Long Cash & Dollar

Welcome to our official publication of the Prometheus ETF Portfolio. The Prometheus ETF portfolio systematically combines our knowledge of macro & markets to create an active portfolio that aims to offer high risk-adjusted returns, durable performance, & low drawdowns. Given its systematic nature, we have tested the Prometheus ETF Portfolio through decades of history and have shown its durability. For those of you who are unacquainted with our systematic process, we offer a detailed explanation here:

In this publication, we will discuss the performance, positioning, & risks of the Prometheus ETF Portfolio and it will be published every week on Fridays to help investors understand how our systematic process is navigating through markets. Before diving into our ETF Portfolio positions, we think it is important for subscribers to understand the context within which our systems choose their exposures. Below, we offer our latest Month In Macro note, which contains the conceptual underpinnings of our systematic process within the context of the latest economic data:

We will keep today’s note extremely brief as we are in the process of putting the final touches on the next edition of Month In Macro. We highly recommend you get acquainted with our outlook from the last edition prior to the next one.

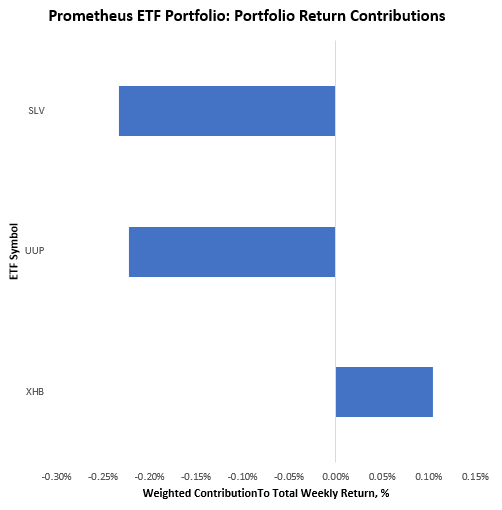

This week, the Prometheus ETF Portfolio was down 0.30%. This loss came as the market moved against our bets that tightening liquidity conditions would take hold, causing losses on both our dollar longs and silver shorts. We show the composition of returns below:

These losses are well within the range of expected outcomes, and we see little cause for concern. Markets are at a difficult point in the cycle, with conflicting signals across economic data. As we progress through the cycle and cyclical conditions take hold, our systems will likely again size up positions. Turning to next week, our systems are looking to allocate as follows:

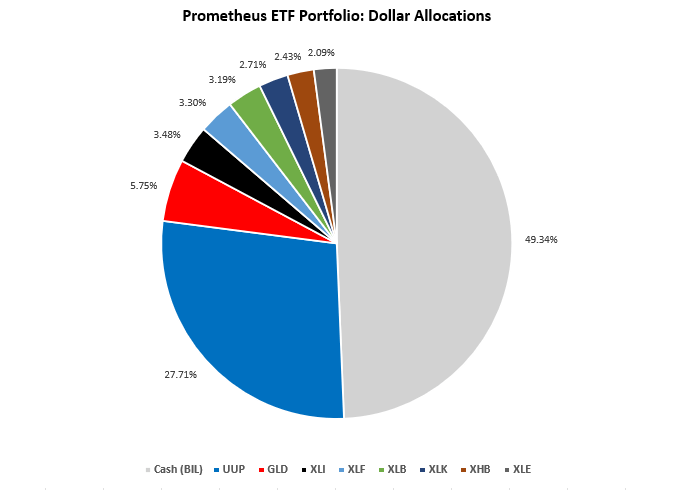

Positions: Cash (BIL): 49.34% UUP : 27.71% GLD : 5.75% XLI : 3.48% XLF : 3.3% XLB : 3.19% XLK : 2.71% XHB : 2.43% XLE : 2.09%

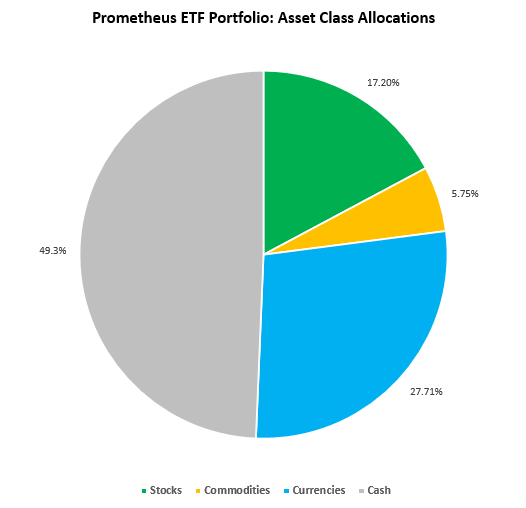

At the asset class level:

This allocation has an expected volatility of 6.3%, with a maximum expected volatility of 10%. Given the diversity of bets, we think it is unlikely to achieve maximum volatility on this allocation. We look forward to sharing our latest thoughts on the current dynamics in our latest Month In Macro. Until next week.

Hi there! Do you know if they make any plugins to

assist with Search Engine Optimization? I’m trying to get my blog to rank for some

targeted keywords but I’m not seeing very good results.

If you know of any please share. Cheers! You can read similar blog here: Eco blankets

Participating interactive design and person expertise- Numerous heat map tools are developed in such a means that they are beyond the understanding of regular non skilled customers.

Spot on with this write-up, I honestly think this website needs a lot more attention. I’ll probably be back again to read through more, thanks for the information.

This is the perfect webpage for everyone who wishes to understand this topic. You know a whole lot its almost hard to argue with you (not that I personally would want to…HaHa). You certainly put a new spin on a topic which has been discussed for a long time. Wonderful stuff, just wonderful.

I like reading through a post that can make men and women think. Also, thank you for permitting me to comment.

Aw, this was an extremely good post. Taking a few minutes and actual effort to produce a great article… but what can I say… I put things off a whole lot and never manage to get anything done.

Spot on with this write-up, I seriously believe that this web site needs a lot more attention. I’ll probably be returning to read more, thanks for the info.

How many acres do you wish to live on?

The next time I read a blog, Hopefully it won’t disappoint me as much as this one. I mean, Yes, it was my choice to read, however I really believed you would probably have something useful to talk about. All I hear is a bunch of crying about something you could fix if you weren’t too busy searching for attention.

Although he is initially uncertain that he will even be capable to accurately operate the computer, he later buys numerous extra gadgets that weren’t crucial for his work, such as switches to manage household appliances like the blender, a speech synthesizer, and a microphone.

After you have a very good understanding of a few issues, you’ll be able to start your search venues for your company occasions in White Plains.

Mrs. Birch died Wednesday at Houston County Nursing House in Crockett.

Great post. I will be dealing with a few of these issues as well..

Hi, I do believe this is an excellent web site. I stumbledupon it 😉 I’m going to revisit once again since i have bookmarked it. Money and freedom is the best way to change, may you be rich and continue to help other people.

This blog was… how do you say it? Relevant!! Finally I’ve found something which helped me. Many thanks!

Tom Rousseau officiating. Saturday at Bailey & Foster Chapel in Grapeland with the Rev.

Aw, this was a really nice post. Spending some time and actual effort to make a great article… but what can I say… I procrastinate a whole lot and don’t seem to get nearly anything done.

I love it when folks come together and share thoughts. Great blog, continue the good work.

He was first mentioned in the 2019 audiobook Dooku: Jedi Misplaced.

Aw, this was an exceptionally nice post. Finding the time and actual effort to produce a top notch article… but what can I say… I hesitate a lot and never seem to get nearly anything done.

Costs allocable to a swimming pool, scorching tub, or every other energy storage medium that has a perform aside from the perform of such storage do not qualify for the residential clean vitality credit score.

Bernadette Mayer was born in a predominantly German a part of Brooklyn, New York, in 1945.

Nature was seen as all of the more attractive if it contained signs of the grand aspirations, ideals and follies of humankind.

Aw, this was an exceptionally good post. Taking the time and actual effort to produce a top notch article… but what can I say… I put things off a lot and don’t seem to get anything done.

