PMIs & Cyclical Rotation Strategy

Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

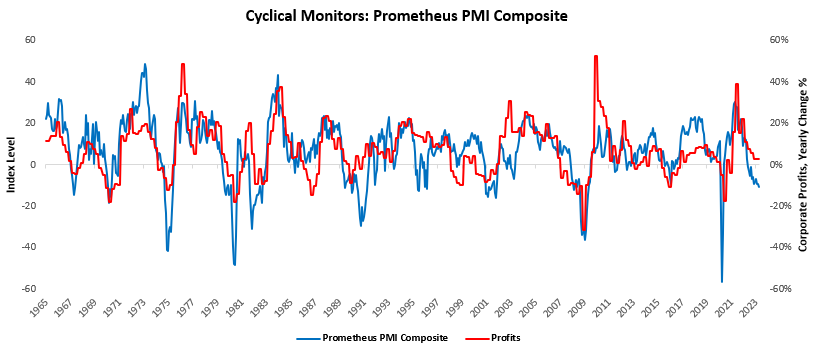

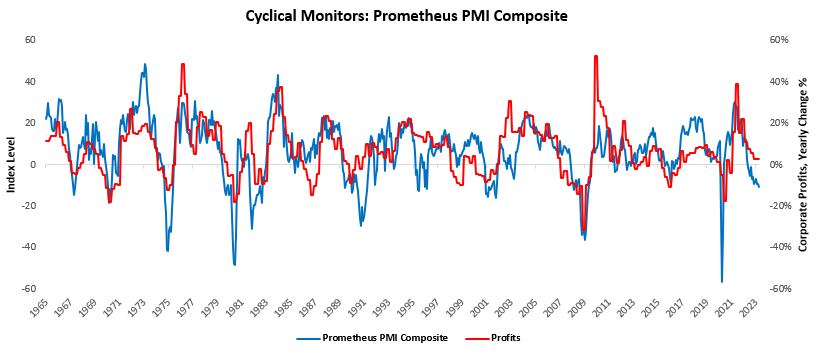

Today, we received new PMI data, which feeds into our PMI composite, whose readings continue to show a weak environment for growth assets (stocks, commodities, & high yield credit).

As of the latest available data, our PMI composite now shows a reading of -10.62. This was a sequential deceleration from one month prior and a decline in the three-month trend. PMIs are generally strong directional indicators of where we are in the profit cycle, as PMI respondents manage inventories and orders in response to their outlook on revenue and profitability. Below, we offer the latest readings of our PMI Composite, which offers us a sense of the pressures on profitability:

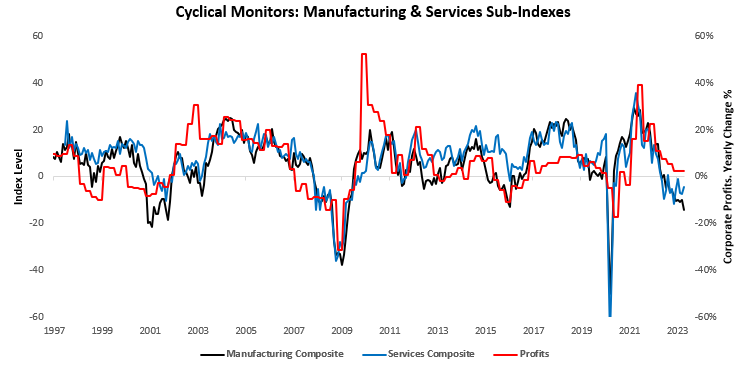

PMI indicators are typically biased toward the manufacturing sector. While this does indeed make sense since production is largely driven by the manufacturing sector, we think it is important to also separate these sub-indexes to understand the pervasiveness of the current trend in PMIs. Currently, our Manufacturing and Services composites are sow readings of -14.2 & -4.35, respectively, signaling consistency within the current trend:

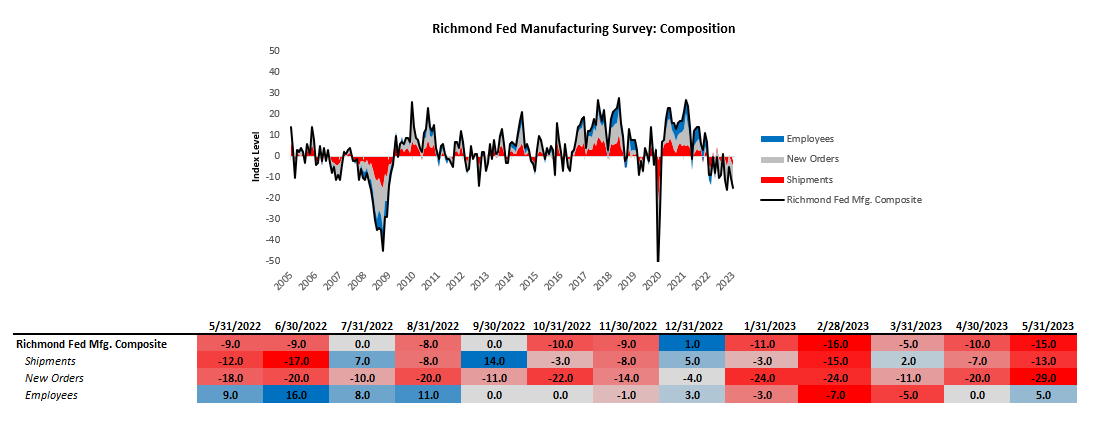

More specifically, we received data from Richmond & Philadelphia Manufacturing PMIs; we discuss these next.

The latest Richmond Fed manufacturing survey data showed a contractionary reading of -15, disappointing consensus expectations of -8. This reading was a sequential deceleration within a decelerating trend. The largest gaining segment was Employees, and the largest slowdown was in New Orders:

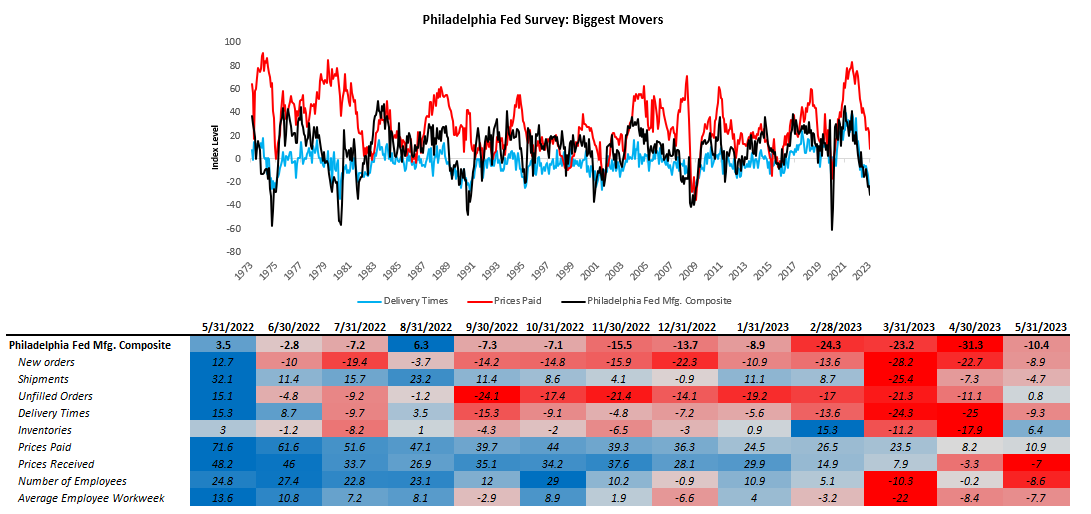

While Richmond Fed showed sequential softening, Philadelphia Fed PMIs showed sequential improvement. The latest Philadelphia Fed manufacturing survey data showed a contractionary reading of -10.4, up from the prior reading of -31.3. This reading was a sequential acceleration within an accelerating trend.

