Welcome to our official publication of the Prometheus ETF Portfolio. Our primary takeaways for last week are as follows:

- Markets have moved to price-in-tightening liquidity conditions, in line with our expectations in our latest Month In Macro note.

- We think the most important thing to note is that this tightening of liquidity conditions is a direct result of resilient nominal GDP.

- Our systems continue to position for resilient nominal GDP, though we expect a turn in liquidity conditions to facilitate weaker growth in the future.

Let’s dive into what’s driving this assessment. Over the last week, our systems moved to price-in-tightening liquidity, with Dollar rising by 0.78%. We show the daily path of returns through the week:

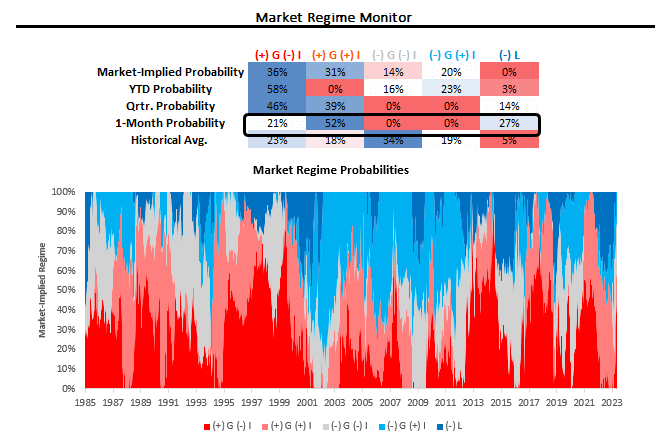

Using our understanding of cross-asset market pricing, we can derive the market-implied odds of varying regimes of growth, inflation, and liquidity. Currently, our proprietary process suggests that we are in a period of (+) G (-) I. We show our market regime monitor below:

We note the rising probability of tightening liquidity.

