Last week we saw significant moves in markets. Equities and treasuries were down significantly, while commodities and the dollar rallied. These moves reflect the fundamental dynamics of heightened inflation, weakening growth, tightening liquidity, and market regime pricing for stagflationary nominal growth. These market moves came from weaker than expected employment data and higher-than-expected inflation in the form of CPI. We examine the drivers of asset returns individually:

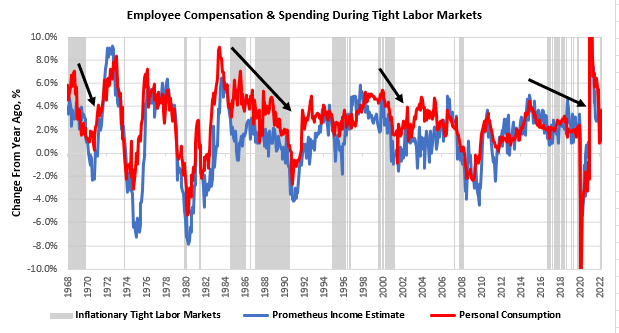

i. Growth remains under pressure. Economic cause-and-effect tell us that there is an increasing likelihood that growth will continue to weaken. Our focus is currently on the US consumer and how they will drive this economic cycle. Consumers spend (thereby creating income) in three ways: they can spend current income, borrow from future incomes, or dig into previously saved income. Current incomes are primarily a function of the number of hours worked, the prevailing rate of wages, and the employment in the labor force. We combine these estimates to get a sense of income-powering spending. We combine these measures with our systematic recognition of periods where labor markets are both tight, and inflation is elevated, i.e., inflationary tight labor markets. We show this below :

When labor markets are tight, employment becomes less of a source of incremental income, as there is less room to reduce unemployment. Furthermore, when inflation is elevated, real wages come under pressure, i.e., consumers have less spending power. Our year-over-year estimates show income declines of -3.1% during inflationary & tight labor markets, and real personal spending typically indicates a -1.8% decline annually. We are experiencing an inflationary, tight labor market, and we expect real incomes and spending to recede.

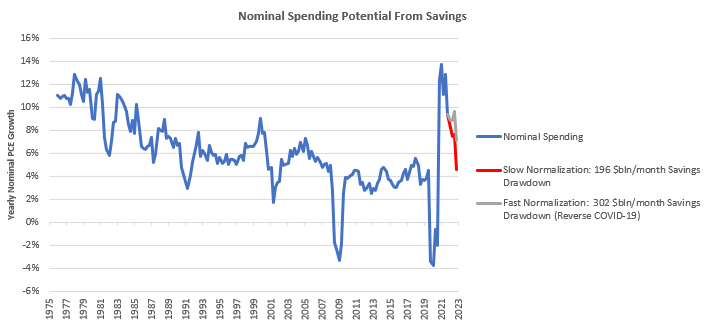

Household cash balances are elevated relative to the last five years. It is often argued that these are the buffer that will continue to support spending in the real economy. While some degree of this is likely, the magnitude of savings drawdown is unlikely to be adequate to offset income losses. Below, we show our estimates for the potential for savings to households to prop up personal spending, i.e., if households choose to reduce their cash balances, how much it would impact spending growth alone. We make room for a fast and slow scenario. In the slow scenario, households reduce their savings in line with historical rates. In the fast scenario, they reverse the uptick in cash balances since COVID-19 over 18 months. We show these below:

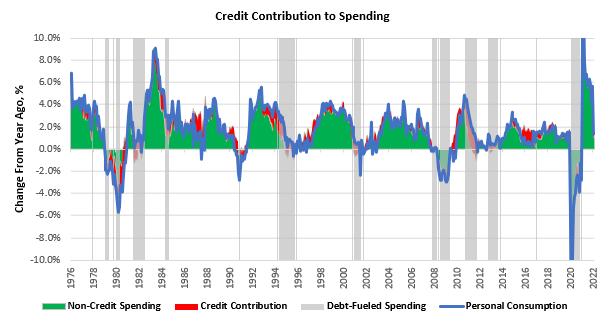

Even at a pace of $302 billion in cash balance drawdown, accumulated savings cannot keep up with the current rate of nominal spending growth. Now that we have covered current and previously saved incomes, we can look at the consumers’ ability to borrow from future income, i.e., credit. We show below how consumer credit growth is not large enough in value to contribute meaningfully to incomes. Furthermore, while credit is an essential feature of the US economy, credit occupying a large share of spending is typically a lagging indicator as it usually occurs during periods where income has contracted considerably. Keep in mind this takes into account only installment credit & not mortgages:

At best, credit could add approximately 0.3% to spending at its current levels. With net worths being impacted by declining asset prices and rising borrowing costs, we find even this to be an optimistic estimate.

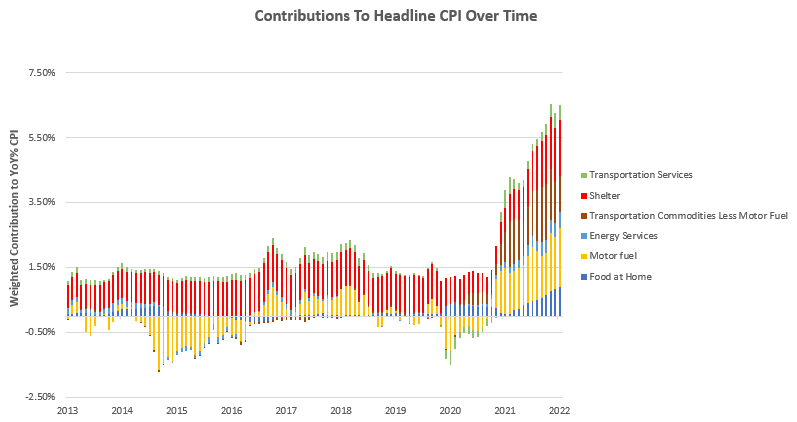

ii. Inflation remains resilient and has spread to areas where price increases tend to be sticky. CPI came in higher than expected, rising at a torrid 1% in May alone, benefitting our systematic exposures greatly. Energy, transportation, home prices, rents, and food prices were the most significant contributors to these moves. We show the top six categories over time below:

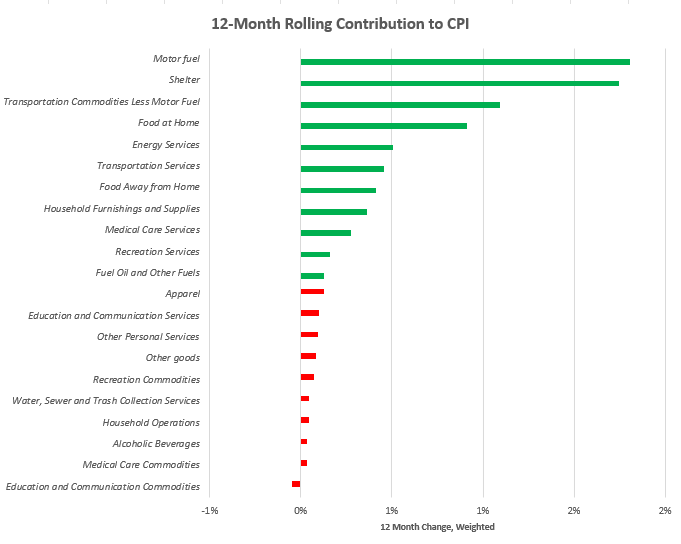

To showcase the contributions to the trends underlying current inflation, we show the contributions to the yearly changes in CPI:

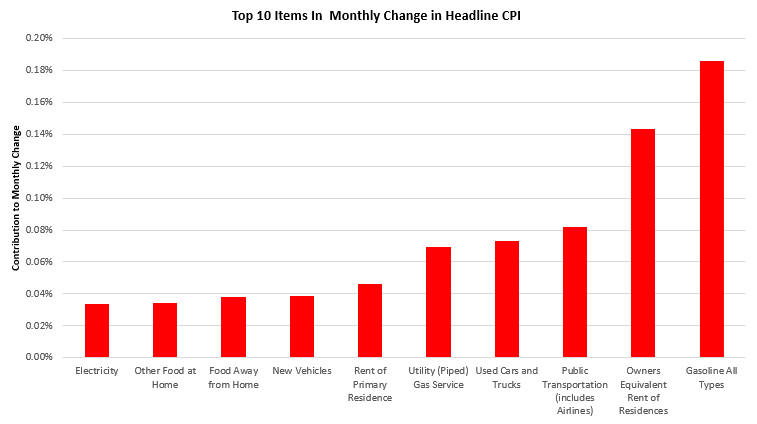

For more specificity, we show the top 10 items that contributed to the current monthly change:

The primary concern we do not feel is adequately appreciated in markets today is that inflationary pressures have spread to items where inflationary tendencies do not revert quickly, i.e., food and housing. With sustained rental inflation, we could see a much higher mean CPI than markets are discounting, which would mean there is significant room for the current downtrend in stocks and treasuries. Our systems tell us to position accordingly, and we continue to short equities and stay long commodities and other inflation beneficiaries.

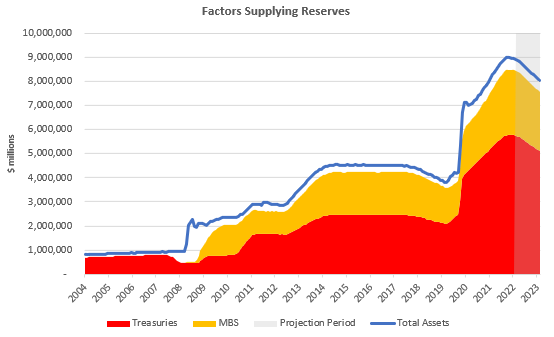

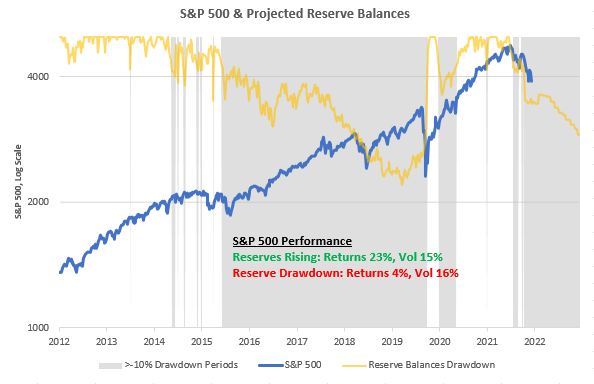

iii. Liquidity has begun to contract quickly and will continue to do so.The majority of the decline in liquidity year-to-date has come due to the pullback in fiscal largess. This month, we will see the initial impacts of the Fed’s balance sheet reduction. We show our forecasts below:

These asset decreases will decrease the reserve balances available to the financial system, decreasing liquidity and increasing volatility. We have long expected the tightening of liquidity conditions to be volatility-inducing and to drag on assets. The reduction of reserve balances (i.e., drawdown) has been true to form in this regard.

