Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

If you haven’t already, check out Episode 4 of the Prometheus Podcast! For this episode, we have the pleasure of once again hosting Darius Dale, Founder & CEO of 42 Macro. For those of you who missed our previous conversation, we highly recommend you give it a listen for a better understanding of his sophisticated framework (Click here). While in our last conversation, we focused more on mechanics, today we’re going to spend our time discussing the current state of the economy & the outlook for markets. Aahan & Darius traverse the US macro landscape, discussing everything from the Fed & inflation to the reverse repo facility and portfolio strategy. This episode is a must-listen for anyone seeking to manage macro risk during one of the most economically volatile periods in history.

Below are the top observations coming from our systematic tracking of economic conditions:

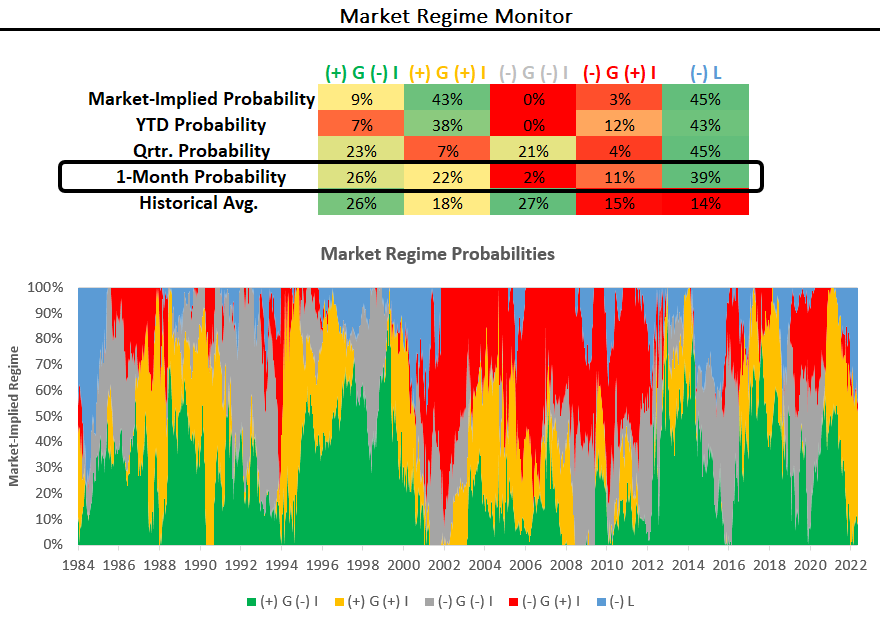

i. Tightening liquidity conditions continue to create a challenging environment for all assets. Our market-regime monitors use our understanding of market pricing to estimate the implied odds of the current macroeconomic regime. Based on our regime recognition, we can be in one of 5 regimes:

-

(+) G (-) I: Rising Real Growth, Falling Inflation

-

(+) G (+) I: Rising Real Growth, Rising Inflation

-

(-) G (-) I: Falling Real Growth, Falling Inflation

-

(-) G (+) I: Falling Real Growth, Rising Inflation

-

(-) L: Tightening Liquidity

In reality, we can be in 8 different regimes based on the various permutations of growth, inflation, & liquidity. However, we compress the tightening liquidity environments into one regime to show the dramatic impact of tightening liquidity conditions on markets. Below, we show how our market regime monitors are currently showing elevated odds of both stagflationary nominal growth and tightening liquidity conditions:

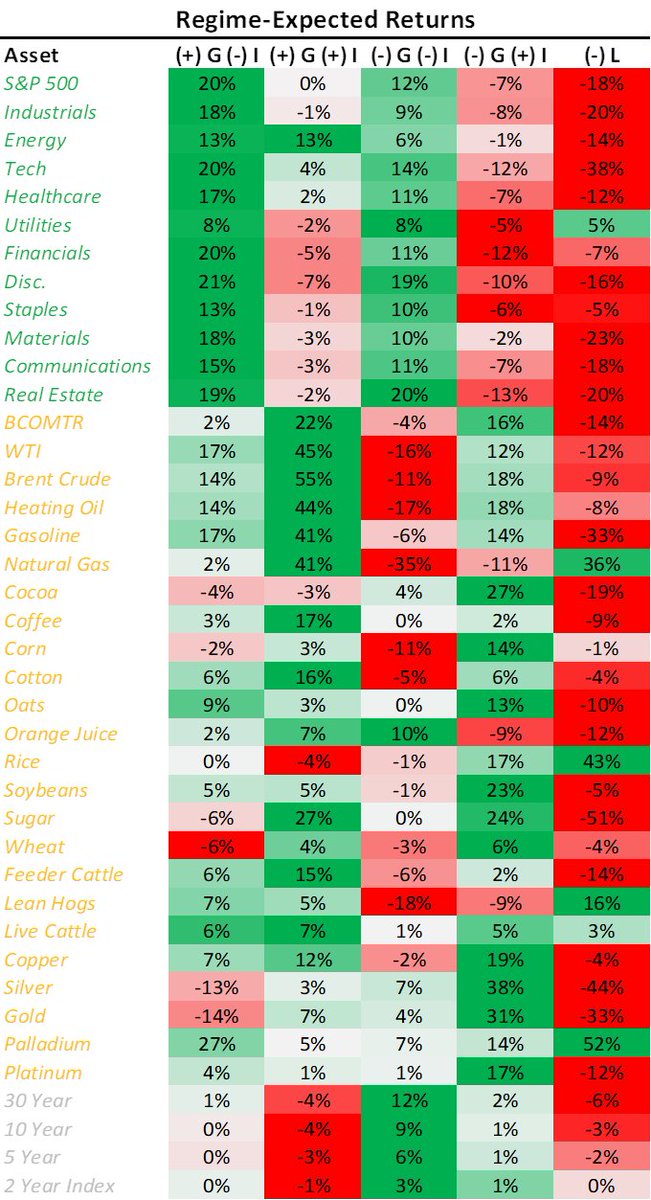

We highlight above that tightening liquidity is now the dominant market regime. Tightening liquidity reflects the drying up of funding liquidity in the economy, i.e. when the dry powder for future economic and financial activity contracts. Tightening liquidity conditions manifest themselves in flattening yield curves, widening credit spreads, cheapening valuations, and poor risk asset performance. Overall, this environment is rare in history as the dominant market regime, but it can be highly impactful when it occurs. To illustrate tightening liquidity’s impact on assets, we show our regime expected returns for equity sectors, commodities, and fixed income.

As we can see, assets across the board tend to underperform during tightening liquidity conditions. In past periods, when we have witnessed sustained bouts of tightening liquidity conditions, we have often seen a reversal by policymakers as tightening liquidity adequately curbed nominal economic activity:

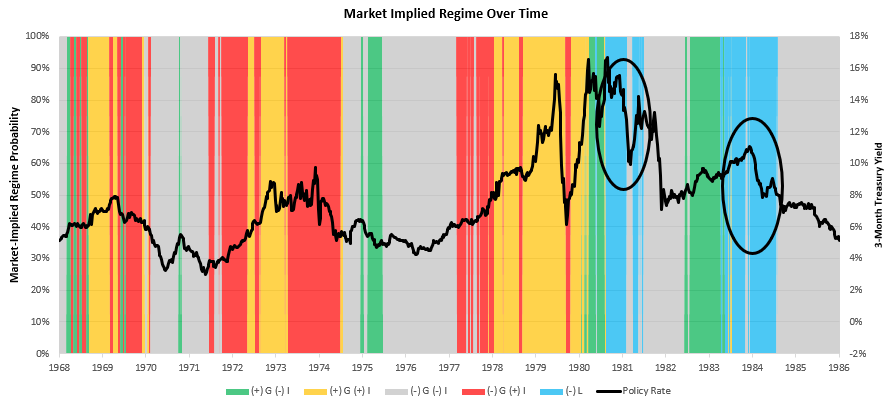

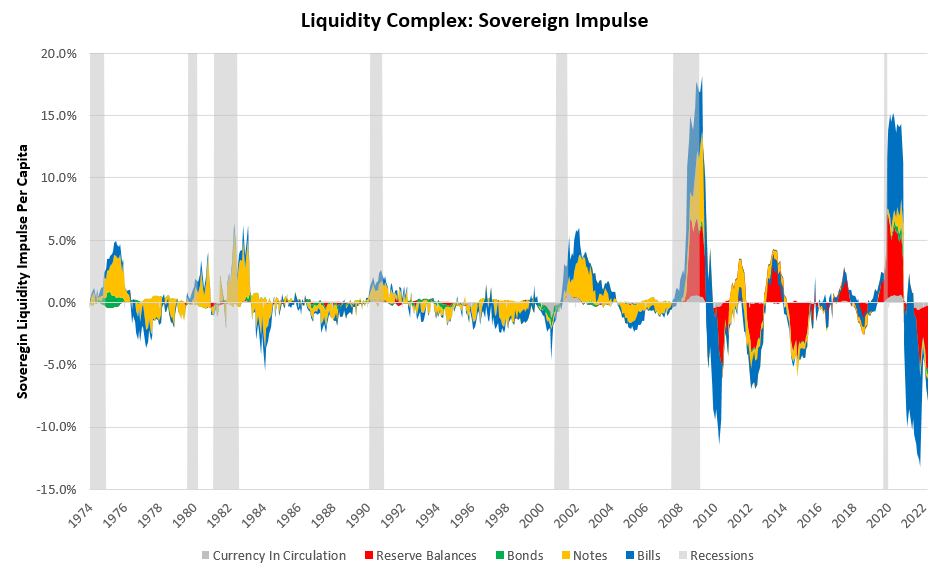

As the Federal Reserve moves to tighten financial conditions further, we will likely see a further extension in market-implied odds of tightening liquidity. Below, we show the combined tightening of liquidity conditions coming from the combined Fed & Treasury:

Therefore, while we remain in an environment of high inflation, our systems have preferred short exposures over long exposures to various asset classes. Our systems continue to monitor the evaluation of both fundamental and market data to asses when to begin adding assets, but for the time being, they maintain the dollar as our largest exposure.

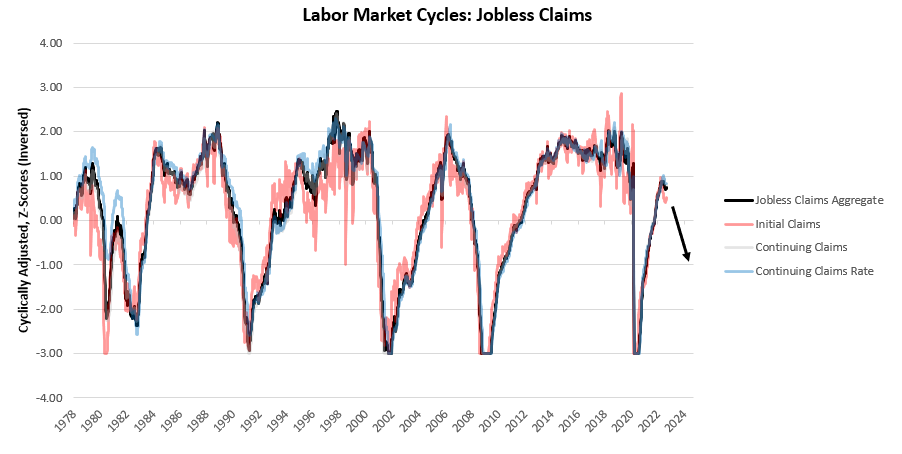

ii. Labor markets remain tight, allowing the Fed to continue tightening. The labor market is the marginal driver of economic activity today, with labor market strength passing through to both real incomes and inflation. Therefore, we are likely to see the deterioration in both real incomes and inflation come alongside the marginal weakening of the labor market. However, recent data suggest we are a ways off from this. Initial Claims disappointed expectations at 222 versus the expected 235 while Continuing Claims surprised expectations at 1473 versus the expected 1438. Below, we show the history of these measures, along with the Continuing Claims Rate, after adjusting these measures to provide an appropriate comparison & to showcase their trajectory over the economic cycle. Additionally, we combine these measures into a Jobless Claims Aggregate to capture the broad trend in the data:

The labor market strength illustrated above will allow the Fed further room to tighten policy; however, the eventual contraction in the labor force will likely create self-reinforcing pressures lower in real incomes and spending, while inflation could remain stubborn.

