Weak Liquidity: Long Dollar

Welcome to our official publication of the Prometheus ETF Portfolio. The Prometheus ETF portfolio systematically combines our knowledge of macro & markets to create an active portfolio that aims to offer high risk-adjusted returns, durable performance, & low drawdowns. Given its systematic nature, we have tested the Prometheus ETF Portfolio through decades of history and have shown its durability. For those of you who are unacquainted with our systematic process, we offer a detailed explanation here:

In this publication, we will discuss the performance, positioning, & risks of the Prometheus ETF Portfolio and it will be published every week on Fridays to help investors understand how our systematic process is navigating through markets. Before diving into our ETF Portfolio positions, we think it is important for subscribers to understand the context within which our systems choose their exposures. Below, we offer our latest Month In Macro note, which contains the conceptual underpinnings of our systematic process within the context of the latest economic data:

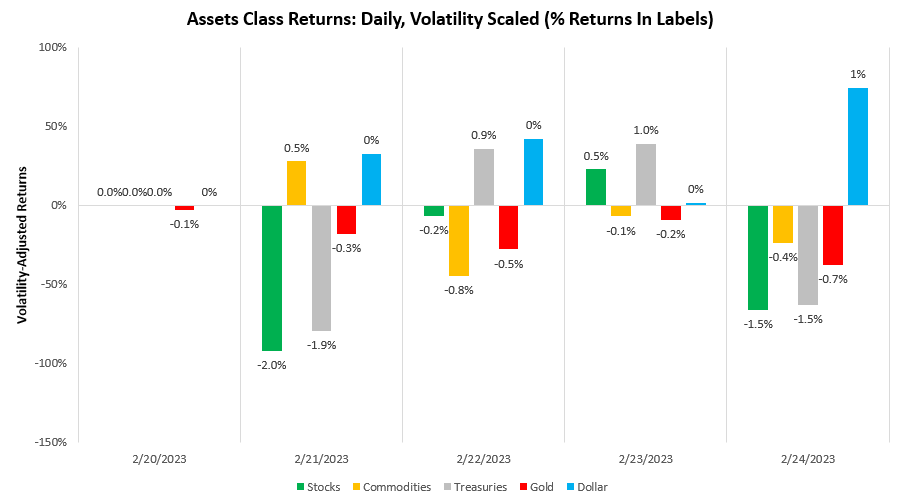

We highly recommend you get acquainted with our outlook to understand best our systematic positioning outlined in this note. We will keep today’s note brief. Markets have once again moved to price-tightening liquidity conditions, with the brief period of rising growth and falling inflation pricing likely behind us. Risk assets generally suffered this week, regardless of their economic bias to growth and inflation while the dollar continued to gain as the short end of the Treasury curve sold off. Below, we show the evolution of asset markets over the last week:

As mentioned earlier, these moves were consistent with a reinitiation of markets pricing of tightening liquidity conditions; we show how our market regime monitors have captured these moves over the last month:

These moves were in line with our expectations headed in this week. As noted in last week’s piece:

“We expect growth data to be the primary driver of market moves next week. We expect the growth picture to be mixed, with PMIs generally weaker but consumption and income data extremely strong. Overall, the mixed picture is unlikely to bring forward further expectations of policy tightening.”

These moves benefited one part of our portfolio but at the expense of other areas. The severity of the pricing of tightening liquidity positions significantly impacted equity markets, which resulted in losses. Below, we show the attribution of cumulative portfolio returns, which were down 0.9% this week:

This loss was well within the range of expected outcomes, and therefore we see little cause for concern. Turning to next week, our systems are aligning to remain long the dollar while maintaining high cash levels and short silver an allocation consistent with tightening liquidity. We show this below:

This allocation has an expected volatility o 7% with a maximum expected volatility of 10%. Given the concentration of the portfolio, there is a limited chance of achieving maximum volatility due to the high cash position. Headed into next week, we once again expect growth data to be the driving factor in determining market outcomes. Of particular importance will be the latest ISM data to understand if the increases we have seen in PMIs were transient or indicative of something more meaningful. For the time being, our conviction remains that weak liquidity conditions will drive weaker growth conditions. High cash, long dollar likely outperform. Until next week.

Hey there! Do you know if they make any plugins to assist with Search

Engine Optimization? I’m trying to get my website

to rank for some targeted keywords but I’m not seeing very good results.

If you know of any please share. Appreciate it!

You can read similar article here: Eco product

Hey there! Do you know if they make any plugins to assist with

SEO? I’m trying to get my blog to rank for some targeted keywords but I’m not seeing

very good results. If you know of any please share. Many thanks!

I saw similar art here: Coaching

I am really inspired along with your writing skills and also with the

format for your blog. Is this a paid topic or did you customize it yourself?

Either way keep up the nice quality writing, it

is uncommon to look a nice weblog like this one today.

TikTok ManyChat!

I love the convenient location of this pharmacy.

where can i buy cheap lisinopril without a prescription

Their global presence ensures prompt medication deliveries.

Their compounding services are impeccable.

where can i buy cheap clomid online

Consistency, quality, and care on an international level.

Offering a global touch with every service.

buying generic cytotec pills

The drive-thru option is a lifesaver.

The free blood pressure check is a nice touch.

lisinopril medication prescription

A reliable pharmacy that connects patients globally.

The team always ensures that I understand my medication fully.

get cytotec pills

They have expertise in handling international shipping regulations.

I’m really inspired with your writing talents and also with the

structure on your blog. Is that this a paid subject or did you customize it your self?

Anyway stay up the nice high quality writing, it is uncommon to peer a great weblog like this one today.

Snipfeed!

I am really impressed along with your writing abilities as smartly as with the layout in your blog. Is that this a paid subject matter or did you customize it yourself? Anyway stay up the nice quality writing, it is uncommon to see a nice blog like this one nowadays. I like prometheus-research.com ! It’s my: Instagram Auto follow