Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

If you haven’t already, check out Episode 4 of the Prometheus Podcast! For this episode, we have the pleasure of once again hosting Darius Dale, Founder & CEO of 42 Macro. For those of you who missed our previous conversation, we highly recommend you give it a listen for a better understanding of his sophisticated framework (Click here). While in our last conversation, we focused more on mechanics, today we’re going to spend our time discussing the current state of the economy & the outlook for markets. Aahan & Darius traverse the US macro landscape, discussing everything from the Fed & inflation to the reverse repo facility and portfolio strategy. This episode is a must-listen for anyone seeking to manage macro risk during one of the most economically volatile periods in history.

Below are the top observations coming from our systematic tracking of economic conditions:

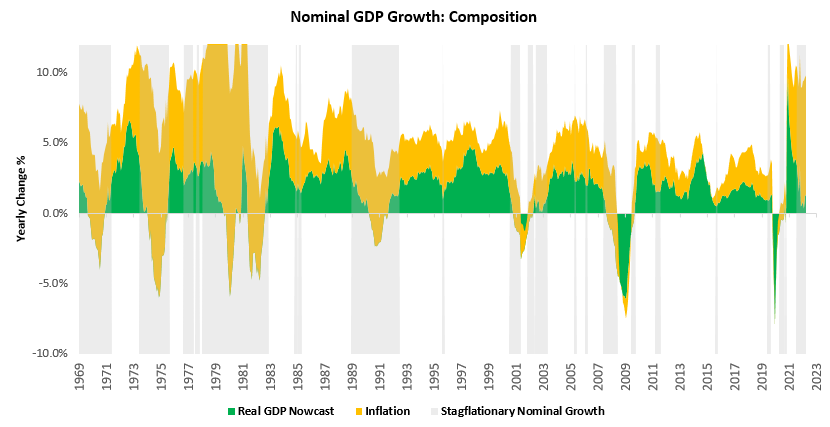

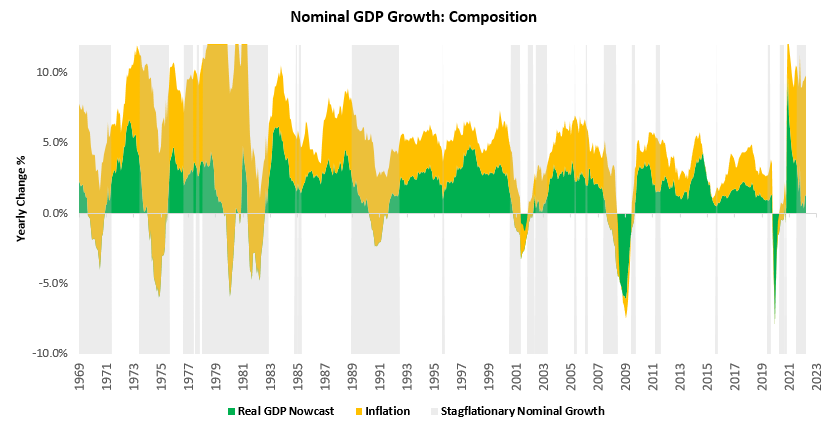

i. We are entering a macroeconomic environment dramatically different from any we have seen over the last 40 years. Our GDP Nowcast currently sits at approximately 1.3%, and CPI inflation is at 8.5%, creating an environment of stagflationary nominal growth. We show this below:

As we can see above, these periods were abundant in the 1960 to 1980 period and generally led the way to a transition to outright stagflation. We continue to highlight these dynamics as this presents a dramatically different investment opportunity set (stagflationary nominal growth) from what most investors have seen over the last 40 years (disinflationary real growth).

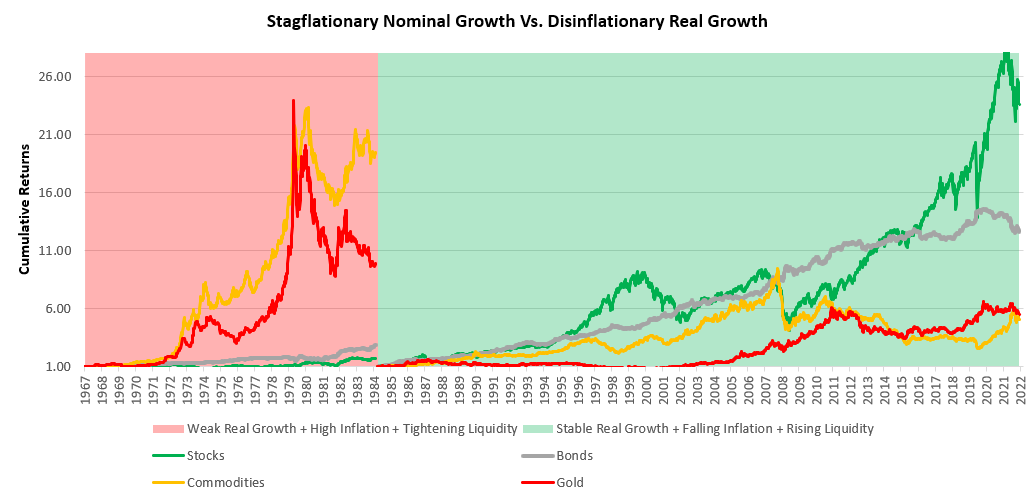

As we can see above, these two environments lead to a completely different distribution of relative returns within asset markets.

