Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

If you would like to get a sense of our picture thoughts and outlook, our Founder, Aahan Menon, recently hosted a Twitter space with @RosannaInvests. Make sure to give it listen if you’re trying to get caught up on our views! Click below to listen on Twitter:

Lets dive into today’s note:

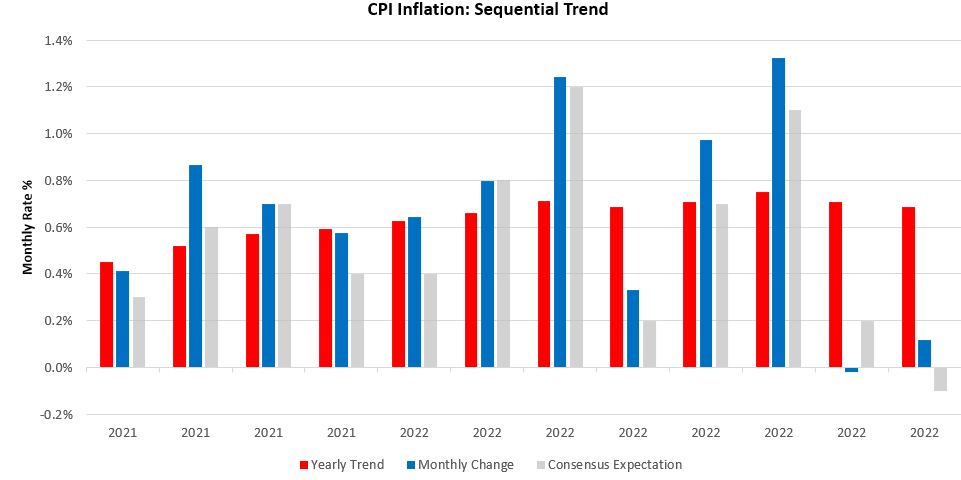

i. CPI surprised expectations significantly. This surprise in CPI has less to do with CPI being extremely strong and more to do with consensus expecting excessively weak CPI. This surprise was very much in-line with our expectations, which we provided our subscribers via our Week Ahead note (click here to read). CPI Inflation increased 0.12% in August, surprising consensus expectations of -0.1%. This print contributed to a sequential deceleration in the quarterly trend relative to the yearly trend. Below, we show the monthly evolution of the data relative to its 12-monthly trend and consensus expectations:

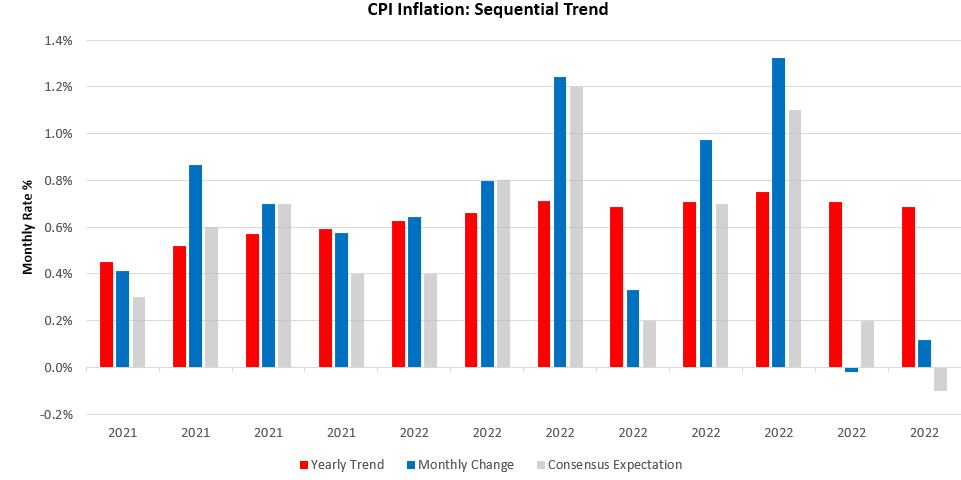

Of particular now was the sustained pressures coming from core-inflation measures. As we have said for a while now the future of inflation will be decided by the balance between the trend strength of services inflation and the decrease in commodity shocks. Today’s CPI print lends credence to the idea that inflation can remain persistent despite declining energy shocks. Below, we show the annualized contributions of various components of CPI to the headline number:

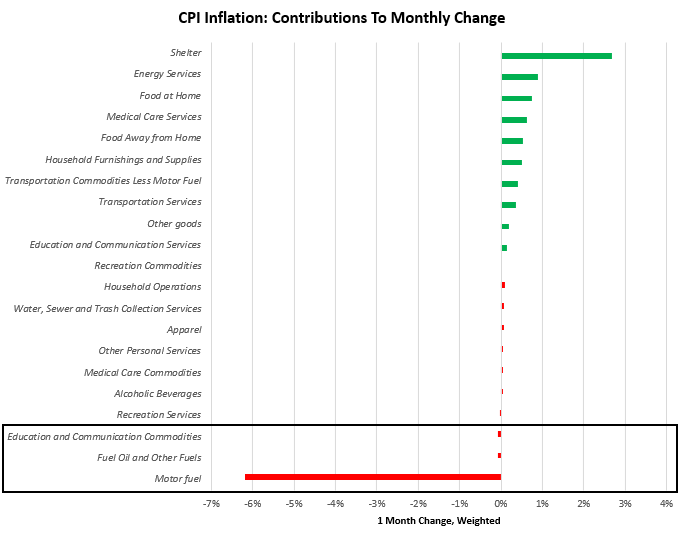

As we can see, headline CPI came in positive despite extremely negative changes in the energy complex. The take-off in shelter prices is critical as the primary driver of inflation upside, and shelter by itself contributed 1.85% to headline & core inflation. This contribution means that even if all other inflation disappeared theoretically, we would still have at least 1.85% inflation. We show this shelter undercurrent below:

In reality, we are likely to be faced with significant inflationary pressures across the economy, which will keep inflation persistent. There remains room for inflation to decelerate, but the level of inflation we continue to experience remains elevated, and both the real economy and financial markets are likely to struggle.

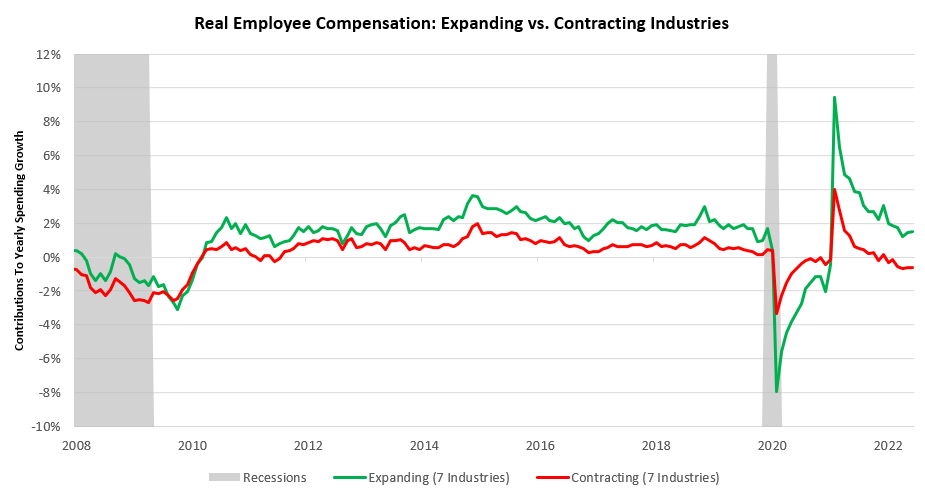

ii. Real incomes are incredibly close to negative territory. While markets today anchored on CPI, our systems also netted out the impact of hourly wage data on aggregate employee compensation. Real wage growth came in -2% versus the prior year, implying significant pressures on real spending. Once again, we will highlight that with these negative wage dynamics; labor market growth is the only thing keeping real incomes expanding. Furthermore, we are seeing that a significant number of industries are now seeing negative income growth, with about half of the industries in the non-farm sector now showing contractionary incomes. We show the weighted contribution to aggregate non-farm income of those industries experiencing positive growth versus those experiencing negative growth below:

This incremental information takes us one step closer to realizing a contraction in real economic activity, i.e., outright stagflation.