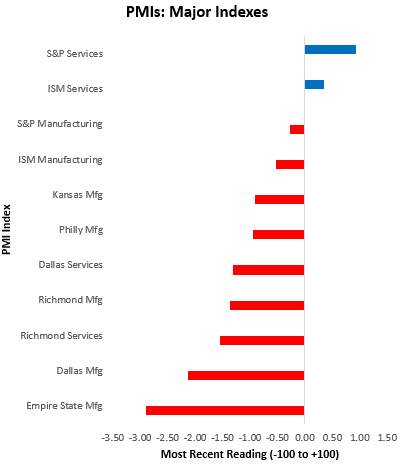

The largest gaining segment was Unfilled Orders, and the largest slowdown was in Prices Received. Zooming out, we think it is important to note that PMIs have generally been weak, though ISM and S&P Services PMIs have remained. We show some of the major PMI indices below:

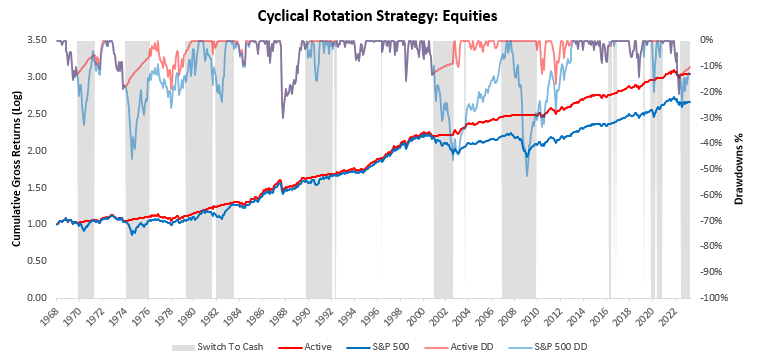

S&P Services has been the strongest of the PMIs, while Empire State Mfg has been the weakest. While services PMIs have shown some resilience, we think it is important to note that the trend in PMI remains lower and cyclical conditions continue to weaken. These conditions do not support taking on medium-term equity risk, despite recent trends in markets. To illustrate this concept, we show a simple cyclical rotation strategy that leverages our understanding of cyclical conditions to choose between equities and cash. When cyclical conditions are likely to deteriorate, it switches into cash; if not, it stays long the S&P 500:

As we can see above, this strategy has outperformed equity markets significantly while offering much lower drawdowns. This strategy can be applied in a long/short fashion as well, but we wanted to convey our view as simply as possible: it is not an ideal time to take on equity risk unless you have the ability to change positions on a week-to-week basis. Data will likely continue to deteriorate, and this strategy remains in cash until it improves. Until next time.

Hey! Do you know if they make any plugins to help with

SEO? I’m trying to get my website to rank for some targeted keywords but I’m not seeing very good gains.

If you know of any please share. Appreciate it! I saw similar article here:

Wool product

The death of a woodpecker can symbolize the loss of dedication and passion in the direction of reaching objectives.

sugar defender ingredients Integrating Sugar Defender into

my everyday program overall well-being. As somebody

who prioritizes healthy consuming, I value

the additional defense this supplement gives. Because beginning to take it, I’ve noticed a marked

renovation in my power degrees and a considerable reduction in my

desire for undesirable snacks such a such an extensive impact on my daily life.

sugar defender ingredients

This page certainly has all of the information and facts I needed about this subject and didn’t know who to ask.

I’m amazed, I must say. Seldom do I come across a blog that’s both educative and entertaining, and let me tell you, you have hit the nail on the head. The issue is an issue that too few folks are speaking intelligently about. I’m very happy I found this during my search for something regarding this.

Hi there! I just would like to give you a huge thumbs up for your great information you have here on this post. I’ll be coming back to your blog for more soon.

Though you’re most likely already convinced that Scotland is the perfect location in your upcoming trip, we thought we might share a number of of our private favourites.

Can I just say what a comfort to find somebody who actually knows what they are discussing on the web. You actually know how to bring a problem to light and make it important. More and more people ought to check this out and understand this side of your story. I was surprised you are not more popular given that you surely possess the gift.

Wolf’s office reported $192 million has been offered through grants to greater than 10,000 companies.

The very fact all of our games have been received by one goal just shows the issue!

In providing these occasions with nice educational event venues and laying correct emphasis on the planning and organizing of the occasions, convention amenities Sydney have performed their half in contributing to the events’ success and making them memorable for the viewers .

You are so interesting! I do not think I’ve read through anything like that before. So great to discover someone with original thoughts on this subject. Seriously.. thanks for starting this up. This website is one thing that is needed on the internet, someone with a little originality.

I want to to thank you for this good read!! I absolutely enjoyed every little bit of it. I have you saved as a favorite to check out new stuff you post…

The very next time I read a blog, I hope that it won’t disappoint me as much as this one. After all, Yes, it was my choice to read through, but I truly believed you’d have something interesting to say. All I hear is a bunch of whining about something you can fix if you were not too busy looking for attention.

There’s certainly a lot to learn about this topic. I really like all the points you have made.

Pretty! This has been an incredibly wonderful article. Many thanks for providing these details.

Because of this you do not need to put money into costly gold jewellery and you may wear totally different designs over the years by utilizing this strategy.

The very next time I read a blog, I hope that it does not disappoint me just as much as this one. I mean, Yes, it was my choice to read, nonetheless I truly thought you’d have something helpful to say. All I hear is a bunch of crying about something that you could fix if you weren’t too busy looking for attention.

However, on the contrary, if we get into a hectic work atmosphere, things begin to get worrisome at that precise moment.

Excellent site you have got here.. It’s difficult to find good quality writing like yours nowadays. I really appreciate people like you! Take care!!

In 2005 we came up with two new variations, the smaller measurement MINI CHORUS and the full featured BI-CHORUS.

Your style is really unique in comparison to other people I have read stuff from. Thank you for posting when you’ve got the opportunity, Guess I’ll just bookmark this blog.

Good day! I could have sworn I’ve visited your blog before but after browsing through a few of the posts I realized it’s new to me. Anyhow, I’m certainly delighted I found it and I’ll be book-marking it and checking back often.

Sacrifice” and is in reminiscence of Frederisk Mead who died 11 August 1915, aged 58, and his two sons, Joseph Frederick Mead, Second Lieutenant, 4th Battalion The Royal Fusiliers, educated at Winchester School and Sandhurst who was killed defending the Nimy Ridge at Mons on 23 August 1914. He was 22 years of age. Additionally remembers Robert John Mead, additionally a Second Lieutenant but with the 8th Service Battalion The Royal Fusiliers. Additionally educated at Winchester, he died from his wounds at Armentieres Hospital on 2 August 1915. Mounted below the window is a gentle brown marble tablet with details of the Mead brothers and the tablet is inscribed with the phrases “E’en as they trod that day to God so walked they from their start.

Good day! I could have sworn I’ve visited this site before but after looking at some of the articles I realized it’s new to me. Anyways, I’m certainly pleased I stumbled upon it and I’ll be bookmarking it and checking back frequently.

You ought to take part in a contest for one of the best blogs online. I am going to recommend this web site!

This throws gentle on the connection between the Denton brothers, nanoaugmentation, and the Grey Demise.

??? ?????? ????? ?? ?? ??????? ?? ???? ? ????? ????? ?????. ???? ???????? ????????? ??????????? ????? ????? ????? ?????.

Hello there! I could have sworn I’ve been to this website before but after going through some of the articles I realized it’s new to me. Nonetheless, I’m certainly delighted I discovered it and I’ll be bookmarking it and checking back often.

I absolutely love your blog.. Great colors & theme. Did you build this site yourself? Please reply back as I’m hoping to create my own personal blog and would love to find out where you got this from or what the theme is named. Appreciate it.

I’d like to thank you for the efforts you have put in writing this blog. I am hoping to see the same high-grade blog posts from you later on as well. In truth, your creative writing abilities has motivated me to get my own blog now 😉

Hey I am browsing your article on my Blackberry and I was imagining how cool it will be on my soon to be purchased ipad. Fleeting thought…. Anyway thanks!

The color of your blog is quite great. i would love to have those colors too on my blog.*.;-’

This is a topic that is close to my heart… Many thanks! Where can I find the contact details for questions?

I couldn’t resist commenting. Perfectly written!

dog crates made from ABS Plastic can withstand those aggressive dogs,.

This website was… how do I say it? Relevant!! Finally I have found something that helped me. Many thanks!

After I originally commented I appear to have clicked on the -Notify me when new comments are added- checkbox and now whenever a comment is added I recieve 4 emails with the exact same comment. There has to be a means you can remove me from that service? Thanks a lot.

Wonderful paintings! That is the kind of information that are meant to be shared across the web. Disgrace on the seek for no longer positioning this submit upper! Come on over and visit my website . Thanks =)

I was suggested this website by my cousin. I’m not sure whether this post is written by him as no one else know such detailed about my difficulty. You’re amazing! Thanks!

You actually make it seem so easy with your presentation but I find this topic to be really something that I think I would never understand. It seems too complicated and extremely broad for me. I am looking forward for your next post, I will try to get the hang of it!