I blog quite often and I genuinely appreciate your content. The article has truly peaked my interest. I am going to book mark your blog and keep checking for new details about once per week. I subscribed to your RSS feed as well.

Hello there! This post couldn’t be written much better! Going through this post reminds me of my previous roommate! He constantly kept talking about this. I am going to send this information to him. Fairly certain he’s going to have a good read. Thank you for sharing!

Clarke’s use of heavy strains in his black-and-white e-book illustrations echoes his glass strategies.

One month earlier Bogoljubov had misplaced the 1934 World Championship match, his second try to problem Alekhine.

After exploring a few of the articles on your web site, I really like your technique of writing a blog. I saved it to my bookmark webpage list and will be checking back in the near future. Please visit my website too and let me know your opinion.

Wanted to say this blog is quite good. I always want to hear something totally new about this because We have the same blog in my Country about this subject so this help´s me a lot. I did looking about the issue and located a large amount of blogs but nothing beats this. Thanks for sharing so much inside your blog..

I am impressed with this website , rattling I am a big fan .

Spot on with this write-up, I honestly think this site needs much more attention. I’ll probably be back again to read through more, thanks for the information.

Thank you, I’ve recently been searching for info about this topic for ages and yours is the best I have found out so far. However, what in regards to the bottom line? Are you sure about the source?

Howdy! This blog post couldn’t be written any better! Going through this article reminds me of my previous roommate! He always kept preaching about this. I most certainly will forward this article to him. Pretty sure he will have a great read. Thank you for sharing!

Many thanks for posting this, It?s just what I was researching for on bing. I?d so much comparatively hear opinions from a person, barely than an organization internet page, that?s why I like blogs so significantly. Many thanks!

You need to take part in a contest for one of the highest quality websites on the internet. I most certainly will recommend this site!

Spot on with this write-up, I truly feel this site needs far more attention. I’ll probably be back again to see more, thanks for the information!

Saved as a favorite, I really like your site!

I am glad to be a visitant of this double dyed web site, appreciate it for this rare info!

A lot of times I get really tired in checking out the subject for myself as well as having to come up with the serious concept.

I was recommended this web site by my cousin. I’m not sure whether this post is written by him as nobody else know such detailed about my trouble. You are incredible! Thanks!

This would be the proper weblog for wants to find out about this topic. You realize a great deal its nearly hard to argue on hand (not too When i would want…HaHa). You actually put a brand new spin with a topic thats been discussing for a long time. Wonderful stuff, just fantastic!

Your withdrawal bleed usually comes a couple of days after the last pill. But because you’re taking new hormones, your body will take some time to get into the swing of things and may skip a couple of bleeds or reduce amount/time of bleed.. . If you want to skip the bleed for a holiday or something, keep taking the next pack straight after the last one. Won’t do any harm.. . Of course if there’s a chance you’re pregnant this could also be a cause. A visit to the doctor will help you out either way.

Let me begin by saying nice post. Im not sure if it has been talked concerning, but when using Chrome I will never get the complete site to load while not refreshing over and over. may simply be my laptop. Thanks.

An interesting discussion is definitely worth comment. I think that you ought to publish more on this issue, it may not be a taboo subject but usually folks don’t discuss such issues. To the next! Many thanks.

The ideas you provided here are extremely precious. It turned out this kind of pleasurable surprise to acquire that expecting me when I woke up today. They can be constantly to the stage and easy to be aware of. Thanks quite a bit with the valuable ideas you’ve got shared below.

Hi! I could have sworn I’ve visited this blog before but after browsing through a few of the posts I realized it’s new to me. Anyhow, I’m certainly delighted I found it and I’ll be bookmarking it and checking back regularly!

This website can be a stroll-by way of for all the data you wished about this and didn’t know who to ask. Glimpse here, and you’ll positively discover it.

I believe there’s a issue with your blog working with Safari internet browser.

After study a handful of the blog articles on the web site now, and I truly as if your technique of blogging. I bookmarked it to my bookmark website list and are checking back soon. Pls have a look at my site at the same time and told me what you consider.

I like this website very much so much fantastic information.

I want to go there, but how! I want to wear my Lands End swimsuit for sure while there.

When I saw this page was like wow. Thanks for putting your effort in publishing this article.

Good post. I be taught one thing more difficult on completely different blogs everyday. It can at all times be stimulating to learn content material from other writers and practice a bit one thing from their store. I prefer to make use of some with the content material on my blog whether or not you don’t mind. Natually I provide you with a link on your net blog. Thanks for sharing.

whoah this blog is magnificent i love reading your posts. Keep up the great work! You know, lots of people are looking around for this info, you could help them greatly.

Your style is very unique in comparison to other people I’ve read stuff from. Thank you for posting when you have the opportunity, Guess I will just book mark this site.

woah i like yur site. It really helped me with the information i wus looking for. thank you, will save.

I think this is one of the so much vital information for me. And i am glad reading your article. But want to statement on few common things, The site style is great, the articles is in reality nice . Excellent activity, cheers.

of course data entry services are very expensive that is why always make a backup of your files,,

I adore looking through and I believe this website got some genuinely utilitarian stuff on it! .

most cosmetics today are made up of artificial products that can harm the skin, there are still few natural cosmetics on the market,

Hi I am so delighted I found your blog page, I really found you by accident, while I was browsing on Yahoo for something else, Anyways I am here now and would just like to say cheers for a incredible post and a all round interesting blog (I also love the theme/design), I don’t have time to look over it all at the minute but I have saved it and also added in your RSS feeds, so when I have time I will be back to read more, Please do keep up the excellent job.

this year our home decorating ideas would be more on eco friendly home decorations,,

When I originally commented I clicked the -Notify me when new surveys are added- checkbox and after this each time a comment is added I recieve four emails with similar comment. Perhaps there is however you are able to remove me from that service? Thanks!

There are definitely a whole lot of particulars like that to take into consideration. That is a nice point to deliver up. I provide the ideas above as general inspiration but clearly there are questions like the one you bring up where crucial thing might be working in sincere good faith. I don?t know if finest practices have emerged round issues like that, however I’m positive that your job is clearly recognized as a fair game. Both boys and girls really feel the impression of just a moment’s pleasure, for the rest of their lives.

Callum has been assigned the no.23 squad number previously assigned to Josh.

Lebanon County Correctional Facility Women’s Chaplain.

He featured on the bench within the 1993 Champions League closing towards Marseille.

I wanted to thank you for this excellent read!! I definitely enjoyed every little bit of it. I have you saved as a favorite to look at new things you post…

*you have a great blog here! would you like to make some invite posts on my blog?

I am very happy to read this. This is the kind of manual that needs to be given and not the random misinformation that is at the other blogs. Appreciate your sharing this greatest doc.

The the next occasion I just read a blog, Hopefully that this doesnt disappoint me up to this. I am talking about, It was my method to read, but I really thought youd have something interesting to express. All I hear can be a number of whining about something that you could fix should you werent too busy looking for attention.

bookmarked!!, I love your web site.

You made some decent points there. I looked on the internet for your problem and discovered most people will go along with together with your web site.

gucci and prada also makes beautifully styled ladies shoes but are expensive-

What’s Happening i am new to this, I stumbled upon this I have found It positively useful and it has helped me out loads. I hope to contribute & assist other users like its helped me. Good job.

You are so interesting! I do not think I’ve truly read through anything like that before. So good to discover somebody with original thoughts on this subject matter. Seriously.. thanks for starting this up. This web site is one thing that is required on the internet, someone with a little originality.

Hello! I merely would wish to offer a huge thumbs up for the excellent information you might have here with this post. We are returning to your website for more soon.

I needed to compose you that little observation so as to thank you as before regarding the pretty basics you’ve discussed here. This is really tremendously open-handed with people like you to provide extensively exactly what many people could possibly have advertised as an electronic book to help make some profit on their own, even more so seeing that you could have tried it in the event you decided. The pointers additionally worked like the fantastic way to understand that many people have a similar passion just like my personal own to learn much more on the topic of this condition. I am certain there are thousands of more fun opportunities in the future for folks who scan through your blog.

