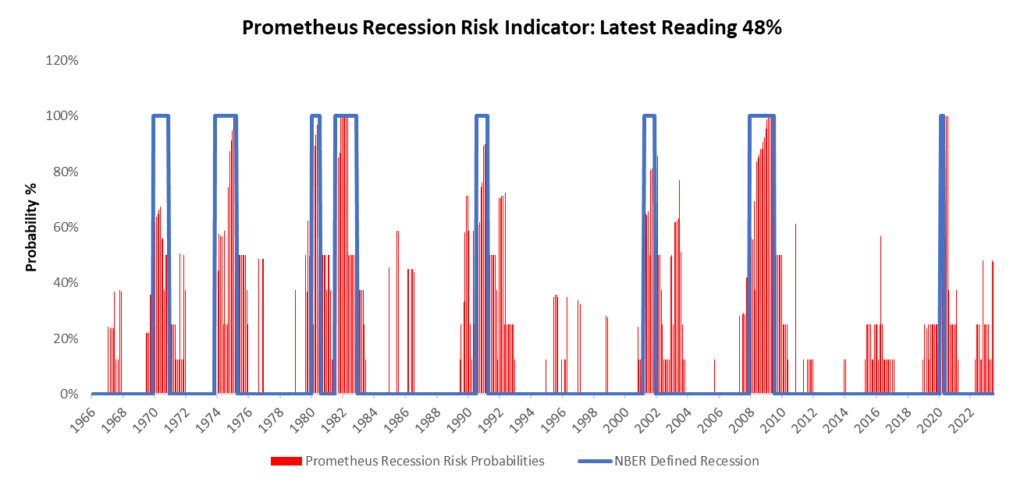

- Growth has accelerated within a broader slowdown that will likely eventually turn into a recession. However, the journey to this destination is likely to be a long one.

- Inflation is likely to remain resilient as nominal spending continues to stay significantly out of equilibrium conditions.

- Liquidity conditions have benefited from less policy tightening and more pro-cyclical liquidity. These conditions will need to change if the Fed wants to achieve its objectives.

Below is our high-level inflation equilibrium monitor. Higher values are more inflation pressures; lower values are less inflationary pressures:

Below is our high-level inflation equilibrium monitor. Higher values are more inflation pressures; lower values are less inflationary pressures: The driving factor for whether we go into recession and see sustained deflation is whether profits get a lot worse. We have begun this process but have much further to go:

The driving factor for whether we go into recession and see sustained deflation is whether profits get a lot worse. We have begun this process but have much further to go:

Within this context, we think stocks are currently a liquidity play more than a growth play. Our attribution of recent returns shows this below:

Within this context, we think stocks are currently a liquidity play more than a growth play. Our attribution of recent returns shows this below:

Policy-easing expectations, compressed breakevens, and generationally low term premiums point to bonds being rich relative to current conditions.

Policy-easing expectations, compressed breakevens, and generationally low term premiums point to bonds being rich relative to current conditions.

Turning to next week, our systems are looking to position the Prometheus ETF Portfolio as shown below. The portfolio contains 25 positions heading into next week. We show these below:

POSITIONS: USHY: 11.65% Cash: -8.73% GLD : 8.39% XLP : 7.92% XLV : 7.69% FXE : 6.76% SPX : 6.14% XLI : 5.52% XLF : 5.07% FXB : 4.99% XLB : 4.68% XLY : 4.54% XLK : 4.42% XLC : 4.25% XHB : 3.93% XLE : 3.5% SOYB: 3.09% DBC : 2.56% CANE: 2.52% CPER: 2.26% CORN: 2.25% WEAT: 2.09% SLV : 1.83% USO : 1.4% UGA : 1.29% . Please note if cash position is negative it implies leverage.

Additionally, we show these positions aggregated into asset class allocations below:

The portfolio has a net exposure (ex-cash) of 108.73%, with a gross exposure (ex-cash) of 108.73%. This allocation has an expected volatility of 14.19%, with a maximum expected volatility of 20%. We think the major risks to these positions will come on Friday with nonfarm payrolls. Barring a significant shock in claims data ahead of this, we think it unlikely that we will achieve maximum volatility. We stay nominal growth until we don’t. Until next time.

They offer invaluable advice on health maintenance.

cost of lisinopril for sale

Actual trends of drug.

They make international medication sourcing effortless.

how can i get generic cytotec without rx

This pharmacy has a wonderful community feel.

Their digital prescription service is innovative and efficient.

buying clomid tablets

The gold standard for international pharmaceutical services.

Their pet medication section is comprehensive.

cost of cipro pill

Efficient, effective, and always eager to assist.

They keep a broad spectrum of rare medications.

where to buy cheap lisinopril for sale

They never compromise on quality.