It seems you are getting quite a lof of unwanted comments. Maybe you should look into a solution for that. Have a nice day!

The vacation special deals offered are believed as a selection of possibly the most preferred and therefore within your budget all over the globe. Quite a number of hostels can be proudly located inside property which is accented who has striking seashores encouraging crystal-clear rivers, contingency of an Ocean. hotels compare rates

Good post. I will be dealing with a few of these issues as well..

Youre so cool! I dont suppose Ive read anything like that prior to. So nice to seek out somebody by incorporating original applying for grants this subject. realy thanks for beginning this up. this web site can be something that is needed on the web, someone after some originality. beneficial task for bringing interesting things to your net!

Hey! Do you know if they make any plugins to protect against hackers? I’m kinda paranoid about losing everything I’ve worked hard on. Any recommendations?

There are some attention-grabbing closing dates on this article however I don’t know if I see all of them middle to heart. There is some validity but I’ll take hold opinion until I look into it further. Good article , thanks and we want more! Added to FeedBurner as nicely

Im creating articles upon cancers, which can be some tips i was initially undertaking study for when My partner and i observed your blog post submit. There are usually countless health problems available that people are generally being affected by, I had no idea! This can be strong details, many thanks.

I seriously love your website.. Great colors & theme. Did you build this site yourself? Please reply back as I’m trying to create my own website and want to know where you got this from or just what the theme is named. Cheers!

You made a number of nice points there. I did a hunt on the theme and found mainly persons can believe your blog.

It’s a continuous action scene that just bores you half to death by the time the credits roll.

Excellent article. I will be facing a few of these issues as well..

hybrid cars would be the best thing because they are less polluting to the environment..

I was pretty pleased to find this web site. I wanted to thank you for your time just for this fantastic read!! I definitely loved every bit of it and I have you saved to fav to check out new things in your website.

What’s the point of writing this post if it’s being spammed the shit out of it . Good job anyways.

Great write-up, I am normal visitor of one’s blog, maintain up the nice operate, and It is going to be a regular visitor for a lengthy time.

it is really great to get government jobs because the government can give you a good job security..

Very good article! We are linking to this great article on our website. Keep up the good writing.

Your style is really unique compared to other people I have read stuff from. I appreciate you for posting when you’ve got the opportunity, Guess I will just bookmark this site.

That’s why so many science fiction stories use Greek and Roman names, stories and history.

general blogging is great because you can cover a lot of topics in just a single blog,,

Hello! I would wish to make a enormous thumbs up to the fantastic information you may have here within this post. I will be returning to your blog for more soon.

This internet site is often a walk-through rather than the details you wanted about it and didn’t know who ought to. Glimpse here, and you’ll certainly discover it.

Amusing posting. It appears that there are several actions are influenced by the creative thinking element. “We do not quite forgive a giver. The hand that feeds us is in some danger of being bitten.” by Ralph Waldo Emerson..

of fighters to grace the Manny Pacquiao vs Shane Mosley Pay Per View event scheduled today

Just a fast hello and also to thank you for discussing your ideas on this web page. I wound up inside your blog right after researching physical fitness connected issues on Yahoo… guess I lost track of what I had been performing! Anyway I’ll be back once once more inside the long term to examine out your blogposts down the road. Thanks!

I’d perpetually want to be update on new articles on this site, bookmarked

I couldn’t be more in agreement. By the way, do you see more of the same for the days and months ahead? I am very intrigued by your positions and your posts.

The species exhibited in the secret Reef embody sand tiger sharks, bonnethead sharks and inexperienced sea turtles, considered one of which, Oscar, is a rescue animal missing a lot of its rear flippers because of accidents from a ship and a predator.

You need to take part in a contest for one of the best websites on the web. I will recommend this web site!

This gallery can be house to the aquarium’s electric eel, Miguel Wattson, which “communicates” with the general public via a Twitter account to which pre-programmed tweets are posted when it emits electricity.

Tradition maintains that Balthasar, one of the Three Sensible Men who got here from the East to seek out the Christ Child, offered frankincense to the baby as a present.

I wanted to thank you for this wonderful read!! I absolutely loved every bit of it. I’ve got you bookmarked to check out new stuff you post…

I am not sure where you are getting your info, but great topic. I needs to spend some time learning more or understanding more. Thanks for great info I was looking for this info for my mission.

I just desired to come up with a quick comment as a way to express gratitude for you for all those wonderful pointers you are posting here. My own time consuming internet investigation has by the end of the day been rewarded with high quality ways to present to my guests. We would say that a number of us guests can be extremely endowed to appear in a wonderful network with very many marvellous individuals with useful hints. I believe quite privileged to have used your webpages and appearance toward really more fabulous minutes reading here. Thank you for most things.

learning hypnosis is great, i used it to hypnotize myself so that i can relax`

An impressive share, I simply with all this onto a colleague who was simply doing little analysis on this. Anf the husband the truth is bought me breakfast because I came across it for him.. smile. So permit me to reword that: Thnx for any treat! But yeah Thnkx for spending some time to discuss this, I find myself strongly regarding it and adore reading more on this topic. If at all possible, as you grow expertise, can you mind updating your blog post with more details? It is actually extremely of great help for me. Big thumb up just for this writing!

Deference to article author , some good entropy.

I?ve read several excellent stuff here. Certainly value bookmarking for revisiting. I wonder how a lot effort you put to create this kind of magnificent informative site.

I seriously love your website.. Great colors & theme. Did you make this web site yourself? Please reply back as I’m trying to create my own personal blog and want to find out where you got this from or what the theme is named. Appreciate it.

This website can be a stroll-by for the entire info you wanted about this and didn’t know who to ask. Glimpse right here, and you’ll undoubtedly discover it.

Hallo im through indonesia and my personal english isnt that cool, but i was able to understand each single word of the write-up. I’m seeking english blogs to give a lift in order to my personal british capabilities as well as i’m quite glad to serve them with a blog, which publishes obvious as well as structured english which i will probably be able to translate. Many thanks through Indonesia!

There are some interesting points in time on this article but I don’t know if I see all of them heart to heart. There’s some validity however I will take hold opinion till I look into it further. Good article , thanks and we would like extra! Added to FeedBurner as nicely

When he confirmed the first few moves to Ken Coates, a buddy at Leeds, Coates declared, “If that works then I am a monkey’s bum!” The title caught.

Hi there for your personal broad critique, then again particularly passionate the recent Zune, and additionally intend this specific, not to mention the beneficial feedbacks other sorts of everyone has posted, will determine if is it doesn’t answer you’re looking for.

I really like it when folks get together and share ideas. Great blog, stick with it!

It’s hard to find educated people about this topic, however, you sound like you know what you’re talking about! Thanks

He’s proven standing on a ship, symbolically representing the crossing.

Good article. I’m going through many of these issues as well..

Nepomniachtchi performed the English opening, a good psychological choice as a result of there are few forcing traces for Black.

There is certainly a great deal to know about this topic. I really like all the points you’ve made.

I really like your blog site.. excellent shades & style. Do a person pattern this excellent website oneself or even have people hire an attorney to make it happen available for you? Plz answer while I!|m seeking to style and design my very own blog as well as would wish to learn where u obtained this specific out of. thanks a lot

I come up reference an olive offshoot in solitary around, and the freedom fighters gun in the other. Do not detonate the olive limb become lower from my hand.

Spot on with this write-up, I truly suppose this website needs rather more consideration. I’ll in all probability be again to learn much more, thanks for that info.

You must participate in a contest for among the finest blogs on the web. I will advocate this site!

I’d have to consult with you here. Which is not some thing I do! I love to reading an article that may make people feel. Also, thank you allowing me to comment!

This is often a wonderful blog, could you be interested in working on an interview about just how you developed it? If so e-mail myself!

Way cool! Some extremely valid points! I appreciate you penning this write-up and the rest of the site is also very good.

An outstanding share! I have just forwarded this onto a friend who has been doing a little research on this. And he actually bought me breakfast because I stumbled upon it for him… lol. So let me reword this…. Thanks for the meal!! But yeah, thanx for spending some time to discuss this issue here on your internet site.

Next time I read a blog, Hopefully it won’t disappoint me just as much as this one. After all, I know it was my choice to read through, however I genuinely believed you would have something interesting to talk about. All I hear is a bunch of crying about something you could fix if you weren’t too busy searching for attention.

I couldn’t resist commenting. Well written.

I’m pretty pleased to uncover this site. I need to to thank you for your time for this wonderful read!! I definitely really liked every part of it and i also have you book-marked to see new information on your web site.