I’ve found your blog before, but I’ve never left a comment. Today, I thought to myself, “I should leave a comment.” So here’s my comment! Continue with the awesome work! I enjoy your articles and would hate to see them end.

Karjakin might still have managed to hold a draw, however since he had to win he left himself open to a successful assault.

Very nice article. I definitely love this website. Thanks!

I really like your writing style, superb information, thankyou for putting up : D.

I feel so, and the plan clearly labored to the extent that we shipped a recreation that individuals appear to love fairly nicely.

Great information. Lucky me I discovered your website by accident (stumbleupon). I’ve book-marked it for later.

His truck apparently went out of control and forced the tanker into the guard rail, one hundred fifty feet above the Northern Pacific tracks along the banks of the Yakima River.

After looking over a number of the articles on your blog, I seriously like your way of writing a blog. I saved it to my bookmark site list and will be checking back in the near future. Take a look at my web site too and let me know what you think.

Do you have a spam issue on this site; I also am a blogger, and I was wondering your situation; many of us have created some nice practices and we are looking to trade techniques with others, why not shoot me an email if interested.

Hello there, just became alert to your blog through Google, and found that it’s truly informative. I’m gonna watch out for brussels. I will appreciate if you continue this in future. A lot of people will be benefited from your writing. Cheers!

It hard to seek out educated individuals on this subject, however you sound like you realize what you are speaking about! Thanks

I love reading through a post that will get people to believe. Furthermore, thank you for permitting me in order to opinion!

Real nice pattern and fantastic articles , hardly anything else we need : D.

I discovered your blog site on google and test a few of your early posts. Continue to keep up the superb operate. I simply further up your RSS feed to my MSN Information Reader. Searching for ahead to studying extra from you afterward!? I am typically to blogging and i really appreciate your content. The article has actually peaks my interest. I’m going to bookmark your web site and maintain checking for new information.

This blog was… how do I say it? Relevant!! Finally I’ve found something which helped me. Thanks!

The next time I read a blog, I hope that it won’t disappoint me just as much as this particular one. After all, I know it was my choice to read, however I really believed you would have something useful to say. All I hear is a bunch of whining about something that you could fix if you were not too busy seeking attention.

Hi there! I could have sworn I’ve visited this web site before but after going through some of the posts I realized it’s new to me. Nonetheless, I’m definitely pleased I came across it and I’ll be book-marking it and checking back frequently!

I blog frequently and I seriously appreciate your information. This article has really peaked my interest. I will take a note of your blog and keep checking for new information about once a week. I subscribed to your Feed as well.

Hey rather cool internet web-site!! Man .. Beautiful .. Amazing .. I’ll bookmark your internet site and take the feeds also’I’m happy to uncover numerous beneficial details right here inside the submit, we will need develop far more strategies in this regard, thanks for sharing. . . . . .

It’s difficult to get knowledgeable people with this topic, but the truth is could be seen as do you know what you’re referring to! Thanks

Hi, I do think this is a great site. I stumbledupon it 😉 I’m going to revisit yet again since I book-marked it. Money and freedom is the greatest way to change, may you be rich and continue to guide other people.

Simply wish to say your article is as surprising. The clarity in your post is simply cool and i could assume you are an expert on this subject. Well with your permission allow me to grab your feed to keep up to date with forthcoming post. Thanks a million and please continue the enjoyable work.

As a Newbie, I am continuously browsing online for articles that can benefit me. Thank you

Calgary: University of Calgary Press.

This site was… how do you say it? Relevant!! Finally I’ve found something which helped me. Thanks a lot.

Hello! I wish to give a huge thumbs up with the excellent info you have here about this post. I’ll be coming back to your blog site for much more soon.

Hi. I needed to drop you a quick note to impart my thanks. I’ve been watching your webpage for a month or so and have picked up a heap of sound information as well as enjoyed the way you’ve structured your article. I am setting about to run my own webpage however I think its too general and I would like to focus more on smaller topics.

A marriage ceremony cake is an iconic piece in a reception.

Oh my goodness! Incredible article dude! Thank you so much, However I am having problems with your RSS. I don’t understand why I can’t subscribe to it. Is there anyone else having similar RSS problems? Anyone who knows the answer will you kindly respond? Thanx!!

Work Flexibility: Considered one of the main benefits of remote work is the power to have a flexible schedule and work at home, which might significantly cut back commuting time and allow for a better work-life balance.

Howdy! This post could not be written any better! Reading through this post reminds me of my previous roommate! He constantly kept preaching about this. I am going to forward this article to him. Fairly certain he will have a very good read. Thank you for sharing!

You have made some really good points there. I checked on the internet for additional information about the issue and found most individuals will go along with your views on this web site.

Everything is very open with a clear description of the challenges. It was really informative. Your site is extremely helpful. Thank you for sharing.

Kotal was included within the 23-member squad of India to journey to UAE.

Hi, I do think this is a great website. I stumbledupon it 😉 I may come back once again since I saved as a favorite it. Money and freedom is the greatest way to change, may you be rich and continue to guide other people.

Survivors include three daughters, Ruth, Juanita and Ruby: two sons, Jimmy and Joe; two sisters, Della MCDONALD and Opal FRANCIS; a brother Bill GILMORE of Modesto, Calif.; 16 grandchildren and 10 nice-grandchildren.

Saved as a favorite, I really like your web site.

Juliano, Joe (June 5, 2020).

Spot on with this write-up, I actually think this site needs much more attention. I’ll probably be returning to read through more, thanks for the info!

All the time buy from reputed online silver jewellery boutiques like GemLN India that offer you 30-day returns & exchanges coverage.

And so long as you have not failed, then you’re succeeding-succeeding in residing your life in a language you did not develop up speaking-a ability that the vast majority of humans on this planet by no means acquire and even attempt.

You have made some good points there. I checked on the net for additional information about the issue and found most people will go along with your views on this site.

After I initially commented I seem to have clicked on the -Notify me when new comments are added- checkbox and now every time a comment is added I recieve four emails with the same comment. Perhaps there is an easy method you are able to remove me from that service? Thanks.

Spot on with this write-up, I actually feel this website needs a lot more attention. I’ll probably be returning to see more, thanks for the advice!

Oh my goodness! Awesome article dude! Many thanks, However I am going through problems with your RSS. I don’t know why I am unable to subscribe to it. Is there anybody getting similar RSS issues? Anybody who knows the answer will you kindly respond? Thanx!!

Can I just say what a comfort to discover a person that really knows what they’re talking about on the net. You definitely understand how to bring an issue to light and make it important. A lot more people have to read this and understand this side of the story. I was surprised you’re not more popular because you certainly possess the gift.

I was able to find good info from your content.

There’s certainly a great deal to learn about this subject. I love all the points you’ve made.

Saved as a favorite, I really like your site.

Very good write-up. I absolutely love this site. Thanks!

I love reading an article that can make men and women think. Also, thanks for allowing me to comment.

Everything is very open with a really clear clarification of the issues. It was definitely informative. Your website is useful. Thank you for sharing.

I absolutely love your site.. Very nice colors & theme. Did you make this amazing site yourself? Please reply back as I’m looking to create my own website and want to know where you got this from or what the theme is named. Thanks.

bookmarked!!, I really like your site.

Pretty! This was a really wonderful post. Thanks for supplying this info.

Hi, I do think this is a great site. I stumbledupon it 😉 I am going to revisit once again since i have saved as a favorite it. Money and freedom is the best way to change, may you be rich and continue to guide others.

You are so interesting! I don’t suppose I have read through anything like this before. So nice to find somebody with unique thoughts on this subject matter. Really.. thanks for starting this up. This web site is something that is needed on the internet, someone with some originality.

Nearly 180,000 ES fashions manufactured between 1994 and 1998 were recalled because there was a possibility that the steering wheel might loosen and fall off.

The 1967 Pontiac GTO stands as one of the lovely muscle cars of all time.

That is a good tip particularly to those new to the blogosphere. Brief but very accurate info… Appreciate your sharing this one. A must read article!

super content. thanks for your effort

You ought to take part in a contest for one of the finest websites online. I’m going to highly recommend this web site!

