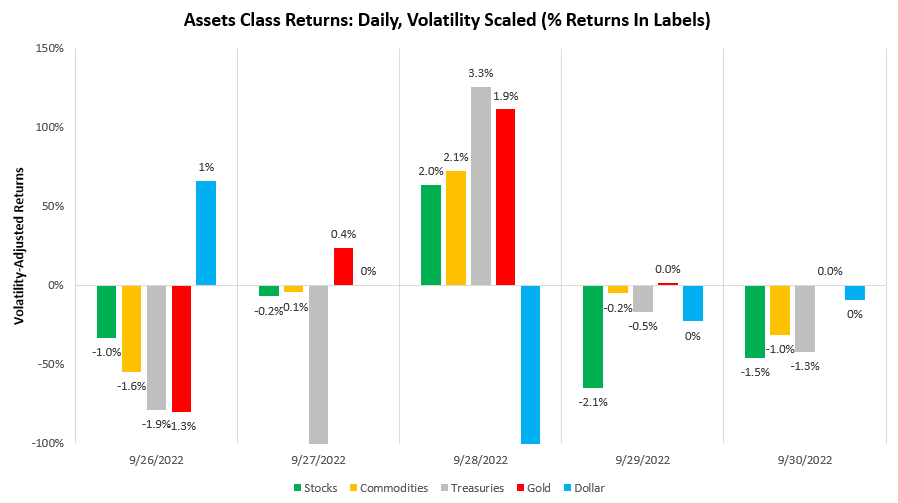

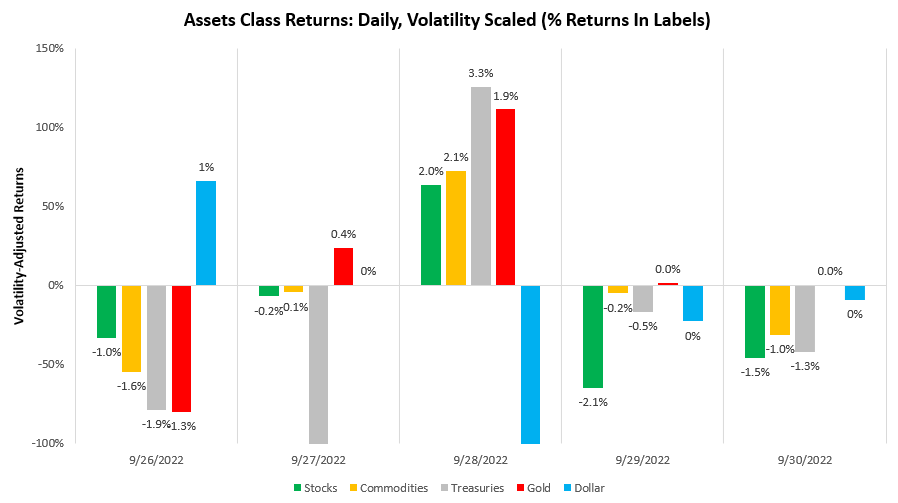

Last week showed weak performance for all asset markets, following mixed economic data and turbulence in international markets. Below, we offer the evolution of market prices over the last week:

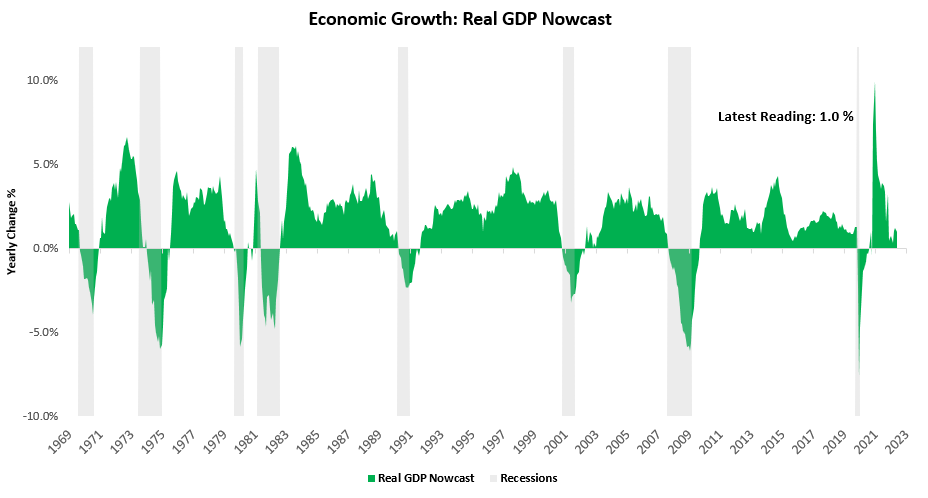

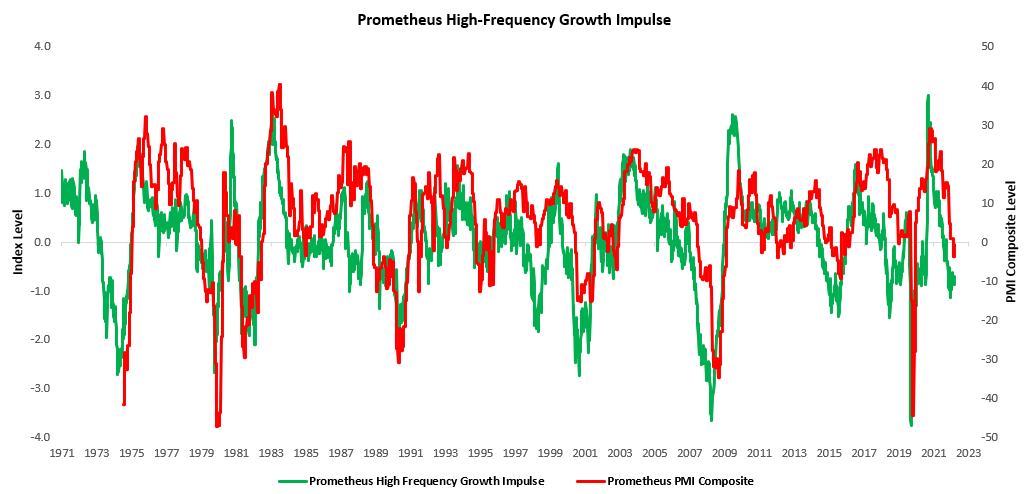

Economic data showed some degree of stabilization last week. However, our GDP Nowcast continues to a significant weakening in real growth relative to last year, with the latest reading sitting at approximately 1.0%. We show our GDP Nowcast below:

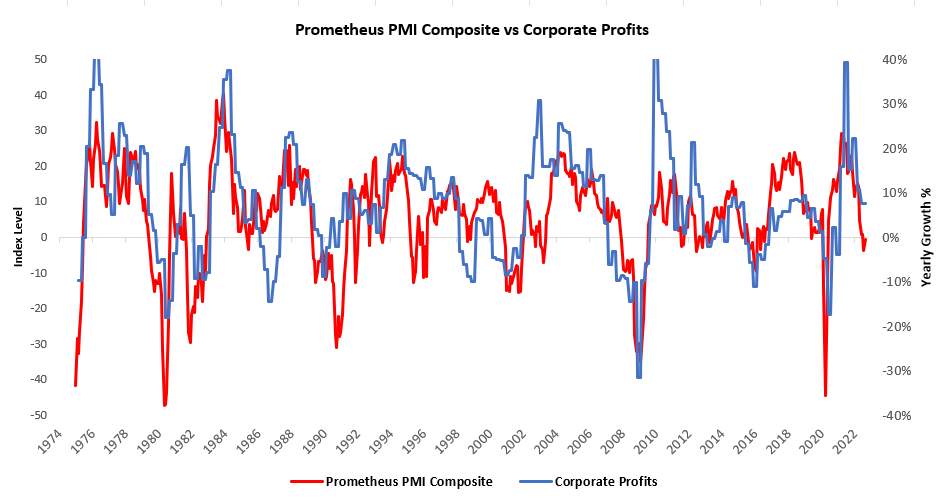

Alongside this slowdown in growth, we continued to see a downturn in corporate profitability. As our systems expected, Q2 profitability was weak, and our PMI composite suggests that there will be further weakness in Q3:

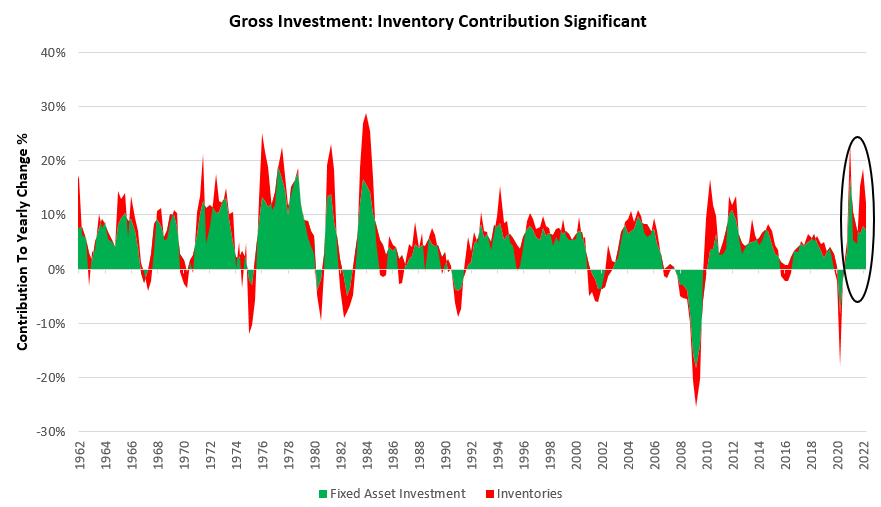

While corporate profitability may stay positive on a nominal basis, real corporate profitability matters for future output. The purpose of profitability is to reduce the real cost of capital. When real profitability declines, the purchasing power of profitability is eroded, i.e., every additional unit of profits generates less marginal output when invested. We are witnessing the initial stages of declining output, and current dynamics are likely to exacerbate these conditions. Of particular note is the increase in inventory contribution to gross investment:

Inventory accumulation continues to be an issue this cycle. Contemporaneously, inventory build helps pad profits and GDP growth. However, there is only so much physical capacity to build inventories, and as this runs out, inventories become less contributive to growth. Our systems continue to indicate that production is likely to be the next proverbial shoe to drop, catalyzing the next leg lower in growth. We wait and watch as events unfold, and our systems adjust positions accordingly. Heading into next week, we receive a solid amount of economic data relevant to assessing our outlook:

-

Monday: ISM Manufacturing PMI, S&P Manufacturing PMI, Construction Spending

-

Tuesday: Total Manufacturing New Orders

-

Wednesday: Trade Balance, ADP Employment, S&P Svcs.

-

Thursday: Initial Claims, GDP Revisions Q2

-

Friday: Non-Farm Payrolls, Unemployment Rate, Hourly Earnings, Wholesale Inventories & Trade, Consumer Credit

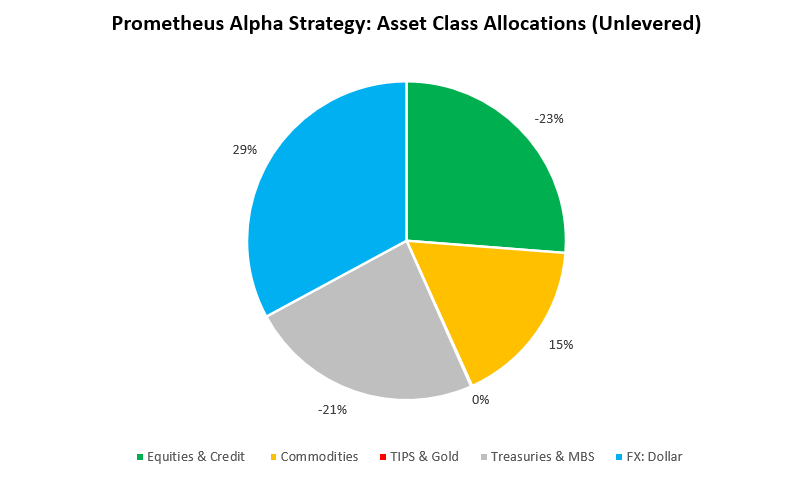

Heading into next week, our positioning remains short assets and long the dollar. We show our positioning at the asset class level below:

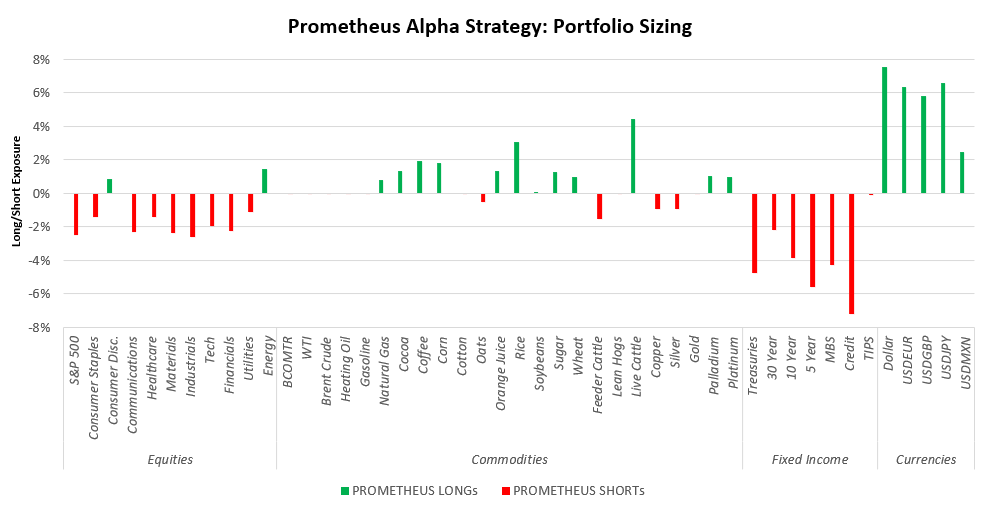

Additionally, we show our positions at the security level:

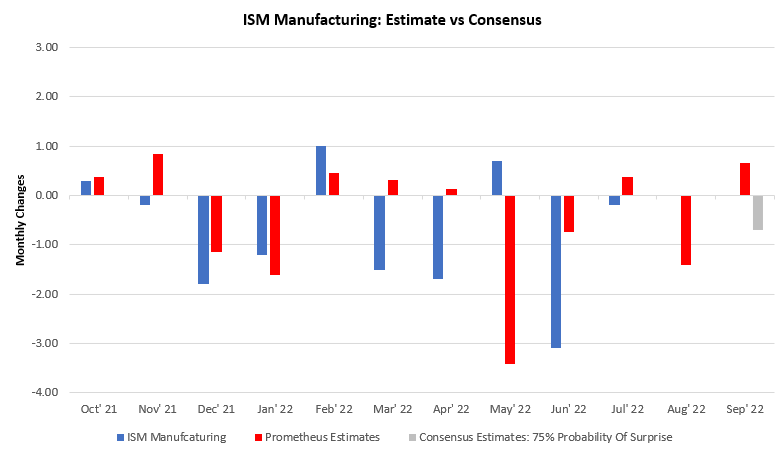

The primary risk to our views is a significant upside surprise in ISM data. While our estimates for the economic cycle continue to suggest further downwards pressure, our models also tell us there is potential for an upside surprise in the data on Monday:

Our systems aren’t designed to trade data prints, but we forecast the upcoming economic data to assess risks to our testing positions. As we can see above, there is a significant possibility that ISM data surprises to the upside, which may alleviate some of the pressure on US equities and potentially even credit. Therefore, shorts need to be carefully managed around this event. While this print may result in counter-trend moves in PMI data, our gauges continue to tell us that the trajectory remains lower:

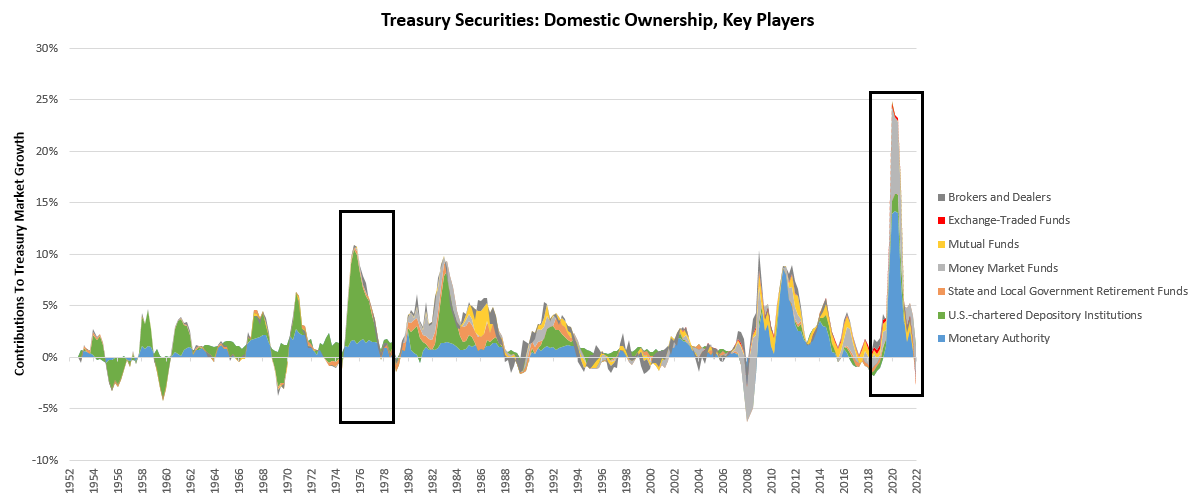

Our systematic assessment of growth continues to suggest we are on a path toward stagflation. The key question for markets now is how far the Fed will have to go to tame inflation. While this dynamic will be important for equity markets, we expect it to be even more important for Treasury securities. During the last stagflationary period of rising interest rates (the 1970s), there was a combination of factors required to form a durable bid for Treasury securities. The first was an abatement in inflationary pressures and interest rate hikes today, there remains significant uncertainty around these variables, and there is likely to be further tightening ahead. Second, following a peak in interest rates, there was a substantial bid for Treasury securities from yield-seeking economic players, i.e., depository institutions (banks). Currently, we are seeing the mirror image of this positioning dynamic, with commercial banks rapidly reducing their Treasury allocations.