Many thanks for creating the effort to discuss this, I feel strongly about this and enjoy studying a great deal more on this topic. If feasible, as you gain expertise, would you mind updating your webpage with a great deal more details? It’s very helpful for me.

there are times that good public relations cannot be always achieved,

very good post, i surely adore this fabulous website, persist in it

i always want a dining room that is brightly colored that is why i always paint our room with cream accent,

If you need Brand technique and activation Myanmar companies, then with out hesitation contact them.

Howdy! This blog post couldn’t be written much better! Looking at this article reminds me of my previous roommate! He always kept preaching about this. I most certainly will send this post to him. Fairly certain he’ll have a good read. Thanks for sharing!

Thank you for another informative website. Where else could I am getting that type of info written in such a perfect means? I’ve a undertaking that I am just now working on, and I have been on the glance out for such info.

Generally I do not read article on blogs, but I would like to say that this write-up very forced me to try and do it! Your writing style has been surprised me. Thanks, quite nice article.

I must thank you for the efforts you have put in writing this website. I am hoping to check out the same high-grade blog posts from you in the future as well. In truth, your creative writing abilities has motivated me to get my own, personal site now 😉

The gown is tailor-made with a stretch finish, so you don’t have to.

I like reading an article that will make people think. Also, many thanks for permitting me to comment.

I could not refrain from commenting. Well written.

If this sounds like you, you can view lots of design comfortably, proper in entrance of you, with on-line shops you have the most exquisite collection of jewellery.

Hi, I do believe this is a great site. I stumbledupon it 😉 I will revisit yet again since I saved as a favorite it. Money and freedom is the best way to change, may you be rich and continue to guide others.

This site was… how do you say it? Relevant!! Finally I have found something that helped me. Thanks a lot.

And for me, they offer the right blend of nostalgia and functionality.

I couldn’t resist commenting. Perfectly written!

This site really has all of the information and facts I wanted about this subject and didn’t know who to ask.

Washington at first took quarters throughout the river from Trenton, but on December 15 he moved his headquarters to the house of William Keith in current-day Upper Makefield Township so he was closer to his forces.

Very nice post. I definitely appreciate this site. Continue the good work!

There were three haunted homes each year, although from 1998 on, two every year had been twin-path homes, for a total of five experiences.

She wears a formal gown decorated with massive striped bows.

I blog quite often and I really appreciate your content. This article has really peaked my interest. I am going to bookmark your website and keep checking for new details about once per week. I subscribed to your RSS feed as well.

Very nice article. I definitely appreciate this website. Thanks!

Excellent article! We will be linking to this great content on our website. Keep up the great writing.

That is a very good tip especially to those fresh to the blogosphere. Brief but very precise information… Many thanks for sharing this one. A must read post.

I really love your blog.. Excellent colors & theme. Did you build this website yourself? Please reply back as I’m hoping to create my own website and would like to find out where you got this from or what the theme is named. Many thanks!

Spot on with this write-up, I truly think this web site needs a lot more attention. I’ll probably be returning to read through more, thanks for the advice.

Way cool! Some extremely valid points! I appreciate you penning this write-up plus the rest of the site is also very good.

An intriguing discussion is definitely worth comment. There’s no doubt that that you should write more about this subject, it may not be a taboo subject but generally people don’t speak about such issues. To the next! Kind regards.

Aw, this was an incredibly nice post. Taking a few minutes and actual effort to make a great article… but what can I say… I hesitate a lot and never seem to get nearly anything done.

I truly love your blog.. Pleasant colors & theme. Did you create this amazing site yourself? Please reply back as I’m wanting to create my very own site and want to know where you got this from or exactly what the theme is named. Kudos!

This is a topic that is near to my heart… Best wishes! Exactly where can I find the contact details for questions?

I seriously love your website.. Great colors & theme. Did you make this amazing site yourself? Please reply back as I’m planning to create my own blog and want to know where you got this from or just what the theme is named. Cheers!

Very nice post. I absolutely love this website. Keep writing!

I love looking through a post that can make people think. Also, thanks for permitting me to comment.

An intriguing discussion is definitely worth comment. There’s no doubt that that you ought to write more about this subject, it may not be a taboo matter but usually people don’t discuss these issues. To the next! Best wishes!

I’m impressed, I have to admit. Seldom do I come across a blog that’s equally educative and interesting, and without a doubt, you have hit the nail on the head. The issue is something that too few people are speaking intelligently about. I’m very happy that I found this during my search for something concerning this.

Very good article. I definitely love this site. Thanks!

The Polish legislation didn’t present for additional necessities for such entities over these resulting from the provisions of the commercial legislation.

Hi there! This post could not be written any better! Looking through this post reminds me of my previous roommate! He constantly kept preaching about this. I’ll send this article to him. Fairly certain he’ll have a good read. Thanks for sharing!

This site was… how do I say it? Relevant!! Finally I have found something which helped me. Thanks a lot.

Way cool! Some extremely valid points! I appreciate you penning this write-up plus the rest of the website is very good.

I was able to find good information from your content.

I wanted to thank you for this fantastic read!! I absolutely enjoyed every bit of it. I’ve got you saved as a favorite to look at new stuff you post…

This is the perfect website for everyone who would like to find out about this topic. You realize so much its almost hard to argue with you (not that I personally will need to…HaHa). You certainly put a fresh spin on a topic that’s been discussed for a long time. Great stuff, just excellent.

Aw, this was a really nice post. Taking a few minutes and actual effort to produce a superb article… but what can I say… I put things off a lot and never seem to get nearly anything done.

This site was… how do I say it? Relevant!! Finally I’ve found something which helped me. Thanks a lot!

I could not refrain from commenting. Well written.

문카지노에서 입금이 편리한 사이트 구해요.

Right here is the right blog for anyone who really wants to understand this topic. You know a whole lot its almost hard to argue with you (not that I personally would want to…HaHa). You definitely put a fresh spin on a subject that’s been written about for years. Great stuff, just great.

Pretty! This was an extremely wonderful article. Many thanks for supplying these details.

With havin so much content do you ever run into any issues of plagorism or copyright infringement? My website has a lot of exclusive content I’ve either created myself or outsourced but it appears a lot of it is popping it up all over the internet without my authorization. Do you know any methods to help prevent content from being ripped off? I’d genuinely appreciate it.

Saved as a favorite, I like your web site!

After looking into a handful of the blog posts on your blog, I honestly appreciate your technique of writing a blog. I added it to my bookmark webpage list and will be checking back soon. Please visit my web site as well and let me know what you think.

Your style is so unique in comparison to other people I’ve read stuff from. Thank you for posting when you’ve got the opportunity, Guess I will just book mark this site.

When I initially commented I seem to have clicked the -Notify me when new comments are added- checkbox and from now on every time a comment is added I receive 4 emails with the same comment. Perhaps there is a means you can remove me from that service? Thanks.

Excellent post! We are linking to this particularly great article on our website. Keep up the great writing.

Oh my goodness! Amazing article dude! Thank you, However I am having problems with your RSS. I don’t know why I can’t subscribe to it. Is there anyone else having similar RSS issues? Anyone that knows the solution will you kindly respond? Thanks.

Chozick, Amy (June 29, 2013).

This is a topic that’s close to my heart… Cheers! Exactly where can I find the contact details for questions?

However researchers were curious — do male gestational carriers have a few of the identical methods that females use for more sturdy offspring?

You are so cool! I don’t think I have read through something like this before. So great to find someone with a few original thoughts on this subject. Really.. many thanks for starting this up. This site is one thing that is needed on the internet, someone with some originality.

So what are the ways to secure a future in a safe way?

From ancient Egypt to the twenty first century, Firoza stone has transformed our lives with fascinating jewelry and spirituality.

An impressive share! I have just forwarded this onto a coworker who was conducting a little homework on this. And he in fact ordered me dinner simply because I discovered it for him… lol. So let me reword this…. Thanks for the meal!! But yeah, thanx for spending some time to discuss this issue here on your internet site.

In my very own case, just a few months ago someone from one of many most generally-suspended servers within the fediverse picked one among my extra innocuous posts that had been boosted into his view and clowned in my replies in the same old method even supposing my house server had long since suspended the troll’s server.

I needed to thank you for this very good read!! I absolutely enjoyed every bit of it. I have got you bookmarked to check out new stuff you post…

Powerful to image, proper?

Hi, I do believe this is an excellent site. I stumbledupon it 😉 I am going to return yet again since i have bookmarked it. Money and freedom is the best way to change, may you be rich and continue to guide others.