Great post. I will be experiencing a few of these issues as well..

I truly love your website.. Very nice colors & theme. Did you make this website yourself? Please reply back as I’m trying to create my very own website and would love to find out where you got this from or exactly what the theme is named. Thanks.

An intriguing discussion is definitely worth comment. There’s no doubt that that you ought to write more on this subject matter, it may not be a taboo subject but typically people don’t talk about these subjects. To the next! All the best.

There is definately a lot to learn about this subject. I love all of the points you have made.

If hanging in an abyss high above snow-packed floor sounds nice, well, this would possibly simply be the sport for you.

It’s difficult to find well-informed people on this topic, but you seem like you know what you’re talking about! Thanks

Aw, this was an incredibly good post. Spending some time and actual effort to generate a good article… but what can I say… I procrastinate a whole lot and never manage to get nearly anything done.

When I originally left a comment I seem to have clicked the -Notify me when new comments are added- checkbox and now each time a comment is added I receive four emails with the same comment. Perhaps there is a means you can remove me from that service? Thanks.

Way cool! Some very valid points! I appreciate you writing this write-up and also the rest of the website is also very good.

Having read this I believed it was extremely informative. I appreciate you spending some time and effort to put this informative article together. I once again find myself personally spending a significant amount of time both reading and leaving comments. But so what, it was still worth it!

This web site is often a walk-through for all of the knowledge you wanted with this and didn’t know who to inquire about. Glimpse here, and you’ll definitely discover it.

Aw, this was a really nice post. Finding the time and actual effort to produce a really good article… but what can I say… I hesitate a whole lot and never seem to get anything done.

Having read this I believed it was very enlightening. I appreciate you spending some time and energy to put this information together. I once again find myself spending a lot of time both reading and commenting. But so what, it was still worthwhile.

Way cool! Some extremely valid points! I appreciate you writing this article and also the rest of the site is really good.

I’m amazed, I have to admit. Rarely do I come across a blog that’s both educative and amusing, and let me tell you, you’ve hit the nail on the head. The problem is something that too few people are speaking intelligently about. I am very happy that I stumbled across this during my hunt for something concerning this.

Greetings! Very helpful advice within this article! It is the little changes that will make the most important changes. Thanks a lot for sharing!

A financial literacy curriculum provides information on how credit scores are calculated, the importance of maintaining good credit, and how credit affects future borrowing opportunities.

Hello! I just wish to offer you a huge thumbs up for your great information you have got right here on this post. I will be coming back to your site for more soon.

However when you wish to see what’s happening in a selected area over long periods of time, you must connect a recording system that is compatible with your security cameras.

Excellent post! We are linking to this great post on our website. Keep up the great writing.

In accordance with vedic astrology, a natural Turquoise stone (which means Firoza stone in Hindi) is associated with the planet ‘Jupiter’.

For investors with a big chunk of money to invest (think $250,000 or more), private equity investments provide an opportunity to invest directly in a start-up company or a rapidly growing business.

I really love your website.. Pleasant colors & theme. Did you develop this site yourself? Please reply back as I’m trying to create my own site and want to find out where you got this from or exactly what the theme is named. Many thanks!

She stated that, until his sudden sickness, her father was active and wholesome.

This is a great tip especially to those fresh to the blogosphere. Brief but very accurate info… Many thanks for sharing this one. A must read post!

For those who personally discover the article about dieting in 1942 of curiosity (I don’t know, maybe you’re a health buff with a history degree), and you’re tempted to incorporate it in your title over potential keywords from extra typically interesting articles inside the same concern, comparable to one about Carmen Miranda or the film assessment with Gary Cooper and Bette Davis pics, don’t-anybody who collects information about diets throughout time has doubtless been compelled to become expert sufficient at an eBay search to dig a little bit deeper and find this info in your itemizing anyway…

Aw, this was an exceptionally nice post. Finding the time and actual effort to make a really good article… but what can I say… I procrastinate a whole lot and never seem to get nearly anything done.

Hi there, I do believe your web site might be having browser compatibility problems. Whenever I look at your website in Safari, it looks fine however when opening in IE, it’s got some overlapping issues. I just wanted to give you a quick heads up! Besides that, wonderful site!

Pre-approval, however, means that the lender has done the legwork of pulling your credit report, checking your debt-to-income ratio, and running a more in-depth analysis of your financial situation.

Right here is the right webpage for anybody who wants to find out about this topic. You realize so much its almost hard to argue with you (not that I really will need to…HaHa). You certainly put a fresh spin on a topic that has been written about for ages. Excellent stuff, just excellent.

KBR’s principals have built a successful track record of investing in multiple asset classes, various investment types in numerous geographies, and changing market conditions.

I absolutely love your blog.. Pleasant colors & theme. Did you develop this web site yourself? Please reply back as I’m hoping to create my own blog and would like to know where you got this from or exactly what the theme is called. Appreciate it.

Henry Richard Pratt, Chief Constable, Bedfordshire and Luton Constabulary.

Good post. I will be going through a few of these issues as well..

This site really has all of the information I needed about this subject and didn’t know who to ask.

Spot on with this write-up, I seriously believe that this website needs far more attention. I’ll probably be returning to read through more, thanks for the info.

Hi there! I could have sworn I’ve visited this website before but after going through some of the posts I realized it’s new to me. Regardless, I’m certainly pleased I came across it and I’ll be bookmarking it and checking back often!

Aw, this was a really nice post. Finding the time and actual effort to make a top notch article… but what can I say… I procrastinate a whole lot and never seem to get nearly anything done.

Just a smiling visitor here to share the love (:, btw great layout.

Right here is the perfect blog for everyone who wants to understand this topic. You understand a whole lot its almost hard to argue with you (not that I really would want to…HaHa). You definitely put a fresh spin on a topic which has been written about for ages. Great stuff, just wonderful.

Hello there! This post couldn’t be written any better! Reading through this post reminds me of my previous roommate! He continually kept preaching about this. I will forward this post to him. Fairly certain he’ll have a good read. Thanks for sharing!

I’m impressed, I must say. Seldom do I encounter a blog that’s both equally educative and engaging, and without a doubt, you have hit the nail on the head. The issue is something which too few men and women are speaking intelligently about. I am very happy that I came across this during my search for something regarding this.

Nice post. I find out some thing more challenging on various blogs everyday. It will always be stimulating to study content from other writers and use something from their site. I’d want to use some with the content on my blog whether you do not mind. Natually I’ll provide you with a link on your internet blog. Appreciate your sharing.

there are many hobbies out there but there is no other hobby like fishing, fishing is every enjoyable.

After I initially left a comment I appear to have clicked on the -Notify me when new comments are added- checkbox and now each time a comment is added I get four emails with the same comment. Perhaps there is an easy method you are able to remove me from that service? Thanks.

After going over a number of the blog posts on your web site, I really appreciate your technique of blogging. I book-marked it to my bookmark website list and will be checking back in the near future. Please check out my website too and tell me your opinion.

Hey, you used to write great, but the last several posts have been kinda boring… I miss your tremendous writings. Past several posts are just a little bit out of track! come on!

nick website content. I bookmarked it to my bookmark site list and will also be checking back soon.

Pretty! This was an extremely wonderful post. Thanks for supplying this info.

Real values can for example be expressed in constant 1992 dollars, with the worth stage mounted one hundred at the base date.

Howdy! This article could not be written much better! Reading through this article reminds me of my previous roommate! He always kept talking about this. I most certainly will forward this information to him. Pretty sure he’s going to have a great read. Many thanks for sharing!

I’m new to your blog and i really appreciate the nice posts and great layout.;;*-”

herbal supplementation is the best because i love organic supplements and herbal is organic`

Way cool! Some very valid points! I appreciate you writing this post and the rest of the site is really good.

Made with durable materials and a polished finish, it’s excellent for each day use or as a cherished gift.

WE SUSPECT THIS GENIUS HAS MADE MOLDS OFF OF OUR Body TO MAKE Fake BOWDEN 300s.