We show our projections of reserve balances below as well:

The Week Ahead

Taking all the information above into context, our systems continue to expect an environment of stagflationary nominal growth and weak liquidity. Historically, this has been a poor time for stocks & bonds, and current market trends continue to validate this assessment. In terms of economic data, we will receive a slew of incremental information next week. Furthermore, we will likely receive an additional 50 basis point rate hike on Wednesday at the FOMC meeting. Here are the upcoming data relevant to our systematic process:

-

Monday: NA

-

Tuesday: NFIB Small Business Surveys, PPI

-

Wednesday: FOMC, MBA Mortgage Applications, Empire Manufacturing, Retail Sales, NAHB Housing Index, Trade Prices

-

Thursday: Building Permits, Housing Starts, Philly Fed Business Outlook Survey, Jobless Claims

-

Friday: Industrial Production, Capacity Utilization, Mfg Production, Leading Index

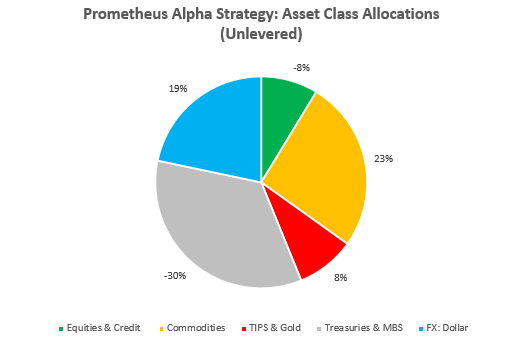

We expect leading growth data like PMIs to paint a weak picture, while production data could continue to come in strong. We will carefully watch housing data to see if there is further deterioration in the housing outlook. In light of these fundamental and market conditions, our systems remain long inflation beneficiaries and short of assets that cannot survive this environment. Below, we show how our Alpha Strategy is positioned at the asset class level:

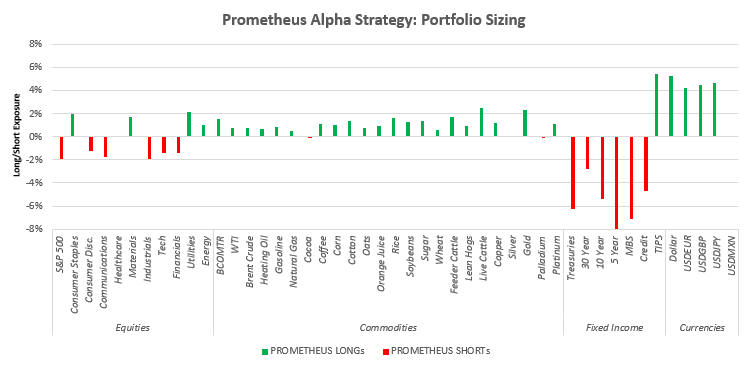

As we can see above, our systems remain aggressively short equities and fixed income while staying long dollars and commodities. Last week was a great week for this approach, and our systems continue to maintain the conviction that the environment has not materially changed yet. We show our exposures for the Alpha Strategies at the asset level below:

We continue to reiterate that this is a time for capital preservation and active shorting. Even if you aren’t generating returns on the short side, not losing money on the long side is also alpha. Stay nimble.

Good day! Do you know if they make any plugins

to help with SEO? I’m trying to get my blog to rank for some targeted keywords

but I’m not seeing very good results. If you know of any please share.

Kudos! You can read similar blog here: Eco product

Be certain that the mattress fits snugly — if you possibly can fit two fingers between the mattress and the side of the crib, your baby’s head might turn out to be wedged there.

After checking out a handful of the blog articles on your website, I honestly like your way of blogging. I added it to my bookmark website list and will be checking back soon. Take a look at my web site too and let me know what you think.

Hello! I could have sworn I’ve visited your blog before but after browsing through many of the posts I realized it’s new to me. Anyways, I’m definitely happy I came across it and I’ll be book-marking it and checking back frequently.

An outstanding share! I’ve just forwarded this onto a coworker who has been conducting a little research on this. And he actually bought me breakfast because I discovered it for him… lol. So allow me to reword this…. Thank YOU for the meal!! But yeah, thanks for spending the time to talk about this topic here on your web page.

I needed to thank you for this excellent read!! I absolutely loved every little bit of it. I have got you bookmarked to look at new things you post…

Oh my goodness! Incredible article dude! Thank you, However I am going through issues with your RSS. I don’t understand why I cannot subscribe to it. Is there anybody getting identical RSS issues? Anybody who knows the answer will you kindly respond? Thanks.

This is a topic that is close to my heart… Many thanks! Where are your contact details though?

There’s definately a great deal to find out about this subject. I really like all of the points you made.

Next time I read a blog, I hope that it does not fail me as much as this one. I mean, Yes, it was my choice to read, but I actually believed you’d have something interesting to say. All I hear is a bunch of whining about something you could possibly fix if you weren’t too busy searching for attention.

Pretty! This has been an incredibly wonderful article. Thank you for providing this info.

Hi, I do think this is a great website. I stumbledupon it 😉 I am going to come back once again since I book-marked it. Money and freedom is the greatest way to change, may you be rich and continue to guide other people.

You’re so interesting! I do not suppose I have read anything like this before. So great to find somebody with genuine thoughts on this topic. Really.. many thanks for starting this up. This site is something that’s needed on the web, someone with some originality.

This is a topic that’s close to my heart… Best wishes! Where can I find the contact details for questions?

Way cool! Some very valid points! I appreciate you penning this write-up and also the rest of the site is really good.

An impressive share! I have just forwarded this onto a co-worker who was conducting a little research on this. And he actually bought me lunch due to the fact that I found it for him… lol. So let me reword this…. Thanks for the meal!! But yeah, thanx for spending some time to discuss this matter here on your website.

I really like it when individuals come together and share ideas. Great site, stick with it.

This is a topic that is close to my heart… Best wishes! Exactly where can I find the contact details for questions?

I seriously love your blog.. Excellent colors & theme. Did you build this amazing site yourself? Please reply back as I’m wanting to create my own website and would love to learn where you got this from or exactly what the theme is named. Kudos.

Nice post. I learn something new and challenging on blogs I stumbleupon everyday. It’s always helpful to read through articles from other writers and use a little something from their sites.

Next time I read a blog, Hopefully it won’t fail me as much as this one. After all, Yes, it was my choice to read, nonetheless I actually thought you’d have something useful to say. All I hear is a bunch of whining about something you can fix if you were not too busy searching for attention.

You made some really good points there. I looked on the net to learn more about the issue and found most people will go along with your views on this site.

Good post. I learn something new and challenging on websites I stumbleupon everyday. It’s always useful to read articles from other authors and practice something from their web sites.

I used to be able to find good advice from your blog articles.

An intriguing discussion is worth comment. I do think that you ought to write more about this issue, it may not be a taboo subject but typically people do not discuss such issues. To the next! Many thanks!

You are so interesting! I do not think I have read through a single thing like that before. So great to find somebody with a few original thoughts on this topic. Seriously.. many thanks for starting this up. This site is something that is required on the web, someone with a little originality.

It’s nearly impossible to find experienced people about this topic, but you seem like you know what you’re talking about! Thanks

Nice post. I learn something new and challenging on blogs I stumbleupon every day. It will always be interesting to read content from other writers and practice a little something from other web sites.

Greetings! Very helpful advice within this post! It’s the little changes that produce the largest changes. Thanks for sharing!

I truly love your site.. Very nice colors & theme. Did you develop this site yourself? Please reply back as I’m looking to create my own personal site and would love to find out where you got this from or just what the theme is called. Cheers!

There’s certainly a lot to learn about this issue. I like all the points you’ve made.

It’s nearly impossible to find well-informed people in this particular subject, but you sound like you know what you’re talking about! Thanks

I truly appreciated this gorgeous blog. Make sure you keep up the good work. Best Regards .

I could not refrain from commenting. Exceptionally well written!

Good post. I learn something totally new and challenging on sites I stumbleupon everyday. It will always be useful to read content from other writers and practice a little something from their sites.

As much as I dislike “Independence Day”, at least you got a good idea of what the aliens looked like in the famous autopsy scene.

Great blog here! Also your website loads up fast! What host are you the usage of? Can I get your affiliate hyperlink for your host? I want my website loaded up as quickly as yours lol.

I really love your website.. Great colors & theme. Did you make this website yourself? Please reply back as I’m hoping to create my own website and would love to learn where you got this from or just what the theme is called. Cheers!

Hey there! I just want to give you a huge thumbs up for your great info you have right here on this post. I’ll be coming back to your site for more soon.

I do agree with all of the ideas you have presented in your post. Theyre really convincing and will definitely work. Still, the posts are too short for beginners. Could you please extend them a bit from next time? Thanks for the post.

I’m amazed, I must say. Rarely do I come across a blog that’s both equally educative and amusing, and without a doubt, you’ve hit the nail on the head. The problem is something that too few people are speaking intelligently about. I’m very happy that I found this during my search for something regarding this.

Hi, I do believe this is an excellent website. I stumbledupon it 😉 I am going to return yet again since I bookmarked it. Money and freedom is the greatest way to change, may you be rich and continue to help other people.

Everybody Hates Chris sometimes bores me because the jokes aren’t so funny anymore but i still watch it all the time,

You have a few helpful ideas! Perhaps I should think of trying to do this myself. Respectfully

The next time I learn a weblog, I hope that it doesnt disappoint me as a lot as this one. I imply, I know it was my option to learn, however I actually thought youd have something interesting to say. All I hear is a bunch of whining about something that you may fix for those who werent too busy in search of attention.

There is definately a lot to know about this issue. I really like all of the points you have made.

After study many of the content with your web site now, we genuinely much like your technique of blogging. I bookmarked it to my bookmark site list and you will be checking back soon. Pls look at my web site likewise and figure out what you consider.

Twitter had a tweet on wholesale designer handbags, and lead me here.

I have noticed that over the course of making a relationship with real estate homeowners, you’ll be able to come to understand that, in every real estate transaction, a commission rate is paid. Finally, FSBO sellers tend not to “save” the commission rate. Rather, they fight to win the commission simply by doing a strong agent’s work. In the process, they shell out their money and time to accomplish, as best they’re able to, the tasks of an realtor. Those duties include revealing the home via marketing, representing the home to all buyers, creating a sense of buyer emergency in order to induce an offer, making arrangement for home inspections, controlling qualification checks with the bank, supervising maintenance, and facilitating the closing of the deal.

my kids really like to play with those assorted pool toys, they specially like pokemon pool toys and stuff like that**

Saved as a favorite, I like your site!

i would love to get some free calendars on the internet, are there are sites or company that gives one?,.

Hey, you used to write wonderful, but the last few posts have been kinda boring¡K I miss your great writings. Past few posts are just a bit out of track! come on!

You are so cool! I do not think I’ve truly read something like that before. So good to find somebody with some unique thoughts on this subject. Seriously.. thank you for starting this up. This website is one thing that is required on the internet, someone with some originality.

Hey very nice site!! Man .. Beautiful .. Amazing .. I’ll bookmark your website and take the feeds also…I’m happy to find numerous useful information here in the post, we need develop more strategies in this regard, thanks for sharing. . . . . .

Thanks for the sensible critique. Me & my neighbor were just preparing to do a little research on this. We got a grab a book from our local library but I think I learned more from this post. I am very glad to see such great info being shared freely out there.