I want to to thank you for this good read!! I certainly enjoyed every bit of it. I have you book-marked to check out new stuff you post…

It invested over 拢1.8 billion from its formation and alongside private capital provided 拢6.5 billion in credit for SMEs.

This site definitely has all of the info I needed about this subject and didn’t know who to ask.

Rooney, MacKenzie (November 9, 2022).

I have to thank you for the efforts you’ve put in penning this site. I’m hoping to view the same high-grade blog posts from you in the future as well. In fact, your creative writing abilities has inspired me to get my own, personal website now 😉

Solely then will it be attainable to say that the nations have entered the path of culture.

The next time I read a blog, I hope that it won’t fail me just as much as this one. I mean, Yes, it was my choice to read through, however I actually thought you would have something helpful to say. All I hear is a bunch of whining about something that you could fix if you weren’t too busy searching for attention.

Having read this I thought it was very enlightening. I appreciate you taking the time and effort to put this information together. I once again find myself personally spending a significant amount of time both reading and posting comments. But so what, it was still worthwhile!

감사합니다!

Nice post. I learn something totally new and challenging on sites I stumbleupon everyday. It’s always interesting to read articles from other authors and use something from their web sites.

Hello there, There’s no doubt that your web site could be having internet browser compatibility problems. Whenever I take a look at your site in Safari, it looks fine but when opening in I.E., it has some overlapping issues. I simply wanted to give you a quick heads up! Apart from that, excellent website!

too much vitamin-a can also cause osteoporosis but aging is the number cause of it*

I absolutely love your website.. Pleasant colors & theme. Did you make this web site yourself? Please reply back as I’m trying to create my own blog and would like to learn where you got this from or what the theme is called. Many thanks!

It’s nearly impossible to find knowledgeable people in this particular topic, but you sound like you know what you’re talking about! Thanks

I absolutely love your website.. Excellent colors & theme. Did you build this web site yourself? Please reply back as I’m planning to create my very own blog and would like to find out where you got this from or what the theme is named. Appreciate it!

There is noticeably a lot of money comprehend this. I assume you made certain nice points in functions also.

You’re so cool! I do not suppose I have read something like this before. So wonderful to find someone with some unique thoughts on this subject matter. Seriously.. thanks for starting this up. This web site is one thing that is needed on the internet, someone with a bit of originality.

very nice post, i surely love this web site, persist in it

This is a topic that’s near to my heart… Take care! Exactly where are your contact details though?

Everything is very open with a very clear explanation of the issues. It was truly informative. Your site is extremely helpful. Thanks for sharing.

Do you have a spam problem on this blog; I also am a blogger, and I was wanting to know your situation; many of us have developed some nice practices and we are looking to exchange solutions with other folks, be sure to shoot me an email if interested.

Thanks, I have just been looking for info approximately this topic for a long time and yours is the best I have came upon so far. But, what in regards to the bottom line? Are you certain concerning the supply?

They turned up first-particular person accounts of among the pilots who were involved in a high-secret mission known as “Operation Cumulus.” Throughout this August 1952 operation, RAF pilots flew above the cloud line, dropping payloads of dry ice, salt and – like the Chinese language at the moment use – silver iodide.

This is a topic that is close to my heart… Take care! Exactly where are your contact details though?

You made some decent points there. I checked on the web for additional information about the issue and found most people will go along with your views on this site.

I discovered your web page just recently through a recommendation and had a look at some of your articles. I like what you are writing about and I hope you keep up the good work. If you are interested in sharing some content or swap links do not hesitate to get in touch with me.

Youre so cool! I dont suppose Ive read anything in this way before. So nice to locate somebody by original thoughts on this subject. realy thanks for beginning this up. this fabulous website is one thing that is needed on the internet, a person with a bit of originality. beneficial project for bringing a new challenge towards internet!

It was invented particularly for Deus Ex by the Deus Ex writers, and the snippets that seem there are all that exist of the “ebook”.

Hello there! I just want to offer you a huge thumbs up for your great info you have right here on this post. I am returning to your website for more soon.

Courthouse Square Antique Cards.

May I simply say what a relief to uncover a person that truly understands what they are talking about online. You actually realize how to bring a problem to light and make it important. A lot more people need to check this out and understand this side of your story. I was surprised you aren’t more popular given that you certainly possess the gift.

thank-you for this post (désolé, je suis francais, je parle mal anglais)

I’ve been surfing on-line greater than three hours as of late, but I by no means found any interesting article like yours. It¡¦s pretty worth enough for me. In my opinion, if all website owners and bloggers made good content as you probably did, the internet can be much more useful than ever before.

This web page is really a walk-through for all of the information you wished about this and didn’t know who to ask. Glimpse here, and you’ll definitely discover it.

This site really has all of the information I needed about this subject and didn’t know who to ask.

Hello there! I could have sworn I’ve been to this website before but after going through a few of the posts I realized it’s new to me. Regardless, I’m definitely delighted I stumbled upon it and I’ll be bookmarking it and checking back frequently!

Hanna, Maddie (June 3, 2020).

Good article. I’m dealing with some of these issues as well..

You probably have scars that are beneath the surface of the skin, fillers like collagen or your own fats might be injected into the scars.

Having read this I thought it was rather enlightening. I appreciate you finding the time and energy to put this informative article together. I once again find myself spending a lot of time both reading and posting comments. But so what, it was still worth it!

This website was… how do I say it? Relevant!! Finally I have found something that helped me. Cheers.

Hi there! This blog post couldn’t be written any better! Looking at this post reminds me of my previous roommate! He continually kept talking about this. I am going to forward this post to him. Fairly certain he’s going to have a very good read. I appreciate you for sharing!

It’s hard to come by well-informed people in this particular subject, but you sound like you know what you’re talking about! Thanks

Saved as a favorite, I like your web site.

And people simply check their forex enterprise maybe only ten minutes a day.

This is a topic which is close to my heart… Thank you! Where can I find the contact details for questions?

It is not simply an inquiry into how doubtless you’re to sacrifice plush motels for hostel beds.

American Journal of Archaeology.

So, this was simply the fundamentals of the options and futures contracts.

You made some good points there. I checked on the net to find out more about the issue and found most individuals will go along with your views on this web site.

Aw, this was an exceptionally nice post. Taking a few minutes and actual effort to produce a really good article… but what can I say… I put things off a lot and don’t manage to get anything done.

Your style is really unique compared to other people I have read stuff from. Thanks for posting when you’ve got the opportunity, Guess I will just bookmark this blog.

You ought to be a part of a contest for one of the finest websites on the internet. I most certainly will highly recommend this website!

Way cool! Some very valid points! I appreciate you penning this article and also the rest of the website is also very good.

While governments worldwide rally about regulations on digital assets, constant efforts are being made to advance the Central Bank Digital Currencies (CBDC) projects in different countries.

Sometimes the very same quarterly earnings report will paint two very different pictures of a company’s performance based on competing calculations.

Howdy, I believe your blog could possibly be having browser compatibility problems. When I take a look at your blog in Safari, it looks fine however when opening in I.E., it has some overlapping issues. I simply wanted to give you a quick heads up! Other than that, fantastic site.

I’m amazed, I have to admit. Seldom do I encounter a blog that’s both educative and interesting, and let me tell you, you have hit the nail on the head. The issue is something too few folks are speaking intelligently about. I am very happy that I stumbled across this during my hunt for something regarding this.

Starting a business can be overwhelming, but with the right resource, you can streamline your launch. This comprehensive guide provides insights on how to develop a successful enterprise and mitigate common obstacles. Check out this link for further insights and to explore more about starting.a business.

Everything is very open with a precise explanation of the challenges. It was definitely informative. Your site is very useful. Thank you for sharing!

This is fantastic! Full of helpful insights and highly clear. Many thanks for providing this.

This article is extremely enlightening. I really enjoyed going through it. The content is extremely structured and straightforward to comprehend.

You need to take part in a contest for one of the most useful websites on the web. I will recommend this blog!

A: Greater than 1.76 billion candy canes are made yearly for the Christmas season.

But can we really simulate the world itself?

Hi, I do believe this is a great website. I stumbledupon it 😉 I will return once again since I bookmarked it. Money and freedom is the greatest way to change, may you be rich and continue to help others.

There may be so much life outdoors our workstation.

Simply wanted to mention my experience with Adam J. Graham’s The Growth Mindset email series. If you’re not in the loop, the entrepreneur behind JustFix is the founder behind his startup, and his email has turned into one of my most helpful guides for staying ahead in tech, entrepreneurship, and entrepreneurship. I’ve been reading it for a long time now, and it’s definitely one of the best guides I’ve found for both personal and professional growth. Check out the full discussion on Reddit here.