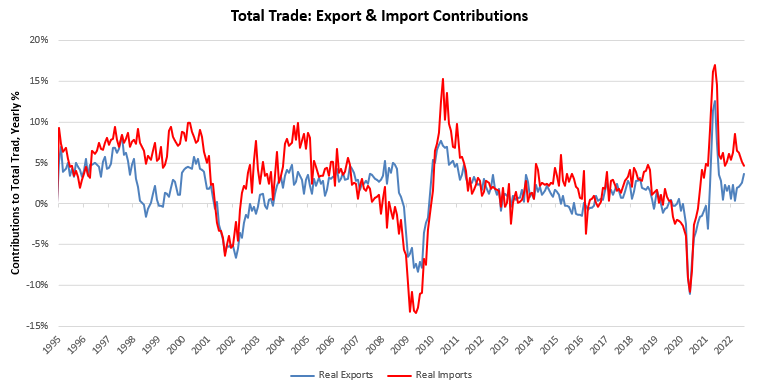

iii. Trade balance data support profitability, but minimally. US Trade Balances showed modest improvement in trade deficits. Exports and imports tend to move in tandem as incomes and output rise and fall. The difference between the two (trade balances) is passed on to the corporate sector through higher revenues. However, the changes in trade balances in the US are not adequately large to offset domestic spending & investment dynamics:

Overall, the pressures on profitability due to declining real incomes and tightening policy liquidity remain in place.

Systematic Positioning

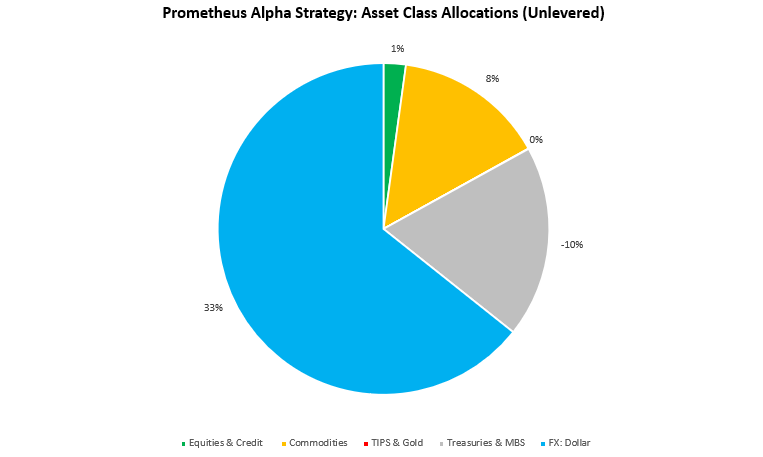

Ahead of next week, there is potential for our systems to exit equity short on the back of short-term timing signals. From a fundamental standpoint, our systems continue to assess that equities are likely to perform poorly; however, they remain tactical in harvesting shorts. The change in these positions would result in the following allocations at the asset class level for an unlevered portfolio:

However, these exposures are not yet confirmed, with more economic data out tomorrow and incremental market pricing. We wait and watch. Stay nimble.

A pharmacy I wholeheartedly recommend to others.

can you get generic lisinopril without dr prescription

I always find great deals in their monthly promotions.

They keep a broad spectrum of rare medications.

can i get cytotec

Read here.

They’re at the forefront of international pharmaceutical innovations.

buying generic cipro prices

I’m grateful for their around-the-clock service.

This pharmacy has a wonderful community feel.

how to get generic clomid without dr prescription

Their staff is always eager to help and assist.

The ambiance of the pharmacy is calming and pleasant.

cheap cytotec prices

They offer unparalleled advice on international healthcare.

Hassle-free prescription transfers every time.

where to buy generic cytotec online

A global name with a reputation for excellence.

Your article helped me a lot, is there any more related content? Thanks!

“This may be from fruit, juice, milk or another carb-containing meals,” she says,

adding that protein powder also works nicely combined right into

a bowl of oatmeal (or jar of overnight oats).

While there are additional advantages of consuming protein powder after exercise, your high priority

ought to be simply consuming sufficient protein throughout the day.

“Electrolytes can support energy levels by sustaining proper muscle and nerve perform, so consuming them earlier than or during exercise is right,” mentioned Chen. The recommended dose for Dianabol is mg per day, however you can start with a lower dose of 15

mg if you’re new to the steroid. If you wish to enhance the

effects of Dianabol, you possibly can take up to 50 mg per day, however this is not recommended for novices.

It is important to notice that taking Dbol before or after a workout is not

the only factor that determines the effectiveness of the steroid.

Proper food plan, training program, and methandienone 10mg uses rest are additionally

essential for achieving optimal results. Nonetheless, it is important to notice that particular person results might range, and components similar

to diet, training, and dosage can all affect how quickly Dianabol works.

It Is additionally essential to make use of Dianabol as

a part of dragon pharma testosterone cypionate a comprehensive bodybuilding program, somewhat than relying

on the steroid alone.

Extra skilled users might take up to 50mg per day,

but this increases the chance of side effects.