We think it is imperative to understand that the returns of stocks & bonds over the last 40 years are not a feature inherent to the asset classes themselves but a feature of the macroeconomic environment. Furthermore, the same is true for the correlations between stocks & bonds. During the 1960 to 1980 period, stocks and bonds had a strong positive correlation. The combination of these factors implies not only a difficult environment for stocks & bonds individually but also as a combination in a portfolio.

Our understanding of these dynamics has once again led us to short both stocks & bonds while maintaining a small allocation to commodities and other inflation hedges. If this environment persists, our systems will likely add more commodity exposure as our timing tools present the opportunity to do so.

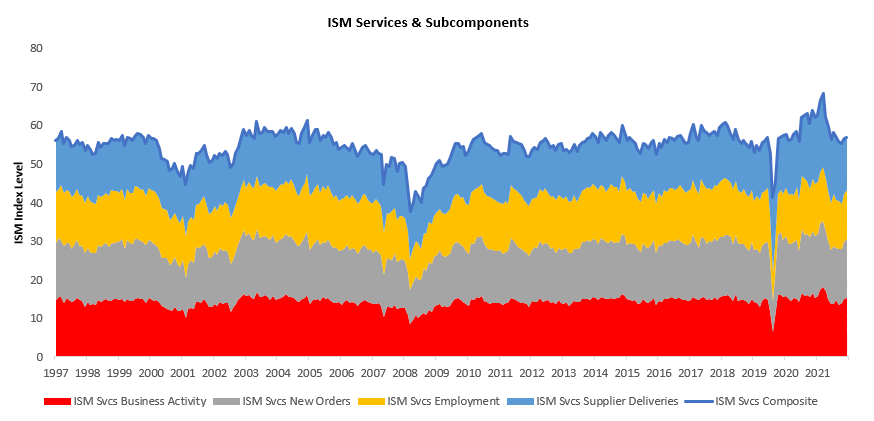

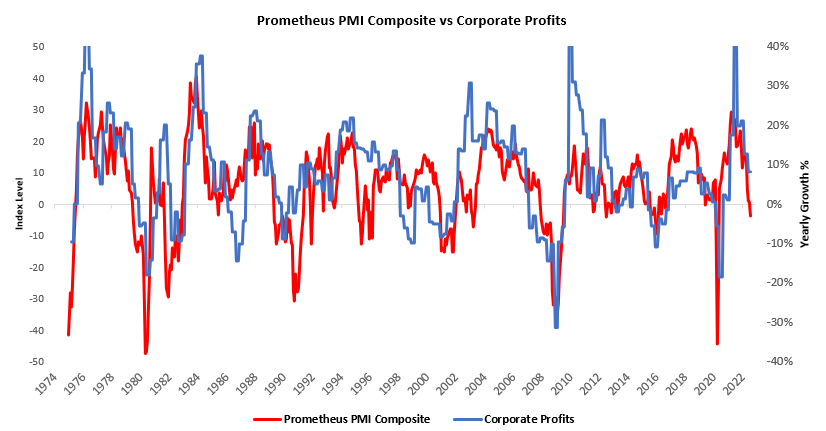

ii. ISM Services data came in stronger than expected, but our PMI Composite tells us the broad trend remains one of weakening. The ISM Manufacturing data showed an expansionary reading of 56.9, surprising consensus expectations of 55.3, implying an 11% YoY change in earnings estimates for the S&P 500. We offer the composition of ISM Services over time below:

This reading was a sequential acceleration within a decelerating trend. This reading surprised expectations with a reading of 56.9 versus the expected 55.3. This datapoint was a sequential acceleration within a decelerating trend. The largest gaining segment was New Orders, and the most significant slowdown was in Employment. We show the composition of this data in tabular form below:

While these numbers indicate a degree of resiliency in the services economy, our broader PMI Composites continue to paint a consistent picture of the outlook for corporate profitability:

Furthermore, these numbers reflect the implied trajectory for nominal earnings, while the picture for real earnings is far worse. Real profitability powers future investment and output; nominal earnings alone are not adequate to do so. The pressures remain on future production and spending.