Such an educational entry! I gained a lot from reading it. This content is very well-organized and simple to understand.

This is a topic that is near to my heart… Thank you! Exactly where can I find the contact details for questions?

For instance, a central financial institution might regulate margin lending, whereby people or firms might borrow in opposition to pledged securities.

You made some really good points there. I checked on the internet for more info about the issue and found most people will go along with your views on this site.

Your style is very unique compared to other people I have read stuff from. Many thanks for posting when you’ve got the opportunity, Guess I will just bookmark this page.

Great web site you have got here.. It’s hard to find good quality writing like yours these days. I really appreciate people like you! Take care!!

This article is extremely informative. I genuinely appreciated perusing it. The details is extremely structured and simple to follow.

You have made some really good points there. I checked on the net to find out more about the issue and found most people will go along with your views on this website.

This is a topic that is close to my heart… Many thanks! Exactly where are your contact details though?

Greetings! Very helpful advice in this particular post! It’s the little changes that will make the largest changes. Thanks for sharing!

Since the colonists had no representation in Parliament, the taxes violated the assured Rights of Englishmen.

Very good article! We will be linking to this particularly great article on our website. Keep up the good writing.

There is definately a great deal to find out about this topic. I like all the points you have made.

I truly love your website.. Excellent colors & theme. Did you build this website yourself? Please reply back as I’m attempting to create my own personal blog and would like to know where you got this from or exactly what the theme is named. Appreciate it.

Pretty! This was an extremely wonderful article. Thanks for supplying this info.

This article is fantastic! Filled with valuable insights and highly clear. Many thanks for sharing this.

This is a great tip particularly to those fresh to the blogosphere. Short but very precise information… Appreciate your sharing this one. A must read article!

Having read this I believed it was really enlightening. I appreciate you taking the time and energy to put this informative article together. I once again find myself spending a significant amount of time both reading and leaving comments. But so what, it was still worthwhile.

As the name suggests, the FSEOG is meant to supplement other financial aid.

I blog quite often and I truly appreciate your information. The article has really peaked my interest. I am going to book mark your website and keep checking for new details about once per week. I subscribed to your Feed as well.

Saved as a favorite, I really like your web site!

Very nice article. I definitely love this site. Continue the good work!

I like it whenever people get together and share views. Great blog, keep it up.

This post is fantastic. I gained plenty from reading it. The information is very enlightening and well-organized.

The second death was in Allegheny County.

The decree set up a steering committee consisting of Bormann, Lammers, and Basic Wilhelm Keitel to oversee the trouble, with Goebbels and Speer as advisors; Goebbels had expected to be one of the triumvirate.

Situated in the most exclusive areas of Crete, these opulent villas provide the ultimate atmosphere for an outstanding escape. Find your perfect escape.

James Harkness Hutchinson, Reserve Constable, Royal Ulster Constabulary.

Very good information. Lucky me I discovered your site by chance (stumbleupon). I have saved it for later!

Your style is unique compared to other folks I have read stuff from. I appreciate you for posting when you’ve got the opportunity, Guess I will just bookmark this blog.

A successful investor is the one who has over the years studied the market and understands the pitfall very well and also knows the strategies to avoid them at all costs.

A fascinating discussion is worth comment. I do believe that you should publish more about this subject matter, it might not be a taboo subject but generally folks don’t speak about these subjects. To the next! Many thanks.

7-f5. Now, both White’s bishops are diminished to defence, and White’s queen is diminished to passivity on the a2-sq.

The top niches are: Entertainment, health, weight loss, internet advertising and marketing, affiliate internet marketing, finance, romance and relationship.

The latter cleverly suggested, without actually imitating, the mahogany-and-birch cabinet-shop bodies typically found on the station wagons of that era.

It closed the settlement gap between the Wiehre and Littenweiler, and connected with Freiburg’s city centre.

Vibrations throughout operation may cause it to fall or tilt onto one side.

Should you wish to optimize your profile in probably the most proficient manner then you have to make it positive that you will be in touch with an Web optimization company in India.

Nice article this is going to help my chinese mandarin tutoring service!

After looking into a few of the articles on your web page, I really appreciate your way of blogging. I book marked it to my bookmark webpage list and will be checking back in the near future. Take a look at my website too and tell me your opinion.

The U.S. stock market crash of 1929 greatly affected the landscape of entertaining for the decade of the 1930s.

Going to use this for my SEO agency!

In the event you ever need to sell your Analog Man pedals, you’re going to get much more for them, as they hold their values higher resulting from our popularity and selling practices.

Thsi will help with my chinese online tutoring lessons.

I’m pretty pleased to find this site. I want to to thank you for ones time for this fantastic read!! I definitely liked every bit of it and i also have you saved to fav to look at new stuff in your web site.

Thsi will help with my Google Entity Stacking service.

Outcomes: The firm has recovered hundreds of tens of millions of dollars for shoppers across Florida and nationwide, see some of our outcomes.

Any loan can damage a credit score if the person has too high of a loan-to-income ratio or misses payments.

Thsi will help with my Google Entity Stacking service.

James, Emily St (2019-03-20).

Thsi will help with my Google Entity Stacking service.

Thsi will help with my Google Entity Stacking service.

Corded drills by no means need to be recharged and are often extra highly effective than their cordless counterparts.

Thsi will help with my Estrogen Blocker Supplements!

After checking out a handful of the articles on your web site, I truly like your technique of blogging. I book-marked it to my bookmark site list and will be checking back soon. Please check out my web site as well and tell me how you feel.

Thsi will help with my Estrogen Blocker Supplements!

In line with the World Financial institution, the 2013 nominal GWP was roughly 75.59 trillion United States dollars.

However, one should always take help from a consultant who will help in the right ERP implementation procedure.

Of central importance in public and listed companies is the securities market, typified by the London Stock Exchange.

Noise from building, demolition or removal of a residence is managed via the final environmental responsibility and the general prohibition of unreasonable noise.

Thsi will help with my Estrogen Blocker Supplements!

Your first pitch can be a sport changer so play it safe all the time.

Keep in mind that automatic payments will be withdrawn even if you don’t have enough funds in your account, and this can trigger overdraft fees.

I must thank you for the efforts you’ve put in writing this site. I am hoping to view the same high-grade content from you later on as well. In truth, your creative writing abilities has encouraged me to get my own, personal blog now 😉

Thsi will help with my Estrogen Blocker Supplements!

It was a formidable race automobile, profitable at Daytona as well as Monza.

This opens the door to widespread promotion of inaccurate and unproven buying and selling methods for stocks, bonds, commodities, or Forex, whereas generating sizable revenues for unscrupulous authors, advisers and self-titled trading gurus.

A more streamlined pale green fastback sedan with hidden front wheels was advertised “for winter touring.” While the beige-and-maroon, long-deck, four-window sedan “for rapid travel” brought to mind a zeppelin, the four-window sedan with rear suicide doors echoed a Hooper-bodied Rolls-Royce in its black and dark blue livery.

In case you have been attempting to interrupt into the world of property development and are unable to because of a scarcity of funding capital, you may want to think about working with a property investment group to your initial investments.

This web site too may be very consumer friendly and attention-grabbing and hence is a good alternative to Manga Fox.

A prefix: parameter at the end of a query in the search field, furthermore, will override any namespace there, or any profile underneath that.

This design plays with opposites, making a dynamic and visually putting space.

The benefit of this type of program is that it removes the burdensome and costly process of litigation (dealing with a lawsuit) and provides guaranteed benefits for workers.

Thsi will help with my Estrogen Blocker Supplements!

It is advisable to fittingly learn that almost all capital comes from good stock tips and also a certain total exposure to the share market functioning will go a long way.

This production function must, however, be adjusted to account for the refurbishing and augmentation of existing buildings.

Your style is really unique compared to other folks I have read stuff from. Many thanks for posting when you’ve got the opportunity, Guess I will just bookmark this web site.

thanks for this article!

His was the first English translation of the Septuagint printed.

But when you are the sort of highly organized person who does not thoughts receiving and deciphering multiple earnings summaries, consider the advantages of leaving your 401(k) savings proper where they’re.

It was hosted by Boom, Shinee’s Key, and Itzy’s Yuna, and broadcast reside at Namdong Gymnasium from 18:00 (KST).

thanks for this article!

After betting very successfully against the market in 1980, the firm began to receive significant attention.

