Get key US macroeconomic and market research directly in your inbox.

This week, the Treasury will release its Quarterly Refunding Announcement (QRA), detailing the estimated supply of Treasury securities over the first half of 2024. Given the recent trends in government spending, this has begun to impact ongoing macroeconomic conditions significantly. We will reserve our detailed, data-driven assessment of the announcement to ETF Portfolio & Prometheus Bespoke subscribers. Still, given the importance in the current context, we offer our thoughts on the mechanics at play.

In the QRA documents, the Treasury offers forward-looking estimates of the supply of treasury securities, along with the composition of this supply, i.e., how many short-term securities (bills) versus long-term securities (coupons) the Treasury will use to finance government spending. Like any security, the price of Treasury securities is determined by supply and demand.

In the post-pandemic period, we have seen a step-function increase in treasury supply as the government spends money on the economy. Simultaneously, we have witnessed one of the biggest inflation shocks in recent history. The combination of these events drove one of the sharpest drawdowns in treasuries on record. These dynamics drag not just on the Treasury market but all asset markets due to the size of funding requirements by the Treasury, draining funds that may have been otherwise used to support other assets. Therefore, in today’s environment, an ongoing assessment of demand and supply forces is required to stay on the right side of macro risk, both in Treasuries and asset markets. This assessment brings us to the upcoming QRA announcement. Two levers will be at play in determining both the direct impact on treasuries and the indirect impact on broader markets: the total issuance and the composition of issuance.

