No information provided by Prometheus is to be considered investment advice.

Given our preferences for diversification across asset classes and instruments for optimal results, we’ve often received questions about deploying our systematic approach to accounts limited to only trading equities. Today, we offer some insight into the ETF allocation mix our systems think makes sense based on the current environment. High-frequency macroeconomic data tell us that we are in a stagflationary regime, and asset markets are pricing positive nominal growth, soaring inflation, and tightening liquidity conditions.

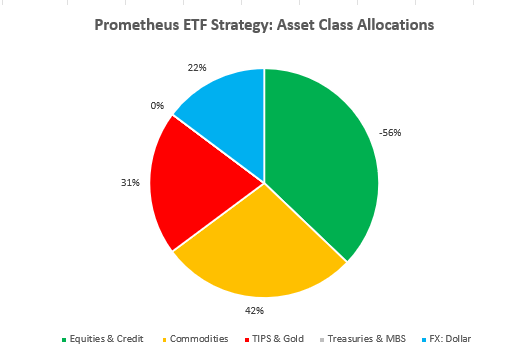

Summarily, our systems offer the following guidance at the asset allocation level:

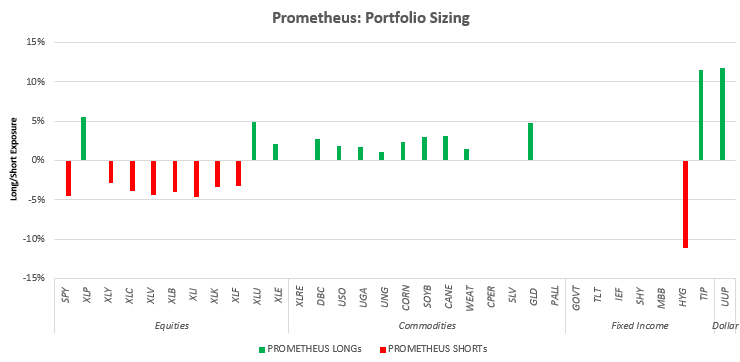

Above, we show the current asset class allocation mix for an levered, long/short portfolio limited to ETFs. The numbers do not add up to one hundred, as it contains shorts (which are expressed as negatives). Specifically, the ETFs contained in the un-levered current allocation are as follows:

- Stocks: SPY (-5%), XLP (6%), XLY (-3%), XLC (-4%), XLV (-5%), XLB (-4%) ,XLI (-5%), XLK (-4%), XLF (-4%), XLU (5%), XLE (3%)

- Commodities: DBC (3%),USO (2%),UGA (2%),UNG (2%), CORN(3%), SOYB(3%), CANE(4%), WEAT(2%), GLD (5%)

- Fixed Income: HYG (-12%), TIP (12%)

- Currencies: UUP (12%)

There are three things to note about these system outputs:

First, they suggest net-long positioning, i.e., despite concerns across financial media of “nowhere to hide,” there remains a balanced mix of longs + active shorts that can help navigate today’s environment even when only limited to ETFs. Second, Credit is a solid short in this environment, given the cyclical slowdown and rampant inflation. Third, the dollar and Commodities continue to have strong trend support and are supported by market regime dynamics creating an unlikely but powerful pairing.

Having gone through major takeaways, let us briefly look at what is driving these views.

Fundamentals: A Tough Macro Landscape

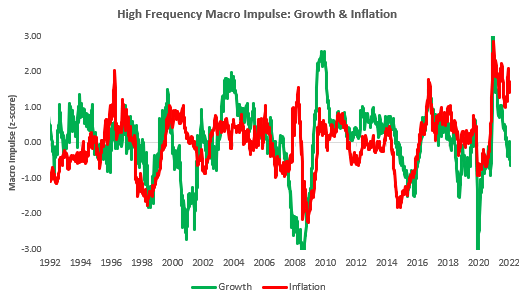

To reiterate thoughts from our previous note: We use a multifactor approach to systematic investment strategy. One of the many slivers our systems use is measures of economic activity to make asset allocation decisions. In particular, our systems consider the impulse in economic data, i.e., the second derivative change in growth rates. Our systems do this via our proprietary High-Frequency Impulse measures, which we have often shown telegraph the direction of coming growth and inflation data. We offer both these measures below:

As we can see above, our Growth measure point to decelerating growth, but our Inflation measures show adamantly elevated inflation. The Growth readings imply lower PMIs and weakening economic activity very soon. Our systems began to warn of a downtrend in growth late last year, and markets are now feeling the pressure of these moves. In contrast, our Inflation measures show inflation remains highly elevated, despite the cyclical pressure to decline. This acceleration primarily comes from high price pressures now coming from the agricultural sector, which we expect to be passed on to households as inflation becomes entrenched.

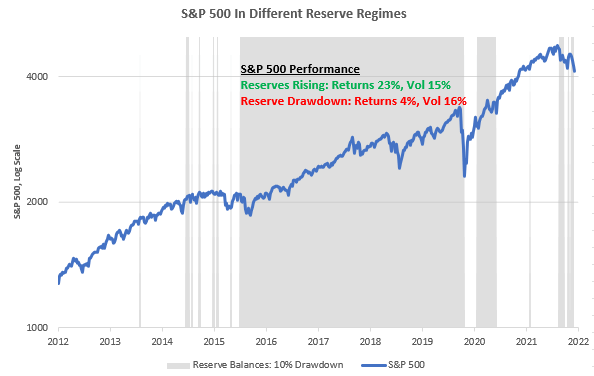

Additionally, alongside these challenging Growth & Inflation dynamics, we are also challenged by tightening Liquidity conditions. We have estimated the impact of Quantitative Tightening, and we assess that it will be further volatility-inducing. This heightened volatility will like come from the drawdown on reserve balances. While reserve balances are not an impetus for financial institutions to lend/transact, they are vital for financial stability and liquidity conditions. QT period tends to have a volatility-generating effect, with average returns on equities and other “risk-on” assets reduced:

Putting these fundamental insights together, we simply don’t think this is a suitable environment for Equities and eventually for Commodities. However, Commodities have been a strong performer year-to-date, which tells us that the need for market-regime analysis is a crucial variable to performance. Our process involves confirmation from asset markets before taking on positions. This brings us to our regime analysis.

Market Regime Dynamics: Shorts Needed To Perform

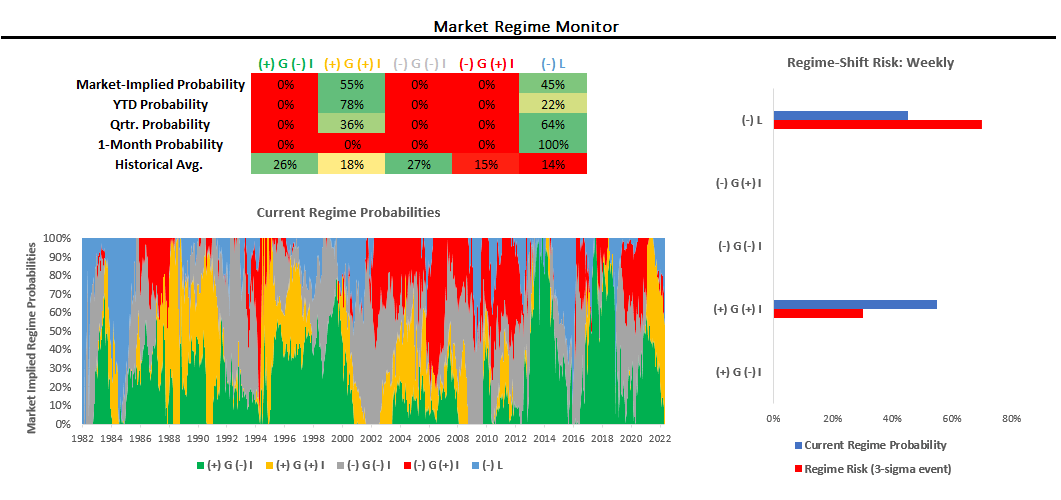

Over the last month, markets have primarily priced (-) L. Nonetheless, our Market Regime Monitors tell us we are in a (+) G (+) I regime. Regime Risk is currently elevated, with the potential for a shift to (-) L. Regime risk has remained elevated for three months, causing many market participants to constantly attempt to catch the proverbial knife of market regime shifts.