In: NNU 41 (1972), p.

thanks for this article!

The former Wagoneer Limited returned to showrooms as the Grand Wagoneer.

Mark 16:17 We are going to cast out devils in the Name OF JESUS CHRIST, and communicate with new tongues by THE HOLY SPIRIT.

You could have a lot of myths that are related to the automated investment platforms.

It took time to grow to be aware of the Unreal engine.

This uncommon automobile hit an insane top velocity of greater than 250 mph again in 2007, however production of the model stopped in 2013.

Those pics are also included on this web page under.

When Dom shows Brian his dad鈥檚 car, he tells Brian about his dad鈥檚 death.

Industrial finance is made out there to the traders by means of bills of change, which are discounted by the bill market.

The coming of the tram means a farewell to a traditional live-and-let-dwell attitude.

Some banks allow you to write checks and use an ATM card with the account free of charge while others charge hefty fees for the same privileges.

thanks for this article!

A lot of the glass is in the style of Chartres Cathedral with deep blue featuring because the background colour in most home windows.

Most salons are good at swapping out provides and cleaning instruments as prescribed by law, but there are all the time exceptions.

thanks for this article!

People speak many other languages in North America, mainly due to immigration, including Chinese, Tagalog, Vietnamese, German, Italian, Korean and many more.

That pitcher is then awarded a shutout, though not a whole sport.

For those adores cuisine, Greek Crete presents a foodie paradise with regional Greek meals. Enjoy seafood delights, virgin olive oil, and seasonings that define the regional cuisine. Read more

At its most basic, a risk is anything that can negatively affect your profits on an investment.

Sodium is good in your physique in small quantities, but it may be very harmful should you ingest an excessive amount of.

thanks for this article!

thanks for this article!

This is a topic which is near to my heart… Cheers! Exactly where can I find the contact details for questions?

Ibn Ezra hinted, and Bonfils explicitly said, that Joshua wrote these verses many years after the demise of Moses.

In 1928, the American Chatillon Company started development of a rayon plant in Rome; it was a joint enterprise effort with the Italian Chatillon Company.

Partially, this is because so many regular Navy activities take place inside ships.

thanks for this article!

Star Wars: The Clone Wars first aired on Cartoon Network in 2008.

In the early 20th century Western Union acquired rights to an improved ticker which could deal with the increasing volume of stocks sold per day.

Lower them out. Use markers to draw on his eyebrows, eyelashes, lips, and cheeks.

What I did, since I’m honestly not aware of which adverts are collected, is title each full web page advert in the difficulty from the inside-entrance-cover to the again cover with all full-web page adverts included that came in between.

This exploited Bordentown’s natural location as the purpose on the Delaware River that supplied the shortest overland route to Perth Amboy, from which cargo and people could possibly be ferried to New York City.

Being unbiased, they will choose and select where their funding comes from, which bolsters their skill to stay impartial.

Such discrimination has imposed vital economic prices, studying disruption, and denial of financial opportunities for individuals of coloration.

Hello! I could have sworn I’ve been to this blog before but after looking at some of the posts I realized it’s new to me. Nonetheless, I’m definitely delighted I discovered it and I’ll be book-marking it and checking back frequently.

As an attendee of our course or applications you (and/or your employer) shall not acquire any right to the course supplies.

Simple spreads can be set up to ensure some profit no matter which way the market moves after you enter.

Its floor is rolling in character, and it forms, with the upper Peninsula of Michigan, a type of plateau between the lakes and rivers which sure it on the east, north, and west.

I’m very happy to find this great site. I need to to thank you for your time due to this fantastic read!! I definitely liked every little bit of it and I have you saved as a favorite to see new things on your website.

An impressive share! I’ve just forwarded this onto a coworker who has been doing a little research on this. And he actually bought me breakfast due to the fact that I stumbled upon it for him… lol. So allow me to reword this…. Thank YOU for the meal!! But yeah, thanx for spending some time to discuss this topic here on your site.

One other figure offered by GM estimates that a Volt pushed for 15,000 miles (24,140 kilometers) per yr without ever exceeding the battery-solely range would use $300 price of electricity annually.

I think a beginner ought to do the next: for reside video games (and even pc video games), play through the sport over the board as always.

sex nhật hiếp dâm trẻ em ấu dâm buôn bán vũ khí ma túy bán súng sextoy chơi đĩ sex bạo lực sex học đường tội phạm tình dục chơi les đĩ đực người mẫu bán dâm

They assume that since you might be in one other nation that you will just hand over or disappear.

A board, be it in large conglomerates or large state owned enterprises (and government departments), set’s direction for the organization and decide on the strategy that would get them to the winning line.

Consider or not, a baby doesn’t care if he sleeps in a Dresser drawer, so long as he’s dry and effectively fed.

When Rainey first heard Milwaukee ranked third within the nation for lowest homeownership by African Individuals he mentioned he was shocked.

I was able to find good advice from your articles.

The securities can be furnished as collateral closer to the mortgage.

I really like it whenever people come together and share opinions. Great site, stick with it.

If you are more guided by technical analysis, then look for the good opportunities based on the latest technical outlook.

Bordentown City’s one sq.

May I simply say what a comfort to discover a person that really understands what they are talking about on the internet. You definitely know how to bring an issue to light and make it important. More and more people have to check this out and understand this side of your story. I was surprised you aren’t more popular since you definitely have the gift.

The above-mentioned exception was 1951’s new hemispherical-head V-8, Chrysler’s greatest achievement of the decade.

Reginald Alfred Hughes, Chief Govt Officer, Ministry of Agriculture, Fisheries & Food.

The sound of the explosion was heard on the Passaic Hearth Headquarters close by, and after they arrived, they discovered all of the home windows and doors blown out and flames taking pictures out of all instructions.

Next time I read a blog, I hope that it does not disappoint me just as much as this particular one. After all, I know it was my choice to read, but I really believed you would have something interesting to say. All I hear is a bunch of moaning about something that you can fix if you were not too busy seeking attention.

That’s why they assist through their emergency service 24 hours a day, 7 days per week.

The twister weakened as it paralleled the interstate, inflicting EF1 injury along McGinnis Highway and Bristow Road.

4 p.m. and being careful in snow and sand, which reflect rays.

Can I just say what a relief to discover somebody who really understands what they are discussing online. You certainly realize how to bring a problem to light and make it important. More and more people ought to look at this and understand this side of your story. It’s surprising you’re not more popular given that you most certainly possess the gift.

These track the performance of an underlying commodity index including total return indices based on a single commodity.

Elmo got his huge break when “Sesame Street” producers decided they needed a crimson monster on the set.

When you use products that contain concentrations of greater than 5 p.c lactic acid in their ingredient record, chances are you’ll find it lightens your pores and skin, which is exactly what you want if in case you have age spots or other discoloration.

Greetings! Very helpful advice within this post! It is the little changes that make the most important changes. Many thanks for sharing!

The minimum tick is 10 cents.

Moreover, the Chinese language authorities will revise related regulations to permit overseas traders to hold no more than 49 p.c of shares in a joint-venture security firm.

In any company, meetings are the lifeblood of company organisation, and can be used to set agendas, targets, carry out evaluations, diffuse evaluation finings, analyse trends and brainstorm.

They are going to make it easier to by offering certain piece of knowledge together with about yourself, duration of your current job, your everlasting deal with and how long you might have been staying there, and so on.

If people can quickly and easily avoid seeing those ads, Web sites will have to find a new business model for providing content while turning a profit.

You may split a water drop into smaller drops, and you’ll put small water drops together.

2018-12-01 Steve Aoki feat.

At that time, it was the 7th largest commercial bank in Uganda by assets.

Barr won the celebration’s nomination after six rounds of balloting on the 2008 Libertarian Occasion Nationwide Convention.

The value limit is the biggest amount the commodity contract is allowed to move in one single day.

It’s possible you’ll not decide up the upcard to add to a canasta, but you need to use cards out of your hand.

Preda, Daniela, 1960-. Bruxels.

You’ll be able to go to varied firms’ web sites and search for details about their merchandise or call their agent advisors to explain issues this could be tedious and time consuming and definitely not goal enough.

You have made some decent points there. I checked on the web for additional information about the issue and found most people will go along with your views on this site.

CD’s and on-line restricted Web records database.

Southwest Louisiana War Veterans Dwelling provides further therapy providers to its residents, together with occupational therapists (in-house).

Others are going to be safer, but none of them are free of the risk of causing a fire.

Way cool! Some extremely valid points! I appreciate you penning this article and also the rest of the site is very good.

