Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of both the economy and financial markets in real-time. Here are the top developments that stand out to us:

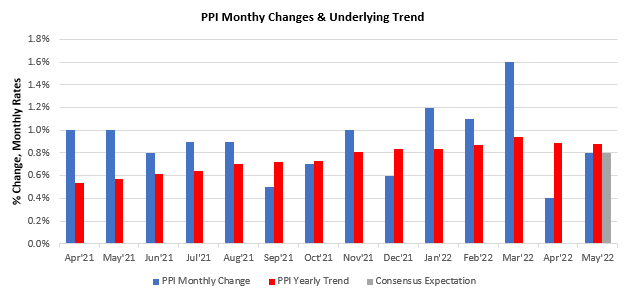

i. PPI inflation remains elevated. PPI data showed a monthly increase of 0.8%, leading to a 10.5% change versus a year ago, in line with consensus expectations. This reading was a sequential deceleration within an accelerating trend 12-month trend.

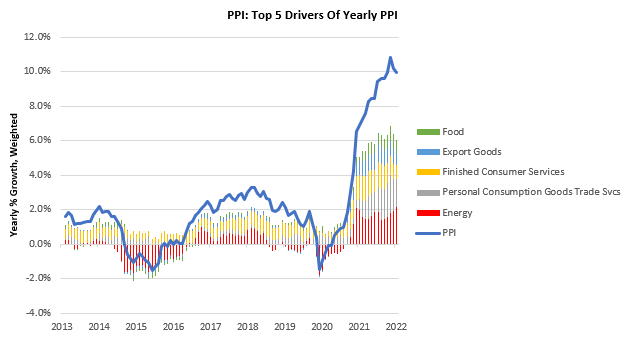

Energy, Personal Consumption Goods-Trade Services, Finished Consumer Services, Export Goods, & Food have exerted the largest influence on PPI over the last twelve months:

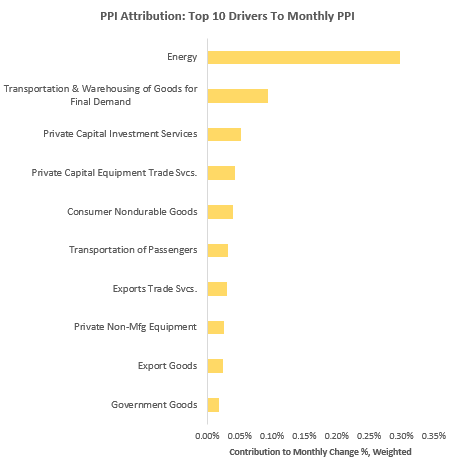

Additionally, we show the top 10 contributors to the monthly changes in PPI:

Our systems continue to tell us that inflation remains at worrying levels, and we continue to think it is optimal to position accordingly. As we can see, energy remains the dominant driver of producer price increases. However, we also see a migration of price pressures to various private services, suggesting the broadening of inflationary pressures.

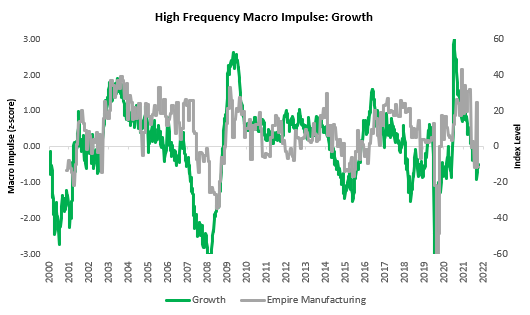

ii. Our systems expect PMIs to continue to deteriorate. In particular, we see potential for Empire Fed Manufacturing to disappoint consennsus expectations significantly.

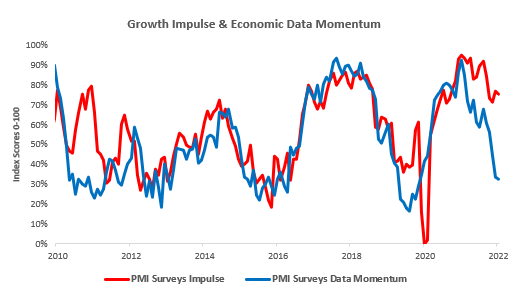

Our proprietary measures of growth continue to tell us the we are in an economic deceleration and to position accordingly. Additionally, we see that PMI data has shown a trend of disappointing consensus expectations as economic growth recedes, we expect this to continue. We show this below, comparing the disappointment/surpises in economic data, i.e. Economic Data Momentum versus our standarized measure of PMI surveys:

Our systems see no reason for these moves to stop, as growth continues to be choked by higher inflation.