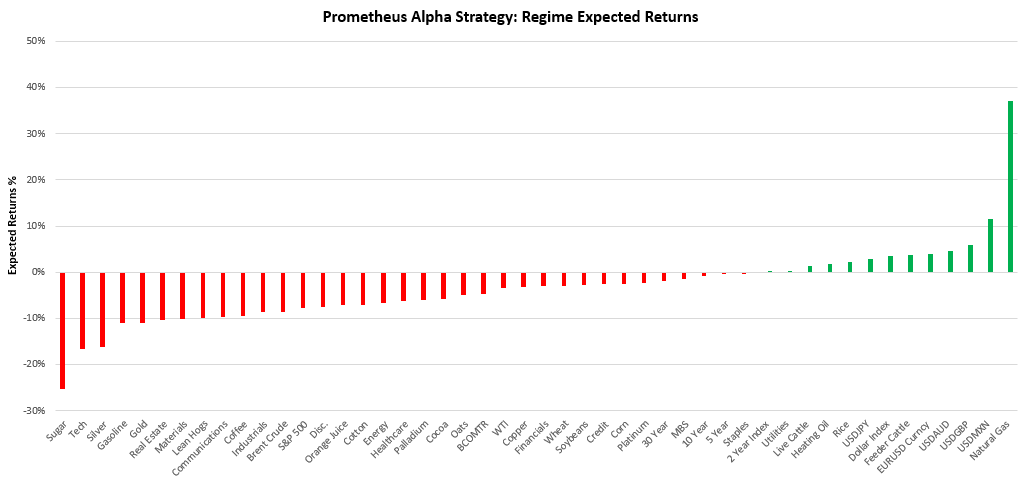

iii. Tightening liquidity is underway, and the regime-expected return on assets continues to suffer. Our proprietary measures of regime-expected returns continue to show an extremely weak opportunity set for investors, especially those limited to long-only strategies. Below, we offer our expected return gauges for all 48 assets we follow:

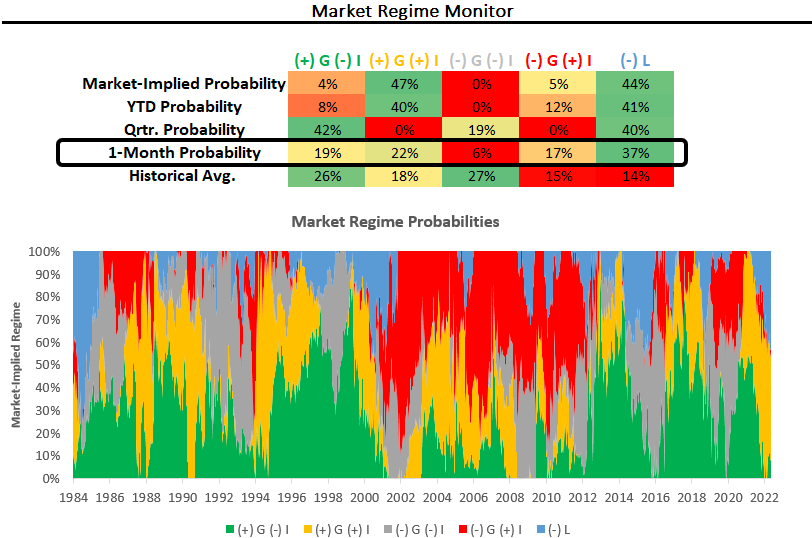

As we can see above, the current opportunity set is primarily limited to the dollar, which is a function of the current macroeconomic backdrop. These estimates stem from our market-regime monitor, which continues to show that we are in a stagflationary nominal growth environment with tightening liquidity conditions:

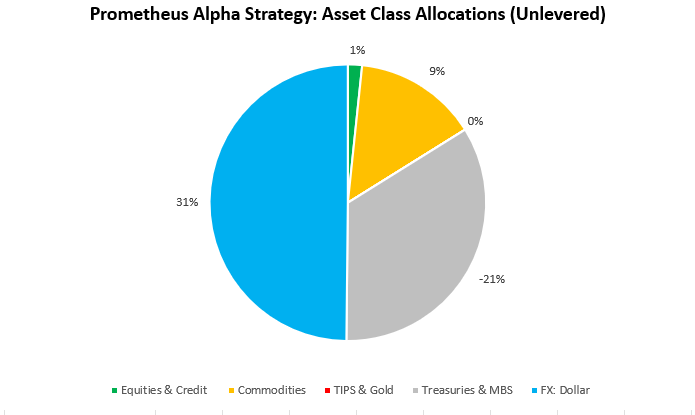

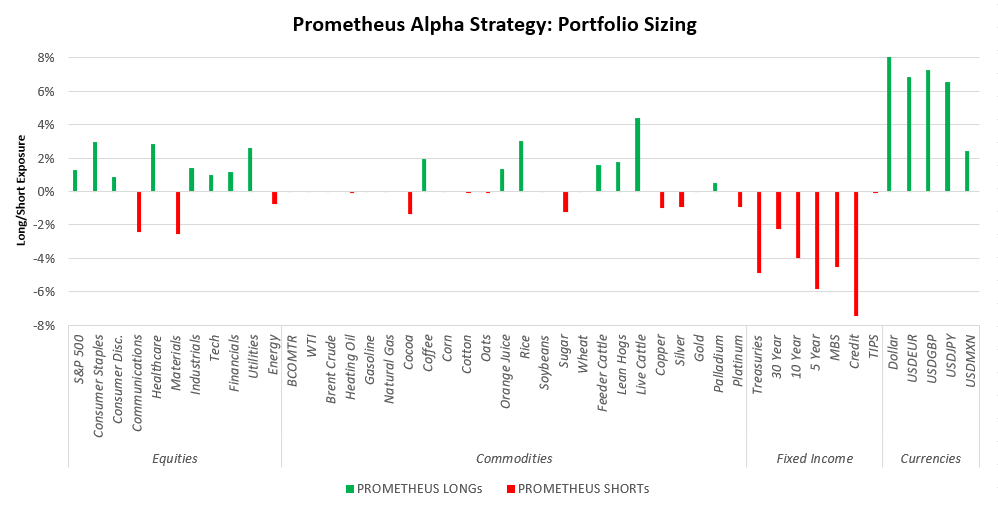

Netting out our fundamental and market signals, we continue to short treasuries & remain long the dollar. We show our systematic portfolio allocations at the asset class level for next week below:

We drill down to the security level below:

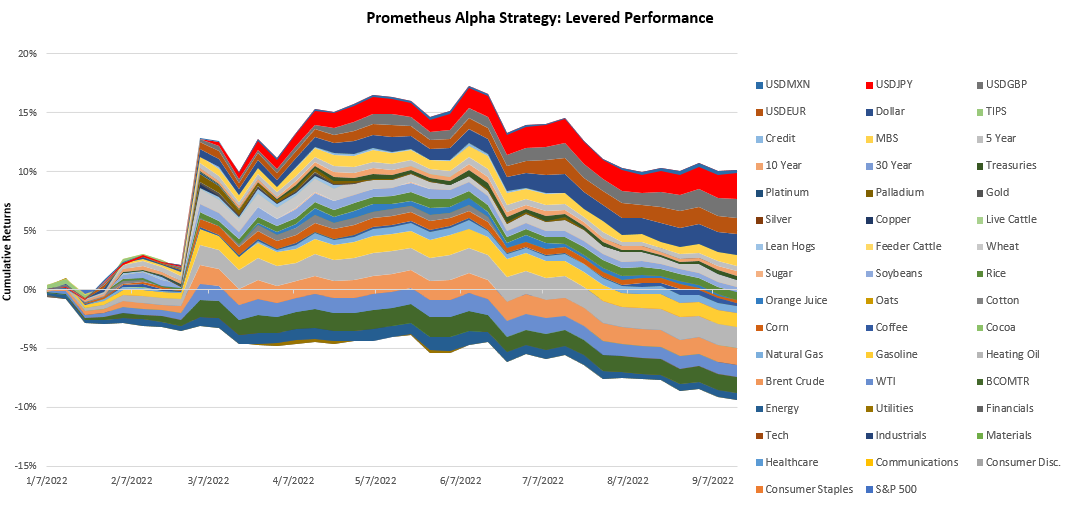

As we can see above, we maintain short exposure to treasuries & long exposures to the dollar as our primary risk. Our systematic approach continues to prove a strong guide this year, with our Alpha Strategy performing well. Below, we show the levered Alpha Strategy performance year-to-date, which targets an ex-ante 10% volatility:

Stay nimble.