful insights. Fantastic job on creating this.

Excellent entry. It’s very well-written and filled with useful insight. Many thanks for providing this content.

Perfect choice. Fantastic.

High-quality product. Absolutely amazing!

Exceeded expectations. Amazing for everyone.

Arrived perfectly. High-quality product.

This article is incredibly educational. I genuinely valued perusing it. The content is extremely well-organized and simple to follow.

Loved this entry. It’s highly well-researched and full of helpful information. Great job!

Great article. I thought the details very helpful. Appreciated the way you explained the content.

Exatamente o que eu queria. Adorei.

Loved it! For sure I’ll tell my friends about it.

Excellent article. I thought the details highly helpful. Appreciated the manner you clarified all the points.

Extremely practical. Recommended for those seeking quality.

This article is fantastic. I gained a lot from going through it. The content is extremely enlightening and arranged.

Fiquei muito satisfeito. Muito útil.

Truly appreciated perusing this entry. It’s very articulate and full of helpful details. Many thanks for offering this.

Super satisfied. Arrived as described.