Prometheus Trend Signals

Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

We continue on our journey to bring you the best macroeconomic research tools that are insightful and actionable. Over the next few months, we will continue to unveil new systematic tools to help you generate an edge in markets. In that spirit, today, we will briefly share some observations coming from our recently released Prometheus Trend signals. These signals will soon be available daily alongside our existing research offering to help active investors navigate markets nimbly and respond to changing conditions.

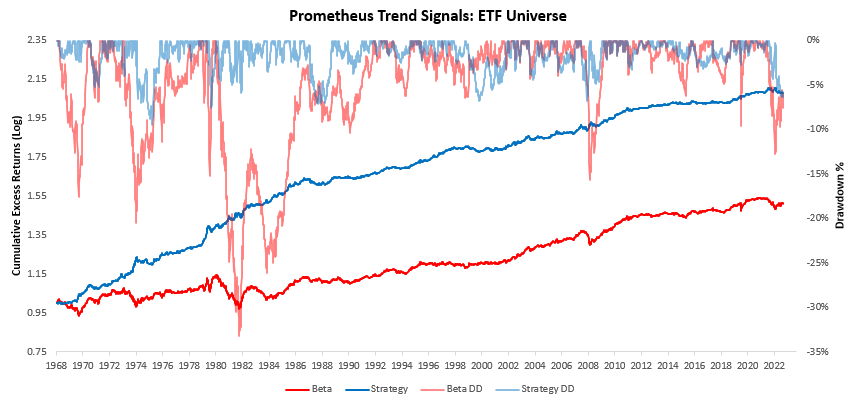

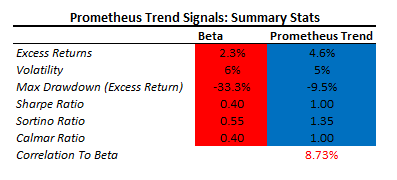

As always, we have tested these trend measures to understand whether they can help reliably generate an edge in markets. Below, we show how the Prometheus Trend Strategies have fared relative to their underlying beta:

The simulation above shows two return streams, an all-weather portfolio of stocks, commodities, bonds, and gold, and an actively managed version of the same using the Prometheus trend signals. The portfolio assets and weights are identical and only differ based on our system signals to go long, short, or stay flat on a given asset. Currencies were excluded from this analysis as currencies have no beta, and a buy-and-hold beta portfolio with currencies included typically suffers in performance. Since we wished to illustrate the value of our market timing signals relative to a buy-and-hold beta portfolio, it would be unfair to include currencies in the beta portfolio. Keep in mind the inclusion of currencies makes the performance gap between our active strategy and the beta portfolio even larger in favor of our trend signals. Below, we show the summary statistics of these portfolios.

As shown above, our trend signal outperforms the beta portfolio on all accounts, offering significantly better return and risk characteristics. Importantly, it does so with little correlation to the underlying markets it trades, i.e., it is not biased to be long or short assets.

While this portfolio possesses strong characteristics, we think it is essential to remember that we do not think of this as a standalone portfolio but rather an additional layer of confirmation alongside our other tools. We think this is best used in conjunction with our market regime monitors and our fundamental forecasting process to improve our timing in selecting exposure for a given economic environment.

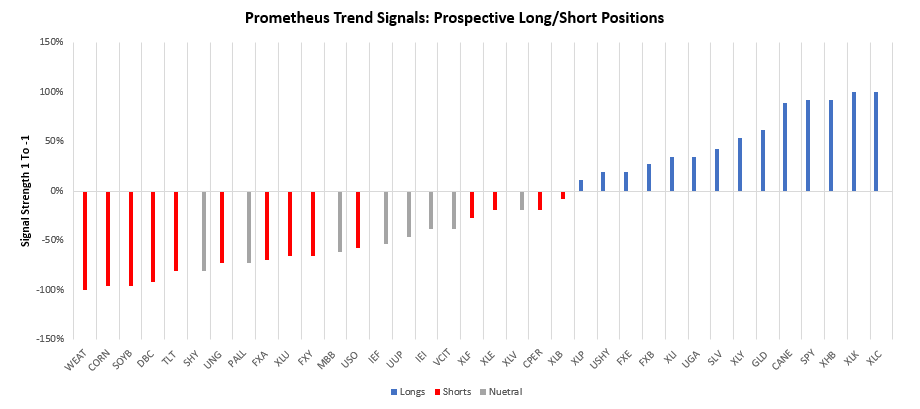

Currently, this trend process offers a range of potential positions. We show these below:

Above, we show the signals generate by our trend process. Our trend process uses a non-linear filtering process to sort for trend signals that we think have the most potential therefore, trend signal strength will not always conform to whether or not our systems take on a position. As can be seen above, positions are sorted into longs, shorts, and neutral positions. Currently, we are seeing a range of potential trends most of which are skewed toward the short side. The strongest signals are currently short commodities (WEAT, CORN, SYB, DBC) and long equities (SPY, XHB, XLK, XLC). The combination of these bets is particularly interesting in a macroeconomic context if they continue to trend, it will likely further current market pricing of disinflation:

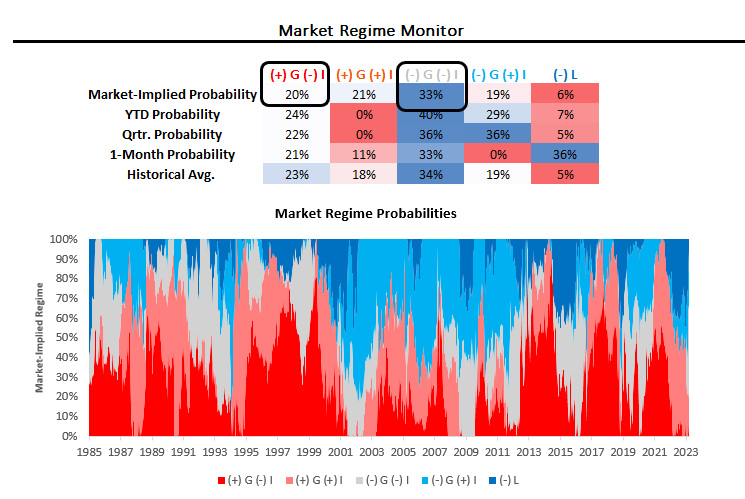

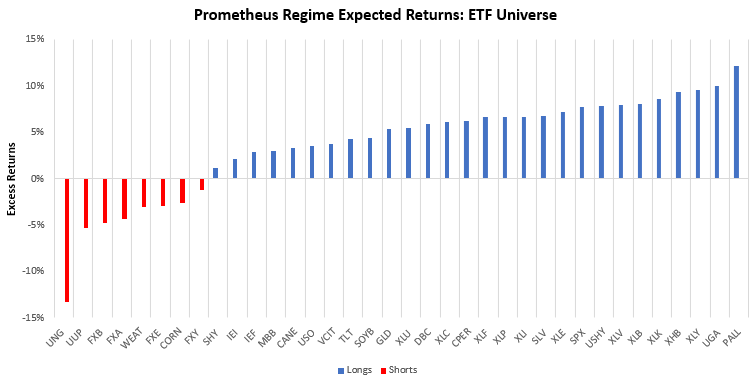

Based on our market-implied regimes, we also estimate the regime-expected returns for our universe of ETFs:

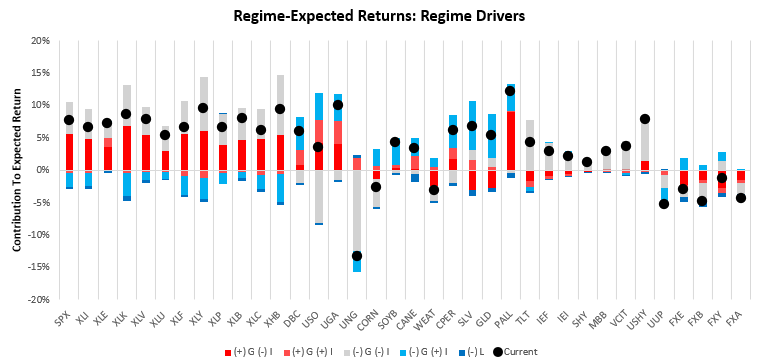

As we can see above, market regime dynamics don’t confirm many trends, somewhat limiting the opportunity set. This is largely due to the confluence of rising and falling growth pricing at the same, i.e., markets have not decidedly priced either outcome. Below, we show the contributions to our expected return measures by the regime. As we can see, there is a significant amount of mixed messaging from growth and inflation factors.

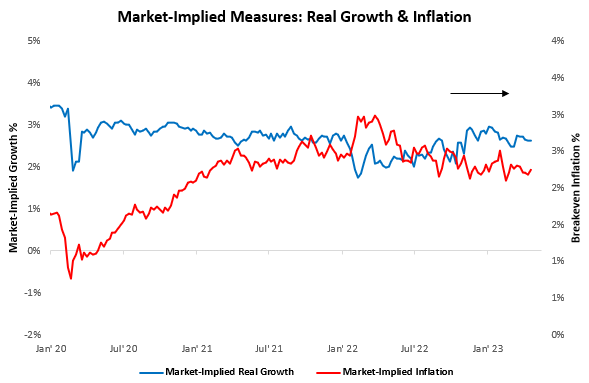

We show a different perspective on the same subject market-implied measures of growth and inflation remain roughly flat this year:

Overall, while trend measures continue to show abundant opportunities, cross-asset pricing does not show significant decisiveness. We think there are two things to be gleaned from this. First, we need to think about return streams that are diverse from macrocycle bets that require imminent pricing. Second, we likely need return streams anchored upon reasonable estimates of where we are headed in the macroeconomic cycle to see through the noise in markets. We will provide both in the weeks and months to come.

If you enjoyed these trend signals and would like to use them more frequently, please let us know in the comments. Until next time.