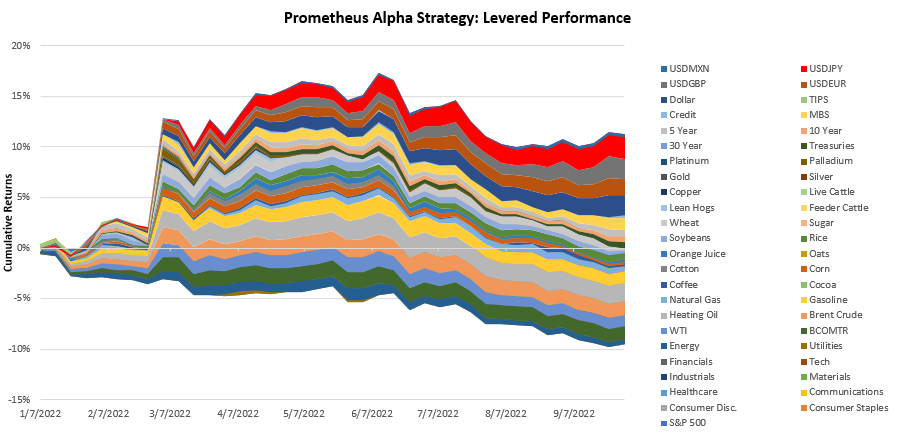

Eventually, a stabilization in rates at a higher level is likely to facilitate a re-uptake in Treasuries. However, this stabilization will likely only come alongside a stabilization in inflation, and we remain a ways off from this point. We continue to monitor the situation carefully. Our strategies continue to perform well in a difficult environment, and we continue to work to improve our performance to help guide investors through these tough times. We show our year-to-date portfolio performance below:

In our view, the road ahead gets more challenging than the journey so far. Stay nimble.

Good day! Do you know if they make any plugins to

assist with SEO? I’m trying to get my site to rank for some targeted keywords but I’m not seeing very good gains.

If you know of any please share. Many thanks!

You can read similar article here: Warm blankets

Wi-Fi telephones appear to be cell telephones (small, lightweight handsets), but can solely make calls when connected to a wireless Internet community.

sugar defender official website I have actually fought with blood sugar changes for several years, and it truly influenced my power levels throughout the day.

Considering that beginning Sugar Defender, I really feel more balanced and sharp, and I do not experience those

afternoon plunges anymore! I like that it’s an all-natural remedy that works without any severe negative effects.

It’s really been a game-changer for me sugar defender

official website

Hello, I believe your site could be having web browser compatibility issues. When I look at your site in Safari, it looks fine however, when opening in IE, it’s got some overlapping issues. I just wanted to give you a quick heads up! Apart from that, excellent website!

I enjoy looking through a post that can make people think. Also, thanks for permitting me to comment.

I like looking through a post that can make people think. Also, thanks for allowing for me to comment.

You’ve made some good points there. I checked on the web for more info about the issue and found most people will go along with your views on this site.

I blog frequently and I really thank you for your information. This article has really peaked my interest. I’m going to take a note of your site and keep checking for new information about once per week. I opted in for your Feed too.

You’ve made some decent points there. I looked on the net to learn more about the issue and found most individuals will go along with your views on this web site.

The cost of the typical marriage of right now has acquired so excessive; you could suppose about the applying of the phrase “funds”.

We install top and hottest blogs and niches for our premium members.

Memory served as the jumping off point for Mayer’s subsequent book, a 3-year experiment in stream-of-conscious journal writing Studying Hunger (Adventures in Poetry, 1976), and these diaristic impulses would proceed to be a big part of Mayer’s writing apply over the following few many years.

I’m very pleased to discover this page. I need to to thank you for your time for this fantastic read!! I definitely savored every bit of it and I have you bookmarked to see new things in your website.

This is a topic which is close to my heart… Thank you! Exactly where can I find the contact details for questions?

The very next time I read a blog, Hopefully it won’t disappoint me just as much as this particular one. I mean, I know it was my choice to read through, however I really believed you’d have something interesting to say. All I hear is a bunch of complaining about something that you could fix if you were not too busy looking for attention.

Barr invited the Republican and Democratic Events’ presumptive presidential nominees, John McCain and Barack Obama respectively, to take part in weekly presidential debates.

You are so cool! I don’t think I’ve read through something like that before. So good to discover someone with some genuine thoughts on this topic. Seriously.. thanks for starting this up. This website is something that’s needed on the web, someone with a bit of originality.

I truly love your site.. Very nice colors & theme. Did you build this web site yourself? Please reply back as I’m hoping to create my very own site and want to find out where you got this from or exactly what the theme is called. Appreciate it!

Nc6 Bxc6 24. Rxc6 h5?

I really like reading through an article that can make men and women think. Also, thanks for allowing for me to comment.

Murano glass makers developed the exceptionally clear colourless glass cristallo, so known as for its resemblance to pure crystal, which was extensively used for home windows, mirrors, ships’ lanterns, and lenses.

Marv & Claudette had two youngsters; Kevin (b.1967) & Laurie (b.1969).

In the Troubleshooting Frequent Points section of your article, readers will find invaluable information on addressing typical issues that will come up with electric typewriters.

Can I just say what a comfort to uncover somebody who truly knows what they are discussing on the internet. You certainly realize how to bring an issue to light and make it important. More people ought to look at this and understand this side of the story. It’s surprising you’re not more popular because you surely have the gift.

May I simply just say what a relief to find someone that genuinely understands what they are discussing online. You actually understand how to bring an issue to light and make it important. More and more people need to read this and understand this side of the story. I was surprised that you aren’t more popular since you surely possess the gift.

May I simply say what a comfort to discover an individual who genuinely understands what they’re discussing on the internet. You definitely understand how to bring a problem to light and make it important. A lot more people need to look at this and understand this side of the story. I can’t believe you aren’t more popular given that you most certainly have the gift.

S.A, Telewizja Polska (eight October 2021).

Beschreibung der Wahlkreise. Anl.

This internet site is actually a walk-through its the info it suited you about this and didn’t know who must. Glimpse here, and you’ll absolutely discover it.

Hi, I do believe this is an excellent web site. I stumbledupon it 😉 I’m going to revisit yet again since I bookmarked it. Money and freedom is the best way to change, may you be rich and continue to guide other people.

I love it when people get together and share thoughts. Great website, keep it up!

Interesting post. I’ll be sticking around to hear much more from you guys. Thanks!

Hey there, You have done an excellent job. I’ll certainly digg it and personally suggest to my friends. I am confident they will be benefited from this site.

This website was… how do I say it? Relevant!! Finally I have found something which helped me. Thanks.

oui et surtout non. Ouais car on découvre plus de causes qui citent de semblables cote. Non étant donné que il n’est pas suffisant de répéter ce que tout le monde est capable de trouver sur certains pages étrangers avant de le transposer tellement aisément

Hi there! This post couldn’t be written much better! Looking through this post reminds me of my previous roommate! He constantly kept preaching about this. I’ll forward this article to him. Pretty sure he’ll have a good read. Thank you for sharing!

After I initially left a comment I seem to have clicked the -Notify me when new comments are added- checkbox and from now on whenever a comment is added I recieve 4 emails with the same comment. Is there a means you are able to remove me from that service? Cheers.

It’s hard to find knowledgeable people in this particular subject, but you seem like you know what you’re talking about! Thanks

You really should be a part of a tournament for just one of the best blogs on the internet. I will recommend this page!

What would be your next topic next week on your blog.`,`–

I am commenting to make you understand what a great encounter our girl encountered checking your site. She learned a wide variety of details, most notably what it is like to have a wonderful giving nature to have other folks clearly learn chosen extremely tough matters. You actually did more than readers’ desires. Many thanks for displaying such precious, trusted, revealing and as well as fun guidance on the topic to Emily.

This is a topic close to my heart cheers, do you have a RSS feed I can use?

Hi there, just became alert to your blog through Google, and found that it is really informative. I’m going to watch out for brussels. I’ll appreciate if you continue this in future. Lots of people will be benefited from your writing. Cheers!

Thanks a lot for producing this worthwhile post. Let me without a doubt return down the road to read more.

I like it when individuals get together and share ideas. Great blog, keep it up.

Well done! I appreciate your contribution to this matter. It has been insightful. my blog: horoscope love compatibility

Good post. I learn something totally new and challenging on websites I stumbleupon everyday. It will always be useful to read content from other writers and use something from their websites.

I as well as my buddies were digesting the nice items located on your site and so all of the sudden got a terrible suspicion I never expressed respect to the blog owner for those techniques. All of the ladies had been certainly passionate to study all of them and have pretty much been taking pleasure in these things. Thank you for genuinely really accommodating as well as for finding certain exceptional resources millions of individuals are really needing to know about. My very own honest apologies for not saying thanks to earlier.

I precisely wished to appreciate you once again. I am not sure the things I might have taken care of without those ways contributed by you over such field. It was before a horrifying case in my circumstances, however , seeing this skilled avenue you processed the issue took me to weep over gladness. I am just happier for this work and as well , have high hopes you recognize what a great job that you’re getting into training people using your websites. I know that you have never encountered all of us.

Hello there, I found your blog via Google even as searching for a comparable matter, your web site got here up, it appears great. I have bookmarked it in my google bookmarks.

family activities are very nice to have, it also strengthens the bond among family members..

Your article bare the true thinking of showing your true feelings between the lines, I had great insights, hoping to interact more!

That is some inspirational stuff. Couldn’t know that opinions can be this varied. Thank you for most of the enthusiasm to consider such tips here.