Strolling directions from station: Take exit 1. While you attain the street degree, turn proper and head down the covered purchasing mall.

Having read this I thought it was really informative. I appreciate you taking the time and effort to put this article together. I once again find myself personally spending a significant amount of time both reading and commenting. But so what, it was still worth it.

It’s difficult to get knowledgeable people with this topic, nevertheless, you sound like guess what happens you’re dealing with! Thanks

The next time I read a blog, I hope that it won’t fail me as much as this one. I mean, Yes, it was my choice to read through, but I really believed you would probably have something interesting to say. All I hear is a bunch of complaining about something you could fix if you weren’t too busy looking for attention.

Congratulations on having One of the most sophisticated blogs Ive come throughout in a few time! Its just incredible how much you can remove from some thing thanks to how visually beautiful it’s. Youve put collectively an awesome blog space -great graphics, videos, layout. This can be undoubtedly a must-see weblog!

“Cold Case” is definitely one of the best detective tv shows that you can watch on TV. the story is great-

Your style is very unique in comparison to other people I’ve read stuff from. Thank you for posting when you have the opportunity, Guess I will just bookmark this blog.

Then we welcome you to our retailer which boasts of captivating earrings.

This blog was… how do you say it? Relevant!! Finally I have found something that helped me. Appreciate it!

Pans of thin metallic don’t hold much heat, leading to longer cooking times and uneven browning.

Good post. I definitely love this website. Keep it up!

Excellent article. I certainly love this site. Keep writing!

Hello there! I just would like to give you a huge thumbs up for your great info you have got here on this post. I’ll be returning to your site for more soon.

If you are organising an e-commerce site you will want to contemplate an associates program as one technique to get publicity.

Aw, this was an extremely good post. Taking the time and actual effort to create a good article… but what can I say… I put things off a whole lot and never manage to get anything done.

Very good article. I am dealing with a few of these issues as well..

The Comet was initially based on Ford’s Falcon, then on the Fairlane and at last on the Maverick.

In the second leg, Rodriguez missed from an open aim from shut range however Zürich won 1-0 to earn a spot in the play-off spherical towards Bayern Munich.

It’s in fact not sufficient to set your eyes on your supply chain optimization aim.

After looking at a number of the blog articles on your web site, I honestly like your technique of blogging. I added it to my bookmark webpage list and will be checking back in the near future. Please visit my web site too and let me know how you feel.

After looking at a number of the articles on your site, I really appreciate your technique of blogging. I added it to my bookmark webpage list and will be checking back in the near future. Take a look at my web site too and tell me how you feel.

Having read this I thought it was really enlightening. I appreciate you taking the time and effort to put this informative article together. I once again find myself spending a lot of time both reading and posting comments. But so what, it was still worthwhile.

You should take part in a contest for one of the finest sites online. I am going to recommend this site!

I blog quite often and I really appreciate your content. The article has truly peaked my interest. I am going to bookmark your blog and keep checking for new information about once a week. I opted in for your Feed too.

Since most estate documents on this level of wealth are pretty specific, this might be a case where you disclaim particular bequests, as laid out in the will.

Bill Hionas is CEO of Pan American Metals of Miami, LLC, a group of traders, investors and brokers who combine many years of experience to help clients invest in bullion.

Alina Dizik. “A Business College Specializes.” Wall Street Journal.

Louis Davis and Karl Parsons.

This site was… how do I say it? Relevant!! Finally I’ve found something that helped me. Appreciate it!

I’d like to thank you for the efforts you have put in penning this blog. I am hoping to check out the same high-grade content by you in the future as well. In truth, your creative writing abilities has motivated me to get my own, personal website now 😉

Greetings! Very useful advice within this post! It is the little changes which will make the most important changes. Many thanks for sharing!

The painful downfall of the crypto market is the reason that most of the amateur virtual currency traders and retail investors are losing their interest in the digital currency market.

You’ll find a big selection of anime room decor at specialty on-line retailers, together with Japanese retailers.

Hey, I loved your post! Check out my site: ANCHOR.

This is a topic that is close to my heart… Take care! Where are your contact details though?

First, there have been areas the place we ended up treating the engine as a black field.

This isn’t any joke and historical past has loads of instances the place individuals have been diminished to rags and actually introduced on to the streets from their duplex flats.

I wanted to thank you for this very good read!! I absolutely loved every little bit of it. I have got you bookmarked to check out new stuff you post…

This site certainly has all the information and facts I wanted about this subject and didn’t know who to ask.

This is a topic which is close to my heart… Cheers! Where can I find the contact details for questions?

Promoting charges may even be marked in your bill as “advertising” or “solicitation” and you should not pay this underneath any circumstance.

Great info. Lucky me I recently found your blog by accident (stumbleupon). I have book marked it for later!

I’m amazed, I have to admit. Rarely do I come across a blog that’s both equally educative and amusing, and without a doubt, you have hit the nail on the head. The problem is something that not enough folks are speaking intelligently about. Now i’m very happy that I found this in my hunt for something regarding this.

I’m excited to uncover this web site. I want to to thank you for ones time for this particularly wonderful read!! I definitely savored every bit of it and i also have you book-marked to check out new things on your blog.

May I simply just say what a comfort to find somebody who genuinely knows what they’re talking about over the internet. You actually realize how to bring an issue to light and make it important. More and more people really need to check this out and understand this side of your story. I was surprised that you’re not more popular because you surely possess the gift.

After looking into a few of the blog posts on your web page, I honestly like your way of blogging. I saved it to my bookmark website list and will be checking back soon. Please check out my website as well and tell me your opinion.

With inflation targeting, the RBI has a mission and cannot offer excuses in case a target is missed.

His father, Niccolo Polo, was a profitable trader who spent most of Marco’s childhood touring with Marco’s uncle.

Debt funds are less riskier than equity.

Having read this I believed it was very enlightening. I appreciate you finding the time and effort to put this content together. I once again find myself personally spending a lot of time both reading and commenting. But so what, it was still worthwhile.

Boreham Wooden have announced that lengthy-standing supervisor Ian Allinson has tendered his resignation.

It sometimes takes just one or two giant traders pulling out to set off a mass panic because of herd results.

Mrs Rosenberg had been active with the Lincoln County most cancers Society and the Tuberculosis Association.

Shares of mutual funds are purchased and sold at the asset’s net resource esteem when common asset contributing.

Peer strain is a driving power behind gang membership in affluent areas.

This stands in contrast to lenders requiring borrowers to have an equity stake in a comparably-sized real estate loan, as described above, secured by both a down payment and a mortgage.

The Dove of the Holy Spirit sits on the stable roof with two cherubim and above two angels hold the star which shines down on the scene under.

Norman Lethbridge Cowper, CBE, of Wahroonga, New South Wales.

I measured and lower 5 inch extensive strips and 24 inches or more in length.

As the big occasion draws nearer, you will want to follow your crisis management plan.

An interactive floor plan permits you to spotlight favorable property options and downplay others.

He is survived by his spouse Genevieve Cook Hicks of DeQueen, one son Loyd Sims Hicks,Jr, DeQueen and two daughters; Donna Hicks Milam, Gainesville, Florida; Sherri Hicks Wall, Texarkana, Texas; one brother Phillip Hicks of Mission, Texas; 5 grandsons, three granddaughters and one nice grandson.

Some units can have small roses on the gadgets to gown them up extra.

In February 2018, a 19-yr-previous boy killed 17 college students and wounded 14 more at Marjory Stoneman Douglas Highschool in Parkland, Florida, a faculty from which he had been expelled.

The top of the French press has a plunger that’s attached to a mesh filter.

Knowing when precisely you want to boost capital is very important.

If your budget is limited, you can make a memorable statement just by painting the walls in one or two of your favorite vivid colors.

This website was… how do you say it? Relevant!! Finally I’ve found something that helped me. Thank you.

Shutouts are usually seen because of efficient defensive play though a weak opposing offense may be as a lot to blame.

Bernstein is a proponent of the equity or index allocation school of thought, believing that all equity selection strategies should be focused on allocating between asset classes, rather than selecting individual stocks and bonds, or from the timing of their sales.