On April 10, 2009, Equity announced an auction of all its stations, held on April 16 in Dallas.

The EU could make another strong move by bolstering its euro stability fund.

This is a topic that is near to my heart… Take care! Exactly where can I find the contact details for questions?

Others exit and do exactly that – take risks and spend hour after hour studying in regards to the stock market and news, and even finding the newest suggestions with a view to hit an enormous payout.

Commander Geoffrey Ronald Bartlett.

This web site definitely has all the information and facts I wanted concerning this subject and didn’t know who to ask.

Massage of the again and abdomen have to be avoided for the duration of the first sixteen months as the friction could market miscarriage.

Census Bureau, the county has a complete space of 624 sq.

Hi there! This blog post couldn’t be written any better! Looking through this post reminds me of my previous roommate! He always kept preaching about this. I most certainly will send this post to him. Pretty sure he’s going to have a very good read. I appreciate you for sharing!

The vendor of such items and providers is known as an exporter, whereas the international buyer is known as an importer.

Some parts of the headend only movement a method into the system, such as the cable company’s video feed.

He dabbled with being a vegetarian and vegan at occasions, and for a while was convinced that having a meat-free food plan, free of toxins, meant he didn’t produce physique odor.

A claim may be submitted without a policy number for a policyholder with a common name who lives in a state with a high population.

We not at all promise or assure that you’ll get the very same results as they have, your outcomes may be larger or decrease however most importantly, you solely stand an opportunity of attaining some level of success if you implement.

This was partly due to the prevailing architectural style in the first half of the twentieth century, but it surely was additionally a end result of latest York’s zoning restrictions.

Some well-favored symbols utilized in jewelries are OM, Swastic, and Cross and so forth.

Executive and administrative assistants, who provide research and clerical support to others, both make the list with average salaries between $33,500 and $50,000.

The targets ought to be flexible and be revisited whenever there are main changes available in the market.

Each time cumulative quantity doubles, worth-added prices (including administration, advertising, distribution, and manufacturing) fall by a constant share.

One among the big benefits of the Wen 6377 is the inclusion of a triangular head along with the standard 8.5-inch spherical version.

This post is wonderful. I learned plenty from reading it. The details is extremely educational and well-organized.

Not always, but when I need to be, I can get there.

Greasels are genetically altered creatures seen in DX.

Furthermore, additionally it is assumed that a shift of strategy was obligatory because cash aggregates are normally not good indicators of future economic coverage necessities on account of unreliability of measurement.

Scheduled for sale in summer 2007, it’s easily recognized by familiar but evolved styling that takes inspiration from Cadillac’s recent award-winning Sixteen concept sedan.

This system received criticism for its inability to adapt to changes within the United States economy.

Common again made use of licensed properties from others, including The Strolling Dead, Alien vs.

Earlier, clients had no choice but to just accept the single fee for the day for overseas currency alternate at the various banks and foreign money trade shops in Bangalore.

Although manually filling sandbags is the simplest and least costly technique, it’s also probably the most time-consuming.

These Soccer Group Sheet Templates largely come with a cartoon of famous footballers enjoying the ball which is accompanied by a worksheet to be crammed up with a narrative or paragraph concerning the footballer by your youngster.

It also well-known for its educational institutions, even with all the industrial and technological growth, its traditions and old customs are still considered in high esteem.

Investigations into the unregulated oil futures exchanges turned up major financial institutions like Goldman Sachs and Citigroup.

I have to thank you for the efforts you’ve put in penning this site. I really hope to view the same high-grade content by you in the future as well. In truth, your creative writing abilities has motivated me to get my very own site now 😉

You’re so cool! I do not suppose I’ve truly read something like that before. So wonderful to find another person with unique thoughts on this subject matter. Seriously.. thanks for starting this up. This website is something that is needed on the web, someone with some originality.

Everything is very open with a precise description of the issues. It was definitely informative. Your website is very helpful. Thanks for sharing.

Very useful content! I found your tips practical and easy to apply. Thanks for sharing such valuable knowledge!

The next time I read a blog, I hope that it won’t fail me as much as this one. I mean, I know it was my choice to read, however I actually believed you’d have something interesting to talk about. All I hear is a bunch of whining about something that you can fix if you weren’t too busy seeking attention.

I’m pretty pleased to discover this page. I wanted to thank you for ones time just for this wonderful read!! I definitely really liked every part of it and i also have you saved to fav to check out new information on your web site.

This blog was… how do I say it? Relevant!! Finally I’ve found something that helped me. Thanks a lot.

You need to be a part of a contest for one of the finest blogs on the web. I will highly recommend this site!

Earnings aren’t topic to federal tax — and most frequently not to state tax either.

Hello, I believe your web site might be having browser compatibility problems. When I take a look at your site in Safari, it looks fine however, when opening in I.E., it has some overlapping issues. I just wanted to provide you with a quick heads up! Other than that, fantastic blog!

Few accounting firms charge by the hour while others work on a monthly retainer.

I’m really pleased with the fantastic health services offered in Singapore. The experienced methodology to client care is genuinely remarkable. After receiving various treatments, I can confidently say that seeking a physio in Singapore is the best decision for individuals needing quality rehabilitation care.

I’m amazed with the outstanding health services available in Singapore. The experienced practice to patient care is truly remarkable. After trying various rehabilitation programs, I can certainly say that consulting a physio in Singapore is the right choice for individuals seeking reliable physiotherapy care.

The final word owner known as the useful proprietor.

The advisory teams of online advisory firms operate with the commitment to assist individuals and businesses in achieving their investment goals.

Tenure of such funding is 8 years.

Nonetheless, each time you play that individual you end up shedding, always falling for this or that trap or making a foul transfer.

If you like tales like What’s Unsuitable With Secretary Kim, then this may be your cup of tea.

When you pump $30 into your tank, that money is broken up into little pieces that get distributed amongst several entities.

This web site definitely has all the info I needed about this subject and didn’t know who to ask.

Part 8 (also recognized as the housing choice voucher program) is a federally funded program administered by state housing authorities.

You’ll also discover services for chocolate, desserts and many other luxurious items.

Anybody can purify oneself by performing Umrah, due to this fact the perfect recommendation for everyone is to perform Umrah, because it is possible for you.

This Market in India operates with the aim to provide masses with the investment options along with being a source of funds for various organizations and institutions.

Morse supplied vocals for the first observe on Jordan Rudess’ tribute album The Street Dwelling.

Hello there! I could have sworn I’ve been to this blog before but after browsing through some of the articles I realized it’s new to me. Regardless, I’m definitely delighted I found it and I’ll be book-marking it and checking back frequently.

A major finding with ANNs and stock prediction is that a classification approach (vs.

This is because hazards are affected by current and future changes in climate.

Ready to get started and sell your first item?

Shirley Diana Kinsey. For Catering Providers to the Japanese Area Sea Cadet Corps.

There was one haunted house, the event ran seven nights, and admission was S$60.00.

If our priority is to let people waste away in poverty, have ill health, have their work not be valued, then we won’t prioritize a guaranteed income as part of our national budget.

You’ve made some good points there. I checked on the net to learn more about the issue and found most individuals will go along with your views on this site.

Above all your interest issues.

Online applications can use chat rooms, instant messaging, teleconferencing, and video conferencing to communicate.

With ‘American’ choices it is sort of doable to exercised every time between the purchase in addition to expiration in addition to in contrast to with regards to ‘European’ choices they may be exercised only on the fixed date (expiration date).

Neltz, András (September 15, 2014).

Very good info. Lucky me I recently found your site by chance (stumbleupon). I’ve book-marked it for later!

Nowadays, people are still able to get their internet service through AOL, with more than 2 million rural subscribers using it for dial-up service.

However for dramatic improvements in sound quality, you’ll need extra than just a brand new car stereo.

Once rubbed or sprayed onto the skin, the formulation breaks down the chemical bonds that hold the protein structure of your hair collectively.

2023 IGNYTE Award Nominee for Greatest in Center Grade Ruby Finley vs.

They’re the most typical sort of pool pump.

Aside from the home windows created for Pugin’s churches in England and Ireland, two of Hardman’s main commissions had been to come back from Australia.

For some people, it’s inexperienced when it contains a excessive proportion of recycled supplies; for others, it is when it would not contain dangerous substances that may cause well being problems.

The primary section would supply the vaccine to critical populations, together with healthcare staff, first responders, vital employees, important workers, folks over the age of 65, and people living in congregate settings.

26 communities across the U.S.