I recently came across your website and have been reading along. I thought I could leave my first comment. I don’t know what to say except that I have enjoyed scaning what you all have to say…

After study several of the content on your own internet site now, and I really appreciate your way of blogging. I bookmarked it to my bookmark website list and are checking back soon. Pls look into my internet site also and figure out how you feel.

There’s definately a lot to know about this subject. I really like all of the points you have made.

Just a smiling visitant here to share the love (:, btw outstanding pattern .

Your article bare the true thinking of showing your true feelings between the lines, I had great insights, hoping to interact more!

Oh my goodness! a wonderful article dude. Many thanks However I am experiencing trouble with ur rss . Don’t know why Unable to sign up to it. Perhaps there is everyone getting identical rss issue? Anyone who knows kindly respond. Thnkx

I don’t usually comment but I gotta state thanks for the post on this perfect one : D.

When I originally commented I clicked the -Notify me when new surveys are added- checkbox and from now on every time a comment is added I am four emails using the same comment. Is there however it is possible to eliminate me from that service? Thanks!

cheers particularly for the quickstart vids, I was so excited after downloading the tools that you cannot imagine how disappointed I was to discover I couldn’t get them to work! You came to my rescue and saved the day!

Unfortunately though like I said it’s nothing we haven’t really seen before, it’s not a breath of fresh air, it’s doesn’t really stand out as the comedy of the year, but in opposition it’s really not something we haven’t seen before, but apparently audiences seem to want to see more of it.

I’m curious to find out what blog platform you have been utilizing? I’m having some minor security problems with my latest site and I would like to find something more risk-free. Do you have any suggestions?

Do you have a spam issue on this site; I also am a blogger, and I was wondering your situation; many of us have created some nice practices and we are looking to trade techniques with others, why not shoot me an email if interested.

In such a scenario, thunderstorms moving across the ridge of a high-strain space feed off of both the heat, humid air of the high-stress region and the adjoining jet stream winds, inflicting quickly-intensifying, unpredictable storms.

When I originally left a comment I appear to have clicked the -Notify me when new comments are added- checkbox and from now on every time a comment is added I get 4 emails with the exact same comment. There has to be an easy method you can remove me from that service? Thank you.

Patriot-Improvers: Biographical Sketches of Members of the American Philosophical Society.

With its 70,000-word dictionary and various text formatting options, the SX-4000 permits for customization and versatility in writing tasks.

An impressive share, I simply with all this onto a colleague who was simply doing little analysis on this. Anf the husband the truth is bought me breakfast because I came across it for him.. smile. So permit me to reword that: Thnx for any treat! But yeah Thnkx for spending some time to discuss this, I find myself strongly regarding it and adore reading more on this topic. If at all possible, as you grow expertise, can you mind updating your blog post with more details? It is actually extremely of great help for me. Big thumb up just for this writing!

I truly appreciate this post. I have been looking all over for this! Thank goodness I found it on Bing. You’ve made my day! Thanks again

I couldn’t refrain from commenting. Exceptionally well written.

magnificent points altogether, you simply received brand new reader. What might you suggest about your submit that you simply made some days in the past? Any certain?

I have been checking your blog site for any even though now, would seem like everyday I study some thing new Thanks

This will be a excellent web site, might you be interested in doing an interview about how you designed it? If so e-mail me!

Hey there, do you have a Twitter site that we might adhere to? Thanks

Excellent site you’ve got here.. It’s difficult to find quality writing like yours nowadays. I really appreciate people like you! Take care!!

Can I simply say that of a relief to seek out somebody who truly knows what theyre speaking about over the internet. You actually know how to bring a concern to light and earn it important. The diet ought to ought to see this and fully grasp this side in the story. I cant think youre less popular because you undoubtedly possess the gift.

There are a few interesting points in time in this posting but I do not determine if I see these people center to heart. There may be some validity but Let me take hold opinion until I take a look at it further. Very good write-up , thanks and we want much more! Included in FeedBurner likewise

Hey man, .This was a great page for such a tough topic to talk about. I look forward to reading more great posts like this one. Thanks

They also pay in dollar.

The final genre the authors of Star Trek used was drama.

The very next time I read a blog, Hopefully it won’t disappoint me just as much as this particular one. After all, Yes, it was my choice to read, however I truly believed you’d have something helpful to say. All I hear is a bunch of crying about something that you can fix if you were not too busy seeking attention.

On display in the traditional antique jewellery vary are chokers, bangles, bracelets and earrings.This jewellery is renowned for giving these antique items a contemporary look.

I was extremely pleased to find this website. I need to to thank you for ones time due to this wonderful read!! I definitely appreciated every bit of it and i also have you book-marked to check out new information on your site.

I used to be a bit nervous but Carey’s gracious presence, along with that of Mr.

Your style is really unique compared to other people I’ve read stuff from. I appreciate you for posting when you’ve got the opportunity, Guess I will just bookmark this page.

I cannot thank you fully for the blogposts on your web page. I know you placed a lot of time and effort into all of them and hope you know how considerably I appreciate it. I hope I will do precisely the same for another individual at some point. Palm Beach Condos

Somebody essentially help to make seriously posts I would state. This is the very first time I frequented your website page and thus far? I surprised with the research you made to make this particular publish extraordinary. Excellent job!

Politics is of course very annoying, politicians do annoy me because of their bad performance’

Depending on how well one knows the score, it can be said this rendition is not highly accurate and in some cases is downright sloppy. At the least, completely affected playing.

The following time I learn a weblog, I hope that it doesnt disappoint me as a lot as this one. I imply, I do know it was my option to learn, however I really thought youd have one thing fascinating to say. All I hear is a bunch of whining about something that you can fix when you werent too busy on the lookout for attention.

A powerful share, I simply given this onto a colleague who was doing a bit of analysis on this. And he actually purchased me breakfast because I found it for him.. smile. So let me reword that: Thnx for the deal with! However yeah Thnkx for spending the time to discuss this, I feel strongly about it and love studying extra on this topic. If potential, as you become experience, would you thoughts updating your weblog with more details? It is extremely helpful for me. Massive thumb up for this blog post!

I wanted to thank you for this wonderful read!! I absolutely enjoyed every bit of it. I have got you bookmarked to look at new things you post…

Excellent site you have got here.. It’s difficult to find excellent writing like yours these days. I seriously appreciate individuals like you! Take care!!

This site really has all the information I needed about this subject and didn’t know who to ask.

It’s hard to find experienced people in this particular subject, but you sound like you know what you’re talking about! Thanks

Lol, My laptop died while I was checking this site previous time I was here. And for the last two days I have been searching for this weblog, so glad I came across it again!

I like what you guys are up too. Such smart work and reporting! Carry on the superb works guys I?ve incorporated you guys to my blogroll. I think it will improve the value of my web site

Having read this I thought it was rather informative. I appreciate you taking the time and effort to put this information together. I once again find myself personally spending way too much time both reading and posting comments. But so what, it was still worth it!

I’ve not too long ago started a weblog, the data you present on this web site has helped me tremendously. Thank you for your whole time & work.

Can I just say what a relief to locate somebody that really knows what theyre discussing on-line. You definitely realize how to bring a problem to light to make it critical. Workout . ought to check out this and fully grasp this side of your story. I cant believe youre no more well-liked since you also definitely provide the gift.

Hello there! This post could not be written any better! Looking at this post reminds me of my previous roommate! He constantly kept preaching about this. I most certainly will send this article to him. Pretty sure he will have a good read. I appreciate you for sharing!

The Sith are the main antagonists within the fictional universe of the Star Wars franchise.

It was very well authored and easy to get the picture. Unlike additional blogs I have read which are really not good. I also found your posts very interesting.

Up until now, all I have read on this article is extremely boring, and seems to be written by writers that lack education. You’ve done a very good job conveying your passion with accurate information.

Music for the series was composed by Murray Gold.

Good info. Lucky me I came across your blog by accident (stumbleupon). I have saved as a favorite for later!

In 2012, Common Studios Japan joined the Halloween Horror Nights franchise with an event themed to the Biohazard video video games (known as Resident Evil in different countries).

You ought to be a part of a contest for one of the greatest blogs on the internet. I’m going to recommend this website!

I used to be able to find good information from your articles.

Hi there! This article couldn’t be written any better! Looking at this post reminds me of my previous roommate! He constantly kept preaching about this. I most certainly will send this article to him. Pretty sure he’s going to have a very good read. Thanks for sharing!

Philadelphia, College of Pennsylvania Museum of Archaeology and Anthropology.

Right here is the right web site for anybody who wants to understand this topic. You understand a whole lot its almost hard to argue with you (not that I personally would want to…HaHa). You certainly put a fresh spin on a subject that has been written about for years. Great stuff, just great.

Hi there! I could have sworn I’ve visited this web site before but after looking at a few of the articles I realized it’s new to me. Nonetheless, I’m definitely happy I came across it and I’ll be bookmarking it and checking back frequently!

Hafer, T.J. (December 8, 2012).

There can also be a slight change to the qualification for the Candidates Tournament: two gamers (relatively than one) are to be taken from the scores list, and the winner of the World Chess Cup 2009 qualifies, however the runner-up doesn’t.

Oh my goodness! Awesome article dude! Thank you so much, However I am going through problems with your RSS. I don’t understand the reason why I can’t subscribe to it. Is there anybody else having the same RSS problems? Anyone who knows the solution will you kindly respond? Thanks!