I recognize there exists a great deal of spam on this blog site. Do you need help cleaning them up? I can help among courses!

After I originally commented I appear to have clicked the -Notify me when new comments are added- checkbox and from now on each time a comment is added I receive 4 emails with the same comment. Is there an easy method you can remove me from that service? Thank you.

Howdy! This article couldn’t be written any better! Looking at this post reminds me of my previous roommate! He constantly kept talking about this. I’ll send this article to him. Pretty sure he will have a great read. I appreciate you for sharing!

thank you for sharing – Gulvafslibning | Kurt Gulvmand with us, I think – Gulvafslibning | Kurt Gulvmand truly stands out : D.

Hello there, May I download that snapshot and make use of it on my personal weblog?

After study a number of the blogs in your website now, and that i genuinely like your method of blogging. I bookmarked it to my bookmark web site list and you will be checking back soon. Pls look at my website also and inform me what you believe.

I was able to find good advice from your blog articles.

very nice post, i definitely enjoy this excellent website, continue it

This is a great blog” and i want to visit this every day of the week .

I truly appreciate this post. I¡¦ve been looking everywhere for this! Thank goodness I found it on Bing. You’ve made my day! Thanks again Pristina Travel

Hello There. I found your blog using msn. This is an extremely well written article. I will be sure to bookmark it and return to read more of your useful information. Thanks for the post. I’ll certainly comeback.

You made some decent points there. I looked on the internet for your issue and located most people may go together with together with your web site.

it is wise to choice to select Light Emitting Diode christmas lights becaue they are not fire hazard“

i do not use adbrite because their pay rate is horrendously low compared to say infolinks;

Man that was very entertaining and at the same time informative.`*-”~

Oh my goodness! an amazing article dude. Thanks However I’m experiencing problem with ur rss . Don’t know why Unable to subscribe to it. Is there anybody getting similar rss downside? Anybody who knows kindly respond. Thnkx

Can I just say what a relief to find somebody who genuinely knows what they are discussing online. You certainly understand how to bring a problem to light and make it important. A lot more people should look at this and understand this side of your story. I was surprised you aren’t more popular since you surely have the gift.

Hi, I do believe this is a great site. I stumbledupon it 😉 I may revisit yet again since I saved as a favorite it. Money and freedom is the best way to change, may you be rich and continue to guide other people.

There are some attention-grabbing closing dates on this article however I don’t know if I see all of them middle to heart. There is some validity but I’ll take hold opinion until I look into it further. Good article , thanks and we want more! Added to FeedBurner as nicely

I do consider all of the concepts you’ve introduced on your post. They’re very convincing and will certainly work. Nonetheless, the posts are too short for starters. Could you please lengthen them a bit from next time? Thanks for the post. Pristina Hotels

there are lots of exercise guides on the internet but some of them are not scientifically proven and just assumptions;;

I like it whenever people get together and share opinions. Great site, stick with it.

You really make it seem so easy with your presentation but I find this topic to be really something that I think I would never understand. It seems too complex and extremely broad for me. I’m looking forward for your next post, I’ll try to get the hang of it!

Hello! I just wanted to ask if you ever have any issues with hackers? My last blog (wordpress) was hacked and I ended up losing several weeks of hard work due to no back up. Do you have any methods to stop hackers?

It’s onerous to seek out knowledgeable folks on this subject, but you sound like you already know what you’re talking about! Thanks

I just put the link of your blog on my Facebook Wall. very nice blog indeed.~,~,*

it does not take too long to learn good piano playing if you have a good piano lesson*

I enjoy what you guys tend to be up too. This kind of clever work and reporting! Keep up the great works guys I’ve added you guys to blogroll.

bookmarked!!, I really like your web site!

One more important issue is that if you are a mature person, travel insurance for pensioners is something you need to really look at. The more mature you are, a lot more at risk you’re for getting something bad happen to you while abroad. If you are not necessarily covered by some comprehensive insurance coverage, you could have quite a few serious challenges. Thanks for discussing your good tips on this web site.

You’re so interesting! I don’t believe I have read through anything like that before. So great to discover someone with a few unique thoughts on this subject. Really.. many thanks for starting this up. This site is one thing that is needed on the web, someone with a bit of originality.

An impressive share! I’ve just forwarded this onto a co-worker who had been doing a little research on this. And he actually ordered me breakfast simply because I discovered it for him… lol. So allow me to reword this…. Thanks for the meal!! But yeah, thanks for spending the time to discuss this topic here on your website.

Hello there! This article couldn’t be written much better! Reading through this post reminds me of my previous roommate! He continually kept talking about this. I am going to send this post to him. Pretty sure he will have a great read. I appreciate you for sharing!

This site certainly has all of the information and facts I needed concerning this subject and didn’t know who to ask.

You made some really good points there. I looked on the internet to find out more about the issue and found most people will go along with your views on this site.

I know which Sage will not be upsetting demise with the appearance, and thus concerns about his or her country’s will fall.

I am glad that I noticed this site , just the right information that I was looking for! .

I’m really enjoying the theme/design of your website. Do you ever run into any browser compatibility issues? A couple of my blog audience have complained about my blog not working correctly in Explorer but looks great in Safari. Do you have any suggestions to help fix this issue?

A fascinating discussion is definitely worth comment. I believe that you need to write more on this subject matter, it might not be a taboo subject but usually folks don’t talk about such subjects. To the next! All the best.

After study few of the articles on your blog nowadays, and i love your method of blogging. I tag it to my favorites net web site list and will be checking back soon. Please visit my web site too and let me recognize your thought.

Vi ringrazio, ho trovato che quanto scritto non sia completamente corretto

When visiting blogs, i always look for a very nice content like yours .

This web site truly has all of the info I wanted about this subject and didn’t know who to ask.

Oh my goodness! Impressive article dude! Many thanks, However I am having troubles with your RSS. I don’t understand why I am unable to subscribe to it. Is there anyone else having the same RSS problems? Anyone that knows the solution can you kindly respond? Thanx.

Greetings, There’s no doubt that your site might be having internet browser compatibility problems. Whenever I look at your web site in Safari, it looks fine but when opening in I.E., it has some overlapping issues. I simply wanted to provide you with a quick heads up! Other than that, excellent website.

Howdy! This post couldn’t be written much better! Looking at this post reminds me of my previous roommate! He constantly kept preaching about this. I most certainly will forward this post to him. Pretty sure he will have a great read. Thanks for sharing!

Blaine is not the best magician but i can say that he has great showmanship and i like his show.

I truly wanted to jot down a brief remark to be able to express gratitude to you for all of the splendid items you are posting here. My incredibly long internet investigation has at the end been compensated with reasonable points to exchange with my colleagues. I would tell you that many of us readers actually are undeniably lucky to exist in a remarkable site with many perfect individuals with very helpful tips. I feel really grateful to have used your entire web site and look forward to some more excellent minutes reading here. Thank you again for a lot of things.

bookmarked!!, I like your website!

I and my buddies were analyzing the nice information found on your site while at once came up with an awful feeling I never thanked you for those techniques. Those boys were as a result glad to see them and have in effect in actuality been tapping into them. Many thanks for getting simply considerate as well as for opting for this form of impressive issues millions of individuals are really desperate to be aware of. My honest regret for not expressing appreciation to sooner.

Play Black Ops Zombies… […]Call of Duty Black Ops zombie mode has been played by millions of gamers…[…]…

I was able to find good advice from your content.

I am curious to find out what blog system you have been using? I’m having some minor security problems with my latest site and I’d like to find something more safeguarded. Do you have any recommendations?

I will immediately snatch your rss feed as I can not in finding your email subscription link or e-newsletter service. Do you’ve any? Kindly allow me recognise so that I may subscribe. Thanks.

May I simply just say what a relief to uncover someone who genuinely understands what they’re talking about online. You definitely know how to bring a problem to light and make it important. A lot more people really need to check this out and understand this side of the story. I can’t believe you’re not more popular since you surely have the gift.

This is a topic that is close to my heart… Many thanks! Where can I find the contact details for questions?

You made some really good points there. I checked on the internet to learn more about the issue and found most people will go along with your views on this site.

I used to be able to find good info from your blog articles.

Your style is so unique compared to other people I have read stuff from. Thanks for posting when you’ve got the opportunity, Guess I will just book mark this site.

Hello there! I could have sworn I’ve visited your blog before but after looking at some of the articles I realized it’s new to me. Regardless, I’m certainly delighted I found it and I’ll be book-marking it and checking back often!

Pretty! This has been an extremely wonderful article. Thank you for providing this information.

I couldn’t refrain from commenting. Exceptionally well written!

It’s difficult to find experienced people in this particular topic, but you sound like you know what you’re talking about! Thanks

There’s certainly a great deal to find out about this issue. I love all of the points you’ve made.

Hi! I could have sworn I’ve been to this blog before but after going through many of the articles I realized it’s new to me. Nonetheless, I’m certainly delighted I stumbled upon it and I’ll be book-marking it and checking back frequently!

I need to to thank you for this wonderful read!! I absolutely loved every bit of it. I’ve got you book marked to check out new stuff you post…

Good post. I learn something new and challenging on sites I stumbleupon every day. It will always be exciting to read through content from other writers and use something from their websites.

Hello, I think your blog may be having browser compatibility problems. Whenever I take a look at your web site in Safari, it looks fine however when opening in I.E., it’s got some overlapping issues. I merely wanted to give you a quick heads up! Besides that, fantastic website.

Next time I read a blog, Hopefully it does not fail me just as much as this particular one. I mean, I know it was my choice to read, but I really believed you would have something useful to talk about. All I hear is a bunch of moaning about something you could possibly fix if you weren’t too busy seeking attention.

Having read this I believed it was rather informative. I appreciate you finding the time and energy to put this content together. I once again find myself spending a lot of time both reading and commenting. But so what, it was still worthwhile!

Your style is so unique in comparison to other people I’ve read stuff from. I appreciate you for posting when you have the opportunity, Guess I will just bookmark this web site.

Excellent article. I absolutely appreciate this site. Continue the good work!

I like it when individuals come together and share views. Great blog, keep it up!

I need to to thank you for this very good read!! I certainly loved every bit of it. I’ve got you book-marked to look at new stuff you post…

There is definately a lot to find out about this topic. I like all the points you’ve made.

After going over a number of the blog posts on your site, I truly like your technique of blogging. I saved it to my bookmark webpage list and will be checking back soon. Please visit my website too and let me know what you think.

I wanted to thank you for this great read!! I absolutely enjoyed every bit of it. I have you book marked to look at new stuff you post…

Aw, this was a really good post. Finding the time and actual effort to make a great article… but what can I say… I put things off a lot and don’t seem to get nearly anything done.

Very good article. I absolutely appreciate this website. Continue the good work!

Very nice article. I certainly appreciate this site. Thanks!

Hey there! I just wish to offer you a huge thumbs up for your great information you have here on this post. I am coming back to your website for more soon.

Having read this I believed it was really informative. I appreciate you taking the time and effort to put this article together. I once again find myself personally spending way too much time both reading and posting comments. But so what, it was still worthwhile.