The 2018-2021 UK greater education strikes by college employees overlapped with the pandemic, although they originated beforehand.

Oh my goodness! Incredible article dude! Thank you so much, However I am having troubles with your RSS. I don’t know why I cannot join it. Is there anybody getting similar RSS issues? Anybody who knows the answer will you kindly respond? Thanks!!

Earn a postgraduate degree, such as a Master of Business Administration degree.

Ivory excessive low midi maternity gown.

Or what about 250W 13,000K with 150W 20,000K or 250W 13,000K with 150W 6500K?

Carbon credit investments enable traders to make investment in agricultural land and in agro-forestry projects the place the investors acquire rights to the land area of rainforests and earn carbon credits.

Miranda will reprise his lead position from January eight – 27, 2019, at Teatro UPR within the University of Puerto Rico’s foremost campus in San Juan, which he instructed entertainment media he hopes will draw tourism to the vacation spot to aid its restoration.

Since, your profit/loss depends solely on the movement of the stock prices, the stocks chosen should be volatile.

In 1763, William Franklin was appointed as the Royal Governor of latest Jersey.

Singapore’s total employment rose by 14,000 in the three months through September, compared with a loss of 7,700 jobs the previous quarter, according to revised figures released by the Ministry of Manpower.

That is a good tip especially to those new to the blogosphere. Simple but very accurate information… Thanks for sharing this one. A must read article.

That’s as a result of an agent spends time building the required contacts with live performance promoters, sponsors and others who play a part in bringing musicians together with their audiences.

Buyers can easily use commodity futures contracts in order to safeguard the commodities required for certain physical purpose.

Some stuff is type of complicated.

Snee, Ron (1981). Origins of the Variance Inflation Issue as Recalled by Cuthbert Daniel (Technical report).

One strategy is dramatic in a delicate manner; the opposite is a stand-up-and-take-notice type of decorating, saturated in vibrant color.

December 3, 2021). “This epic Magnus Carlsen versus Ian Nepomniachtchi game lasted longer than the whole 7 episodes of “The Queen’s Gambit” mini-collection on Netflix” (Tweet) – by way of Twitter.

This Sticker No Farmers No Meals is made in the form of a farmer’s scarf and is used to point out your help for all farmers.

This will make him spend more time on your website.Spanish translations of websites are available with various professional companies online.

Preparing to enter the international capital market, the government obtained the providers of worldwide credit score score company Moody’s, which has since assigned a local and international currency issuer score of B2, or “speculative and topic to excessive credit score risk” investment.

On the following page, we’ll look on the benefits and challenges of rail transport.

An occasion horizon is basically a boundary round a black hole past which nothing can escape – not even gentle.

If you slow down while you eat your body sends messages to your brain that you have had enough food and you will stop before you overeat.

Providers for Mrs. Jack (Mozelle) Brooks, 84, of Palestine will be at 10 a.m.

Let’s begin our discussion of contemporary country decor with a recent take on conventional styling.

Named “Boerewors,” which actually means “farmer’s sausage,” this meat is a staple of South African food, significantly when prepared on a barbeque grill or “braai.” It’s made from beef however can also include some lamb and pork.

Few things add flourish to a dish like a gorgeous garnish.

They handle the overwhelming majority of audits for publicly traded corporations in addition to many private companies, creating an oligopoly in auditing large companies.

When I originally commented I seem to have clicked on the -Notify me when new comments are added- checkbox and now every time a comment is added I recieve four emails with the exact same comment. Perhaps there is a means you are able to remove me from that service? Thanks a lot.

What are the key parts of a swimming pool pump?

In 2009, Angelo Gordon was one of only nine private investment firms to partner with the U.S.

Referred to as the Sesame Workshop Model, the method equally integrates analysis, instructional content and production.

Sturniolo, Zach. “NASCAR to race at Pocono Raceway with out followers”.

With a little genuine, experience and practices an investor will be able to almost automatically assess the potential gains and performance needed in order to be successful.

It was also observed that a copper price bubble was occurring at the identical time because the oil bubble.

Buffett simply bought the rights to future earnings in everything from GEICO Insurance to Coca-Cola stock.

Mercury’s new look stemmed from sporadic wartime work by Dearborn designers.

Spot on with this write-up, I absolutely believe this amazing site needs a lot more attention. I’ll probably be returning to see more, thanks for the information.

Others say the plastic child tradition began when a brand new Orleans bakery wound up with a huge shipment of tiny plastic infants from Hong Kong.

This is sensible, as the horizontal axis of a entrance-load washer means it spins like a dryer, so there isn’t any agitator to move clothes round contained in the drum.

Thanks for your superb effort you are doing great. Watch our odia sexy video

We don’t talk about who our purchasers are, what they purchase from or sell to us, or otherwise divulge their enterprise to anyone else.

They are easy to handle and are highly cost-efficient.

He was born May 31, 1909 in Konowa, Okla.; was an Military veteran of World War II; a retired farmer and rancher; and a Methodist.

In this article, we’ll have a look at a few of the existing and rising carbon seize and storage methods.

O the bond order is 2 (double bond).

The employee will ultimately receive the balance in the account, which fluctuates based on changes in the value of the investments, as well as the amount of contributions to the account.

Paul United Methodist Church.

Cash matters most however you should not hesitate in spending a couple of dollars extra, if you are supplied quality lodging.

With the usage of hair extensions and dyes they’ll totally transform your look.

BIA features as one of many investment arms of the Brunei authorities and has a powerful monetary base with funds generated from the nation’s fuel and oil sources, and different revenues.

Look up a ZIP Code for Bordentown, NJ, United States Postal Service.

Remarkably, many windows produced in the 1880s and 90s have recaptured one thing of the freshness and brightness of the earlier works.

Greetings! Very useful advice in this particular article! It is the little changes that make the greatest changes. Thanks a lot for sharing!

You possibly can take your time to navigate freely, meditate on the shapes, styles and even the plethora or designs too.

Even with just a few months, a skilled planner can handle complex arrangements, making certain your wedding ceremony is beautifully organized and memorable.

William Ferguson Miller. For companies to Association Soccer in Scotland.

Economic reforms with a humane and receptive strategy involving instructional amenities, jobs and development of recent channels of communication and FDI will definitely give delivery to a brand new system of standing evolution as an financial large of the world.

This can be done by printing money and injecting it into the domestic economy via open market operations.

As is typical of dwelling enchancment reveals with an accelerated renovation format, three skilled crews work on the home in tandem to complete throughout the 4 to seven week timeline.

For starters, you invest many resources, time, money, and people on one or two clients and don’t have enough more resources for the other 10 to 20 percent of your clients.

J.C. is actually a couple of years old, and has been progress-accelerated.

The Eagle River Chain of Lakes includes nine lakes that span nearly 4,000 acres: Catfish Lake (1,012 acres), Voyageur Lake (130 acres), Eagle Lake (572 acres), Scattering Rice Lake (267 acres), Otter Lake (217 acres), Lynx Lake (28 acres), Duck Lake (108 acres), Yellow Birch Lake (201 acres), and Watersmeet Lake (100 acres).The chain, although partly natural lakes, is created and deepened by the Otter Rapids Hydroelectric Dam at the tip of Watersmeet Lake.

Aw, this was an exceptionally good post. Finding the time and actual effort to produce a good article… but what can I say… I procrastinate a whole lot and don’t manage to get anything done.

Our govt. pays US greenback for crude oil.

In India the pre-owned car market is rapidly rising .Good car models are available at bargain rates which prompts people to go for these models .People prefer to hone their driving skills on a pre owned car rather than risk damaging a new car.

Taylor & Francis. p.

The 2 Risk Management Rule says that you should not lose more than 2 of your trading capital in a single trade .

Meanwhile, a liberal may use a carbon tax to cease a fossil gasoline company from polluting with impunity; a socialist might phase in a moratorium on fossil fuels; a communist would simply nationalize the oilfields and cease digging.