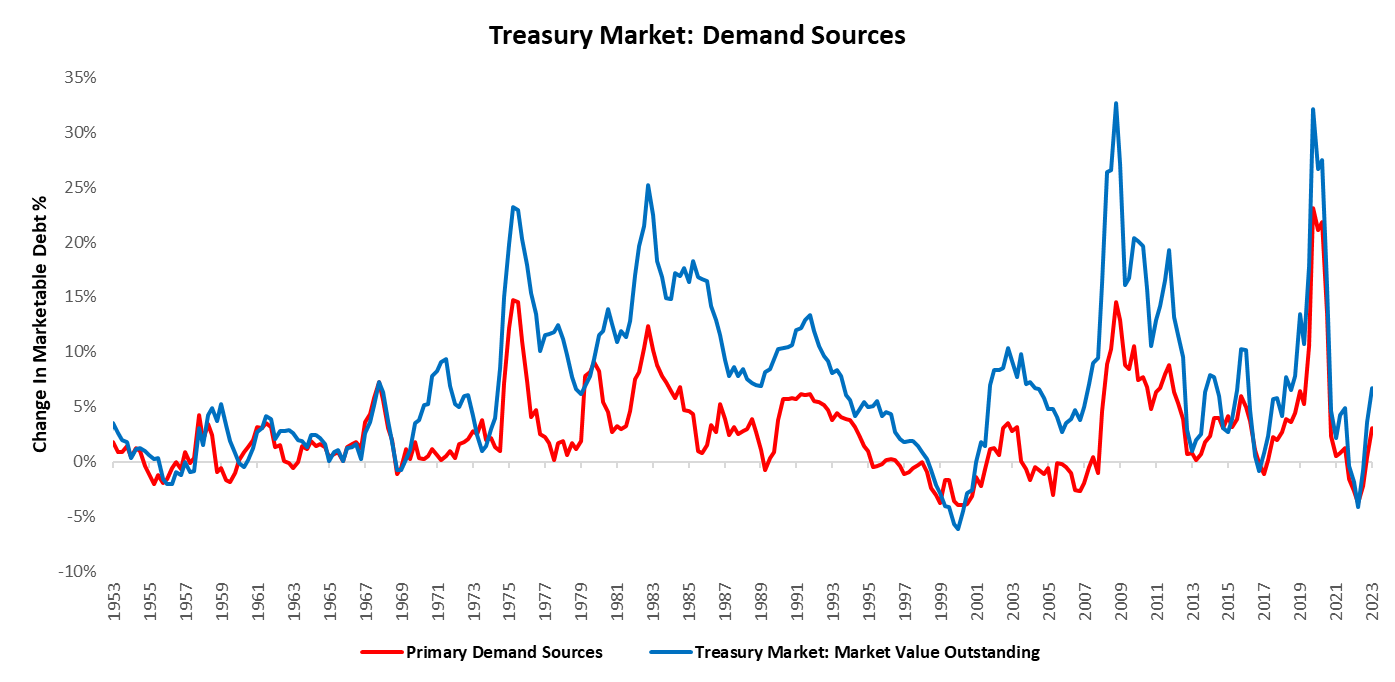

We begin with the impacts of total issuance, which is the more linear component. The total issuance size reflects the supply of treasuries, and an increase in supply for an existing level of demand creates a weakness in prices. Demand for treasuries can come from one of three places: i) savings come from nominal GDP, ii) the sale of assets, and iii) an increase in borrowing. We discuss these flows:

- NGDP: The flow of nominal GDP creates income for households and businesses, which largely never enters financial markets. However, part of this nominal activity is saved, and some of this savings flows into treasury markets to absorb new issuance of treasuries. As such, nominal activity is a natural limit on the amount of support issuance can receive from the economy.

- Rebalance: Alongside this demand from the real economy, we can also demand treasuries from the financial economy. As previously listed, this can be either via the sale of assets or an increase in borrowing. The sale of assets is effectively a rebalance of positions, e.g., an investor may sell some stock to increase their treasury position. This channel largely depends on the relative attractiveness of the securities (risk vs. reward), which is contingent upon macroeconomic conditions. Cash is a financial asset, and the sale of cash for assets is also a type of rebalancing.

- Leverage: Finally, economic entities may choose to leverage their exposure to an asset. This channel occurs primarily through lending created by intermediaries (banks, security dealers, etc.). Intermediaries create credit, allowing households, corporations, and other investors to take on leverage positions. The intermediaries embed the most significant amount of leverage in the system since their exposure is also leveraged.

The combination of these three flows supports a given level of treasury supply to determine the price of treasuries. We currently see these forces as a weight on treasury prices, as they have been since the initial response to the COVID-19 pandemic. The net supply of US Treasuries continues to outpace nominal GDP, creating a shortfall of nominal activity that can support issuance.

While this nominal activity falls below the issuance rate, it continues to operate at a high level relative to recent history, creating a backdrop that supports stocks and credit far more than treasuries. This is because corporate securities earn a risk premium for pro-cyclical exposure to the economy. As nominal activity accelerates, investors favor more exposure to these corporate assets than treasuries. Investors have little reason to rebalance these allocations meaningfully without a significant shock to growth conditions. Finally and historically anomalously, this spike in treasury supply relative to nominal GDP growth has occurred during a high-interest rate environment, where short-term rates are above long-term rates. This interest rate dynamic does little to promote a rebalance from cash into longer-dated securities or a leveraging up of positions. As such, the shape of the yield curve (the short rate vs. the long rate) inhibits both the rebalancing of cash and the leveraging of existing balance sheet potential. Therefore, looking across these determinants of demand relative to supply, the big-picture backdrop for treasuries continues to look weak.