I’m amazed, I have to admit. Seldom do I encounter a blog that’s both educative and amusing, and without a doubt, you’ve hit the nail on the head. The issue is something which too few people are speaking intelligently about. Now i’m very happy I found this in my hunt for something concerning this.

Way cool! Some extremely valid points! I appreciate you writing this article and the rest of the website is very good.

You have made some good points there. I looked on the net to find out more about the issue and found most people will go along with your views on this web site.

There’s definately a lot to know about this subject. I really like all of the points you’ve made.

When I initially left a comment I appear to have clicked on the -Notify me when new comments are added- checkbox and from now on each time a comment is added I recieve four emails with the same comment. There has to be a way you are able to remove me from that service? Kudos.

Having read this I thought it was very informative. I appreciate you taking the time and effort to put this information together. I once again find myself personally spending a lot of time both reading and leaving comments. But so what, it was still worthwhile!

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%ED%9B%84-%EA%B4%91%EA%B3%A0-%EA%B4%80%EB%A6%AC%EC%97%90-%ED%99%9C%EC%9A%A9%ED%95%98%EB%8A%94-%EB%B0%A9%EB%B2%95-6a822042a160

https://naveridbuy.blogspot.com/2024/12/blog-post_52.html

https://witty-apple-dd3cm1.mystrikingly.com/blog/bf0bc875058

https://ocher-cat-dd3cmm.mystrikingly.com/blog/642842abd0f

https://ko.anotepad.com/note/read/wyj88hps

https://sociable-corn-dd3cmt.mystrikingly.com/blog/4997451cd2d

https://diplomatic-shrimp-dbgzh2.mystrikingly.com/blog/079e4cac293

https://naveridbuy.blogspot.com/2024/11/5_28.html

You’ve made some decent points there. I checked on the web for additional information about the issue and found most people will go along with your views on this site.

https://xn--w6-hd0j99gyns5z0qeiim2i.mystrikingly.com/blog/f33715c06a4

https://maize-wombat-dd3cms.mystrikingly.com/blog/869d7ae7ea5

You’ve made some good points there. I checked on the net to find out more about the issue and found most individuals will go along with your views on this web site.

Very nice write-up. I certainly love this site. Keep writing!

https://medium.com/@charlielevesque328/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EC%98%A8%EB%9D%BC%EC%9D%B8-%EA%B5%AC%EB%A7%A4-%ED%9B%84%EA%B8%B0%EC%99%80-%EC%A3%BC%EC%9D%98%ED%95%B4%EC%95%BC-%ED%95%A0-%EC%A0%90%EB%93%A4-4a51bcd6c007

https://ko.anotepad.com/note/read/mfwncatr

Everyone loves it whenever people come together and share ideas. Great website, stick with it!

https://candid-lion-dd3cm3.mystrikingly.com/blog/8c25ae9d7a9

https://witty-apple-dd3cm1.mystrikingly.com/blog/6e9742ef068

https://naveridbuy.blogspot.com/2024/12/blog-post_19.html

https://naveridbuy.exblog.jp/37090971/

Everything is very open with a clear clarification of the challenges. It was definitely informative. Your site is extremely helpful. Thanks for sharing.

https://naveridbuy.blogspot.com/2024/11/top-5.html

https://witty-apple-dd3cm1.mystrikingly.com/blog/6e9742ef068

https://adaptable-camellia-dd3cm4.mystrikingly.com/blog/79c90dfb696

https://naveridbuy.exblog.jp/37091141/

https://naveridbuy.exblog.jp/37152070/

https://inky-owl-dd3cmv.mystrikingly.com/blog/f111c3c7d0d

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94%EA%B0%80-%ED%95%84%EC%9A%94%ED%95%A0-%EB%95%8C-%EA%B5%AC%EB%A7%A4%EA%B0%80-%EB%8B%B5%EC%9D%BC%EA%B9%8C-4bbacce4d7df

https://candid-lion-dd3cm3.mystrikingly.com/blog/8c25ae9d7a9

https://candid-lion-dd3cm3.mystrikingly.com/blog/2024

Spot on with this write-up, I really feel this amazing site needs a lot more attention. I’ll probably be back again to read through more, thanks for the advice!

https://maize-wombat-dd3cms.mystrikingly.com/blog/90c3ba770c0

https://writeablog.net/cxt2qn6408

https://telegra.ph/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4-%EC%8B%9C-%ED%95%84%EC%88%98-%EC%B2%B4%ED%81%AC%EB%A6%AC%EC%8A%A4%ED%8A%B8-10-10

Having read this I believed it was extremely informative. I appreciate you taking the time and energy to put this information together. I once again find myself spending a significant amount of time both reading and leaving comments. But so what, it was still worth it!

https://telegra.ph/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4%EB%A5%BC-%EC%9C%84%ED%95%9C-%EC%A0%84%EB%AC%B8%EA%B0%80%EC%9D%98-%EC%A1%B0%EC%96%B8-09-26

https://medium.com/@1kelly76/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4-%ED%9B%84-%EB%B6%80%EC%9E%91%EC%9A%A9-%EB%8C%80%EC%B2%98%EB%B2%95-52675767f799

https://naveridbuy.blogspot.com/2024/11/blog-post_50.html

https://naveridbuy.blogspot.com/2024/11/blog-post_95.html

https://naveridbuy.blogspot.com/2024/11/2024.html

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EB%B9%84%EB%B0%80%EB%B2%88%ED%98%B8-%EB%B3%B5%EA%B5%AC%ED%95%98%EB%8A%94-5%EA%B0%80%EC%A7%80-%EB%B0%A9%EB%B2%95-216aafd6cf7c

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%B9%B4%ED%8E%98-%EC%9A%B4%EC%98%81%EC%9D%84-%EC%9C%84%ED%95%9C-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%ED%8C%81-eb39c3e24984

https://candid-lion-dd3cm3.mystrikingly.com/blog/5037f72f44c

https://telegra.ph/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EC%97%86%EC%9D%B4-%EC%84%9C%EB%B9%84%EC%8A%A4-%EC%9D%B4%EC%9A%A9%ED%95%98%EB%8A%94-%ED%8C%81-12-13

https://candid-lion-dd3cm3.mystrikingly.com/blog/8085327d927

https://naveridbuy.blogspot.com/2024/11/blog-post_7.html

https://medium.com/@carlfrancoh38793/%EC%95%84%EC%9D%B4%EB%94%94-%EC%83%9D%EC%84%B1-%EC%96%B4%EB%A0%A4%EC%9A%B8-%EB%95%8C-%EA%B5%AC%EB%A7%A4-%EB%8C%80%EC%95%88-%EC%95%8C%EC%95%84%EB%B3%B4%EA%B8%B0-62055e09b46c

https://writeablog.net/jr525di7pj

https://medium.com/@charlielevesque328/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%ED%9A%A8%EA%B3%BC%EC%99%80-%EA%B5%AC%EB%A7%A4-%EC%8B%9C-%EC%A3%BC%EC%9D%98%EC%82%AC%ED%95%AD-%EC%B4%9D%EC%A0%95%EB%A6%AC-165d650962af

https://medium.com/@carlfrancoh38793/%EA%B5%AC%EA%B8%80-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%EC%9D%B4%EC%A0%90%EA%B3%BC-%EB%8B%A8%EC%A0%90%EC%9D%80-%EB%AC%B4%EC%97%87%EC%9D%B8%EA%B0%80%EC%9A%94-4dccd7ee3fc1

https://medium.com/@nsw5288/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EC%98%A8%EB%9D%BC%EC%9D%B8-%EC%B2%98%EB%B0%A9-abaaad6ae4b4

https://naveridbuy.blogspot.com/2024/12/blog-post_52.html

https://naveridbuy.blogspot.com/2024/12/blog-post_82.html

https://naveridbuy.exblog.jp/37152100/

https://writeablog.net/mzlw3kmb0y

https://naveridbuy.blogspot.com/2024/12/blog-post_31.html

https://salmon-peach-dd3cm8.mystrikingly.com/blog/dbd2b0155cb

https://writeablog.net/cxt2qn6408

https://golden-grape-dd3cml.mystrikingly.com/blog/4644761650e

https://maize-wombat-dd3cms.mystrikingly.com/blog/dad3e41e83f

https://viastoer.blogspot.com/2024/09/blog-post_82.html

https://ko.anotepad.com/note/read/hi75snr3

Great post. I’m facing many of these issues as well..

https://hallbook.com.br/blogs/376901/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B1%B0%EB%9E%98%EB%8A%94-%EC%95%88%EC%A0%84%ED%95%9C%EA%B0%80-%EC%A0%84%EB%AC%B8%EA%B0%80%EC%9D%98-%EC%A1%B0%EC%96%B8

https://naveridbuy.exblog.jp/37152158/

https://medium.com/@nsw5288/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4-%EB%B0%A9%EB%B2%95%EA%B3%BC-%ED%9A%A8%EA%B3%BC%EC%A0%81%EC%9D%B8-%EC%82%AC%EC%9A%A9%EB%B2%95-71efc491ca1b

https://naveridbuy.exblog.jp/37152120/

https://witty-apple-dd3cm1.mystrikingly.com/blog/6e9742ef068

https://gajweor.pixnet.net/blog/post/162189334

https://xn--w2-hd0j99gyns5z0qeiim2i.mystrikingly.com/blog/f803065301b

https://telegra.ph/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC%EB%A5%BC-%EC%B2%98%EC%9D%8C-%EC%8B%9C%EB%8F%84%ED%95%98%EB%8A%94-%EB%B6%84%EB%93%A4%EC%9D%84-%EC%9C%84%ED%95%9C-%EA%B0%80%EC%9D%B4%EB%93%9C-09-12

https://naveridbuy.blogspot.com/2024/12/blog-post_52.html

https://naveridbuy.blogspot.com/2024/12/blog-post_29.html

https://azure-elk-dbgzhz.mystrikingly.com/blog/59835514c6a

https://telegra.ph/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4-%EA%B0%80%EC%9D%B4%EB%93%9C-%EC%95%88%EC%A0%84%ED%95%98%EA%B3%A0-%EC%A0%80%EB%A0%B4%ED%95%98%EA%B2%8C-%EA%B5%AC%EB%A7%A4%ED%95%98%EB%8A%94-%EB%B0%A9%EB%B2%95-09-26

https://medium.com/@carlfrancoh38793/%EC%A4%91%EA%B3%A0-%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94%EB%A5%BC-%ED%9A%A8%EA%B3%BC%EC%A0%81%EC%9C%BC%EB%A1%9C-%ED%99%9C%EC%9A%A9%ED%95%98%EB%8A%94-%EB%B0%A9%EB%B2%95-a5bd35053073

https://writeablog.net/qmceliv4q8

https://inky-owl-dd3cmv.mystrikingly.com/blog/570378fab9f

After going over a few of the blog posts on your site, I seriously like your technique of blogging. I saved it to my bookmark site list and will be checking back in the near future. Please check out my web site too and tell me your opinion.