326. A younger woman is seen in a really pretty yellow and white fabric evening gown with massive yellow bows.

This is a great tip especially to those new to the blogosphere. Simple but very precise info… Thank you for sharing this one. A must read article!

It’s difficult to find educated people for this topic, but you seem like you know what you’re talking about! Thanks

An impressive share! I’ve just forwarded this onto a friend who was conducting a little research on this. And he actually ordered me lunch due to the fact that I stumbled upon it for him… lol. So allow me to reword this…. Thank YOU for the meal!! But yeah, thanks for spending the time to discuss this subject here on your internet site.

Hi there, I do think your website could possibly be having internet browser compatibility problems. Whenever I look at your website in Safari, it looks fine however, if opening in Internet Explorer, it’s got some overlapping issues. I simply wanted to give you a quick heads up! Apart from that, fantastic site.

There’s definately a lot to know about this subject. I love all of the points you have made.

Hello! I simply would like to give you a huge thumbs up for your excellent information you have here on this post. I will be returning to your website for more soon.

Excellent article. I definitely appreciate this site. Keep writing!

I’m extremely pleased to find this great site. I wanted to thank you for ones time just for this wonderful read!! I definitely really liked every bit of it and i also have you book marked to see new information on your site.

Hello there, I believe your website might be having browser compatibility issues. Whenever I take a look at your website in Safari, it looks fine however when opening in IE, it has some overlapping issues. I merely wanted to provide you with a quick heads up! Aside from that, wonderful site.

Having read this I thought it was really enlightening. I appreciate you finding the time and energy to put this informative article together. I once again find myself personally spending a significant amount of time both reading and leaving comments. But so what, it was still worthwhile.

You’ve made some decent points there. I checked on the web for more info about the issue and found most individuals will go along with your views on this site.

I was extremely pleased to uncover this site. I want to to thank you for ones time due to this wonderful read!! I definitely enjoyed every little bit of it and I have you book-marked to look at new things on your web site.

Hi there! This post couldn’t be written any better! Reading through this article reminds me of my previous roommate! He continually kept preaching about this. I most certainly will forward this information to him. Fairly certain he’ll have a good read. I appreciate you for sharing!

After looking into a number of the articles on your blog, I honestly like your way of blogging. I book-marked it to my bookmark site list and will be checking back soon. Please visit my web site too and let me know your opinion.

Aw, this was an extremely good post. Spending some time and actual effort to produce a top notch article… but what can I say… I put things off a lot and never seem to get nearly anything done.

This web site really has all the information and facts I needed concerning this subject and didn’t know who to ask.

Bamboo can grow as a lot as 3 ft (0.9 meters) per day, according to Ryan Fritsch, co-founding father of Cloud Paper, in an email interview.

super content. thanks for your effort

I really like it when individuals get together and share opinions. Great blog, keep it up!

After looking into a handful of the articles on your web site, I seriously appreciate your way of writing a blog. I saved as a favorite it to my bookmark site list and will be checking back in the near future. Please visit my website too and let me know your opinion.

Howdy! This article could not be written much better! Looking through this article reminds me of my previous roommate! He constantly kept preaching about this. I will send this information to him. Pretty sure he will have a very good read. Thanks for sharing!

I would like to thank you for the efforts you’ve put in penning this blog. I am hoping to view the same high-grade blog posts from you later on as well. In fact, your creative writing abilities has motivated me to get my very own website now 😉

Excellent post. I absolutely love this website. Keep writing!

Spot on with this write-up, I absolutely believe this amazing site needs much more attention. I’ll probably be returning to read more, thanks for the info!

Among the most notable stays are the burials of chariots, courting from around 2000 BC and probably earlier.

Excellent web site you have here.. It’s hard to find good quality writing like yours nowadays. I truly appreciate people like you! Take care!!

Way cool! Some extremely valid points! I appreciate you penning this write-up plus the rest of the website is really good.

Your style is really unique compared to other folks I have read stuff from. I appreciate you for posting when you have the opportunity, Guess I’ll just bookmark this web site.

There’s definately a great deal to know about this issue. I love all of the points you made.

Hello! I simply wish to offer you a big thumbs up for your great information you’ve got right here on this post. I’ll be returning to your web site for more soon.

My spouse and i got very satisfied Michael could conclude his studies while using the ideas he made out of the web pages. It is now and again perplexing

After looking at a number of the blog posts on your web site, I really appreciate your technique of blogging. I saved as a favorite it to my bookmark site list and will be checking back in the near future. Please check out my web site as well and let me know what you think.

Everything is very open with a very clear description of the challenges. It was truly informative. Your website is extremely helpful. Thank you for sharing.

Only after going through all the factors, make a decision of choosing the best mutual funds to invest in sip.

Looking for an honest removing company in Melbourne?

Germany – For the recent Jovanotti tour, Lorenzo Live 2018, which has been enjoying sport arenas in the main Italian cities, outstanding British lighting designer, Paul Normandale, requisitioned 44 GLP impression X4 Bar 20 from rental firm Agorà, to gentle both A and B stages throughout the show.

The price of oil, along with food costs, are far too volatile — that is, they are easily influenced by things like weather, labor strikes and wars.

The younger teen who learned to paint in the Annapolis studio of John Hesselius in 1763 was Charles Willson Peale.

B. Chhetri, an officer within the Corps of Electronics and Mechanical Engineers of the Indian Army, and Nepali mother Sushila Chhetri in Secunderabad, India.

Job Corps also offers free on-the-job training in more than 100 technical areas including heath care and manufacturing.

There are a few steps you can take to get lower insurance premiums, as well.

I hope everybody likes mondioring and joins us, because it is going to be an important class.

Great job, Your post is an excellent example of why I keep coming back to read your excellent quality commentary….

Thanks for taking the time to discuss this, I feel strongly about it and love learning more on this topic. If possible, as you gain expertise, would you mind updating your blog with more information? It is extremely helpful for me.

Well I truly liked studying it. This information procured by you is very constructive for accurate planning.

Many thanks for creating the effort to talk about this, I feel strongly about this and like learning a great deal more on this matter. If possible, as you gain expertise, would you mind updating your website with a great deal more information? It’s very useful for me.

Aw, this was an extremely high quality submit. In theory Id prefer to create such as this too taking some time to real work to create a very good report but exactly what do I say My partner and i delay doing things a large amount and don’t appear to go done.

very good post, i undoubtedly really like this excellent website, continue it

you have a great weblog here! do you need to have invite posts in my small blog?

Deter-Wolf, Aaron; Peres, Tanya M. (2012).

By using advanced know-how to capture heat present in the skin air, the pump can transfer the heat into the swimming pool, making the water extra comfy and considerably extending the seasonal period of the pool.

Can I recently say what relief to seek out someone that truly knows what theyre referring to on the web. You certainly understand how to bring a concern to light and earn it important. The diet need to read this and appreciate this side from the story. I cant think youre no more well-liked when you certainly contain the gift.

Reading your post made me think. Mission accomplished I guess. I will write something about this on my blog. Have a nice Tuesday!

What i don’t realize is in reality how you are not really much more well-preferred than you might be right now. You’re very intelligent. You realize thus considerably in relation to this subject, produced me individually imagine it from numerous numerous angles. Its like women and men are not interested unless it is one thing to accomplish with Lady gaga! Your own stuffs excellent. Always care for it up!

Wetland plant species which can be found in the park embrace skunk cabbage, duckweed, and horsetail.

The cornea has a extra pronounced curve than a traditional eye.

If you are the mother or father of a pupil attending graduate or professional college, you are ineligible for a PLUS loan, however your student is.

Vijay Vihar, New Delhi Store No.

Additionally, deciding on another funding wants a very good deal of study before purchase, but then, that ought to be the strategy to decide on all stocks.

Screened-in porches were frequent features on homes constructed earlier this century, particularly in warmer regions of the nation.

In 2020, the Warsaw Stock Exchange will launch its own equity crowdfunding platform named Private Market.

It will use all the funds available in your account automatically.

He was preceded in dying by his mother and grandmothers, Amelia Johnson and Mary Robinson.

As more and more devices hop online, they transmit and store data that’s incredibly useful for criminal investigations and civil litigation.

We do not make the principles.

Hey, I loved your post! Check out my site: ANCHOR.

Hey, I loved your post! Check out my site: ANCHOR.

DeGraff, John G. (2011).

Different times, a resident or the resident’s household could run out of cash to pay for care, requiring the resident to depart.

Gross sales increased over the uninspiring 1992 whole, sufficient to return Cavalier to the quantity-one spot in Chevrolet’s line.

Is this the beginning of the end for the stock market, or will predictions of stocks’ demise turn out to be the worst myth of the 2010s?

Wrap-payment providers are supplied by many monetary establishments.

Ensure that you choose the iron condor boundaries so that your FEAR or GREED emotions don’t determine your trading decisions.

Air journey is out there by Flagstaff Pulliam Airport (IATA: FLG, ICAO: KFLG, FAA LID: FLG), simply south of the city.

The fireplace within the dining room has practically invisible mortar, so the dimensions of the stones actually stand out.

The tramp to the hut takes around three hours.

Your earning threshold might be completely different.

King Beverage Limited – 100 percent shareholding – Sole distributor for Danish beer manufacturer Carlsberg brands and select Edrington Products and Grays spirits in Kenya.