Now, while total issuance determines a large part of these outcomes, a marginal and more nuanced impact comes from the composition of issuance. When the treasury issues securities, it can issue either short-term securities (bills) or long-term ones (coupons). Short-term securities earn the short rate and have virtually zero price risk, while long-term securities earn long-term interest rate rates and have considerable price risk. The demand for these securities comes from two relatively distinct places. Bills are demanded by economic entities looking to manage cash reserves while offsetting the impact of inflation. Coupons are demanded mainly by investors looking to earn interest and assume the risk of price appreciation baked into yields. When bills are issued, a large portion of demand stems from nominal activity with no change in private sector leverage. However, when coupons are issued, portfolio rebalance and leverage become significant demand components. The Treasury’s choice between bills and coupons determines which channels it taps the most. The more bills are issued, the more demand comes from demand sources closer to the real economy; the more coupons are issued, the more demand comes from asset sales and leverage. Thus, while increasing the aggregate supply of treasuries puts pressure on treasury prices, it can be mitigated by the choice between bills and bonds. The more coupons issued, the more risk the financial system needs to take on, and the more pressure there is for treasury prices to fall. The more bills issued, the less pressure on the financial system to sell assets or leverage up. Therefore, while increasing treasury supply puts pressure on prices, issuance composition can somewhat mitigate it. Understanding this dynamic is crucial in today’s environment, where robust nominal growth has created large cash balances, allowing the Treasury to fund itself using more bills vs. coupons than historically. This skew in issuance composition, particularly last quarter, has allowed for a pause in the bond bear market. This policy is consistent with the Treasury’s objectives, i.e., to achieve the most stable and competitive funding for the US Government over the long term. In an environment where bonds were seeing weakness in demand, it made sense for the Treasury to skew its issuance towards bills to reduce price pressure on coupons, thereby maintaining a stable interest burden for the government.

Looking ahead, the Treasury will follow one of two paths: it will continue with its issuance skewed towards bills or move back to norms more consistent with recent history. Both paths will likely remain pressures on treasury prices as the gross issuance remains extremely large, though issuing more bonds would be significantly worse. When executing risk based on these concepts in markets, we think it is crucial to recognize that these drivers will broadly impact term premiums/the slope of the yield curve and not the path of the Fed’s policy rate. This distinction is an imperative one to understand for investors, as the path of the Fed’s policy rate is the number one driving factor in driving the total return of treasury securities. Unlike last midyear year, when QRA coincided with a hiking cycle, QRA aligns with the probable onset of an easing cycle. As such, the opportunity to be outright short treasuries has diminished, but relative value opportunities remain for those looking to generate macro alpha. However, we reserve these views for our subscribers.

Overall, the pace of overall treasury supply remains a headwind for bond markets relative to a lower supply regime. Further, this headwind will likely continue to weigh on overall risk-taking, as investors will probably need to weigh on portfolio rebalance effects to fund ongoing issuance. However, the initiation of a cutting cycle counteracts some of these pressures. Combining these forces creates more relative value than absolute return opportunities in treasuries. Finally, we conclude by sharing that this isn’t a dynamic that market participants need to attempt to front-run or trade very swiftly. While we expect market action around the announcement, the market reaction to these events will likely be consistent, as market participants watching these flows are unlikely to front-run the sheer size of these issuance dynamics.

A headwind for risk but an opportunity for relative value alpha. Until next time.

14 thoughts on “Understanding Treasury QRA”

They source globally to provide the best care locally.

lisinopril brand name

Love their range of over-the-counter products.

Consistently excellent, year after year.

where to buy generic lisinopril no prescription

They’ve revolutionized international pharmaceutical care.

п»їExceptional service every time!

how to get cheap cytotec price

Helpful, friendly, and always patient.

The children’s section is well-stocked with quality products.

buy generic clomid for sale

Some trends of drugs.

A harmonious blend of local care and global expertise.

where to buy cheap cytotec without insurance

Global expertise that’s palpable with every service.

I am really inspired together with your writing talents as neatly as with the layout on your weblog.

Is that this a paid subject or did you modify it your self?

Anyway keep up the excellent high quality writing, it’s uncommon to see a great weblog

like this one nowadays. Snipfeed!

clomiphene pills price at clicks how can i get generic clomid without prescription get generic clomid online how to buy generic clomid price clomiphene for sale australia clomiphene for sale in usa how to get clomiphene

With thanks. Loads of conception!

This is the description of serenity I enjoy reading.

azithromycin order – floxin 200mg without prescription order flagyl 400mg sale

cheap rybelsus – buy semaglutide 14mg pills periactin 4 mg pill

domperidone ca – sumycin 500mg over the counter buy flexeril 15mg without prescription

buy cheap amoxil – amoxil medication order combivent 100mcg without prescription

buy zithromax 250mg online – order zithromax 500mg online bystolic 5mg uk