https://naveridbuy.blogspot.com/2024/11/5_28.html

https://naveridbuy.blogspot.com/2024/11/blog-post_28.html

https://medium.com/@nsw5288/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4-%ED%9B%84%EA%B8%B0-%EB%AA%A8%EC%9D%8C-%EC%8B%A0%EB%A2%B0%ED%95%A0-%EC%88%98-%EC%9E%88%EC%9D%84%EA%B9%8C-5dc2946813fc

https://writeablog.net/mqcuo9vdox

https://naveridbuy.exblog.jp/35659120/

https://inky-owl-dd3cmv.mystrikingly.com/blog/8b5f29aef6c

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EC%A0%95%EB%A7%90-%ED%95%84%EC%9A%94%ED%95%9C%EA%B0%80-%EA%B5%AC%EB%A7%A4-%EC%9D%B4%EC%9C%A0-10%EA%B0%80%EC%A7%80-551cc5f335a5

https://adaptable-camellia-dd3cm4.mystrikingly.com/blog/70aed56e7e8

https://hallbook.com.br/blogs/300792/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B0%80%EA%B2%A9-%EB%B9%84%EA%B5%90-%EC%A0%80%EB%A0%B4%ED%95%98%EA%B2%8C-%EA%B5%AC%EB%A7%A4%ED%95%98%EB%8A%94-%ED%8C%81

https://humorous-lemon-dbgzhk.mystrikingly.com/blog/8329e7be5a2

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EC%97%B0%EB%8F%99%ED%95%9C-%EB%8B%A4%EB%A5%B8-%EC%84%9C%EB%B9%84%EC%8A%A4-%ED%99%9C%EC%9A%A9%EB%B2%95-5dde0d66c6f6

https://xn--w7-hd0jg6f81lm0dhhw74c.mystrikingly.com/blog/8c2d2ec4d69

https://medium.com/@nsw5288/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC%EB%A5%BC-%EC%A0%80%EB%A0%B4%ED%95%98%EA%B2%8C-%EA%B5%AC%EB%A7%A4%ED%95%98%EB%8A%94-%EB%B2%95-%EA%B0%80%EA%B2%A9-%EC%A0%88%EA%B0%90-%ED%8C%81-0d6cba0d9d92

https://naveridbuy.blogspot.com/2024/11/blog-post_7.html

https://candid-lion-dd3cm3.mystrikingly.com/blog/53469580831

That is a very good tip particularly to those new to the blogosphere. Short but very accurate info… Many thanks for sharing this one. A must read post.

https://medium.com/@nsw5288/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4-%EC%82%AC%EC%9D%B4%ED%8A%B8-be7ed9932b6f

https://ko.anotepad.com/note/read/pymsgn44

https://naveridbuy.exblog.jp/37091323/

https://medium.com/@carlfrancoh38793/%EA%B5%AC%EA%B8%80-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%EC%9D%B4%EC%A0%90%EA%B3%BC-%EB%8B%A8%EC%A0%90%EC%9D%80-%EB%AC%B4%EC%97%87%EC%9D%B8%EA%B0%80%EC%9A%94-4dccd7ee3fc1

https://telegra.ph/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B1%B0%EB%9E%98%EB%8A%94-%EC%95%88%EC%A0%84%ED%95%9C%EA%B0%80-%EC%A0%84%EB%AC%B8%EA%B0%80%EC%9D%98-%EC%A1%B0%EC%96%B8-12-13-2

https://gajweor.pixnet.net/blog/post/162874531

Having read this I thought it was very informative. I appreciate you finding the time and energy to put this informative article together. I once again find myself spending way too much time both reading and posting comments. But so what, it was still worthwhile!

https://gajweor.pixnet.net/blog/post/162189334

https://loyal-giraffe-dbgzh9.mystrikingly.com/blog/324f4b43b02

https://writeablog.net/nujuali38e

https://writeablog.net/z3f3wqgycr

You’re so awesome! I do not suppose I’ve read something like that before. So nice to discover another person with a few original thoughts on this issue. Really.. thank you for starting this up. This site is something that is needed on the web, someone with a bit of originality.

https://candid-lion-dd3cm3.mystrikingly.com/blog/2024

https://naveridbuy.blogspot.com/2024/11/blog-post_50.html

https://naveridbuy.blogspot.com/2024/11/blog-post_58.html

https://ko.anotepad.com/note/read/hfewbt6j

https://gajweor.pixnet.net/blog/post/162874321

Hello there! This article could not be written much better! Going through this article reminds me of my previous roommate! He continually kept talking about this. I am going to send this information to him. Pretty sure he will have a very good read. Thanks for sharing!

https://naveridbuy.blogspot.com/2024/11/blog-post_3.html

https://candid-lion-dd3cm3.mystrikingly.com/blog/53469580831

https://witty-apple-dd3cm1.mystrikingly.com/blog/5dbde675bb4

https://inky-owl-dd3cmv.mystrikingly.com/blog/8b5f29aef6c

https://candid-lion-dd3cm3.mystrikingly.com/blog/8085327d927

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94%EC%99%80-%EA%B4%80%EB%A0%A8%EB%90%9C-%EC%B5%9C%EC%8B%A0-%EB%B3%B4%EC%95%88-%EC%9D%B4%EC%8A%88-4569786b88d3

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%ED%9B%84-%EA%B3%84%EC%A0%95-%EB%B3%B4%ED%98%B8-%EB%B0%A9%EB%B2%95-%EC%99%84%EB%B2%BD-%EC%A0%95%EB%A6%AC-ab3a80545ed1

https://naveridbuy.exblog.jp/35878161/

https://witty-apple-dd3cm1.mystrikingly.com/blog/55463079550

https://naveridbuy.blogspot.com/2024/11/blog-post_95.html

Greetings, I believe your blog could be having web browser compatibility problems. Whenever I look at your website in Safari, it looks fine however, if opening in Internet Explorer, it has some overlapping issues. I simply wanted to provide you with a quick heads up! Aside from that, great website!

https://vermilion-elephant-dd3cm3.mystrikingly.com/blog/5bbbfba035e

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%B9%B4%ED%8E%98-%EC%9A%B4%EC%98%81%EC%9D%84-%EC%9C%84%ED%95%9C-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%ED%8C%81-eb39c3e24984

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%ED%9B%84-%EC%8A%A4%EB%A7%88%ED%8A%B8%EC%8A%A4%ED%86%A0%EC%96%B4-%ED%99%9C%EC%9A%A9%EB%B2%95-2d79dbaf8605

https://inky-owl-dd3cmv.mystrikingly.com/blog/481bc4e3083

https://naveridbuy.blogspot.com/2024/11/blog-post_3.html

https://candid-lion-dd3cm3.mystrikingly.com/blog/8085327d927

https://wise-onion-dbgzh0.mystrikingly.com/blog/ca930eb2678

https://candid-dinosaur-dbgzhv.mystrikingly.com/blog/5

https://candid-lion-dd3cm3.mystrikingly.com/blog/b99e214c11a

Aw, this was an incredibly good post. Spending some time and actual effort to produce a very good article… but what can I say… I put things off a lot and never manage to get nearly anything done.

https://candid-lion-dd3cm3.mystrikingly.com/blog/7114981bc76

https://ko.anotepad.com/note/read/pymsgn44

https://gold-gull-dd3cmf.mystrikingly.com/blog/fa06ca9b8e6

I?¦ve recently started a blog, the info you offer on this website has helped me greatly. Thanks for all of your time & work.

https://maize-wombat-dd3cms.mystrikingly.com/blog/b957b6440d6

https://turquoise-dove-dd3cmd.mystrikingly.com/blog/11fff6361ff

https://naveridbuy.exblog.jp/35891793/

https://xn--w0-hs1izvv81cmb366re3s.mystrikingly.com/blog/2e7803c75a6

https://mustard-yucca-dbgzh7.mystrikingly.com/blog/d934217294a

https://writeablog.net/nujuali38e

https://gajweor.pixnet.net/blog/post/162874321

https://writeablog.net/vh97m08dqv

https://medium.com/@nsw5288/%EC%B2%98%EB%B0%A9%EC%A0%84-%EC%97%86%EC%9D%B4-%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4-%EC%9C%84%ED%97%98%EC%84%B1%EA%B3%BC-%ED%95%A9%EB%B2%95%EC%84%B1-3bf901b3695b

https://xn--w3-hd0jg6f81lm0dhhw74c.mystrikingly.com/blog/633b5d0c891

That is a great tip particularly to those fresh to the blogosphere. Short but very precise info… Thanks for sharing this one. A must read article!

https://adaptable-camellia-dd3cm4.mystrikingly.com/blog/79c90dfb696

https://naveridbuy.blogspot.com/2024/11/blog-post_3.html

https://naveridbuy.blogspot.com/2024/11/2024.html

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%EA%B3%BC%EC%97%B0-%EB%8F%88%EA%B0%92%EC%9D%84-%ED%95%A0%EA%B9%8C-d89a0fd7d3c4

https://hallbook.com.br/blogs/376908/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%EB%8C%80%EC%8B%A0-%EC%82%AC%EC%9A%A9%ED%95%A0-%EC%88%98-%EC%9E%88%EB%8A%94-%EB%B0%A9%EB%B2%95%EB%93%A4

An outstanding share! I’ve just forwarded this onto a co-worker who was conducting a little homework on this. And he actually ordered me lunch due to the fact that I found it for him… lol. So let me reword this…. Thank YOU for the meal!! But yeah, thanx for spending some time to discuss this matter here on your website.

https://umber-iris-dd3cm2.mystrikingly.com/blog/5d5639e3317

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%ED%95%A9%EB%B2%95%EC%9D%B8%EA%B0%80%EC%9A%94-%EC%95%8C%EC%95%84%EB%B4%85%EC%8B%9C%EB%8B%A4-40dff2b624f5

https://naveridbuy.blogspot.com/2024/12/blog-post_70.html

https://naveridbuy.exblog.jp/37152083/

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94%EA%B0%80-%ED%95%84%EC%9A%94%ED%95%A0-%EB%95%8C-%EA%B5%AC%EB%A7%A4%EA%B0%80-%EB%8B%B5%EC%9D%BC%EA%B9%8C-4bbacce4d7df

https://adaptable-goat-dd3cmf.mystrikingly.com/blog/2a7fa1850fe

https://candid-lion-dd3cm3.mystrikingly.com/blog/8085327d927

https://naveridbuy.exblog.jp/37152138/

https://candid-lion-dd3cm3.mystrikingly.com/blog/7114981bc76

An impressive share! I’ve just forwarded this onto a coworker who has been doing a little homework on this. And he in fact bought me breakfast due to the fact that I stumbled upon it for him… lol. So allow me to reword this…. Thank YOU for the meal!! But yeah, thanks for spending time to discuss this topic here on your internet site.

https://writeablog.net/ep887shpzn

I’m amazed, I must say. Rarely do I encounter a blog that’s equally educative and engaging, and without a doubt, you’ve hit the nail on the head. The problem is something too few folks are speaking intelligently about. I am very happy I came across this in my hunt for something relating to this.