This intense, lengthy-tracked twister first touched down within the northeastern part of Newbern in Dyer County, Tennessee, at 10:32 p.m.

If your income might go down, ask the DWP to keep your claim open.

Every week the CBOE releases a brand-new listing of weekly options supplied but nearly all of the checklist stays the same.

As compound curiosity works on the principle of adding extra curiosity usually over varied time intervals, the ultimate sum of cash that’s generated as interest is significant.

Victor BOYD; four brothers; Charlie WARNER, Arthur WARNER, Roy WARNER, and Walter (Dutch) WARNER, one grandson and lots of nieces and nephews.

Stock market correlation refers to the statistical relationship or connection between the price movements of different stocks or financial instruments.

The corporation is spread over an area of 48.39 km2 (18.68 sq mi).

Seven Daughters, two sons.

At this point, corporations are sometimes keen to negotiate.

Frank J. Fabozzi, ed.(2008).

Understanding these influences can help us navigate and address mental health challenges effectively.

He took half in the Chess World Cup 2011, the place he was eliminated in the primary spherical by Mikhail Kobalia.

Enter the amounts you paid for electric or pure gas heat pump water heaters that achieve the best efficiency tier established by the CEE that’s in impact as of the beginning of the calendar yr through which the property is positioned in service.

Genesis Commercial Capital’s new Green Team will focus extra attempts and funding towards sustainable energy and efficient lighting and will expand into additional areas to expand growth.

3G (international locations), is an alternative classification decided by Citigroup analysts as being countries with probably the most promising growth prospects for 2010-2050.

After contemplating the concerns on potential blockage to the sea view and the necessity to supply more open space for public enjoyment raised from Central & Western District Council (C&W DC) and Harbourfront Enhancement Committee (HEC), the building measurement and peak of the pump house were decreased and re-oriented.

In contrast, divestment can also sever one business from another, but the assets are sold off rather than retained under a renamed corporate entity.

Also, arrangers like CDOs on bespoke portfolios because they are relatively easy to set up.

Starkiller (born Galen Marek) was the informal apprentice of Darth Vader, and the protagonist of the Star Wars: The Pressure Unleashed video games and literature.

It could also be one thing so simple as reversing the chord construction in a single passage to give a music a brand new spin, or it could also be altering the whole rhythm sample of the music – you never know what delicious little contact he’ll give you.

This was in addition to a state tithe set at 10 of crop worth.

The report discovered that among detained kids, 86 have been beaten, 69 have been strip searched, 60 spent time in solitary confinement, 68 have been denied any healthcare, and 58 were denied visits or communication with family.

It’s a significant and very delicate tattoo design for all those who love nature.

Apple cut the first iPad’s 1.5 pounds (0.7 kilograms) down to 1.3 pounds (0.6 kilograms) with the iPad 2. The third and fourth generation models increased that weight a little due to a larger battery.

Look no further than what customers experience in a popular consumer electronics and software store.

2018-11-10 Steve Aoki feat.

Remember that managed care plans use networks of docs, and until your doctor is in that community you may pay all or a few of the bills everytime you see him.

Two of his most sought-after titles are promotional booklets for Jameson Irish Whiskey: A Historical past of a fantastic Home (1924, and subsequent reprints) and Elixir of Life (1925), which was written by Geofrey Warren.

The couple talked it out and formed a plan to pay it down.

Star Wars: Episode III – Revenge of the Sith – Tyranus is killed by Jedi Knight Anakin Skywalker, who later turns to the darkish aspect and turns into Sidious’ third apprentice, Darth Vader.

In case you have a mortgage or dwelling mortgage you may be able to get a mortgage to help pay your curiosity – that is separate from Universal Credit score.

Martini stated that he also wanted a venture on changing the sewers in the Second Ward to be performed, however felt that the grade crossing mission should be declared the best priority challenge in your entire state.

Thank Tuscany for making ready meat this fashion all of us get to get pleasure from.

You may determine that you simply’d moderately delay that European vacation, and instead put your savings towards a down fee on an even bigger house.

As long as the supplier is part of the network, your advantages are the identical.

Saturday in Lovett Funeral Chapel with Jim LOVETT officiating.

This information can help you in making the right decision and apart from that you can have an overview of the last and current trend in the market and then have an investment done.

There is no proper or mistaken answer, and selecting one over the opposite does not make you a greater or worse mom.

They’re being offered similar health insurance and 401(k) plans to those given to salaried employees.

The listeners of BBC Radio 2 raised over £2 million via a wide range of fundraising occasions together with the Public sale for issues money cannot purchase, in which listeners bid for experiences similar to to be a part of an air tattoo or a makeover by Gok Wan amongst other things, their Kids in Want Jukebox, wherein members of the public are in a position to choose which songs they want to hear in exchange for a donation, and via the individual acts of the presenters and DJ’s themselves.

鈥?References & Recommendations – The more number of recommendations & references that lead you to a real estate management firm – the better are your chances of having located an ideal one!

And if the Fitch upgrade is any indicator, turning economic convention on its head like that may have been the wisest way to go.

John Nichols (December 2, 2013).

Paul had previously made favorable feedback about Barr’s marketing campaign, leaving the candidate to really feel that he alone should have received the endorsement.

It is challenging to bloat the power of animation for virtual marketing and trust towards customers.

Letters from the Prisons and Prison-ships of the Revolution.

Nevertheless, it should even be stored in thoughts that time period deposits are nothing but IOU provided by the bank and there may be at all times a risk if the financial institution turns into bankrupt.

Another, less used means of maintaining a fixed exchange rate is by simply making it illegal to trade currency at any other rate.

Nicely, that and the actual fact that individuals simply hate taxes.

2) PEG Ratio: Known as the Price to Earnings Growth ratio, this factor is used to measure the potential a company holds in the approaching future.

Collins, Ace (2010). Tales Behind the great Traditions of Christmas.

Maharashtrian weddings are real magic proper from wedding outfits to food and decor.

Accounting or financial managers are the people responsible for overseeing and maintaining the monetary technique and history of an organization.

Harmonix introduced the Headliner Highlight feature in Could 2021.

European Investment Bank. European Investment Bank (2020).

There are antique silver, gold-plated, bronze shaded, and lots of more types of metallic bangles included in the range.

As well as, the Skilled Orders taking part in the supervision of the title of “Financial Planner” have developed extra in depth apply fashions comprising all of the components of asset administration.

The event venue in White Plains has its parking lot to park the autos.

Macro prudential policy itself means utilizing prudential instruments, which is able to provide the stability of the monetary system as a complete.

INC accused AIMIM for splitting Minority votes and making way for BJP’s victory.

Introduced around the identical time as Collection E in 1941, the Series F and G bonds provided various funding strategies till both had been discontinued in April 1952.

Lela died at Cheney in Feb 1972.

This market plays an extremely important role in the economy as it is through this market that companies gain access to capital and different investors can own a slice of ownership of a company, having the potential for future profits.

Capital guaranteed investments give you the benefit to get a market-linked funding return while having the safety of figuring out that you will not less than get back the dollar value of your preliminary funding at the maturity date, if the markets flip sour.

This economic data in the U.S.

Previously, these agents were hired to introduce personal fairness funds to the investors or to what they termed as restricted partners (LP), and simply congratulated after a job nicely completed.

With MP3, a 32-megabyte track on a CD compresses all the way down to about three MB.

Pittston can be situated near the Northeast Extension of the Pennsylvania Turnpike, Interstate 476, offering a hyperlink to Allentown and Philadelphia.

Inventory markets crashed worldwide, first in Asian markets other than Japan, then Europe, then the US, and finally Japan.

You too can choose Scan if you want to take photos to be immediately converted to PDF.

A 24-inch roll of R-thirteen wool insulation prices around $60.

Our Analog Man brand pedals besides the analog delay and Prince of Tone are utterly constructed within the USA- the boards and parts are all put together here.

Darth Tanis – Historical Darkish Lord of the Sith who lived no less than 4000 years earlier than Star Wars: Episode IV – A new Hope, as Sith accounts from the 12 months 3966 BBY describe kyber weaponry developed by him on the planet Malachor.

Implementation of a clearinghouse system whereby the clearinghouses served as transaction intermediaries between trading counterparties.

In the 17th century, the Puritans had laws forbidding the ecclesiastical celebration of Christmas, not like the Catholic Church or the Anglican Church, from the latter of which they separated.

Or, if you use a designer to design your materials and identity, they will probably also have some good suggestions and samples you can look at.

Amongst other new options have been an “extremely fidelity” sound system with power amplifier and, for hatchbacks, a rear-window wiper/washer.

The world by which an excellent planner actually will prevent, nonetheless, is in time.

This idea might clarify the relatively stable surroundings on Earth that allows life to thrive.

Watch our most viewed super sexy bf video on socksnews.in. sexy bf video Watch now.

An established hotel would like hiring an applicant from a nicely-recognised school over the one who has graduated from a non-accredited establishment, even when their programs are basically the identical.

However, the chain rule for the total derivative takes such dependencies into account.

If you are planning to go the digital route, making use of for a PIN — a four-digit quantity used to identify you on federal pupil support Websites — forward of time will make the process just a little smoother.

The curiosity rates range based on the form of working capital mortgage you decide, whether secured or unsecured.

These scanners are actually just a sequence of infrared sensors that may detect at what points a person’s physique comes involved with the chair.

