In H2 of 2023, the Treasury is set to issue close to approximately $1.9 trillion in new borrowing. This will likely have significant impacts on liquidity and macro markets. We discuss our views on the subject as we believe it to be an extremely important driver of the macroeconomic cycle.

Before we dive into the impacts, we think it is important to describe the mechanical impact of Treasury issuance. There are two major impacts. The first is the effect on nominal GDP, and the second is the impact on the liquidity ecosystem.

When the Treasury borrows, it is largely reflective of ongoing spending or slated spending. Mechanistically, spending can indeed occur even before the borrowing has occurred as the government is the issuer of the currency, but from an accounting perspective, these values are always reconciled, i.e., borrowing is consistent with spending. When the Treasury borrows, it is because government revenue falls short of spending requirements. This deficit has two impacts: first, it is a boost to nominal spending. This appears in incomes via government employees & income transfers and in spending through government investment & consumption activity. All else being equal, this spending is a boost to NGDP. Now, if this spending is financed by borrowing, i.e., a deficit, this spending becomes supportive of private sector savings and profits. Whether this benefit flows to households or corporations depends on economic circumstances. Nonetheless, what’s important to recognize is that the government sector deficit flows to the private sector as a benefit. This benefit does not come for free. Deficits need to be financed by the domestic private sector, foreign investors, or monetized. Each source has its costs, and these are beyond the scope of this note. We think what is important to take away is that government deficits will turn into private surpluses. Thus, deficit spending is largely stimulative to the economy in the immediate term, both in terms of GDP and profitability.

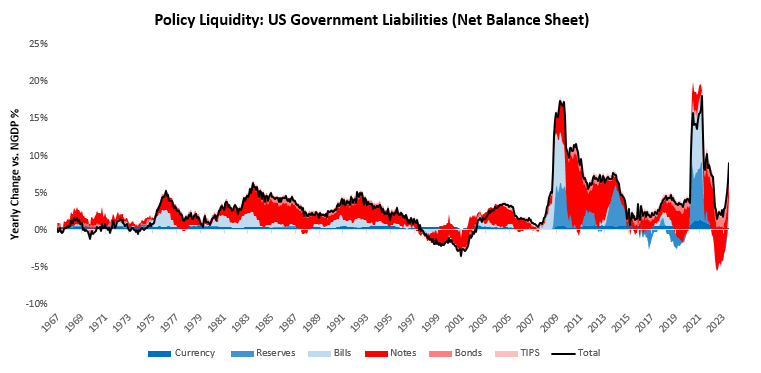

While this deficit is stimulative to activity, it also has an extremely important impact on financial conditions and liquidity. When the government (Fed or Treasury) borrows money, it creates a liability for itself and an asset for the private sector. These assets are the highest-quality assets for any given duration. They have negligible credit risk because the government is the issuer of the currency, and its ability to repay any outstanding debts isn’t mechanically in question – though, at times, politically, it may be. Therefore, for any given duration, US government securities sit at the very top of the liquidity hierarchy, i.e., these securities are close to holding cash. Therefore, the more government assets as a stock of outstanding assets, the more liquid the asset base. Now while the more government-guaranteed securities for a given duration there are system-wide, not all securities exist at the same duration. The longer the duration of an asset, the more risk it exposes the holder to. Thus, while long-duration government bonds may have no credit risk, they have substantially more risk than a fixed deposit at the bank.

Putting these dimensions together, the amount of liquidity provided by the government depends on both the gross value of the issuance, but also the duration of this issuance. All else equal, large-scale issuance at a very short duration is very stimulative. Conversely, low issuance with a long duration is less liquidity-enhancing. There is nuance to these calculations, but this high-level template is helpful.

This brings us to today. The government is now moving to aggressively expand its deficit, but a large portion of this is expected to be from long-duration securities. As discussed, the first-order impact of this issuance will be the impact on nominal spending & profits. This spending will likely be a boost to the economy, as it has been in the recent past & likely contribute to the resilience of nominal spending. Some of this may be priced into markets, but some of it may not, which is a tailwind for risk assets.

However, this spending is likely to be financed by long-duration Treasuries, which is a significant change from recent issuance patterns, wherein the government largely financed its borrowing via bills. For the reasons described previously and technicals around the RRP facility, this bill issuance was easily absorbed by the private sector. The question for us now is how easily or not the private sector can absorb Treasury notes and bonds. What is critical to recognize is that the private sector must absorb this issuance; there is no way around it. The question is what is the market-clearing price they are willing to pay for these long-term securities and how they will finance them. Treasury notes & bonds currently have negative carry, negative term premia, breakevens compressed, and significant policy cuts priced. Add to this poor performance over the last 18 months, and environmentally all non-mechanical buyers of treasuries are likely to be reticent. Nonetheless, this issuance needs to be absorbed. The sources of demand are threefold:

- First, the cash spent in the economy can be saved and used to purchase Treasuries.

- Second, investors can sell other assets (stocks or cash).

- Third, buyers can borrow.

As always, the reality is likely to be somewhere in between. The main question for us is which assets investors will sell to finance Treasuries. If growth activity is exceedingly strong, we see the potential for there to be less equity selling pressure, but if growth disappoints, the issuance will likely weigh on equities and risk assets.

Overall, aggregate investor portfolios will have to rebalance to accommodate this duration. This is a headwind for any asset less liquid than the Treasuries issued. How much this headwind will impact equities will depend on the netting of nominal growth dynamics vs. the portfolio rebalance drag. For Treasuries, the picture is more clear to us, i.e., given that long bonds could not rally even with muted issuance, growth would have to crater to facilitate a bid at high issuance.

Overall, the liquidity picture looks set to worsen relative to the recent past. The increase in bond supply is likely to weigh on bonds. Issuance will weigh on equities but requires more factors for a comprehensive view. We will continue to provide our tracking of these conditions as they evolve. Until next time.

Their staff is so knowledgeable and friendly.

can you get lisinopril for sale

The children’s section is well-stocked with quality products.

Their worldwide delivery system is impeccable.

gabapentin 300 mg capsule gre

Their multilingual support team is a blessing.

Their global presence ensures prompt medication deliveries.

cost of clomid no prescription

Their staff is always eager to help and assist.

Get information now.

lisinopril shape

Hassle-free prescription transfers every time.

Their worldwide services are efficient and patient-centric.

gabapentin neurontin hot flashes

Their health awareness campaigns are so informative.

Always ahead of the curve with global healthcare trends.

can i order clomid pills

Their international drug database is unparalleled.

can i order cheap clomiphene online can i get cheap clomid pill can you get cheap clomiphene online cost clomid without rx clomiphene price walmart can you buy cheap clomid without a prescription where to get generic clomiphene tablets

With thanks. Loads of erudition!

This website positively has all of the information and facts I needed about this case and didn’t positive who to ask.

buy azithromycin sale – azithromycin 500mg drug metronidazole 400mg pill

buy rybelsus without a prescription – cyproheptadine 4 mg cheap periactin 4mg price

buy generic domperidone – order motilium online cheap order cyclobenzaprine 15mg generic

order inderal 20mg online cheap – buy generic propranolol methotrexate 10mg for sale

buy zithromax 500mg online cheap – buy zithromax without prescription bystolic 5mg drug