https://adaptable-goat-dd3cmf.mystrikingly.com/blog/a69238eac25

https://gold-gull-dd3cmf.mystrikingly.com/blog/dc52558c085

https://candid-lion-dd3cm3.mystrikingly.com/blog/7114981bc76

https://medium.com/@carlfrancoh38793/%EB%B9%A0%EB%A5%B4%EA%B2%8C-%EC%8B%9C%EC%9E%91%ED%95%98%EB%8A%94-%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%ED%99%9C%EC%9A%A9%EB%B2%95-e4a7bf2e3c57

https://naveridbuy.blogspot.com/2024/12/blog-post_36.html

https://gold-gull-dd3cmf.mystrikingly.com/blog/2a47c25c4d9

https://naveridbuy.blogspot.com/2024/12/blog-post_52.html

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EC%97%B0%EB%8F%99%ED%95%9C-%EB%8B%A4%EB%A5%B8-%EC%84%9C%EB%B9%84%EC%8A%A4-%ED%99%9C%EC%9A%A9%EB%B2%95-5dde0d66c6f6

After going over a handful of the blog posts on your web site, I honestly like your technique of blogging. I saved as a favorite it to my bookmark website list and will be checking back in the near future. Please visit my web site as well and tell me your opinion.

https://naveridbuy.exblog.jp/37091263/

https://naveridbuy.blogspot.com/2024/12/blog-post_87.html

https://telegra.ph/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4%EA%B0%80-%EB%B6%88%EB%9F%AC%EC%98%A4%EB%8A%94-%EB%B3%B4%EC%95%88-%EC%9C%84%ED%97%98-12-13

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%EA%B3%BC%EC%97%B0-%EB%8F%88%EA%B0%92%EC%9D%84-%ED%95%A0%EA%B9%8C-d89a0fd7d3c4

https://naveridbuy.blogspot.com/2024/12/blog-post_31.html

https://naveridbuy.exblog.jp/37090804/

https://maize-wombat-dd3cms.mystrikingly.com/blog/869d7ae7ea5

https://xn--w2-hd0j99gyns5z0qeiim2i.mystrikingly.com/blog/f803065301b

https://telegra.ph/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EB%B3%B5%EC%9A%A9%EC%9D%B4-%EA%B8%88%EC%A7%80%EB%90%9C-%EA%B2%BD%EC%9A%B0%EB%8A%94-%EC%96%B8%EC%A0%9C%EC%9D%BC%EA%B9%8C-09-12

This site was… how do I say it? Relevant!! Finally I’ve found something that helped me. Thank you.

https://viastoer.blogspot.com/2024/09/blog-post_30.html

https://umber-elk-dbgzh8.mystrikingly.com/blog/5

https://candid-lion-dd3cm3.mystrikingly.com/blog/9cd12105d44

https://telegra.ph/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4-%EC%8B%9C-%ED%95%84%EC%88%98-%EC%B2%B4%ED%81%AC%EB%A6%AC%EC%8A%A4%ED%8A%B8-10-10

https://medium.com/@1kelly76/%EC%A1%B0%EB%A3%A8%EC%99%80-%EB%B0%9C%EA%B8%B0%EB%B6%80%EC%A0%84-%EC%9E%90%EC%A1%B4%EA%B0%90%EC%9D%84-%ED%9A%8C%EB%B3%B5%ED%95%98%EB%8A%94-5%EA%B0%80%EC%A7%80-%EB%B0%A9%EB%B2%95-c0027f644e86

https://adaptable-camellia-dd3cm4.mystrikingly.com/blog/55fdb661b86

https://candid-lion-dd3cm3.mystrikingly.com/blog/8c25ae9d7a9

https://xn--kp-ro2i3ru49at1jokm7ma.mystrikingly.com/blog/50a5900f6b3

https://naveridbuy.blogspot.com/2024/12/blog-post_87.html

https://writeablog.net/jr525di7pj

https://candid-lion-dd3cm3.mystrikingly.com/blog/8c25ae9d7a9

https://hallbook.com.br/blogs/376908/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%EB%8C%80%EC%8B%A0-%EC%82%AC%EC%9A%A9%ED%95%A0-%EC%88%98-%EC%9E%88%EB%8A%94-%EB%B0%A9%EB%B2%95%EB%93%A4

https://telegra.ph/%EB%84%A4%EC%9D%B4%EB%B2%84-%EA%B3%84%EC%A0%95-%EA%B4%80%EB%A6%AC-%EB%B0%8F-%EB%8B%A4%EC%A4%91-%EC%95%84%EC%9D%B4%EB%94%94-%EC%83%9D%EC%84%B1-%EB%B0%A9%EB%B2%95-%EA%B0%80%EC%9D%B4%EB%93%9C-12-13

https://gold-gull-dd3cmf.mystrikingly.com/blog/aecd5fba094

https://naveridbuy.blogspot.com/2024/12/blog-post_29.html

https://medium.com/@carlfrancoh38793/%EA%B5%AC%EA%B8%80-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%EC%9D%B4%EC%A0%90%EA%B3%BC-%EB%8B%A8%EC%A0%90%EC%9D%80-%EB%AC%B4%EC%97%87%EC%9D%B8%EA%B0%80%EC%9A%94-4dccd7ee3fc1

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%ED%9B%84-%EC%8A%A4%EB%A7%88%ED%8A%B8%EC%8A%A4%ED%86%A0%EC%96%B4-%ED%99%9C%EC%9A%A9%EB%B2%95-2d79dbaf8605

https://naveridbuy.exblog.jp/37091323/

https://candid-lion-dd3cm3.mystrikingly.com/blog/5037f72f44c

https://telegra.ph/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EB%AC%B8%EC%A0%9C%EB%A5%BC-%ED%95%B4%EA%B2%B0%ED%95%98%EB%8A%94-%ED%95%A9%EB%B2%95%EC%A0%81%EC%9D%B8-%EB%B0%A9%EB%B2%95-12-13

https://naveridbuy.blogspot.com/2024/11/blog-post_3.html

https://witty-apple-dd3cm1.mystrikingly.com/blog/63d61343ce4

https://adaptable-goat-dd3cmf.mystrikingly.com/blog/ab864ad3a8f

https://medium.com/@nsw5288/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4-%ED%9B%84%EA%B8%B0-%EB%AA%A8%EC%9D%8C-%EC%8B%A0%EB%A2%B0%ED%95%A0-%EC%88%98-%EC%9E%88%EC%9D%84%EA%B9%8C-5dc2946813fc

https://humorous-rabbit-dbgzh6.mystrikingly.com/blog/51e35c53ec6

https://witty-apple-dd3cm1.mystrikingly.com/blog/55463079550

https://candid-lion-dd3cm3.mystrikingly.com/blog/8085327d927

https://naveridbuy.exblog.jp/37091016/

https://telegra.ph/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EB%B3%B5%EC%9A%A9%EC%9D%B4-%EA%B8%88%EC%A7%80%EB%90%9C-%EA%B2%BD%EC%9A%B0%EB%8A%94-%EC%96%B8%EC%A0%9C%EC%9D%BC%EA%B9%8C-09-12

https://medium.com/@nsw5288/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC%EC%99%80-%ED%95%A8%EA%BB%98%EB%9D%BC%EB%A9%B4-%EC%A3%BC%EC%9D%98%ED%95%B4%EC%95%BC-%ED%95%A0-%EC%95%BD%EB%AC%BC%EB%93%A4-a3861b835e15

https://viastoer.blogspot.com/2024/09/blog-post_5.html

https://xn--w5-hd0jg6f81lm0dhhw74c.mystrikingly.com/blog/7dbe3159553

https://gwojawe-fjaow-jiao.mystrikingly.com/blog/669541f58ff

https://medium.com/@nsw5288/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EC%98%A8%EB%9D%BC%EC%9D%B8-%EA%B5%AC%EB%A7%A4-%EC%8B%9C-%EC%A3%BC%EC%9D%98%EC%82%AC%ED%95%AD-7eb81634b40d

https://witty-apple-dd3cm1.mystrikingly.com/blog/63d61343ce4

https://viastoer.blogspot.com/2024/09/blog-post_44.html

https://responsible-seal-dd3cm4.mystrikingly.com/blog/0f08a7ad417

https://xn--fc-hd0jg6f81ltjas9lbns.mystrikingly.com/blog/dcd84c3fc9c

https://hallbook.com.br/blogs/278115/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4%EC%9D%98-%EB%B2%95%EC%A0%81-%EC%82%AC%ED%95%AD%EA%B3%BC-%EA%B7%9C%EC%A0%95

https://telegra.ph/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%EB%8C%80%EC%8B%A0-%EC%82%AC%EC%9A%A9%ED%95%A0-%EC%88%98-%EC%9E%88%EB%8A%94-%EB%B0%A9%EB%B2%95%EB%93%A4-12-13

https://telegra.ph/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4-%EC%8B%9C-%EC%95%8C%EC%95%84%EC%95%BC-%ED%95%A0-%EC%9C%A0%EC%9D%98%EC%82%AC%ED%95%AD-7%EA%B0%80%EC%A7%80-09-20

https://naveridbuy.blogspot.com/2024/12/blog-post_27.html

https://naveridbuy.blogspot.com/2024/11/blog-post_3.html

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%ED%9B%84-%EA%B4%91%EA%B3%A0-%EA%B4%80%EB%A6%AC%EC%97%90-%ED%99%9C%EC%9A%A9%ED%95%98%EB%8A%94-%EB%B0%A9%EB%B2%95-6a822042a160

https://naveridbuy.exblog.jp/37090804/

https://telegra.ph/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B1%B0%EB%9E%98%EB%8A%94-%EC%95%88%EC%A0%84%ED%95%9C%EA%B0%80-%EC%A0%84%EB%AC%B8%EA%B0%80%EC%9D%98-%EC%A1%B0%EC%96%B8-12-13

https://viastoer.blogspot.com/2024/09/blog-post_22.html

https://xn--w3-o02ik82a9kav54aokmxvc.mystrikingly.com/blog/1303baaafdb

https://naveridbuy.blogspot.com/2024/12/blog-post_82.html

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4%EB%A1%9C-%ED%95%98%EB%A3%A8-%EB%A7%8C%EC%97%90-%EC%8A%A4%EB%A7%88%ED%8A%B8%EC%8A%A4%ED%86%A0%EC%96%B4-%EA%B0%9C%EC%84%A4%ED%95%98%EA%B8%B0-439f0195fc49

Hi there! This blog post could not be written much better! Going through this post reminds me of my previous roommate! He continually kept talking about this. I’ll forward this post to him. Pretty sure he’ll have a very good read. I appreciate you for sharing!

