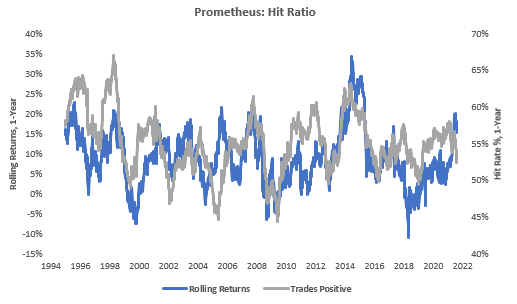

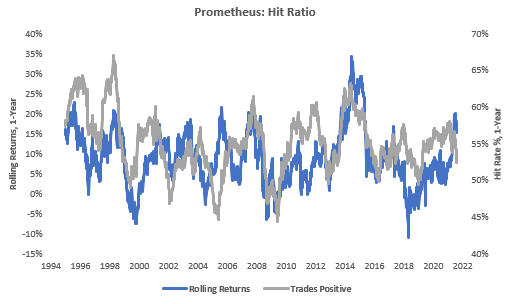

Week 18 2022 proved challenging for Equities and Fixed Income, both finishing the week in the red. Our Alpha Strategy fared well in this context, ending the week flat. Our positions in Commodities performed strongly; however, our Gold exposures dragged on the portfolio. Our hit remained level, holding at 52%:

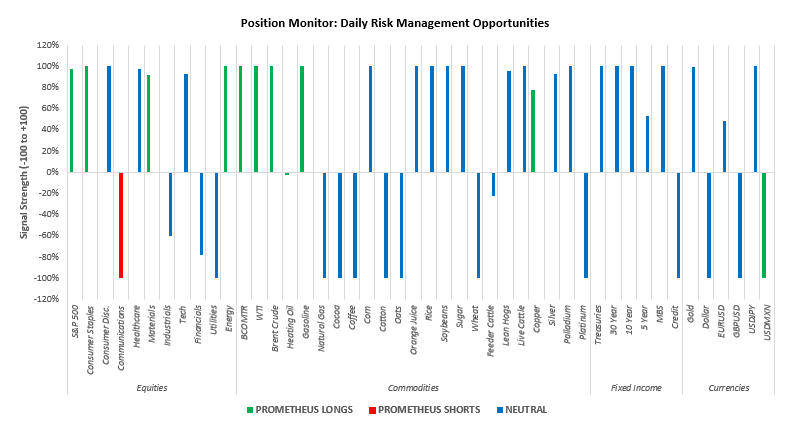

Turning to next week, our systems now have confirmed positions for the next week:

The Prometheus Alpha Strategy is LONG: S&P 500, Consumer Staples, Materials, Energy, BCOMTR, WTI, Brent Crude, Heating Oil, Gasoline, Copper, USDMXN, and SHORT: Communications. Keep in mind; Equity positions are currently sized minimally, given the high noise to signal we are currently witnessing. Our Beta Rotation Strategy is currently LONG: Commodities. A Market Regime Portfolio would be allocated to Stocks & Credit: 2.7%, Commodities: 56.9%, Treasuries & IG Debt: 0%, Gold & TIPS: 0%, Cash: 40.6%.

With regards to economic data, here are the data points most relevant to our systematic tracking of economic conditions:

-

Monday: Wholesales Inventories, Wholesale Trade Sales

-

Tuesday: NFIB Small Business Survey

-

Wednesday: MBA Mortgage Applications, Average Hourly Earnings, CPI

-

Thursday: Jobless Claims, PPI

-

Friday: Michigan Surveys

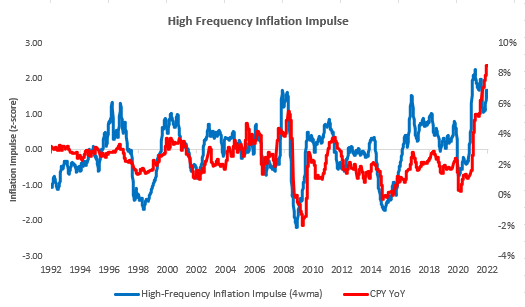

CPI & PPI data will be particularly important and incrementally update our system’s expectations for the future inflation path. Heading into next week, our High-Frequency Inflation Impulse measure has recently shown a significant re-acceleration which could point to further resilience in CPI. We wait and watch:

In this context, it’s worth thinking about the relative value opportunities created by high inflation. Equity beta isn’t a place to be right now. However, relative value does exist between different sectors. One instance is Energy vs. Consumer Discretionary. The current dynamic of extreme inflation favors commodities (and their producers) relative to discretionary spending.