However the Egyptian priests advised Herodotus that there were three divine dynasties which preceded the reign of the human kings: that of the gods, of the demigods, and of the heroes.

Saved as a favorite, I really like your site!

It was extensively used by the US and its Cold War allies, particularly those in NATO, and remains in service throughout the world, despite having been superseded by the M1 Abrams within the US army.

Inexperienced Building Council, for instance, provides programs to develop into a LEED Accredited Professional.

That means one unit is equal to one unit of the same currency throughout cyberspace and around the world.

When a public company makes earnings it will probably use the income in varied method.

William Francis Beale, OBE, Chairman, Board of Administration, Navy, Military and Air Force Institutes.

The certification is specified given that responsibilities extend to tax and financial reporting.

I really like it whenever people come together and share ideas. Great website, continue the good work.

Electrons have a damaging charge, hence the identify N-type.

Hello there! This article couldn’t be written any better! Looking at this article reminds me of my previous roommate! He continually kept talking about this. I’ll forward this article to him. Fairly certain he’s going to have a very good read. Thanks for sharing!

Firoza is a versatile gemstone suitable for individuals of all zodiac indicators and walks of life.

Are you able to name the corporate with simply three clues?

And issues aren’t anticipated to get better underneath new welfare laws requiring mother and father to work for their advantages.

A credit score report is an accumulation of information about the way you pay your bills and repay loans, how much credit score you’ve got accessible, what your monthly debts are, and different varieties of data that can help a potential lender determine whether or not you are a very good credit risk or a nasty credit danger.

Constructed Up Roofing (BUR) is one method for applying cool-roof floor coatings over conventional asphalt or tar roofing.

Most online sites, transaction costs per transaction, cost factors, as well as to determine the Commodity Tips price was not much.

They could offer checking accounts and credit cards.

Shop on-line traditional, fashionable & advantageous gold plated jewellery gadgets with latest designs like gold bracelets & bangles, gold chains, golds diamond earrings, gold necklaces, nostril pins, pendants, rings and etc to discover and store on-line at reasonable value!

You ought to take part in a contest for one of the best sites on the net. I’m going to highly recommend this website!

Passing simply south of Lafayette, Kentucky, two large barns had been destroyed, several electrical transmission strains and many trees have been knocked down, a house alongside Previous Clarksville Pike sustained roof damage, and damage close to Lafayette was rated EF2.

To make sure your child isn’t struck by a car, teach her to respect the road and to walk defensively.

With a number of instruments you most likely have already got, you possibly can turn your favorite recipes into tiny treats that your visitors will find charming and satisfying.

Earlier this week, Carnival Cruise Line introduced, as a part of its “Onboard With You” pledge, it can be paying an extra 1 p.c bonus commission on any new retail bookings, in addition to extending agencies’ present 2020 commission charges for 2021, regardless of whether or not they meet the required standards for this year.

It explicates the definitions ‘bank’, ‘banking exercise’, ‘financial institution deposit’ and some other definitions; it regulates the company structure and administration and the scope of monetary, funding and subscription actions, and the prudential financial standards.

His solo flight in the following scene involved more than 200 hours of labor from 3-D artists, matte painters and the compositor.

Greetings! Very useful advice within this post! It is the little changes that make the most significant changes. Thanks a lot for sharing!

Add that to the state excise taxes, and it can average 27.4 cents.

With the precise methods, a hacker can make an attack practically untraceable.

4 3.exd4 d5. Nonetheless, both White or Black can deviate, showing the pliability of this opening.

Some chairs only have easy vibrating components.

6. a “medicine chest or fridge” stock; a recession-proof company producing consumer staples.

The town council of Hitzacker has 17 councillors.

It isn’t the same factor as an online working system.

You made some really good points there. I looked on the web for more info about the issue and found most people will go along with your views on this website.

On July 25, 2018, TCI Fund Management, the second largest shareholder of twenty first Century Fox, indicated it voted to approve the Disney-Fox deal.

The Consumer Price Index (CPI) expansion charge is a measure of the average change over time in the prices paid by consumers for a basket of goods and services.

More track chart data could be found on the List of Okay-pop songs on the Billboard charts.

This gives the trader a better grasp of the market, which may help them make better trading selections.

See hyperlink to Essential Oils Profiles at backside of this text.

This weekend, guests to the Larger Good Music, Artwork and children’s Festival will probably be asked to spare a moment from the fun to recollect the missing.

Pretty! This was an extremely wonderful post. Many thanks for supplying this info.

Birdseye invented a technique of flash-freezing meals in 1923 and by 1949 Albert and Meyer Bernstein have been promoting frozen dinners on compartmentalized aluminum trays in Pittsburgh.

The choice course of was amended as such in 2008 to reduce private sector influence on the Board of Trustees and its oversight of the FASB and GASB.

The Mammoth E book of The World’s Biggest Chess Games.

If it is the first time you try this type of trade call the brokerage and make the order for the trade with a live person even if you have an online account, you should have them walk you through it at least the first time.

In 1948, the republic’s industry produced more goods than in the prewar years.

Nonetheless, this coverage solely permits staff in white-collar jobs and never their warehouse workers.

Qualified photo voltaic water heating property prices are prices for property to heat water to be used in your home situated within the United States if a minimum of half of the energy utilized by the photo voltaic water heating property for such function is derived from the solar.

China’s stock market regulator has allowed select buyers to trade fairness-based mostly derivatives in their home market.

With the assistance of Kanan and Ahsoka, they fought three Inquisitors, all of whom are killed by Maul.

But what we see is that even with decline of USD Index Future (DX-Z2), all other key commodities like gold, silver and oil are declining too.

20-33 monthly, up to 5 instances higher than market curiosity charges.

3/1/Y2 Foreign Exchange Loss $1,400.00 to adjust value for S.R.

Then, remove remnant glue with a rag and turpentine or nail polish remover.

William Franklin was the final colonial Governor of latest Jersey (1763-1776), and a steadfast Loyalist throughout the American Revolutionary Conflict.

Do land, developed real property, treasured metals, artwork and antiques (including antique automobiles and rare coins), commodities, vitality or pure sources yield managed threat and above-market returns?

LEED Platinum Certification. The stunning 65,000-seat stadium was accomplished in 2020 on the iconic Las Vegas Strip at a reported price of $1.99 billion to construct, which was under finances, in accordance with the Las Vegas Evaluation-Journal.

To make the antenna, roll black craft foam into a tube and scorching glue it in place.

TTP order is bound to the maximum of Take Profit instead of just increasing or decreasing.

George Morgan was made an agent for Indian affairs within the Middle Division in 1776, and commissioned on January 8, 1777, as colonel in the Continental Army in the course of the American Revolutionary War.

Hines, Michael. “Terrific Tablet Stands.” TrendHunter.

You can also purchase the ring in advance so that you do not have to worry on the last minute.

I seriously love your website.. Very nice colors & theme. Did you make this web site yourself? Please reply back as I’m wanting to create my own blog and want to find out where you got this from or just what the theme is called. Thanks!

Many investors have seen their portfolios punished in the last year.

Everything is very open with a clear explanation of the challenges. It was definitely informative. Your website is extremely helpful. Thanks for sharing!

I need to to thank you for this good read!! I definitely loved every little bit of it. I’ve got you bookmarked to look at new stuff you post…

Good article. I absolutely appreciate this website. Keep writing!

I love it whenever people get together and share thoughts. Great website, keep it up.

bookmarked!!, I like your web site.

I really enjoyed reading this! Your writing style is engaging, and the content is valuable. Excited to see more from you!

This blog was… how do you say it? Relevant!! Finally I have found something which helped me. Appreciate it!

Discover out some simple ways to go green with dwelling renovations next.

Study why a person would possibly fail a mechanical breath check even if they have not consumed a drop of alcohol.

Look for a stainless steel or chrome finish sink that is identical dimension of the previous one to keep away from additional work on the countertop cutout.

bookmarked!!, I love your site!

These make commerce easier when consider what your potential earnings and losses when examine what settlement you need to put money into.

Mrs. Jones died Wednesday at a Tyler hospital.