https://witty-apple-dd3cm1.mystrikingly.com/blog/e592523ee2b

https://gold-gull-dd3cmf.mystrikingly.com/blog/277217c9c6c

https://naveridbuy.blogspot.com/2024/12/blog-post_2.html

https://candid-lion-dd3cm3.mystrikingly.com/blog/8085327d927

https://candid-lion-dd3cm3.mystrikingly.com/blog/2024

https://naveridbuy.blogspot.com/2024/12/blog-post_66.html

https://gold-gull-dd3cmf.mystrikingly.com/blog/8624dd23af4

https://bronze-lily-dbgzh7.mystrikingly.com/blog/b9f326cbd55

https://ocher-cat-dd3cmm.mystrikingly.com/blog/642842abd0f

https://naveridbuy.blogspot.com/2024/11/blog-post_28.html

https://witty-apple-dd3cm1.mystrikingly.com/blog/55463079550

https://naveridbuy.blogspot.com/2024/12/blog-post_19.html

https://witty-apple-dd3cm1.mystrikingly.com/blog/63d61343ce4

https://medium.com/@nsw5288/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EC%96%B8%EC%A0%9C-%EB%B3%B5%EC%9A%A9%ED%95%B4%EC%95%BC-%ED%9A%A8%EA%B3%BC%EA%B0%80-%EC%A2%8B%EC%9D%84%EA%B9%8C-12c8395a1912

https://ameblo.jp/naveridbuy/entry-12866333769.html

https://gold-gull-dd3cmf.mystrikingly.com/blog/277217c9c6c

https://naveridbuy.blogspot.com/2024/11/top-5.html

https://naveridbuy.blogspot.com/2024/11/blog-post_50.html

https://naveridbuy.blogspot.com/2024/12/blog-post_36.html

https://naveridbuy.blogspot.com/2024/12/blog-post_19.html

https://inky-owl-dd3cmv.mystrikingly.com/blog/9dacaeed43a

https://naveridbuy.exblog.jp/37152083/

https://naveridbuy.exblog.jp/37090804/

https://adaptable-camellia-dd3cm4.mystrikingly.com/blog/25f45f68c48

https://gold-gull-dd3cmf.mystrikingly.com/blog/dc52558c085

https://telegra.ph/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4-%EC%86%8C%EC%85%9C-%EB%AF%B8%EB%94%94%EC%96%B4%EB%A5%BC-%ED%99%9C%EC%9A%A9%ED%95%9C-%EC%A0%95%EB%B3%B4-%EC%B0%BE%EA%B8%B0-09-26

https://naveridbuy.exblog.jp/35891783/

https://medium.com/@nsw5288/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EC%98%A8%EB%9D%BC%EC%9D%B8-%EA%B5%AC%EB%A7%A4-%EB%B0%A9%EB%B2%95%EA%B3%BC-%EC%A3%BC%EC%9D%98-%EC%82%AC%ED%95%AD-c80ca72b0103

https://telegra.ph/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4%EA%B0%80-%EB%B6%88%EB%9F%AC%EC%98%A4%EB%8A%94-%EB%B3%B4%EC%95%88-%EC%9C%84%ED%97%98-12-13

https://telegra.ph/%EC%95%84%EC%9D%B4%EB%94%94-%EA%B1%B0%EB%9E%98%EC%9D%98-%EC%88%A8%EA%B2%A8%EC%A7%84-%EC%9C%84%ED%97%98-%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EC%95%88%EC%A0%84%ED%95%98%EA%B2%8C-%EC%A7%80%ED%82%A4%EB%8A%94-%EB%B2%95-12-13

https://medium.com/@nsw5288/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EC%98%A8%EB%9D%BC%EC%9D%B8-%EA%B5%AC%EB%A7%A4-%EB%B0%A9%EB%B2%95%EA%B3%BC-%EC%A3%BC%EC%9D%98-%EC%82%AC%ED%95%AD-c80ca72b0103

https://naveridbuy.blogspot.com/2024/12/blog-post_76.html

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%B9%B4%ED%8E%98-%EC%9A%B4%EC%98%81%EC%9D%84-%EC%9C%84%ED%95%9C-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%ED%8C%81-eb39c3e24984

Very good information. Lucky me I recently found your site by chance (stumbleupon). I have saved it for later.

You should take part in a contest for one of the highest quality sites on the internet. I am going to highly recommend this website!

https://telegra.ph/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EB%B3%B5%EC%9A%A9-%ED%9B%84-%EC%A3%BC%EC%9D%98%ED%95%B4%EC%95%BC-%ED%95%A0-%EA%B1%B4%EA%B0%95-%EC%8B%A0%ED%98%B8%EB%93%A4-09-12

https://viastoer.blogspot.com/2024/10/blog-post.html

https://candid-lion-dd3cm3.mystrikingly.com/blog/5037f72f44c

https://xn--fn-hd0jg6f81ltjas9lbns.mystrikingly.com/blog/290000a8b29

Good web site you have here.. It’s hard to find excellent writing like yours nowadays. I honestly appreciate people like you! Take care!!

https://naveridbuy.exblog.jp/35891783/

https://naveridbuy.exblog.jp/35891802/

Very nice blog post. I definitely love this site. Stick with it!

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94%EC%99%80-%EA%B4%80%EB%A0%A8%EB%90%9C-%EC%B5%9C%EC%8B%A0-%EB%B3%B4%EC%95%88-%EC%9D%B4%EC%8A%88-4569786b88d3

https://gajweor.pixnet.net/blog/post/162189406

https://gold-gull-dd3cmf.mystrikingly.com/blog/dc52558c085

https://gold-gull-dd3cmf.mystrikingly.com/blog/aecd5fba094

https://naveridbuy.exblog.jp/37091016/

https://naveridbuy.exblog.jp/37152040/

https://naveridbuy.exblog.jp/37152100/

https://naveridbuy.blogspot.com/2024/12/blog-post.html

Great article. I am experiencing a few of these issues as well..

https://hallbook.com.br/blogs/278114/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4-%EC%8B%9C-%EA%B3%A0%EB%A0%A4%ED%95%B4%EC%95%BC-%ED%95%A0-%EA%B0%9C%EC%9D%B8%EC%A0%81%EC%9D%B8-%EA%B1%B4%EA%B0%95-%EC%9A%94%EC%86%8C

https://writeablog.net/37n5a9w9yv

https://sociable-corn-dd3cmt.mystrikingly.com/blog/62214e87a2c

https://ko.anotepad.com/note/read/5f6b88g5

https://salmon-peach-dd3cm8.mystrikingly.com/blog/vs

Your style is really unique compared to other people I’ve read stuff from. Many thanks for posting when you’ve got the opportunity, Guess I will just bookmark this blog.

An impressive share! I have just forwarded this onto a co-worker who was conducting a little research on this. And he in fact ordered me dinner because I discovered it for him… lol. So let me reword this…. Thank YOU for the meal!! But yeah, thanx for spending some time to talk about this matter here on your web site.

https://ocher-cat-dd3cmm.mystrikingly.com/blog/f6aa48fdc0c

https://turquoise-dove-dd3cmd.mystrikingly.com/blog/e1eca45d868

https://medium.com/@1kelly76/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4-%EC%A0%84-%EC%96%B4%EB%96%A4-%EA%B2%83%EC%9D%84-%EA%B3%A0%EB%A0%A4%ED%95%B4%EC%95%BC-%ED%95%A0%EA%B9%8C-743d5cd4580e

https://gajweor.pixnet.net/blog/post/162317545

This website truly has all the information and facts I needed about this subject and didn’t know who to ask.

https://ameblo.jp/naveridbuy/entry-12865282919.html

https://umber-iris-dd3cm2.mystrikingly.com/blog/674c3251b7d

https://naveridbuy.blogspot.com/2024/11/blog-post_3.html

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%ED%9B%84-%EA%B3%84%EC%A0%95-%EB%B3%B4%ED%98%B8-%EB%B0%A9%EB%B2%95-%EC%99%84%EB%B2%BD-%EC%A0%95%EB%A6%AC-ab3a80545ed1

https://naveridbuy.blogspot.com/2024/12/blog-post_53.html

https://inky-owl-dd3cmv.mystrikingly.com/blog/570378fab9f

https://naveridbuy.exblog.jp/37152138/

https://naveridbuy.blogspot.com/2024/11/blog-post_58.html

https://gold-gull-dd3cmf.mystrikingly.com/blog/58fe76cd6ee

https://naveridbuy.blogspot.com/2024/12/blog-post_26.html

Good info. Lucky me I recently found your website by accident (stumbleupon). I’ve book-marked it for later.

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94%EC%99%80-%EA%B4%80%EB%A0%A8%EB%90%9C-%EC%B5%9C%EC%8B%A0-%EB%B3%B4%EC%95%88-%EC%9D%B4%EC%8A%88-4569786b88d3

https://naveridbuy.blogspot.com/2024/11/top-5.html

https://hallbook.com.br/blogs/376905/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EC%97%86%EC%9D%B4-%EC%84%9C%EB%B9%84%EC%8A%A4-%EC%9D%B4%EC%9A%A9%ED%95%98%EB%8A%94-%ED%8C%81

https://candid-lion-dd3cm3.mystrikingly.com/blog/8c25ae9d7a9

Great information. Lucky me I ran across your blog by accident (stumbleupon). I’ve bookmarked it for later.

https://golden-grape-dd3cml.mystrikingly.com/blog/5cc22257c87

https://naveridbuy.blogspot.com/2024/12/blog-post_12.html

https://naveridbuy.blogspot.com/2024/12/blog-post_76.html

https://inky-owl-dd3cmv.mystrikingly.com/blog/9f4dcb67968

https://medium.com/@nsw5288/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EC%96%B8%EC%A0%9C-%EB%B3%B5%EC%9A%A9%ED%95%B4%EC%95%BC-%ED%9A%A8%EA%B3%BC%EA%B0%80-%EC%A2%8B%EC%9D%84%EA%B9%8C-12c8395a1912

I would like to thank you for the efforts you’ve put in penning this site. I really hope to see the same high-grade content from you later on as well. In truth, your creative writing abilities has motivated me to get my own blog now 😉

https://naveridbuy.blogspot.com/2024/12/blog-post_31.html

https://naveridbuy.blogspot.com/2024/11/blog-post_7.html

https://gajweor.pixnet.net/blog/post/157629283

https://maize-wombat-dd3cms.mystrikingly.com/blog/6f12963a21b

Hello there, I think your site might be having browser compatibility problems. Whenever I look at your blog in Safari, it looks fine however, when opening in Internet Explorer, it has some overlapping issues. I merely wanted to give you a quick heads up! Besides that, fantastic blog.

https://medium.com/@carlfrancoh38793/%EA%B5%AC%EA%B8%80-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%EC%9D%B4%EC%A0%90%EA%B3%BC-%EB%8B%A8%EC%A0%90%EC%9D%80-%EB%AC%B4%EC%97%87%EC%9D%B8%EA%B0%80%EC%9A%94-4dccd7ee3fc1

https://naveridbuy.exblog.jp/37091263/

https://naveridbuy.exblog.jp/37090861/

https://medium.com/@carlfrancoh38793/%EC%A4%91%EA%B3%A0-%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94%EB%A5%BC-%ED%9A%A8%EA%B3%BC%EC%A0%81%EC%9C%BC%EB%A1%9C-%ED%99%9C%EC%9A%A9%ED%95%98%EB%8A%94-%EB%B0%A9%EB%B2%95-a5bd35053073