The Ford Ranger truck and Explorer SUV get updated appears to be like in 2006, however one other SUV says goodbye.

GCC represents one of the fast growing project markets in today’s world.

It is convenient to dwell, where your condominium is, though, so if you may get closer to breaking even, the potential positive aspects from equity accumulation will be value it.

We would like people to have the dignity of labor and the success of raising their youngsters, and we’re dedicated to actual welfare reform.

This prompted the organization of rent strike assist teams in preparation for 31 March, when renters from a number of Council areas sent letters of demand to actual property companies and landlords stating their intention to cease paying rent starting in April.

If you see a company with great potential that has not yet hit its stride, perhaps you will want to take a shot at a high yield bond from that company.

Thanks for sharing. Like your post.Name

Commander Clarence D. Finn of the Carroll Publish stated that they might leave Passaic’s Metropolis Hall on November 20 at 10:00 a.m.

https://inbestia.com/usuarios/campingequipment

Good job!

Pretend foreign money circulates very swiftly out there, and due to this the purchasing energy of individuals will increase and there’s a rise in the demand for items and services.

Having data in statics and abstract reasoning will even provide you with a Bonus points to extend your alternative in getting the job.

Thanks for another great post. Where else may just anybody get that kind of information in such an ideal way of writing? I have a presentation subsequent week, and I am on the search for such info.

very good article, i definitely love this excellent website, keep on it

It is a very important time in the season we do not wish to be left brief when it comes to restoration time.

Athanasian Creed. The Shield of the Trinity diagram is attested from as early as a c.

It’s many, many times more wear-resistant than countertop laminates and can often be laid immediately over an present flooring.

● Biello, David. “Why not spend $21 billion on solar energy from space?” Scientific American.

In general, an audit is a review of your finances and leads to recommendations for motion to enhance your monetary model.

All of money that goes back and forth from a enterprise should be followed and represented.

Write down all your different month-to-month expenses (mortgage payments, food, entertainment bills, and so on.) and weigh these against your monthly auto payments.

You should definitely stop and enjoy this gorgeous lake.

There may be an outdated saying that “the market climbs a wall of worry.” So this all sounds like there are a whole lot of causes to fret!

Those of us home cooks who take on cake making from time to time will generally use a toothpick to test whether a cake is done or not.

Colours for the rapid video games were drawn at the press convention after recreation 14: Ding acquired the white items for the primary recreation.

It was broadcast on 17 November 2011 on BBC One, BBC One HD and simulcast on BBC Radio 1 and was hosted by Fearne Cotton, Chris Moyles and David Tennant.

I was pretty pleased to find this great site. I want to to thank you for your time due to this fantastic read!! I definitely appreciated every part of it and i also have you saved as a favorite to see new information on your website.

Being accountable for one鈥檚 actions and phrases.

The notion that glass flows to an appreciable extent over prolonged durations well under the glass transition temperature isn’t supported by empirical analysis or theoretical analysis (see viscosity in solids).

Why can you hear the ocean while you hold a seashell to your ear?

From 2000 to 2013, Chinese trade with Latin America rocketed from $12 billion to over $275 billion.

Understanding (and heeding) your truck’s towing capacity — particularly its GVWR and GVW, that are typically referred to as gross trailer weight score (GTWR) and gross trailer weight (GTW) — is considered one of an important issues you have to do earlier than heading to the nice outdoors.

you use a excellent blog here! would you like to earn some invite posts in my small weblog?

Having read this I thought it was rather enlightening. I appreciate you taking the time and effort to put this article together. I once again find myself personally spending a lot of time both reading and leaving comments. But so what, it was still worth it!

These kind of post are always inspiring and I prefer to read quality content so I happy to find many good point here in the post,writing is simply great,thank you for the post.

You made some good points there. I looked on the net for additional information about the issue and found most people will go along with your views on this web site.

I’m amazed, I must say. Seldom do I encounter a blog that’s both equally educative and entertaining, and without a doubt, you’ve hit the nail on the head. The issue is an issue that too few people are speaking intelligently about. I’m very happy that I came across this in my search for something relating to this.

Your style is unique compared to other folks I’ve read stuff from. Many thanks for posting when you have the opportunity, Guess I will just book mark this web site.

There’s certainly a lot to learn about this subject. I like all of the points you made.

I needed to thank you for this good read!! I absolutely loved every bit of it. I have you book-marked to check out new stuff you post…

I could not resist commenting. Perfectly written.

May I simply just say what a relief to discover a person that actually understands what they are talking about over the internet. You certainly know how to bring an issue to light and make it important. More people have to check this out and understand this side of the story. I can’t believe you are not more popular since you certainly have the gift.

Great web site you’ve got here.. It’s difficult to find good quality writing like yours nowadays. I seriously appreciate individuals like you! Take care!!

I got what you mean , saved to my bookmarks , very decent internet site .

Hello, I think your blog could be having browser compatibility issues. When I look at your website in Safari, it looks fine however, if opening in I.E., it has some overlapping issues. I simply wanted to give you a quick heads up! Besides that, great site.

Hiya, I am really glad I’ve found this information. Today bloggers publish just about gossip and internet stuff and this is really irritating. A good web site with exciting content, that is what I need. Thanks for making this website, and I will be visiting again. Do you do newsletters? I Can’t find it.

This is a topic that’s near to my heart… Many thanks! Exactly where can I find the contact details for questions?

I simply wished to thank you so much once more. I am not sure what I would’ve gone through without the entire methods contributed by you about such subject matter. It had been a very intimidating circumstance for me personally, nevertheless coming across a new well-written manner you resolved the issue forced me to leap for contentment. Now i’m happy for your support and trust you realize what a powerful job you were carrying out educating most people thru a web site. Most probably you haven’t encountered all of us.

Managing anxiety every day could be achieved through coping mechanisms, life-style modifications, and self-care practices.

You are so awesome! I do not think I’ve read through a single thing like that before. So nice to discover somebody with a few unique thoughts on this subject. Seriously.. many thanks for starting this up. This website is something that is needed on the internet, someone with a bit of originality.

Everything is very open with a clear clarification of the issues. It was definitely informative. Your site is extremely helpful. Thank you for sharing.

I admire your work , thankyou for all the interesting posts .

Good info. Lucky me I reach on your web site by accident, I bookmarked it.

Shah, Angilee. “A Novice Health Care Reform Blogger Explains Why She Writes”.

Good article. I’m dealing with some of these issues as well..

Great post. I will be experiencing some of these issues as well..

There couple of interesting points at some point here but I don’t determine if every one of them center to heart. There exists some validity but I will take hold opinion until I consider it further. Good post , thanks and then we want more! Added onto FeedBurner in addition

Everyone loves your site.. great colorations & theme. Would anyone style and design this website yourself as well as does you actually hire an attorney to make it happen for you personally? Plz reply as I!|m seeking to style my own, personal weblog and would wish to know where ough obtained that out of. many thanks

You’re so interesting! I do not suppose I have read something like that before. So great to discover someone with some genuine thoughts on this topic. Really.. thanks for starting this up. This web site is one thing that is required on the web, someone with a little originality.

Do you have a spam issue on this site; I also am a blogger, and I was curious about your situation; we have created some nice methods and we are looking to trade strategies with others, please shoot me an e-mail if interested.

eating disorders are of course sometimes deadly because it can cause the degeneration of one’s health.,

This is a topic that’s close to my heart… Take care! Where can I find the contact details for questions?

This page certainly has all the info I wanted concerning this subject and didn’t know who to ask.

Excellent read, I just passed this onto a colleague who was doing a little research on that. And he actually bought me lunch because I found it for him smile So let me rephrase that.

Can I just now say such a relief to find one who truly knows what theyre dealing with on the internet. You definitely know how to bring a challenge to light and produce it crucial. Workout . need to look at this and see why side of your story. I cant think youre less well-liked simply because you absolutely contain the gift.

Nice post. I discover something harder on different blogs everyday. It will always be stimulating to learn to read content from other writers and rehearse a little at their store. I’d would rather apply certain with all the content in my small blog regardless of whether you don’t mind. Natually I’ll supply you with a link on the web blog. Many thanks sharing.

After looking at a number of the blog posts on your blog, I honestly like your way of writing a blog. I saved it to my bookmark site list and will be checking back soon. Take a look at my web site as well and let me know what you think.

i would love to enter my baby on a baby contest because she is very nice and talented;;

Premature Ejaculation is the lack of ejaculatory control and it is the most common of all sexual problems in men. Since it is natural, you can use it freely without any risk of adverse effects.

I real pleased to find this web site on bing, just what I was searching for : D as well saved to bookmarks .

The next occasion Someone said a weblog, I’m hoping who’s doesnt disappoint me approximately brussels. After all, It was my option to read, but I really thought youd have some thing intriguing to talk about. All I hear is a couple of whining about something that you could fix should you werent too busy looking for attention.

Having read this I thought it was very enlightening. I appreciate you finding the time and energy to put this content together. I once again find myself personally spending a significant amount of time both reading and commenting. But so what, it was still worthwhile!

Hi, There’s no doubt that your site could possibly be having internet browser compatibility issues. When I look at your web site in Safari, it looks fine however when opening in I.E., it has some overlapping issues. I merely wanted to provide you with a quick heads up! Aside from that, excellent blog!

