This note is a new experimental format, where we share our thoughts on the macro mechanics at play in the context of the current economic cycle. If well received, we will continue to share these Macro Mechanics. Lets us know in the comments below.

Tightening liquidity has resumed. This is a pressure on all assets. The question remains how these pressures will be distributed between assets – which will depend on how these tightening pressures impact the growth cycle.

The Treasury has now extended the duration of its issuance while the Fed continues to keep interest rates elevated and roll off its balance. The combination of these pressures is a tightening of liquidity conditions. The mechanics of how these factors come together to paint the liquidity picture is beyond the scope of this note, but we have written on this subject extensively in others. Today, we are primarily concerned with the transmission mechanism of policy tightening to economic activity.

Government policy acts through a variety of channels, both in income & spending in the real economy, but also through balance sheet channels, in order to achieve its societal objectives. Today, the government needs to use these tools to achieve a slowdown in nominal spending relative to the output capacity of the economy, to engineer inflation durably in line with its 2% objective. Specifically, there are two major areas of spending that tightening financial conditions need to weigh on to generate these outcomes: investment and consumption.

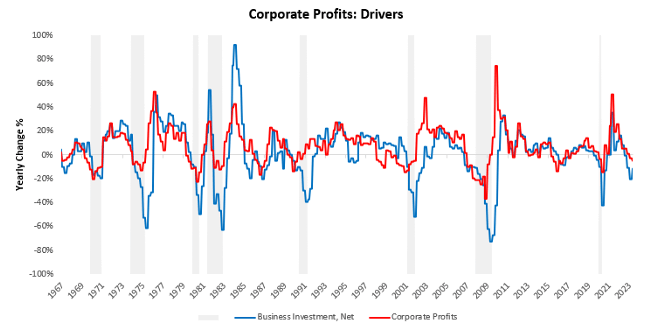

We deal with investment spending first. Investment spending is the most levered form of spending in the economy, with residential and industrial spending making up the bulk of the investment. These areas are extremely sensitive to interest rate changes for a given level of nominal income. As interest rates rise, debt service costs rise, which creates a pullback in investment. When severe, this in itself can pull GDP into contraction. However, this cycle has been different due to several factors which we have explained in the past namely: i) More Cash vs. Borrowing On Balance Sheets ii) A Smaller Manufacturing Sector iii) Booming Semiconductor Construction iv) Automobile Supply Shortages.

The combination of these factors has kept investment spending resilient relative to prior tightening cycles despite most of the mechanisms for tightening to flow through still remaining in place. We think monetary policy will indeed have its typical impacts here, but the Fed will likely have to sustain higher rates to generate its desired outcomes.

This brings us to consumption. Consumption spending is far less levered than investment spending- making monetary policy less effective in curtailing an income-driven expansion like today. As such, the only channels the Fed has to counteract income-based consumer spending are indirect ones in the form of the net worth effect and employment pressures from firms cutting back due to profit squeezes. The Treasury can mechanically exert significant pressure here via taxation, but this seems unrealistic in the current context. However, the Treasury can also pressure net worth via new Treasury bond issuance, which in today’s environment will drag on liquidity conditions and hurt all assets. This is once again a reduction of net worth, which will put downward pressure on spending.

Putting these perspectives together, the Fed and Treasury can exert pressure on spending by attempting to curtail real investment in the economy or hurt asset markets. A combination of these two factors is likely to be most potent in controlling nominal spending, particularly given the resilience of the economy during this hiking cycle. What we think is that the tightening of asset markets or a modest slowdown in investment is unlikely to generate the outcomes that policymakers require.

Additionally, we think it is essential to understand that while asset price declines are an important part of the mix, they will have little impact with a commensurate decline in real investment. Across time, real net investment declines have been the driving force for profit contractions relative to increases in savings rates coming from net worth pressures. Fortunately, these variables are likely to be correlated- as both real and financial investment will be driven by expectations for growth and fueled by existing liquidity.

Zooming into these dynamics, we think that the pressures have begun to build once again. In financial markets, we see the change in Treasury issuance as a meaningful change in the liquidity ecosystem, which will likely continue to weigh on all financial assets. However, stocks continue to outperform bonds, telling us of the ongoing resilience of the nominal economy. In the real economy, we have begun to see the initial stages of weakness emerging in manufacturing, retail, wholesale, and residential construction.

These conditions still remain far from a durable downturn and well-removed from a self-reinforcing contraction. Overall, we are currently seeing the initial stages of tightening liquidity, not contracting growth. However, if we continue to contract liquidity in a broad-based fashion, i.e., with higher bonds issuance, higher rates, ongoing QT, and contracting investment activity- we think contracting growth pricing could be the next stage of the economic cycle.

More specifically, we think that with enough of this sustained-broad-based tightening. We can move from an environment where stocks outperform bonds to one where bonds outperform stocks. Whether either performs on a standalone basis will depend on liquidity conditions.

For the time being, we simply think not enough meaningful deterioration has been achieved to create a self-reinforcing spiral downwards. Without sustained tightening on all these fronts, we think we are in for more of the same, i.e., the economy remains resilient and mixed, and stocks continue to outperform bonds. We are watching carefully. We hope this helps, and thanks for reading.

Please continue writing Macro Mechanics. The articles are very informative.

Thanks

Gary

Do you think it would be possible to quantify the size of the group of people who benefited immensely over the years from the increase in asset prices? The extra wealth accumulated during this period make people less considerate in their spending despite the increase in prices, and hence they continue spending, may be even more than before; due to their perceived net wealth increase. And this is reflected in the consumer spending statistics recently, number came higher than expected. What do you think

I love it, please keep it.

Oh, I like the format, thanks.

Excellent. Thank you.

Love the format.

Thank you for the this write-up. It is a nice format and crisply argued case.

In this piece and indeed in the podcast with Andy Constan there is this idea of the net worth decline (i.e. lower equity prices) leading to reduced spending, which itself leads to increased unemployment. Hence that is the way into a more sustained downturn/ proper recession.

I am struggling to understand this and wonder if it’s more that the equity market pricing pre-empts the reduced spending and that reflects in pricing accordingly. When I think about reduced wealth effect and break it into the top 10% (in terms of wealth) I imagine their consumption is not really affected by their drop in equity portfolios. And the other 90% don’t really have much equity so not sure how they are affected?

how to get cheap clomiphene without dr prescription buy clomid no prescription clomid sale get clomiphene without a prescription how can i get generic clomid without dr prescription can i order clomiphene without a prescription where can i get clomiphene