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%ED%9B%84-%EA%B4%91%EA%B3%A0-%EA%B4%80%EB%A6%AC%EC%97%90-%ED%99%9C%EC%9A%A9%ED%95%98%EB%8A%94-%EB%B0%A9%EB%B2%95-6a822042a160

https://naveridbuy.blogspot.com/2024/12/blog-post_9.html

https://telegra.ph/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4%EB%A5%BC-%EC%9C%84%ED%95%9C-%EC%8A%A4%EB%A7%88%ED%8A%B8%ED%8F%B0-%EC%95%B1-%EC%B6%94%EC%B2%9C-09-26

https://adaptable-camellia-dd3cm4.mystrikingly.com/blog/55fdb661b86

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EC%97%B0%EB%8F%99%ED%95%9C-%EB%8B%A4%EB%A5%B8-%EC%84%9C%EB%B9%84%EC%8A%A4-%ED%99%9C%EC%9A%A9%EB%B2%95-5dde0d66c6f6

https://hallbook.com.br/blogs/376903/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B1%B0%EB%9E%98%EB%8A%94-%EC%95%88%EC%A0%84%ED%95%9C%EA%B0%80-%EC%A0%84%EB%AC%B8%EA%B0%80%EC%9D%98-%EC%A1%B0%EC%96%B8

https://inky-owl-dd3cmv.mystrikingly.com/blog/1f98f73959a

https://naveridbuy.exblog.jp/35891806/

https://telegra.ph/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4%EB%A5%BC-%EC%9C%84%ED%95%9C-%EC%8A%A4%EB%A7%88%ED%8A%B8%ED%8F%B0-%EC%95%B1-%EC%B6%94%EC%B2%9C-09-26

https://gajweor.pixnet.net/blog/post/162874255

Greetings! Very helpful advice within this post! It is the little changes that will make the biggest changes. Thanks for sharing!

https://umber-iris-dd3cm2.mystrikingly.com/blog/9e5d9a0e4a7

https://grape-pear-dbgzh0.mystrikingly.com/blog/48ea9f72e99

https://candid-lion-dd3cm3.mystrikingly.com/blog/7114981bc76

https://candid-lion-dd3cm3.mystrikingly.com/blog/7114981bc76

https://gold-gull-dd3cmf.mystrikingly.com/blog/809bdcf69a1

https://medium.com/@carlfrancoh38793/%EC%95%84%EC%9D%B4%EB%94%94-%EC%A4%91%EB%B3%B5-%EB%AC%B8%EC%A0%9C-%ED%95%B4%EA%B2%B0-%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%ED%99%9C%EC%9A%A9%EB%B2%95-a0ec8344a6bd

https://naveridbuy.blogspot.com/2024/12/blog-post_12.html

https://naveridbuy.blogspot.com/2024/11/5.html

https://medium.com/@carlfrancoh38793/%EB%B9%A0%EB%A5%B4%EA%B2%8C-%EC%8B%9C%EC%9E%91%ED%95%98%EB%8A%94-%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%ED%99%9C%EC%9A%A9%EB%B2%95-e4a7bf2e3c57

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94%EA%B0%80-%ED%95%84%EC%9A%94%ED%95%A0-%EB%95%8C-%EA%B5%AC%EB%A7%A4%EA%B0%80-%EB%8B%B5%EC%9D%BC%EA%B9%8C-4bbacce4d7df

https://adaptable-camellia-dd3cm4.mystrikingly.com/blog/55fdb661b86

https://naveridbuy.exblog.jp/37091016/

https://adaptable-camellia-dd3cm4.mystrikingly.com/blog/25f45f68c48

https://naveridbuy.blogspot.com/2024/11/blog-post_50.html

https://naveridbuy.blogspot.com/2024/11/2024.html

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%EC%88%A8%EA%B2%A8%EC%A7%84-%EC%A7%84%EC%8B%A4%EC%9D%84-%ED%8C%8C%ED%97%A4%EC%B3%90%EB%B4%A4%EC%8A%B5%EB%8B%88%EB%8B%A4-ad07e5d2c8d7

Pretty! This has been a really wonderful article. Thank you for supplying this information.

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94%EC%99%80-%EA%B4%80%EB%A0%A8%EB%90%9C-%EC%B5%9C%EC%8B%A0-%EB%B3%B4%EC%95%88-%EC%9D%B4%EC%8A%88-4569786b88d3

https://telegra.ph/%EC%95%84%EC%9D%B4%EB%94%94-%EA%B1%B0%EB%9E%98%EC%9D%98-%EC%88%A8%EA%B2%A8%EC%A7%84-%EC%9C%84%ED%97%98-%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EC%95%88%EC%A0%84%ED%95%98%EA%B2%8C-%EC%A7%80%ED%82%A4%EB%8A%94-%EB%B2%95-12-13

https://naveridbuy.blogspot.com/2024/11/blog-post_58.html

https://ameblo.jp/naveridbuy/entry-12865283090.html

https://xn--lq-o02ik82aiqcqsko8mfg5a1sb.mystrikingly.com/blog/b10ad28d131

https://ko.anotepad.com/note/read/ekdmqg4x

https://medium.com/@nsw5288/%EB%B0%9C%EA%B8%B0%EB%B6%80%EC%A0%84%EA%B3%BC-%EC%A1%B0%EB%A3%A8-%EC%89%BD%EA%B2%8C-%EC%9D%B4%ED%95%B4%ED%95%98%EA%B3%A0-%EA%B7%B9%EB%B3%B5%ED%95%98%EB%8A%94-%EB%B2%95-5212fd7c4fa0

Excellent article. I will be experiencing some of these issues as well..

Very interesting topic, thank you for posting. “The deepest American dream is not the hunger for money or fame it is the dream of settling down, in peace and freedom and cooperation, in the promised land.” by Scott Russell Sanders..

Excellent post. I’m dealing with some of these issues as well..

https://medium.com/@1kelly76/%EC%A1%B0%EB%A3%A8%EB%A1%9C-%EC%9D%B8%ED%95%9C-%EA%B3%A0%EB%AF%BC-%ED%95%B4%EA%B2%B0%EC%B1%85%EC%9D%80-%EB%AC%B4%EC%97%87%EC%9D%BC%EA%B9%8C-7fbd3a7a1e9b

https://inky-owl-dd3cmv.mystrikingly.com/blog/570378fab9f

https://naveridbuy.blogspot.com/2024/12/blog-post_6.html

https://hallbook.com.br/blogs/376898/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4%EA%B0%80-%EB%B6%88%EB%9F%AC%EC%98%A4%EB%8A%94-%EB%B3%B4%EC%95%88-%EC%9C%84%ED%97%98

After checking out a number of the articles on your blog, I seriously like your way of blogging. I saved as a favorite it to my bookmark website list and will be checking back in the near future. Please visit my web site as well and let me know what you think.

https://naveridbuy.exblog.jp/37090971/

https://naveridbuy.blogspot.com/2024/11/blog-post_28.html

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94%EA%B0%80-%ED%95%84%EC%9A%94%ED%95%A0-%EB%95%8C-%EA%B5%AC%EB%A7%A4%EA%B0%80-%EB%8B%B5%EC%9D%BC%EA%B9%8C-4bbacce4d7df

https://salmon-peach-dd3cm8.mystrikingly.com/blog/dbd2b0155cb

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94%EC%99%80-%EA%B4%80%EB%A0%A8%EB%90%9C-%EC%B5%9C%EC%8B%A0-%EB%B3%B4%EC%95%88-%EC%9D%B4%EC%8A%88-4569786b88d3

Great info. Lucky me I ran across your blog by accident (stumbleupon). I’ve saved it for later.

https://telegra.ph/%EC%95%84%EC%9D%B4%EB%94%94-%EA%B1%B0%EB%9E%98%EC%9D%98-%EC%88%A8%EA%B2%A8%EC%A7%84-%EC%9C%84%ED%97%98-%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EC%95%88%EC%A0%84%ED%95%98%EA%B2%8C-%EC%A7%80%ED%82%A4%EB%8A%94-%EB%B2%95-12-13

https://writeablog.net/37n5a9w9yv

https://medium.com/@carlfrancoh38793/%EC%A4%91%EA%B3%A0-%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94%EB%A5%BC-%ED%9A%A8%EA%B3%BC%EC%A0%81%EC%9C%BC%EB%A1%9C-%ED%99%9C%EC%9A%A9%ED%95%98%EB%8A%94-%EB%B0%A9%EB%B2%95-a5bd35053073

https://inky-owl-dd3cmv.mystrikingly.com/blog/f111c3c7d0d

https://candid-lion-dd3cm3.mystrikingly.com/blog/53469580831

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4%EA%B0%80-%EC%9D%B8%EA%B8%B0-%EC%9E%88%EB%8A%94-%EC%9D%B4%EC%9C%A0%EB%A5%BC-%EC%95%8C%EC%95%84%EB%B3%B4%EC%9E%90-854637610dd2

Is this a new post? i ask because i think i read the same article a month ago on hubpages.

I adore your website.. excellent colours & theme. Did an individual design this site oneself or maybe have you actually rely on someone else to do it for you personally? Plz answer while I!|m planning to design and style my very own blog site as well as want to learn where by u became this specific through. thanks

https://salmon-peach-dd3cm8.mystrikingly.com/blog/5ebd4cee1f6

https://ko.anotepad.com/note/read/pymsgn44

https://naveridbuy.blogspot.com/2024/11/blog-post_7.html

https://candid-lion-dd3cm3.mystrikingly.com/blog/7114981bc76

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%ED%95%A9%EB%B2%95%EC%9D%B8%EA%B0%80%EC%9A%94-%EC%95%8C%EC%95%84%EB%B4%85%EC%8B%9C%EB%8B%A4-40dff2b624f5

https://candid-lion-dd3cm3.mystrikingly.com/blog/b99e214c11a

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%B9%B4%ED%8E%98-%EC%9A%B4%EC%98%81%EC%9D%84-%EC%9C%84%ED%95%9C-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%ED%8C%81-eb39c3e24984

I blog quite often and I really thank you for your information. The article has truly peaked my interest. I am going to book mark your website and keep checking for new information about once a week. I opted in for your Feed as well.

https://telegra.ph/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B1%B0%EB%9E%98%EB%8A%94-%EC%95%88%EC%A0%84%ED%95%9C%EA%B0%80-%EC%A0%84%EB%AC%B8%EA%B0%80%EC%9D%98-%EC%A1%B0%EC%96%B8-12-13

https://ameblo.jp/naveridbuy/entry-12866333999.html

https://xn--w0-hd0jg6f81lm0dhhw74c.mystrikingly.com/blog/2ea87cc6ee1

I’m impressed, I must say. Seldom do I come across a blog that’s equally educative and interesting, and without a doubt, you’ve hit the nail on the head. The problem is something which not enough people are speaking intelligently about. Now i’m very happy that I found this in my search for something regarding this.

Hey There. I found your blog using msn. This is an extremely well written article. I’ll be sure to bookmark it and return to read more of your useful information. Thanks for the post. I’ll definitely comeback.

https://inky-owl-dd3cmv.mystrikingly.com/blog/f111c3c7d0d

https://wise-onion-dbgzhg.mystrikingly.com/blog/58f918f70c9

https://hallbook.com.br/blogs/326299/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4-%EC%8B%9C-%ED%95%84%EC%88%98-%EC%B2%B4%ED%81%AC%EB%A6%AC%EC%8A%A4%ED%8A%B8