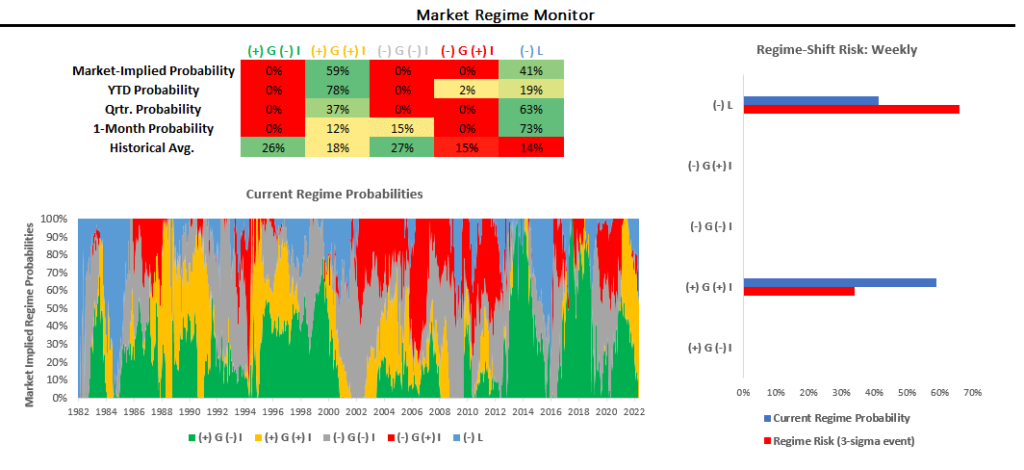

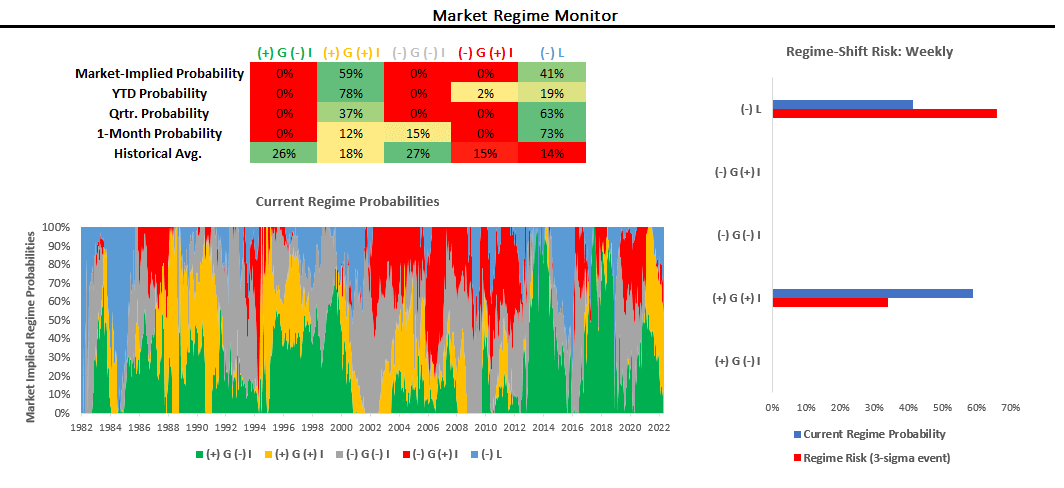

Our systematic tracking of economic conditions paints a picture of stagflation alongside tightening liquidity conditions. Markets mirror this dynamic, pricing strong and inflationary nominal growth and tightening liquidity. Last week, Equities continued their descent while Commodities further extended their rally. We show our Market Regime monitor heading into next week:

Over the last month, markets have primarily priced (-) L. Nonetheless, our Market Regime Monitors tell us we are in a (+) G (+) I regime. Regime Risk is currently elevated, with the potential for a shift to (-) L. The probability-weighted market regime suggests a challenging environment for Equities. Resultantly, our active strategies all suggest equity shorts in the current environment. For those limited to trading ETFs, here’s how our systematic ETF portfolio is set up for the next week:

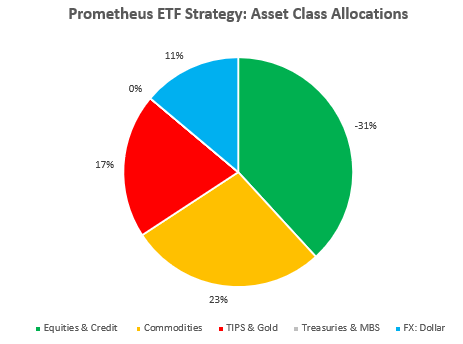

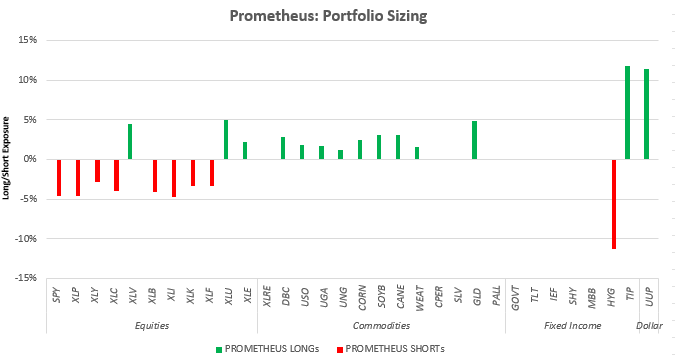

Last week, our ETF strategy recorded gains from equity shorts and commodity longs the previous week. Specifically, here’s our ETF strategy is positioned in individual securities heading into the next week:

- Equities: SPY (-5%), XLP (-5%), XLY (-3%), XLC (-5%), XLV (5%), XLB (-5%), XLI (-5%), XLK (-4%), XLF (-4%), XLU (5%), XLE (3%)

- Commodities: DBC (3%), USO (2%), UGA (2%), UNG (2%), CORN(3%), SOYB(4%), CANE(4%), WEAT(2%), GLD (5%)

- Fixed Income: HYG (-12%), TIP (12%)

- Currencies: UUP (12%)

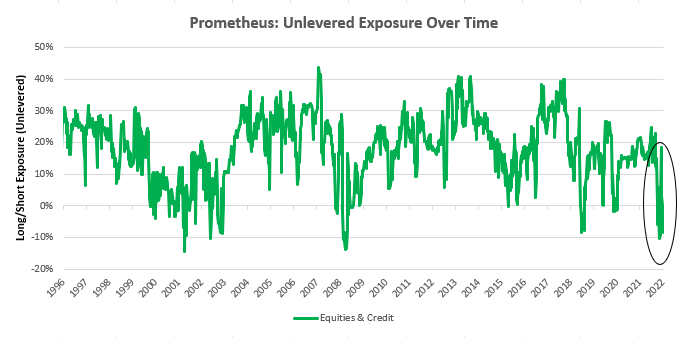

Broadly speaking, all signs point to equity shorts, and despite all odds, commodity strength remains abundant. Therefore, the aforementioned ETF strategy is largely in line with our discretionary assessment of current macro conditions. The un-levered ETF portfolio could experience a max-loss of 6.3% if all portfolio positions move three-standard deviations against the strategy. A 3% loss is most likely on a probability-weighted basis if all portfolio positions move against the system. Of course, we do not expect all positions to move like this, given the healthy balance of long and short positions simultaneously. We again stress the importance of Equity & Credit shorts as diversifiers in the current context. Our signals, which incorporate fundamental data, market regime dynamics, and trend conditions, all point to solid Equity & Credit short conditions, leading to net short exposure:

Please note this display is beyond just ETFs; therefore may differ from ETF Strategy Positioning.

History has typically shown equities to be assets to be long; however, there are times when short exposure can be massively portfolio accretive, and today is one of those times. Now let’s take a look at the risk/catalysts for next week. With regards to economic data, here are the data points most relevant to our systematic tracking of economic conditions:

- Monday: Markit Composite PMIs, New Home Sales

- Tuesday: NA

- Wednesday: Durable Goods Orders, Crude Oil Inventories

- Thursday: Jobless Claims

- Friday: Personal Income & Spending, Goods Trade Balance

Further, on Wednesday, we will receive the FOMC minutes. We will be looking for further messaging around Quantitative Tightening alongside the pace of continued rate hikes. Finally, we will have many FOMC members speaking this week, though we don’t expect a reprieve from the current hawkishness. The biggest risk to our positions is upside surprises in Market PMIs, which are expected to come in at the same level as March at 59.7. However, our High-Frequency trackers give us the conviction that the trend in economic data is indeed lower, therefore turning this risk into an opportunity to fade any bounces in Equities. For long-only strategies, defensive posture and high cash levels remain essential in this environment. Stay nimble!