Additionally, by our measures, Energy has a 17% expected return in the current regime, and its performance YTD has been true to form. In contrast, Consumer Discretionary has an expected return of -7%. Long/short pairing can neutralize some of the pain in beta:

Finally, a deluge of FOMC members will be speaking this week. While we aren’t experts in analyzing the nuances of “Fedspeak,” we will carefully be watching for further information on balance sheet reduction, especially for any messaging around the outright sale of mortgages. For a more thorough dissection, check out our recent note on QT here:

We remain in a challenging market environment, where active management is key to avoiding drawdowns. Stay nimble!

Hello there! Do you know if they make any plugins to help with SEO?

I’m trying to get my site to rank for some targeted keywords but

I’m not seeing very good gains. If you know of any please share.

Appreciate it! You can read similar text here: Eco wool

Good day! Do you know if they make any plugins to help with

SEO? I’m trying to get my blog to rank for some targeted

keywords but I’m not seeing very good success. If you know of any please share.

Appreciate it! I saw similar art here: Change your life

I’m really inspired with your writing skills and also with the format

to your blog. Is this a paid theme or did you modify it yourself?

Anyway stay up the nice high quality writing, it’s rare to peer a

nice blog like this one these days. Blaze ai!

I’m extremely impressed along with your writing skills and also with the format for your blog.

Is this a paid theme or did you modify it

yourself? Anyway stay up the nice high quality writing,

it is rare to see a nice weblog like this one today.

HeyGen!

I’m really inspired together with your writing abilities and also with the layout to your weblog. Is that this a paid theme or did you customize it your self? Either way keep up the excellent high quality writing, it’s rare to peer a great blog like this one nowadays. I like prometheus-research.com ! I made: Madgicx

Откройте для себя мир азарта в Kometa Casino — платформа для настоящих ценителей игр, где представлены лучшие

игровые автоматы, азартные развлечения, а также эксклюзивные предложения,

которые помогут увеличить выигрыш!

Комета лучший сайт для ставок.

Почему выбирают Kometa Casino?

Быстрые финансовые операции без комиссий.

Огромный выбор игр от классики до новинок.

Щедрые акции и турниры, делающие игру

ещё выгоднее.

Начните играть прямо сейчас и испытайте удачу! https://kometa-777-spin.bond/

В Aurora Casino каждый момент наполнен азартом, а выигрыши

становятся реальностью. Здесь вы

найдете самые популярные

игры, включая слоты, настольные игры и живое

казино с реальными крупье. Не забывайте про бонусы

и регулярные акции, которые сделают вашу игру еще более увлекательной.

Что отличает Aurora казино от других казино?

Мы предоставляем высококачественные игры, защищенные платёжные системы и

гарантируем быстрые выплаты.

С нами вы получите честную игру и полную прозрачность всех процессов.

Когда начать играть в Aurora Casino?

Присоединяйтесь прямо сейчас и начните выигрывать

большие суммы. Вот, что вас ждет:

Щедрые бонусы для новых игроков.

Участвуйте в регулярных акциях и турнирах, чтобы повысить свои шансы на победу.

Мы предлагаем множество вариантов игр для любого вкуса.

В Aurora Casino ваши мечты о больших выигрышах

становятся реальностью. https://aurora-diamondcasino.quest/

Additionally, moving truck rental companies can charge additional fees that might greatly increase your

initial quote.

I am truly happy to read this weblog posts which consists

of plenty of helpful information, thanks for providing such statistics.

I am extremely impressed together with your writing skills as smartly as with the structure to your weblog.

Is this a paid subject or did you customize

it your self? Anyway keep up the nice high quality writing, it

is uncommon to look a nice weblog like this one nowadays.

Affilionaire.org!

For hottest information you have to go to see world-wide-web and on the web

I found this website as a finest web site for latest updates.

Short commutes in Dallas can easily train you for lesser fees.

Keep track of your gas mileage to show qualification.

Pretty! This was an extremely wonderful post.

Thank you for supplying these details.