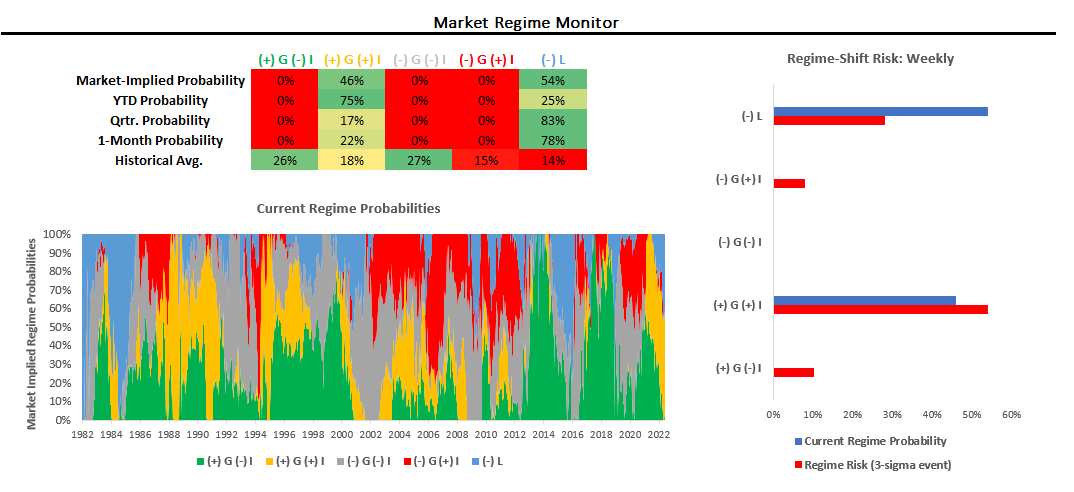

iii. Markets have moved to dominantly price tightening liquidity. This environment is typically kyrptonite for risk asset, with the dollar being the only safe haven. We must wait and see if this dynamic to hold for our systems to further increase our short exposure. We show our market regime monitor below:

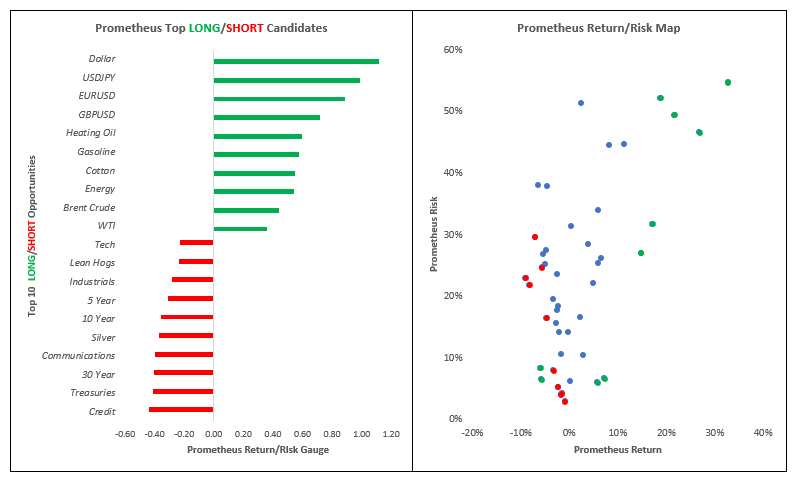

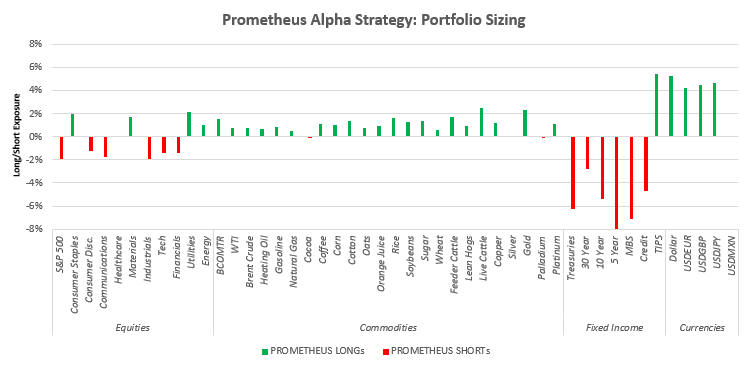

Combining this with measures of market trends, our systems estimate that the best return/risk characteristics are LONG: Dollar & USDJPY and SHORT: Credit & Treasuries:

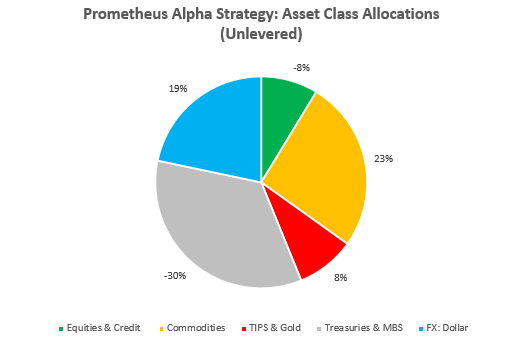

Our systems continue to generate string performance in the current economic backdrop. In light of these fundamental and market conditions, our systems remain long inflation beneficiaries and short assets that cannot survive this environment. Over time, we expect our systems to pull-back on commodity positions as volatility escalates and return prospects dimish. However, we aren’t there yet. Below, we show how our Alpha Strategy is positioned at the asset class level:

As we can see above, our systems remain aggressively short equities and fixed income while staying long dollars and commodities. Last week was a great week for this approach, and our systems continue to maintain the conviction that the environment has not materially changed yet. We show our exposures for the Alpha Strategies at the asset level below:

We continue to reiterate that this is a time for capital preservation and active shorting. Even if you aren’t generating returns on the short side, not losing money on the long side is also alpha. Stay nimble.

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.