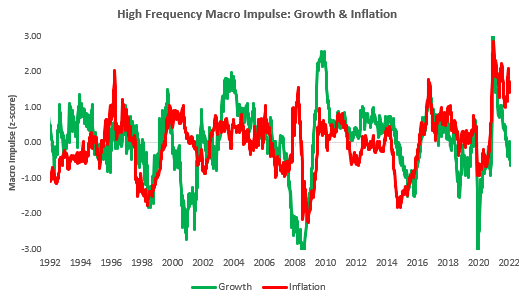

At Prometheus, we use a multifactor approach to systematic investment strategy. One of the many slivers our systems use is measures of economic activity to make asset allocation decisions, i.e., our Fundamental Strategy. In particular, our systems consider the impulse in economic data, i.e., the second derivative change in growth rates. Our systems do this via our proprietary High-Frequency Impulse measures, which we have often shown telegraph the direction of coming growth and inflation data. We offer both these measures below:

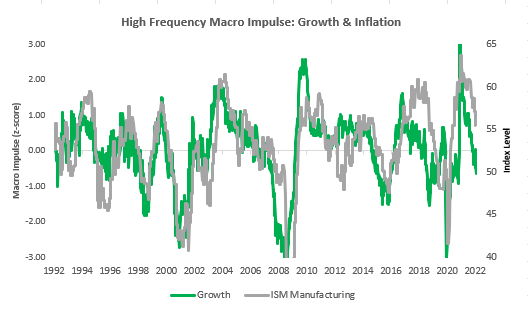

As we can see above, our Growth measure point to decelerating growth, but our Inflation measures show adamantly elevated inflation. The Growth readings imply lower PMIs and weakening economic activity very soon. We offer our High-Frequency Impulse measure versus ISM Manufacturing below:

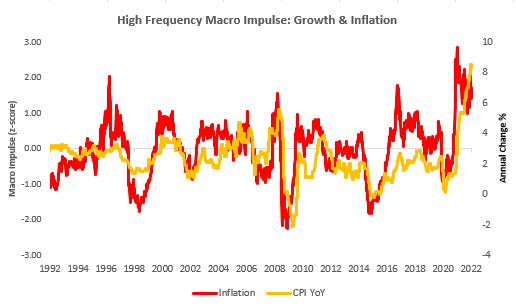

Our systems began to warn of a downtrend in growth late last year, and markets are now feeling the pressure of these moves. In contrast, our Inflation measures show inflation remains highly elevated, despite the cyclical pressure to decline. This acceleration primarily comes from high price pressures now coming from the agricultural sector, which we expect to be passed on to households as inflation becomes entrenched. We show our High-Frequency Impulse measure versus CPI below:

Even if inflation moderates, it is likely that inflation will continue to remain above its medium-term trend due to global supply and demand dynamics. Putting these facts together, we have weakening Growth and persistently high Inflation, which puts us in a stagflationary environment. While this environment may be new relative to recent history, the principles we believe underpin systematic macro allocation can help us through this challenging environment. To reiterate our long-stated views:

We think that Growth, Inflation, and Liquidity are the driving forces for macro-markets. Every asset class is predisposed to benefit from certain combinations of these variables and be hurt by other varieties. In general, all asset markets are hurt by tightening Liquidity conditions. Therefore, when making long-only asset allocation decisions, we focus primarily on the permutations of Growth & Inflation.

We typically look at Equities and Credit (non-investment grade) as assets that perform during periods of stable/falling inflation and rising economic growth due to their variable cash flow and input costs. Conversely, Gold and TIPS are assets that benefit from higher inflation rates and lower growth rates due to perceived inflation resilience. Commodities typically perform best during run-away cost pressures with positive nominal growth rates. Finally, Treasuries & other Investment Grade debt perform during periods of slowing growth and inflation due to their fixed cash flows relative to the declining outlook and haven status. Therefore, using our High-Frequency Impulse measures, we can formulate allocation rules:

- Rising Growth & Falling Inflation = Equities & Non-IG Credit

- Rising Growth & Rising Inflation = Commodities

- Falling Growth & Falling Inflation = Treasuries, MBS & Dollar

- Falling Growth & Rising Inflation = TIPS & Gold

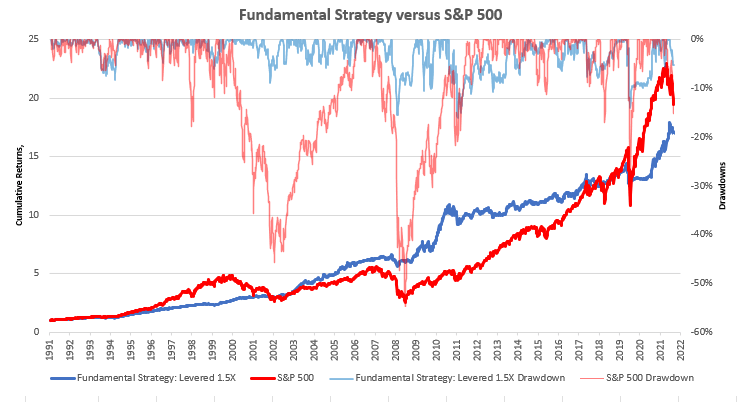

Using these regime-based groups, we can create systematic asset allocations contingent upon the signals from our High-Frequency Impulse measures; we call this our Fundamental Strategy. This strategy sliver generates signals to allocate to the groups mentioned above depending on the current fundamental environment. It allocates to these assets in a manner consistent with their volatilities; therefore, no one asset accounts for the majority of the variance of the portfolio. Finally, we lever the portfolio modestly (1.5X) for illustrative purposes as it includes several low-volatility assets. We show the relative performance of this fundamentals-based strategy versus the S&P 500 below:

As we can see above, this approach underperforms the S&P 500; however, it does so because of much lower volatility. Nonetheless, drawdowns are much less pronounced using our fundamental system due to the agile adjustment of positions with the economic cycle. Further, risk-adjusted returns are far more substantial using this approach than outright S&P 500 exposure.

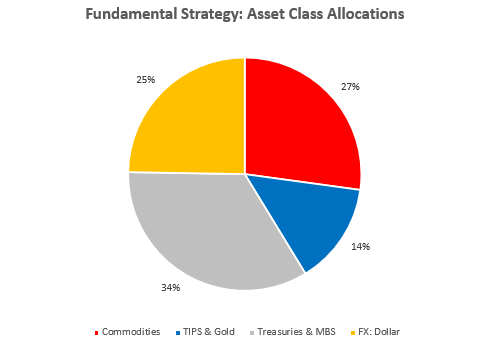

Having shown the historical evidence of asset allocation based on our High-Frequency Impulse measures, let us look at the current context. Currently, our systems estimate that we are experiencing a falling growth impulse and an elevated inflation impulse. Using these factors, our Fundamental Strategy offers the following asset-class guidance in terms of exposure:

Our Fundamental Strategy suggests a 0% exposure to Equities & Credit and has done so since February. This allocation is consistent with what we have seen from our market regime analysis, which prompted our Alpha Strategy to short the Communications Sector beginning at the same time. However, we think it extremely important to note that fundamentals are simply not adequate to grow capital in the current environment. A purely fundamental-based strategy would also be experiencing a drawdown, albeit one significantly less than equities. This drawdown is because the current climate in our assessment demands active shorting, for which fundamentals typically prove inadequate. Of course, we have a host of tools to this end. Nonetheless, economic data does not warrant “buying the dip” in stocks any time soon, nor do market trends. Economic data tells a story of stagflation, and for the long-only investor, it’s a time for capital preservation.

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.