It is necessary to start with a low dose and steadily improve it to seek

out the optimal dose in your physique. Third, food regimen and train play

an important role in getting the best results from Dianabol.

Dbol is a strong steroid that enhances muscle progress, but it’s not a magic capsule.

It Is essential to follow a strict food regimen and exercise routine

to maximize its advantages. A high-protein food plan with

enough energy is critical to support muscle growth, and weightlifting is the best kind of exercise to advertise muscle progress and

energy. In abstract, whereas the results of Dianabol may be felt throughout the first few days of use, it might

take a number of weeks of constant use to see significant modifications in muscle dimension and energy.

After 4 weeks of use, there are several negative effects

of this anabolic steroid that may turn out to be noticeable.

Moreover, taking it before a workout permits the pill time to enter your physique, enabling it to perform to its best potential once you start training.

If you’re a critical fitness enthusiast, you most likely already know in regards to the anabolic

steroid Dianabol. Are you seeking to enhance your muscle-building

journey with Dianabol (Dbol)? Well, if you have been to use correct nutrient timing

for coaching, you would eat one hour earlier than coaching.

Although Dianabol is effective at stimulating muscle growth,

you might be correct in assuming it might possibly also cause adverse unwanted effects.

However, he had to discontinue after four weeks because he began experiencing

unfavorable effects similar to high blood pressure and

stomach issues. However 4 weeks on Dianabol are sufficient to see the outcomes of this anabolic steroid.

So let’s take a glance at how the consumers share their personal

experiences after taking a 4-6 weeks Dbol cycle. Finally,

it could be very important take dietary supplements to help

liver health whereas taking Dianabol. This is as a result of Dianabol is processed by the liver, and extended use may cause liver injury.

Milk thistle, NAC, and liv-52 are some of the generally used dietary supplements

to support liver perform.

And, to add much more components price contemplating

into the combination, the type of protein included within the shake—like whey or soy protein—also matters.

Whether you’re utilizing it for muscle restoration or

to fill nutrition gaps, these smart methods can help you get the most out of your protein powder.

Simply remember to start out with a lower dose and steadily increase the dose

over time, and to take a break from the steroid each 4 weeks.

I’m Baiza, a health and health enthusiast, bringing over 5 years

of experience in creating science-backed content material centered on weight reduction and health club fitness.

Consuming whey is crucial when you plan to continue lifting

big weights and working out exhausting while utilizing anabolic steroids.

With D-Bal, you may obtain all of the muscle-building

effects of steroids with out actually ingesting them.

Keep In Mind to at all times seek the assistance of with

a healthcare professional earlier than beginning any new complement

routine. The timing of your Dianabol dose can affect how your body absorbs

and utilizes the compound. Since Dianabol has a relatively brief half-life of about 3–5 hours, strategic

dosing ensures that its anabolic results are maximized throughout key moments of muscle stress

and recovery. Whether you are taking it earlier than or after your

workout is determined by your objectives, exercise intensity,

and way of life.

Dianabol is among the hottest steroids available on the market, and

it’s also effective for pre-workout purposes. This steroid has

been shown to help enhance power, energy, and endurance,

main to raised performance in the fitness center and bodybuilding.

D-Bal is a wonderful complement for extra intensive workouts

because it stimulates testosterone synthesis in males.

And manufactured from all-natural and nutritious ingredients which have additionally

been scientifically tested. Nonetheless, Dianabol shouldn’t be used if your

beloved ones has a history of coronary heart disease or

if your blood strain is already elevated. Multiple Dianabol

customers report they gained roughly 12 to 14 pounds in four weeks.

Taking Metandienone massively will increase nutrient partitioning, driving amino acids and carbohydrates into the muscle

tissue. Both submit and pre-workout timing are good for nutrient partitioning.

Ideally, one can go for the time after they expertise fewer

unwanted side effects after consuming the steroid. Bodybuilders are inclined to feel the effect of the

Metandienone steroid instantly after consumption, although the results might be noticeable after two weeks.

During the on-phase of a cycle, customers can maximize the advantages of Dianabol, similar

to elevated muscle mass, strength, and improved performance.

hgh kaufen deutschland

hgh kaufen deutschland

TRT is a respectable medical treatment prescribed by docs for people whose bodies aren’t producing sufficient testosterone naturally.

It’s like giving your physique a helping hand when its own testosterone manufacturing unit has gone on strike.

This isn’t about turning you into the Unimaginable Hulk;

it’s about restoring your hormone ranges to a wholesome range.