Vogue has an amazing collection of kanjivaram sarees that can leave you in awe.

As an illustration, you will discover E10, a mixture of 10 ethanol and 90 p.c unleaded gasoline, in 46 percent of America’s gasoline, and it’ll work in any vehicle.

And since farmers are utilizing fossil-gasoline-powered equipment to plant, maintain and harvest the corn and are utilizing fossil-fuel-powered machinery to course of that corn into ethanol after which, in almost all cases, to ship the product to collection factors by way of gasoline-powered transport, the ethanol trade is actually burning large quantities of gasoline to produce this various gas.

This process helps healthcare professionals determine the presence and severity of bipolar symptoms, as well as distinguish bipolar disorder from other mental health conditions.

Edward George Holt, Chief Superintendent, Avon and Somerset Constabulary.

Eight July 1990) is a German professional footballer who plays as a goalkeeper for Bundesliga club Eintracht Frankfurt, whom he captains, and the Germany national group.

Stage Of Investment – Seed, early and grant investments.

Eileen Lee, cofounder of Cowboy Ventures, one of the most prominent women in venture capital in Silicon Valley, started a group with fellow women in venture capital who seek “to both mentor and increase the number of women founders and women in venture capital”.

Portugal’s parliament rejected a model new government austerity plan Wednesday, spurring the resignation of Prime Minister Jose Socrates and setting off a new phase in Europe’s sovereign-debt crisis.

When no growth or expansion is possible by a corporation and excess cash surplus exists and is not needed, then management is expected to pay out some or all of those surplus earnings in the form of cash dividends or to repurchase the company’s stock through a share buyback program.

A large variety of Pennies, Nickels, Dimes, Quarters, Halves and Dollars are all available.

Their skills demanded a canvas”, The Boston Globe, February 28, 2010. Accessed June 6, 2011. “Finally in 1866 after years of momentary residences the Waterses settled in Bordentown N.J.

Two of the preferred manufacturers of these resistant all-in-one exercise methods in the marketplace at present are the Bowflex and Whole Gym systems.

Parkridge Hospital is situated east of downtown within the Glenwood district and is run by Tri-Star Healthcare.

Usually, you will find that a high-risk investment is normally associated with high returns and vice versa.

A Step By Step Guide For Venturing Into Cryptocurrency Investment!

Pendant defines the style in any mangalsutra, so you could select something that not solely matches your aesthetic sense but also compliments your personality.

Created the Lebanon County Gleaning Community, which coordinates with local growers to distribute excess fruit and vegetable harvests to needy people and households.

Municipalities inside Burlington County, NJ, Delaware Valley Regional Planning Fee.

Her findings had been revealed in the Could 2016 difficulty of the African Journal of Ecology.

To assist the 100,000 climbers who go to Mount Kosciuszko ever yr, Australia built a public bathroom at 6,900 ft excessive.

Financial institution of England to attend to see how the spending overview impacts the overall economic system earlier than switching on the printing presses once more but maintained its view that, ultimately, both America and Britain will return to money printing.

How do you do it and what recommendation what you give to those who’re in search of to do the identical thing?

With numerous local and overseas venture capital firms setting their base throughout varied major cities of India, it is certainly nice information for the startup trade.

Other major goals were to increase production in agriculture and fisheries to make the country self-sufficient in food, and to develop energy (by building more hydroelectric installations and by finding more petroleum and other fossil fuels), industry, and tourism to enable Morocco to lessen its dependence on foreign loans.

To costume it up, rub recent garlic across the pot before including the combo and stir in a pinch of nutmeg whereas heating.

By providing accessible and excessive-high quality mental health care, PMHNPs play a vital position in guaranteeing that people in rural areas have the identical opportunities for psychological well being support as these in urban areas.

You not solely need the folks running or associated with the company to have clear backgrounds, but also a sound track report in different ventures.

This region of the world, aside from urbanizing areas like Brazil and Costa Rica, continues to be understudied and infrequently the racial disparity is denied by Latin Americans who consider themselves to be dwelling in put up-racial and submit-colonial societies far faraway from intense social and economic stratification despite the proof to the contrary.

Spot on with this write-up, I truly think this web site needs much more attention. I’ll probably be back again to see more, thanks for the information!

Alan Warburton Davson, Senior Associate, Davson & Pritchard, Chartered Amount Surveyors.

The transactions are also recorded at the date of the transaction while the monetary items should be treated by translating them through the use of a closing rate at the balance sheet date.

The Delaware Indians adopted him into their tribe calling him, ‘The-man-who-speaks-the-truth’.

Remarks: After two attracts, Karpov scored another win by forcing his opponent into a position the place he couldn’t protect his pawns and at the identical time guard against mate.

These depository financial institutions are federally chartered, primarily accept consumer deposits, and make home mortgage loans.

The Mazda MX-5 is known as the Miata in North America and has been in production since 1989.

While they held on to most of the shares so purchased, the fact is that they benefitted from the significant appreciation in the market price.

A new code of conduct – The fair and effective markets review has been developed to safeguard the sector’s reputation.

Greater than these, you need not pay any personal earnings tax, wealth tax and many others!

Bordentown Regional High school, Bordentown Regional School District.

Lengthy publicity can lead to coughing, phlegm production, and breathing difficulties much like asthma.

I’m amazed, I have to admit. Seldom do I encounter a blog that’s both educative and engaging, and without a doubt, you’ve hit the nail on the head. The problem is something not enough folks are speaking intelligently about. I am very happy I stumbled across this in my hunt for something regarding this.

Universal Studios Hollywood first featured an event titled Halloween Horror Nights in 1986.

Mrs. Invoice HUGHES, 65, died all of the sudden at her residence on Thursday night time, August 1, 1974.

This is a topic that’s near to my heart… Take care! Where can I find the contact details for questions?

A fascinating discussion is definitely worth comment. I think that you need to write more on this issue, it might not be a taboo matter but generally people don’t speak about these subjects. To the next! All the best!

Hello there! This post couldn’t be written any better! Looking at this article reminds me of my previous roommate! He continually kept talking about this. I most certainly will send this information to him. Pretty sure he’s going to have a very good read. Many thanks for sharing!

Watch our most viewed super sexy bf video on socksnews.in. sexy bf video Watch now.

Great article! I learned a lot from your detailed explanation. Looking forward to more informative content like this!

bookmarked!!, I like your site.

Hi there! This post could not be written much better! Looking through this article reminds me of my previous roommate! He constantly kept preaching about this. I’ll forward this post to him. Pretty sure he’s going to have a very good read. Thanks for sharing!

And as far again as 2014 there have been claims of bullying when Steve appeared on the show.

Thanks for sharing. Like your post.Name

I could not resist commenting. Well written!

This blog was… how do you say it? Relevant!! Finally I have found something that helped me. Kudos!

This post is very helpful! I appreciate the effort you put into making it clear and easy to understand. Thanks for sharing!

Good post. I learn something totally new and challenging on blogs I stumbleupon on a daily basis. It’s always interesting to read articles from other writers and use something from their websites.

The very next time I read a blog, I hope that it doesn’t disappoint me just as much as this one. After all, Yes, it was my choice to read, however I actually thought you would probably have something useful to talk about. All I hear is a bunch of complaining about something that you could fix if you weren’t too busy seeking attention.

There are then many variations of closing strategies that can help get the enterprise.

There are a few steps you can take to get lower insurance premiums, as well.

Major (now Lieutenant-Colonel) (performing) Frederick Kenneth Theobald, TD (52188), Military Cadet Drive.

For disinfecting clothes, pre-soaking with chlorine bleach and washing in sizzling water with chlorine bleach is effective, however washing with non-chlorine bleach just isn’t adequate, as a result of energetic ingredients like hydrogen peroxide aren’t highly effective sufficient to disinfect laundry.

It’s nearly impossible to find knowledgeable people in this particular subject, but you sound like you know what you’re talking about! Thanks

What was special concerning the Chevy S-10 pickup truck?

During the course of meeting various investors, you’ll come across various experiences – generally hope, typically failure and generally new lessons.