We remain focused on being in the dominant market regime throughout the economic cycle rather than perfectly predicting regime-switching. This approach has served us well throughout this year. However, we would be remiss to note that there exists a high likelihood of regime shift, with tightening Liquidity conditions amply and consistently priced in markets. This dynamic makes shorting extremely valuable in today’s context, as during tightening Liquidity environments, very few long positions work well. This brings us to our ETF Strategy.

Putting It Together: ETF Strategy

Unlike our Alpha Strategy, our ETF Strategy doesn’t require constant trading and risk management for entries and exits, i.e., we don’t have dynamic estimates of fair value.

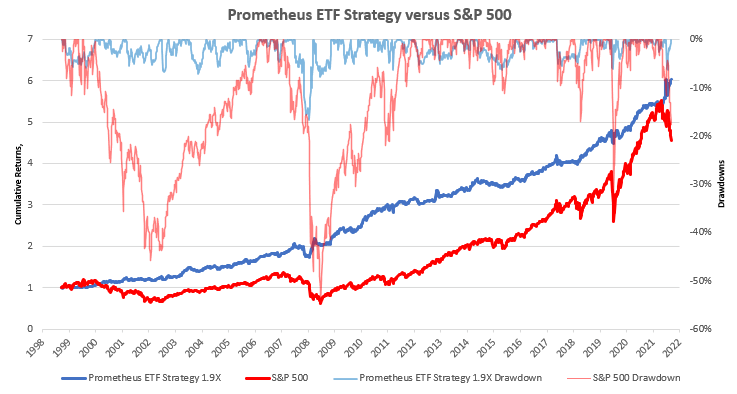

The ETF Strategy takes Prometheus’ measures fundamental economic data and market regime trends to generate signals and trade sizing. We select ETFs so that they are the most liquid in their respective class so that the strategy is scalable for most. To have a long history where ETF data is unavailable, we estimate return data using returns of the underlying assets. We show the performance of the approach relative to the S&P 500 below. We select ETFs so that they are the most liquid in their respective class so that the strategy is scalable for most. We lever the strategy for illustrative purposes to match S&P 500 returns, resulting in a modest level of leverage of 1.9X, which we believe to be accessible to most. We show how this approach has fared since 1998:

As we can see above, this approach outperforms the S&P 500; however, and does so with much lower volatility and drawdowns. However, the level of performance is contingent upon the leverage applied (and potential costs associated with the same). Nonetheless, this approach has generated strong risk-adjusted returns and offers a solid alternative to weathering the pain of drawdowns in environments like today. To sum up what the inputs of this strategy are telling us:

- We are in a stagflationary economic environment. Allocate accordingly on the long side.

- The current market regime favors Commodity and Dollar Longs.

- Equities and Credit are in a downtrend and are not supported by either the market or economic regime we are witnessing.

A picture says a thousand words:

Stay nimble!

Hi there! Do you know if they make any plugins to assist with Search

Engine Optimization? I’m trying to get my blog

to rank for some targeted keywords but I’m not seeing very good results.

If you know of any please share. Appreciate it! You

can read similar article here: Warm blankets

Hi there! Do you know if they make any plugins to assist with Search

Engine Optimization? I’m trying to get my website to rank for some targeted keywords but I’m not seeing very good success.

If you know of any please share. Many thanks! I saw similar text

here: Coaching

I am really inspired along with your writing abilities as neatly as with the format to your blog.

Is this a paid subject matter or did you modify it your self?

Anyway keep up the nice quality writing, it is uncommon to peer a great blog like

this one these days. Beehiiv!

I’m extremely inspired with your writing skills as smartly as with the format in your blog. Is that this a paid subject or did you modify it yourself? Anyway keep up the nice high quality writing, it is rare to peer a great weblog like this one nowadays. I like prometheus-research.com ! I made: TikTok ManyChat

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Your point of view caught my eye and was very interesting. Thanks. I have a question for you. https://www.binance.com/es/register?ref=T7KCZASX