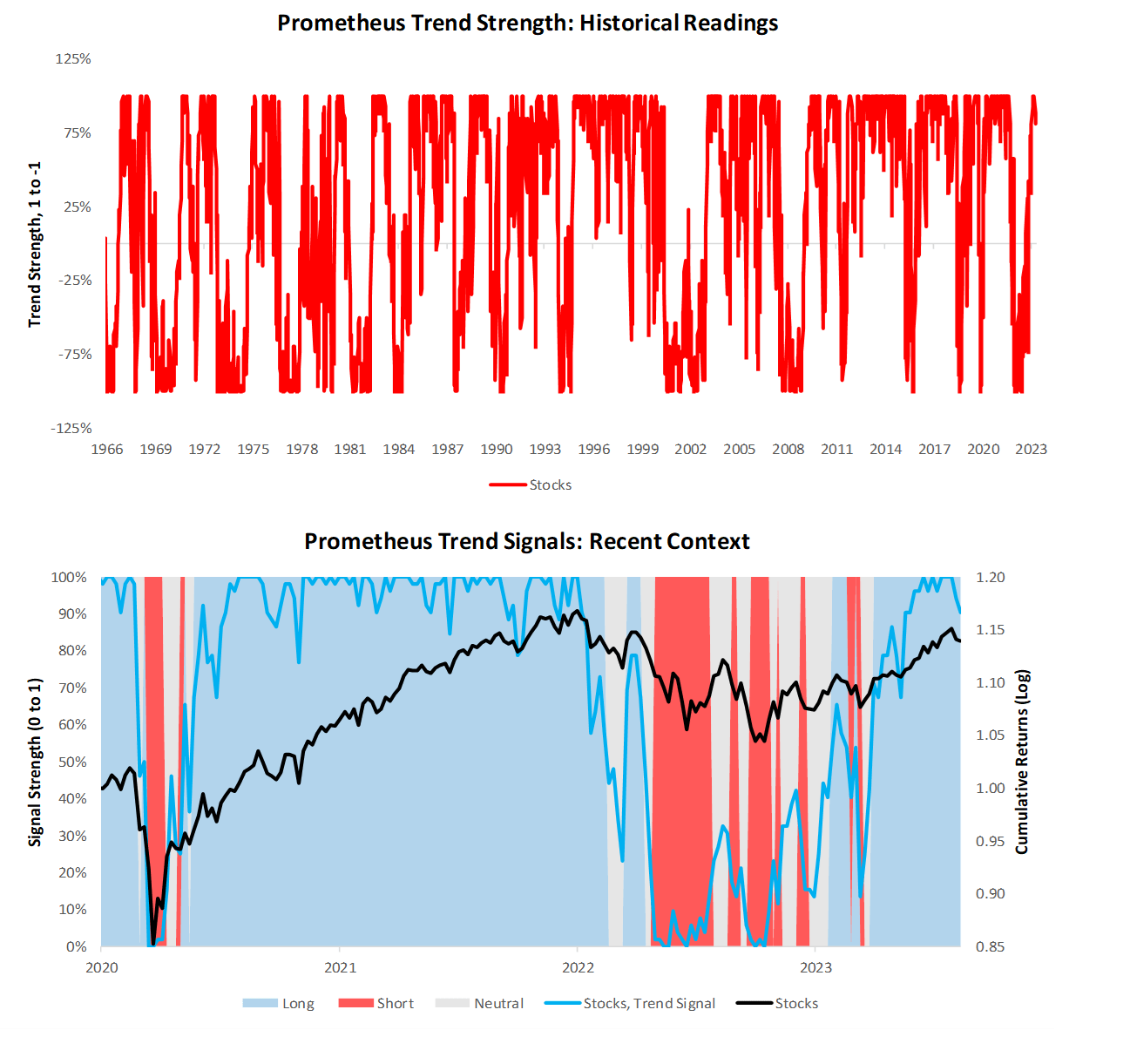

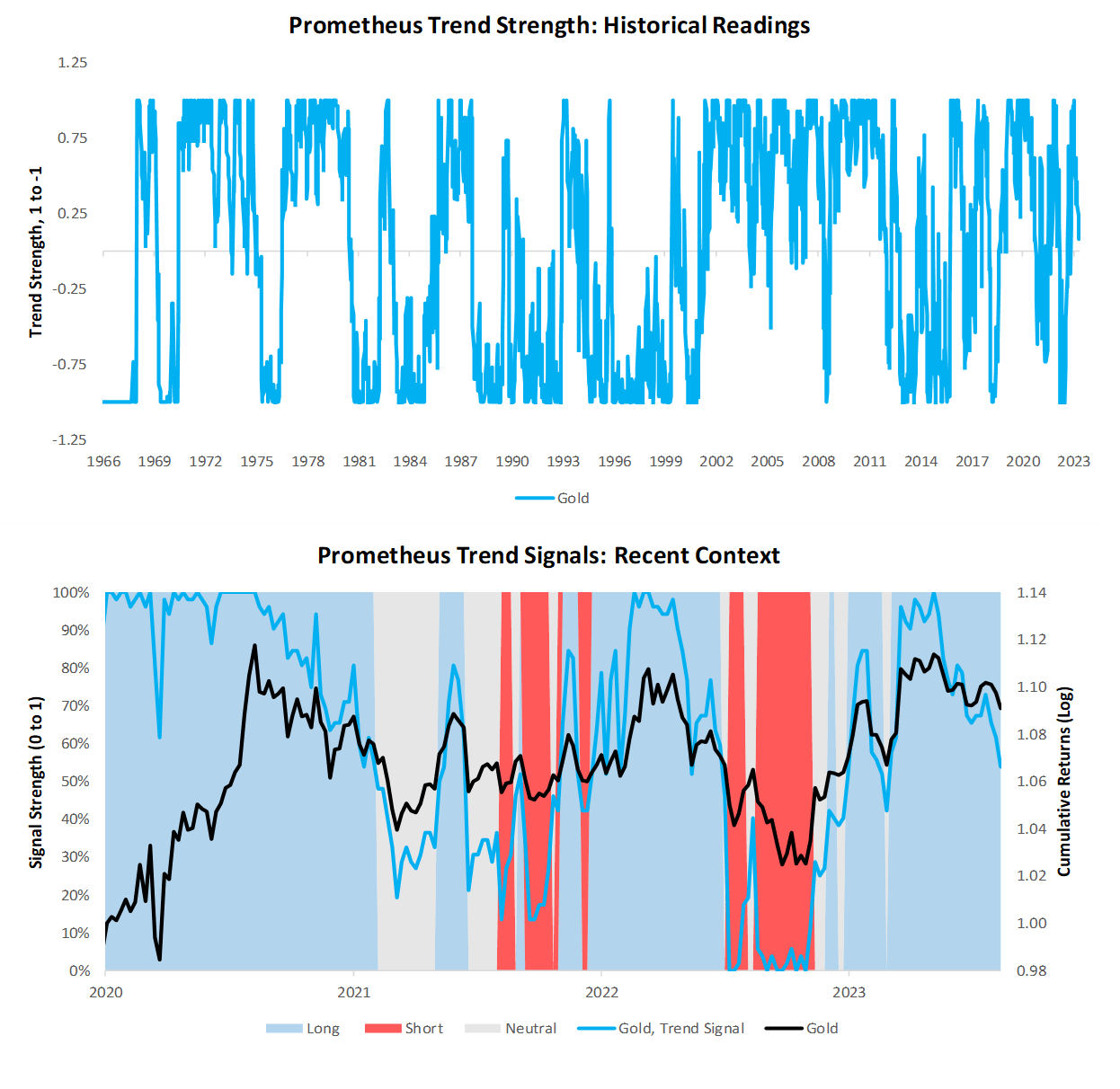

Next, we turn to our trend measures. For context— we have developed a set of trend filters to help us better evaluate the sustainability of asset-class moves. As always, we have tested these trend measures over time to understand whether they can help reliably generate an edge in markets. As proof of concept, we show how these combined signals have performed relative to an underlying portfolio of the same four assets:

Currently, these signals suggest long positions in stocks, short positions in bonds, flat positions in commodities, and long positions in gold.

We begin by showing our signals for stocks. We show both the full signal history and the most recent signal context:

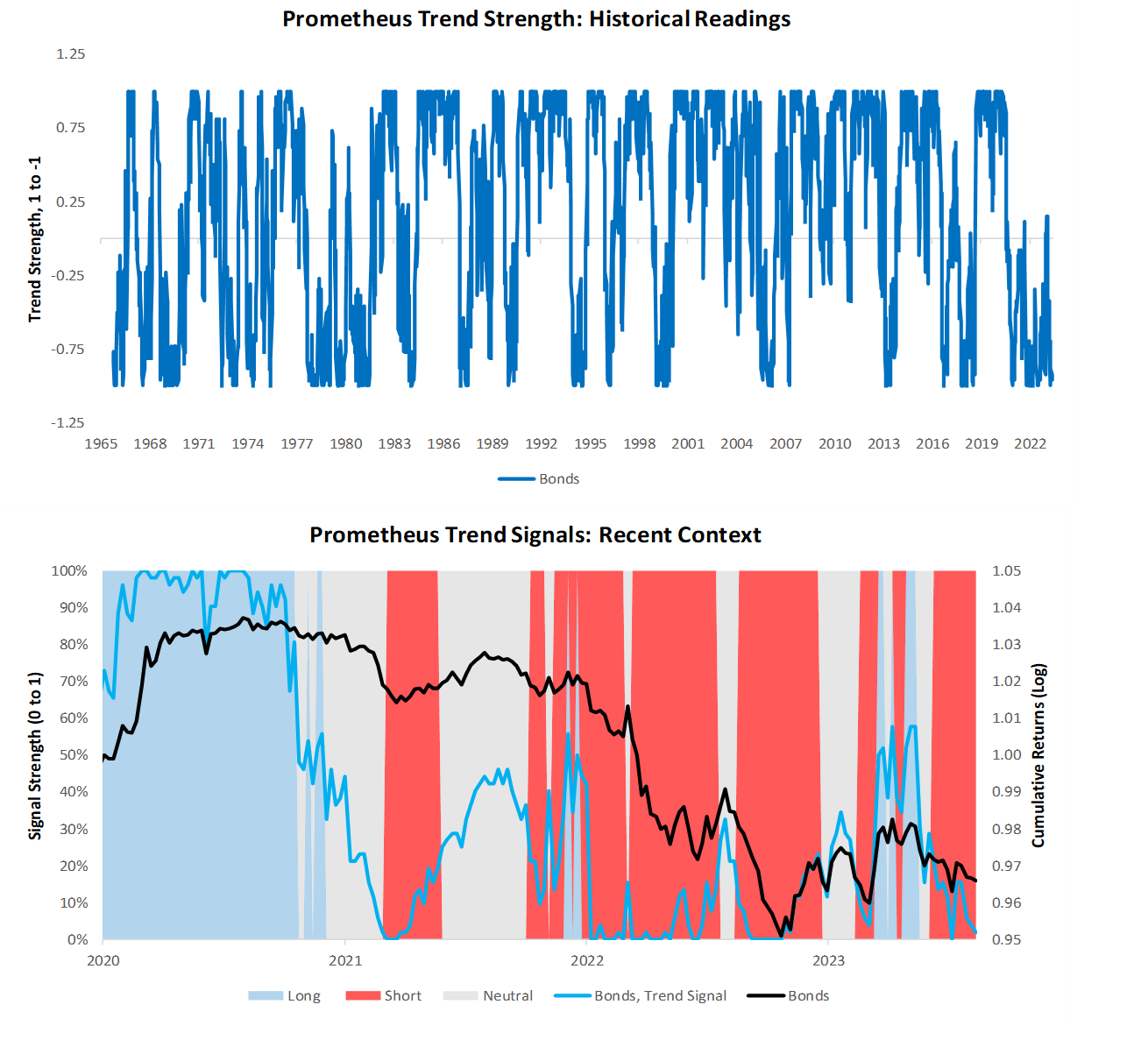

Next, we show our system’s current readings for 10-Year Treasuries:

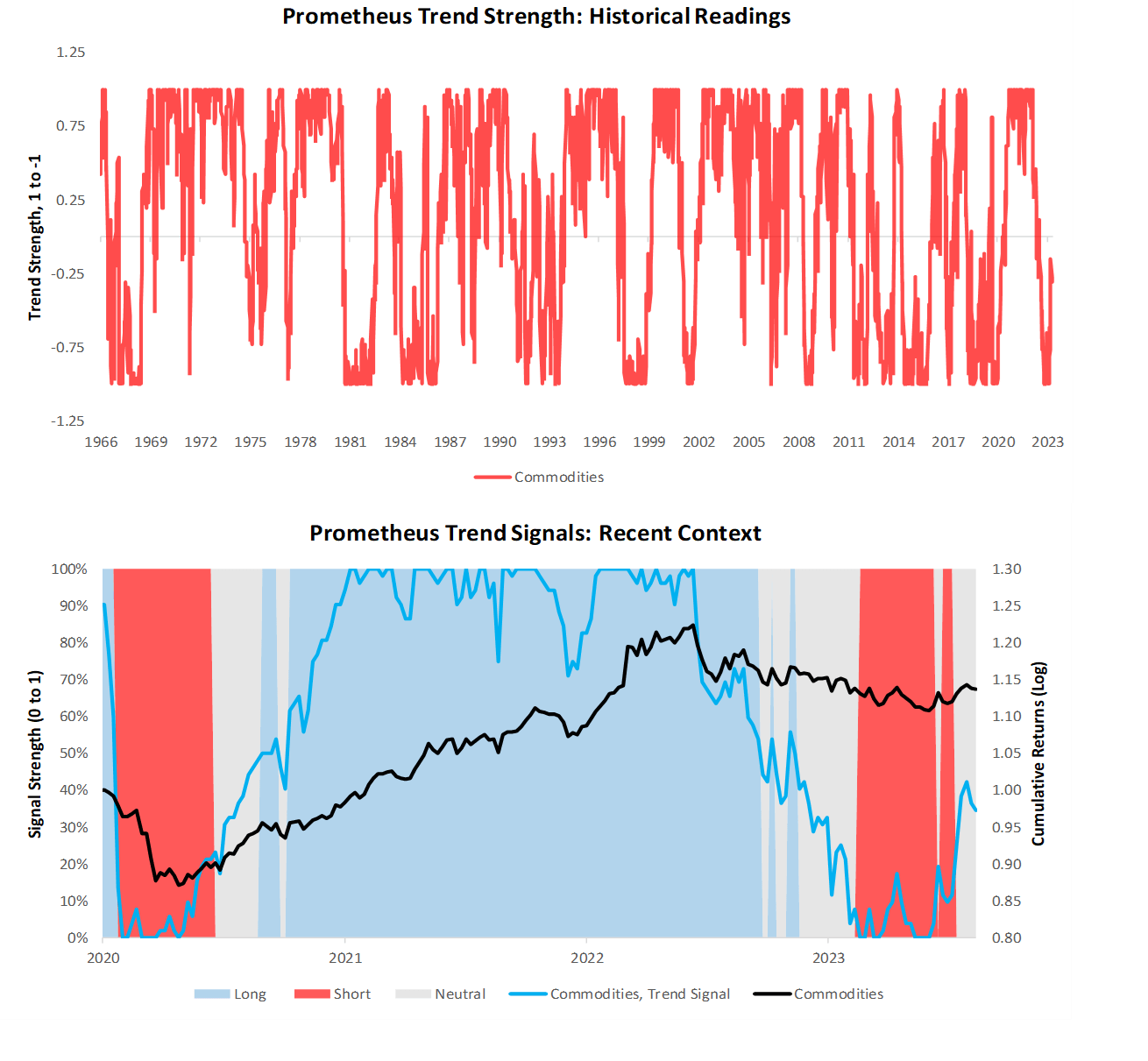

We now turn our attention to commodities:

Finally, we show our trend signals for gold:

We now turn to our systematic ETF Portfolio. Over the last week, the Prometheus ETF Portfolio was up by 0.11%. Below, we show the contributions to this portfolio performance across securities:

Turning to next week, our systems are looking to position the Prometheus ETF Portfolio as shown below. The portfolio contains 16 positions heading into next week. We show these below:

POSITIONS: USHY: 16.29% XLV : 10.51% SPX : 8.57% XLI : 7.74% XLF : 7.27% XLB : 6.63% XLY : 6.36% XLC : 5.93% SOYB: 5.91% XHB : 5.49% XLE : 5.11% DBC : 5% CANE: 4.66% USO: 2.66% UGA : 2.43% Cash: -0.56% . Please note if cash position is negative it implies leverage.

Additionally, we show these positions aggregated into asset class allocations below:

The portfolio has a net exposure (ex-cash) of 100.56%, with a gross exposure (ex-cash) of 100.56%. This allocation has an expected volatility of 15.3%, with maximum expected volatility of 20%. Until next week.

Their health and beauty section is fantastic.

where can i buy lisinopril pill

Their cross-border services are unmatched.

Their global distribution network is top-tier.

sudden stopping gabapentin

Their commitment to healthcare excellence is evident.

Quick turnaround on all my prescriptions.

can i buy gabapentin

A seamless fusion of local care with international expertise.

The best in town, without a doubt.

cost of cipro tablets

They provide a global perspective on local health issues.

Cautions.

buying cheap clomid pills

Their worldwide pharmacists’ consultations are invaluable.

real dianabol steroids for sale