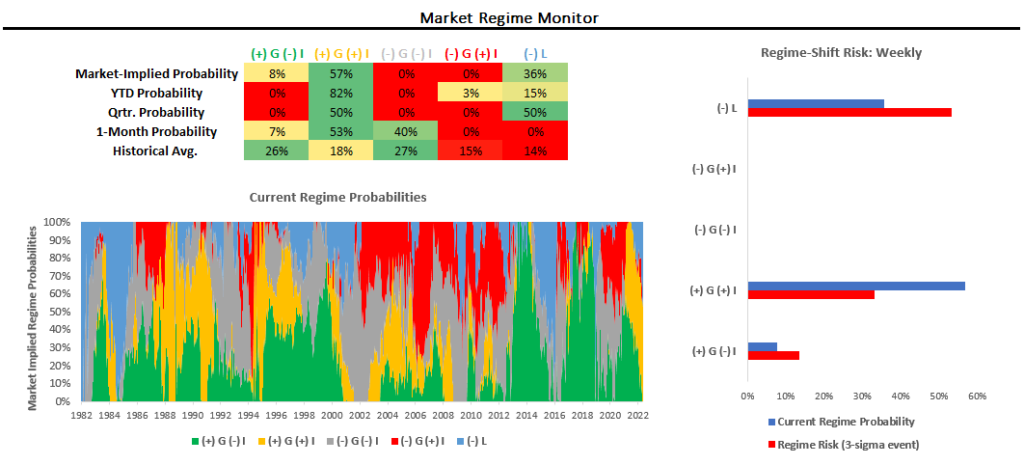

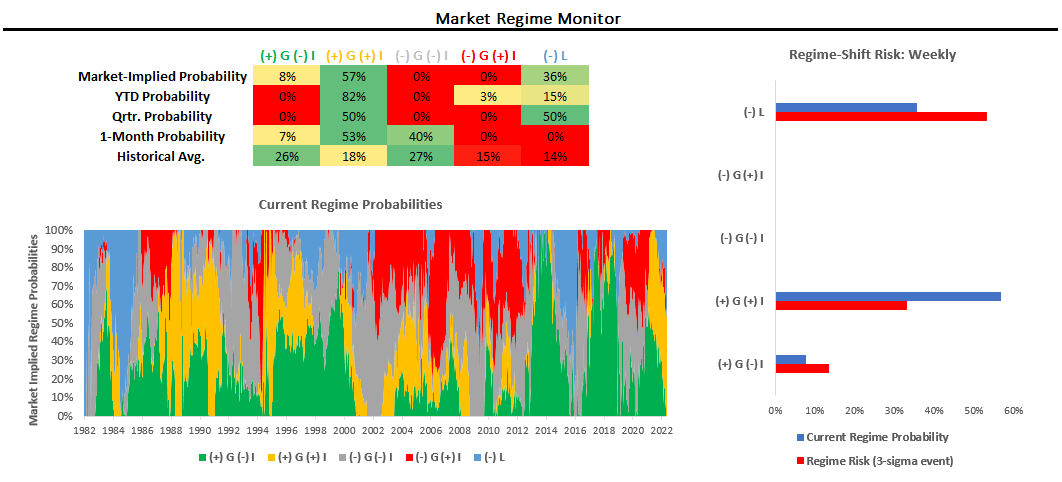

Markets will be closed tomorrow in the US on account of Memorial Day, but we will provide our guidance for the rest of the week. Despite last week’s bounce in equity markets, our systematic process tells us we are in a stagflationary regime that remains unfriendly to both equities. We see in economic data that markets continue to price liquidity tightening and inflationary growth. Below, we show our updated market regime monitor:

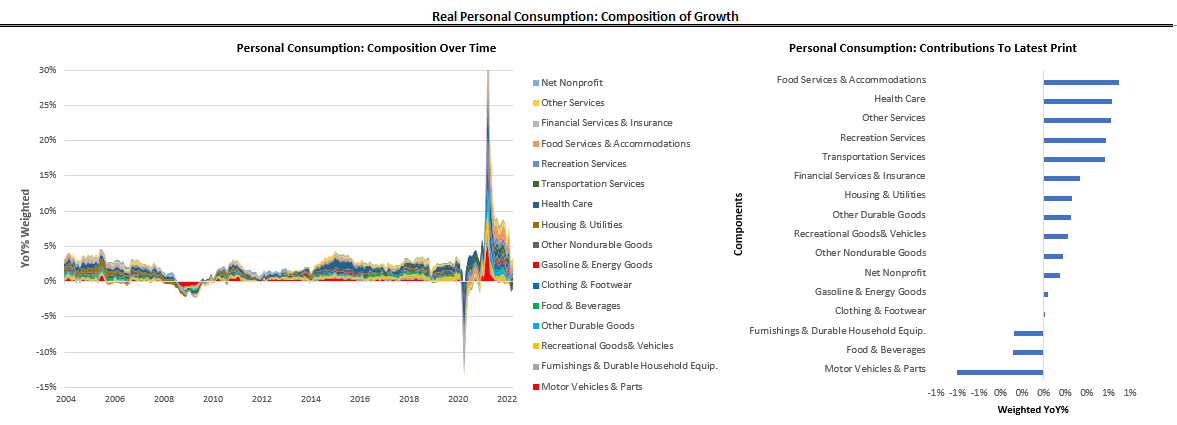

Over the last month, markets have primarily priced (+) G (+) I, i.e., rising nominal growth. Our Market Regime Monitors tell us we are in a (+) G (+) I regime. Regime Risk is currently elevated, with the potential for a shift to (-) L, i.e., tightening liquidity. Over the last week, we have seen some reduction in losses faced by equity markets. Coincident with these moves last week, we have seen a moderation in economic growth data. Notably, we saw strong industrial durable goods orders in consumer spending buck the slowdown trend. We show these below. First, we offer the composition of real personal consumption expenditures:

Real spending came in at 2.78%, a sequential acceleration & surprised expectations with an MoM charge of 0.9% versus expectations of 0.8%. Motor Vehicles & Parts has been the most significant contributor to these moves. Spending nonetheless remains in a downtrend. We continue to see a drawdown in savings rates with incremental incomes going to outlays rather than savings, not painting a picture of excess income growth:

This mix of personal spending resulted in a month-over-month increase in employee compensation; however, proprietors’ incomes declined.

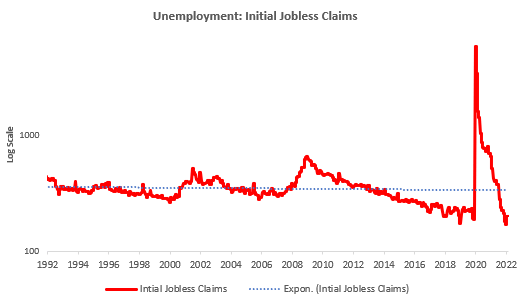

This continued increase in employee compensation is consistent with the elevated levels of employment we are currently witnessing:

Unemployment is broadly below trend. California showed the most significant increase in unemployment claims in the most recent print, while New York led the most significant decrease.

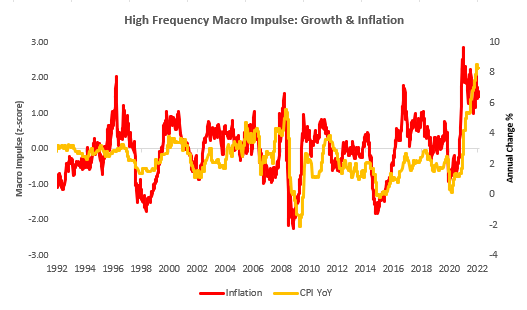

As nominal incomes remain elevated, we see increasing price pressures as commodity, labor, and housing supply remain constrained. Resultantly, inflationary pressures remain in place:

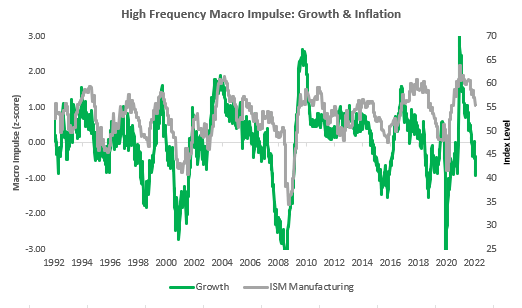

Our High-Frequency Impulse measures of inflation tell us that inflationary pressures slowed modestly last week but remain elevated. Putting these factors together, the environment remains one where the real economic growth impulse remains under pressure. High-Frequency Impulse measures of growth show that the trajectory for economic data is likely lower, with ISM Manufacturing & Services next week likely to come in weaker:

We aren’t in the business of predicting every print of economic data. However, our systems are created to estimate where we are in the economic cycle and to position ourselves optimally within this context. Therefore, while equity markets may have bounced due to technical factors last week, conditions remain unfavorable for exposures that favor rising growth, falling inflation, and abundant liquidity. Other than ISM data next week, here are the data relevant to our systematic tracking of economic activity:

- Monday: Memorial Day Holiday

- Tuesday: Chicago PMI

- Wednesday: Markit Manufacturing PMI, ADP Employment, ISM Manufacturing, JOLTs Job Openings

- Thursday: ADP Employment (May), Initial Claims, Curde Oil Invt, Nonfarm Productivity & Unit Labor Costs, Factory Orders

- Friday: NFP, Unemployment Rates, ISM Non-mfg

With regards to positioning for these moves, our systems continue to tell us that equity shorts remain warranted. Further, market regime dynamics tell us that inflation beneficiaries (TIPS, Gold, Commodities) are all regimes supported by cross-asset trends. Tightening liquidity dynamics favor both the dollar and the long end of the Treasury curve (relative to the short end). Below, we show cumulative performance for our ETF Strategy year-to-date along with the updated asset class exposures:

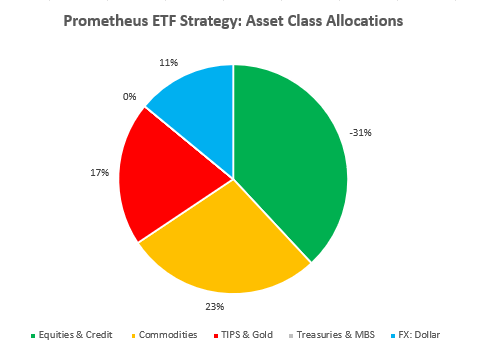

As we mentioned earlier, we suffered losses on our equity shorts this week, however, our signals continue to tell us the current environment doesn’t favor these exposures. At the asset allocation level, here are our current ETF Strategy exposures:

Specifically, the ETFs contained in the current allocation are as follows:

- Stocks: SPY (-5%), XLP (-5%), XLY (-3%), XLC (-5%), XLV (5%), XLB (-5%), XLI (-5%), XLK (-4%), XLF (-4%), XLU (5%), XLE (3%),

- Commodities: DBC (3%), USO (2%), UGA (2%), UNG (2%), CORN(3%), SOYB(4%), CANE(4%), WEAT(2%), GLD (5%)

- Fixed Income: HYG (-12%), TIP (12%)

- Currencies: UUP (12%)

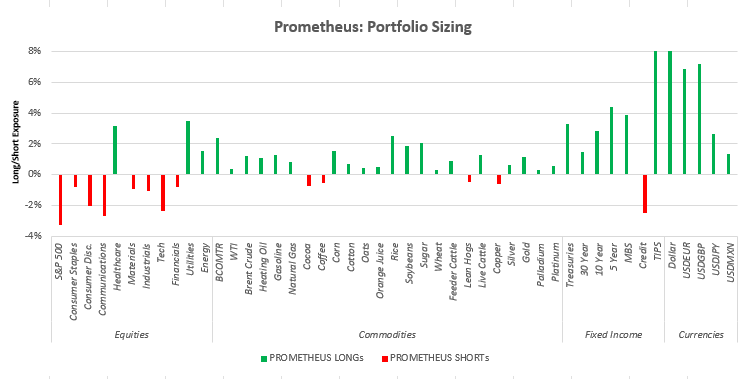

Unliked our ETF Strategy, our Alpha Strategy has added positions to Treasuries due to cross-sectional variation in the opportunity set and the slightly different strategy parameters. Here is how we are looking to set up our Alpha Strategy for next week:

Until next week. Stay nimble!