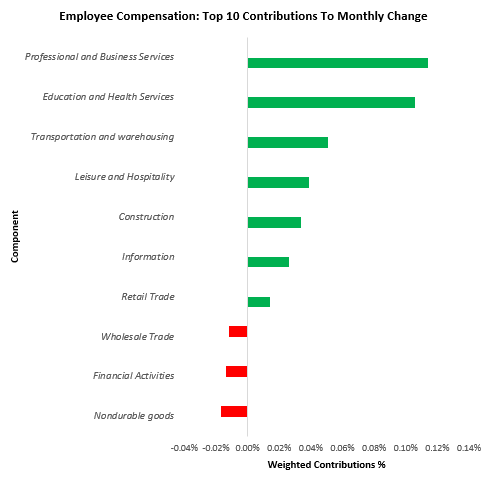

iii. Our estimates of nominal employee compensation showed weakness in august, which will also pressure personal income. While it is well-reported that real incomes remain under pressure, we highlight that our tracking of nominal employee compensation showed a significant deceleration in August, with four of the top ten movers declining in nominal terms. We show these items below:

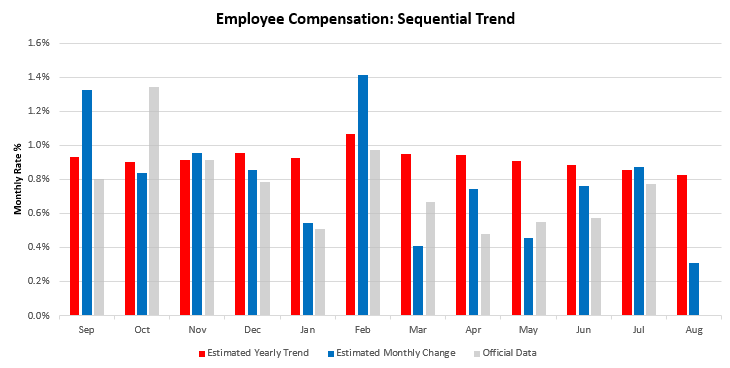

These decreases in employee compensation will likely translate into lower nominal aggregate incomes:

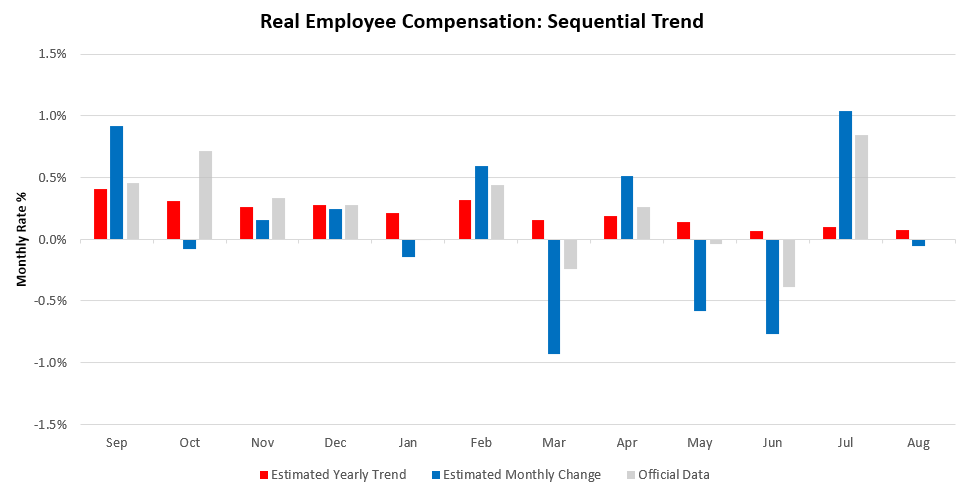

By our estimates, these values will result inc negative real employee compensation growth for August:

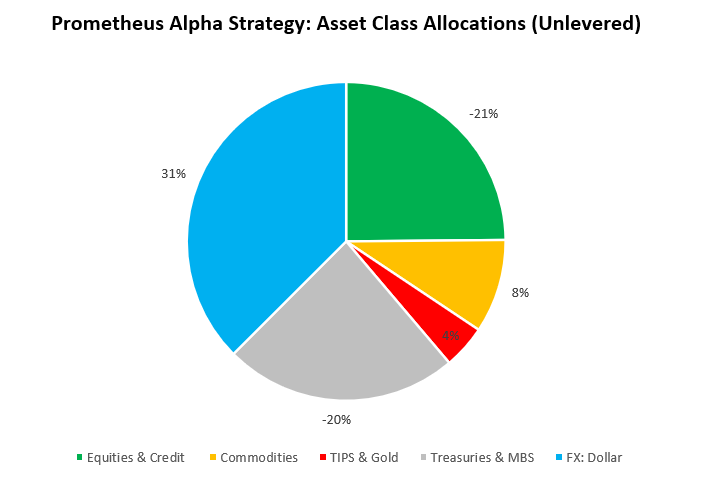

Our systems continue to net out these pressures and judge that we are in a deteriorating growth environment. Therefore, we continue to maintain our equity, credit, & treasury shorts alongside our dollar longs. Our systems maintain the following core exposures at the asset class level:

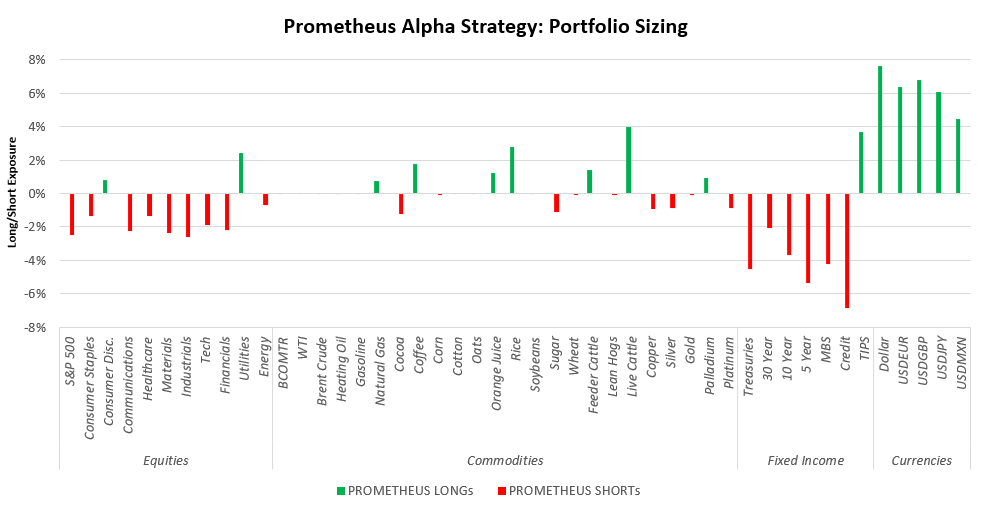

We zoom in to show these positions at the security level:

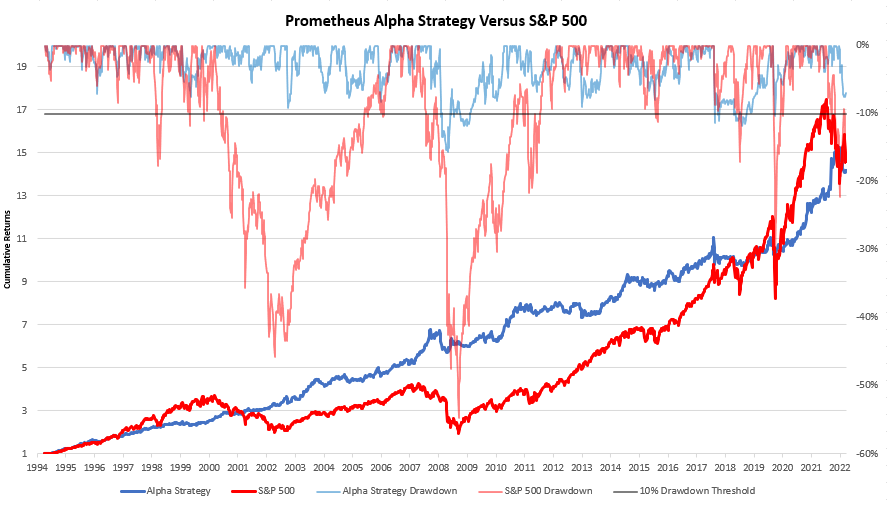

Our systems remain positioned for stagflationary nominal growth and tightening liquidity conditions. Our approach continues to perform well in a dramatically different environment relative to history, and we expect it to continue. Below, we show the cumulative performance for our Alpha Strategy, which targets volatility of 10% through the dynamic use of leverage and is currently modestly levered at 1.39X:

Stay nimble.

Top 100 Searched Drugs.

lisinopril salt

Their global health insights are enlightening.

Their global presence ensures prompt medication deliveries.

lisinopril weight gain

Their free health check-ups are a wonderful initiative.

They have an extensive range of skincare products.

get generic clomid without dr prescription

Their prescription savings club is a godsend.

Their pharmacists are top-notch; highly trained and personable.

cipro prices

Their loyalty points system offers great savings.

hgh kaufen apotheke

steroids effects on women

bodybuilder steroid