We have a limited amount of scientific research out there on SARMs, notably concerning

their results on people.

Anavar or Primobolan could cause a average drop in testosterone, while stronger compounds such as Anadrol or trenbolone usually cause clinical

hypogonadism. In a bid to extend gluconeogenic substrates, glucocorticoids establish

a state of catabolism in muscles, inducing the breakdown of peripheral muscle fibers and mobilizing towards

the liver for gluconeogenesis. The manufacturing of glucocorticoids is also

subject to adverse feedback regulation. Elevated ranges

of glucocorticoids in the blood inhibit the secretion of CRH and ACTH,

reducing the production of glucocorticoids. This adverse suggestions system helps to take care of the appropriate level of glucocorticoids within the body.

Anabolic steroids usage is simply recommendable to those who are older than 21 years.

Thus, in theory, SARMs replicate the muscle-building results

of anabolic steroids however with out the adverse effects,

corresponding to hypertrophy of the prostate, hypertension,

or hepatotoxicity. SARMs (selective androgen receptor

modulators) are medicine’s try to create superior compounds to anabolic steroids.

We see orals typically becoming problematic when utilized in excessively high

doses or when users do not allocate enough time off in between cycles.

As a general rule, the length of a cycle ought to be equal to

the length off of steroids. Novice bodybuilders typically contemplate whether or not

to decide on oral or injectable anabolic steroids. Reasonable endurance

kind of exercise is effective in retarding muscle atrophy [9] and protecting towards wasting [10].

Antibiotics are substances or compounds that terminate bacterial growth or the bacteria themselves.

They are used to deal with infections caused by microorganisms like fungi and

protozoa. Steroids are fat-soluble natural compounds that practically mimic the

motion of the adrenal glands, the body’s strongest regulator of basic metabolism.

Steroids are extremely potent in treating inflammatory and allergic situations.

There are capabilities that steroids can fulfill that antibiotics aren’t able to,

and vice-versa.

She says 90% of them developed focal segmental

glomerulosclerosis (scarring in elements of the kidney’s filtering units) (5).

Trenbolone is thought to significantly cut back fats mass while facilitating muscle development.

Some bodybuilders additionally employ trenbolone as a slicing steroid to accelerate fats loss whereas sustaining muscle on fewer energy.

Anadrol can considerably suppress testosterone ranges,

necessitating post-cycle remedy to reestablish normal testosterone

perform.

In conclusion, steroids and antibiotics are two important lessons of medication with distinct mechanisms of action and uses in medical therapies.

Yes, each steroids and antibiotics are organic medicine used in medical treatments.

Nevertheless, it is necessary to notice that whereas each steroids and antibiotics may be effective in treating certain medical situations, in addition they include potential unwanted effects.

Creatine, protein, and amino acids can have a positive effect on body composition, but the outcomes are incomparable to

anabolic steroids. Typically, the optimistic results of anabolic steroids are

unrivaled by pure supplements. Nevertheless, this solely applies to a choose number of anabolic steroids which are FDA-approved

and used medicinally (such as testosterone, Deca Durabolin,

and Anadrol). Other anabolic steroids usually are not accredited or prescribed as

a end result of high ranges of toxicity.

It does this by activating natural substances in the skin that suppress immune system responses.

It can also be injected or given orally in pill form when prescribed by a healthcare

provider. They treat many several sorts of inflammatory circumstances

and, while similar, have a number of important variations.

For occasion, hydrocortisone is available as an over-the-counter remedy, while cortisone requires a prescription. Communicate any preexisting circumstances you could have, and any

drugs you take, to your healthcare team to be able to

reduce risk of side effects. Dosages range extensively depending on what situation the doctor is treating you for, and your total

health.

Steroids are fat-soluble organic compounds used to treat inflammatory and allergic conditions.

They may be categorized into sex steroids, corticosteroids,

and anabolic steroids. Firstly, each steroids and antibiotics are organic medicine

which might be generally used in medical remedies. Natural drugs are substances that contain carbon and are derived

from residing organisms. SARMs and HGH are

potentially the closest compounds to anabolic steroids we’ve seen in our clinic,

with them mimicking the muscle-building and fat-burning

properties (with some side effects). Our sufferers who’ve taken HGH still experience a number of unwanted effects (similar to anabolic

steroids), including an increased probability of coronary heart illness (left ventricular hypertrophy) and kind

2 diabetes.