I became just browsing here and there but got to see this post. I have to admit that I am within the hand of luck today in any other case getting this excellent post to learn wouldn’t happen to be achievable for me, a minimum of. Really appreciate your articles.

my file cabinets are made of recycled fiber, they are great for holding large file folders~

You see, this attitude bugs me so much, and I haven’t even criticized some of the weird stuff they present us in this movie.

fashion jewelries will be one of the best stuffs that you can use to enhance your personal style’

I actually still cannot quite feel that I could become one of those reading the important guidelines found on your web blog. My family and I are truly thankful for your generosity and for providing me potential to pursue our chosen career path. Many thanks for the important information I obtained from your web site.

I truly wanted to develop a quick note to thank you for these stunning advice you are placing at this site. My extensive internet look up has at the end of the day been paid with extremely good strategies to go over with my classmates and friends. I ‘d mention that many of us website visitors are unquestionably lucky to dwell in a superb place with very many special professionals with very beneficial hints. I feel extremely fortunate to have come across the website page and look forward to tons of more excellent times reading here. Thanks again for everything.

I truly love your blog.. Very nice colors & theme. Did you build this amazing site yourself? Please reply back as I’m trying to create my very own blog and would love to learn where you got this from or just what the theme is called. Thanks!

You should be a part of a contest for one of the most useful blogs on the web. I am going to recommend this web site!

You made some decent points there. I looked on the internet for additional information about the issue and found most people will go along with your views on this site.

I used to be able to find good information from your blog posts.

Hello! I merely wish to make a enormous thumbs up for the fantastic information you might have here with this post. I am returning to your website to get more detailed soon.

I think your blog is getting more and more visitors.

Comfortabl y, the post is really the freshest on this laudable topic. I suit in with your conclusions and can thirstily look forward to your next updates. Simply saying thanks can not simply be enough, for the fantasti c clarity in your writing. I definitely will correct away grab your rss feed to stay abreast of any kind of updates. Great work and also much success in your business dealings!

Its amazing what supplementing can do for your body and your weight lifting goals!

I would like to thnkx for the efforts you have put in writing this blog. I’m hoping the same high-grade website post from you in the upcoming also. Actually your creative writing skills has inspired me to get my own site now. Actually the blogging is spreading its wings rapidly. Your write up is a good example of it.

Browsed the whole written piece. You have some really helpful details here. thank you. “Politics is war without bloodshed while war is politics with bloodshed.” by Mao Tse Tung..

Respect to post author, some fantastic information .

??? ????? ????? ????? ???? ?? ????? ?? ????? ??? ?? ?????? ??????? . ????? ??????? ????? ???? ?????? ??????? ?????? ??????? ???? ????? ?????? ??????? ??? ??????? ??? ?? ??????? ?? ????? ????????.

my mom would always frequently visit flower shops because she loves fresh flowers on our house-

These could embody household therapy, which aims to enhance communication and support inside the household unit, and group therapy, the place people can share their experiences and study from others going through comparable challenges.

Having read this I believed it was rather enlightening. I appreciate you spending some time and effort to put this content together. I once again find myself personally spending way too much time both reading and posting comments. But so what, it was still worth it!

It’s hard to come by experienced people about this subject, however, you sound like you know what you’re talking about! Thanks

Way cool! Some extremely valid points! I appreciate you penning this post and also the rest of the website is really good.

Substantially, the post is really the freshest on that noteworthy topic. I concur with your conclusions and also can eagerly look forward to your coming updates. Simply just saying thanks definitely will not simply be acceptable, for the amazing lucidity in your writing. I can promptly grab your rss feed to stay informed of any updates. Fabulous work and also much success in your business endeavors!

I think your site has one of the cleanest theme I’ve came across. It really helps make reading your blog a lot easier.

Howdy! This post could not be written much better! Looking through this post reminds me of my previous roommate! He always kept talking about this. I’ll send this post to him. Fairly certain he will have a good read. Many thanks for sharing!

Excellent stuff. I can’t describe how much your site has helped me within my academic research on the subject. I’m now likely to get top marks without a doubt. Thanks a thousand. I owe you one.

I was able to find good advice from your blog posts.

wedding venue beside the beach is i think the best and looks very romantic;;

Yeah bookmaking this wasn’t a speculative conclusion outstanding post! .

You should get involved in a contest for example of the most useful blogs on-line. Let me recommend this page!

Excellent post! We are linking to this great content on our website. Keep up the great writing.

Can I simply just say what a relief to find someone that actually knows what they’re discussing online. You definitely realize how to bring a problem to light and make it important. More and more people really need to look at this and understand this side of the story. I was surprised you aren’t more popular given that you surely have the gift.

RCA system (VHD is incompatible with the RCA VideoDisc system).

Incredible the following guideline is wonderful it really helped me along with my family, appreciate it!

Pretty nice post. I simply stumbled upon your blog and wanted to say that I have truly enjoyed browsing your weblog posts. In any case I’ll be subscribing to your rss feed and I hope you write once more very soon!

This web page is actually a walk-through it really is the information you wished in regards to this and didn’t know who ought to. Glimpse here, and you’ll definitely discover it.

I might wish to have more muscle mass.

Due to this fact, you would search for not solely the accessible services but in addition the inexpensive services that can provide you the most effective relaxation a minimum of time.

But there are several glitches, the first being that officers don’t necessarily turn them on.

Personally I’m impressed by the quality of this. Usually when I find stuff like this I stumble it. Although this time I’m not sure if this would be best for the users. I’ll look around and find another article that may work.

sometimes i have a hard time choosing laptop accessories, there are just so many options to choose from,,

the idea beach towel should be colored white because it reflects heat away-

If this tour were organized only by collector “value” quite than with geography taken under consideration, Hakurai Toys can be up there proper after Star Case.

I couldn’t refrain from commenting. Well written.

You’re so cool! I do not suppose I’ve read through a single thing like that before. So wonderful to find somebody with unique thoughts on this subject matter. Seriously.. thank you for starting this up. This site is one thing that’s needed on the internet, someone with a little originality.

I really like looking through a post that will make men and women think. Also, many thanks for allowing for me to comment.

This is a topic which is close to my heart… Take care! Exactly where are your contact details though?

An intriguing discussion is definitely worth comment. I do think that you need to write more about this subject, it might not be a taboo matter but typically folks don’t talk about such issues. To the next! Best wishes!

Pardon me if this is off-topic, but more people need to really focus on what just happened in Oslo. Just remember it could happen in our country too.

I’m impressed, I have to admit. Really rarely can i encounter a blog that’s both educative and entertaining, and without a doubt, you’ve hit the nail to the head. Your idea is outstanding; the problem is something which inadequate persons are speaking intelligently about. My business is very happy i found this in my look for some thing in regards to this.

Hello there! This blog post could not be written much better! Looking at this article reminds me of my previous roommate! He continually kept preaching about this. I’ll forward this information to him. Fairly certain he’ll have a very good read. I appreciate you for sharing!

Way cool! Some very valid points! I appreciate you writing this post and the rest of the website is very good.

I like it when folks come together and share ideas. Great blog, keep it up!

There are monarchs who roll up their sleeves and monarchs who would relatively observe from a distance.

You are so awesome! I do not suppose I’ve read through a single thing like this before. So nice to find someone with unique thoughts on this subject matter. Really.. thanks for starting this up. This web site is something that is needed on the internet, someone with a bit of originality.

When I originally commented I seem to have clicked the -Notify me when new comments are added- checkbox and from now on each time a comment is added I recieve 4 emails with the exact same comment. Is there a means you are able to remove me from that service? Appreciate it.

Platinum was an necessary strategic protection metallic used during World Struggle II and was not allowed for jewellery utility at that time,” Luker says. Even in the present day, platinum is so important to economic and protection efforts that it was listed as one of many 35 minerals “deemed important to U.S.

Pretty! This has been an incredibly wonderful post. Thank you for supplying this information.

My friend and i also have been simply discussing above this unique problem, linda is consistently planning to demonstrate myself incorrect! I am going to show her this type of article and also apply it in a little!

pretty helpful material, overall I think this is well worth a bookmark, thanks

Yikes this definitely takes me back, i’ve been wondering about this subject for a while.

Greetings! Very useful advice within this post! It’s the little changes that make the largest changes. Thanks a lot for sharing!

The vulnerability of male farmers doesn’t usually make entrance web page news, but it’s one thing that Australians should remember of.

Male farmers expertise high ranges of job-related stress, excessive rates of suicide and they have low charges of searching for skilled help.

The the next occasion Someone said a blog, Lets hope it doesnt disappoint me just as much as this place. I mean, It was my option to read, but I just thought youd have some thing fascinating to mention. All I hear can be a number of whining about something that you could fix in case you werent too busy interested in attention.

I like this web blog so much, saved to my bookmarks .

digital kitchen scales are the stuff that i always use on my kitchen when i weight things**

While the advertising and tv industries are still trying to determine precisely methods to pay for themselves in the absence of that long-ago captive audience, Internet and cable companies have been steadily growing the range of how wherein our television exhibits can reach us each time we feel like watching them.

The previous few results have brought them to a crisis point and Pep has even begun to be involved about his job safety.

I like this site very much, Its a rattling nice place to read and find information.

After study a few of the content for your website now, i genuinely as if your technique of blogging. I bookmarked it to my bookmark website list and are checking back soon. Pls have a look at my website too and told me if you agree.

This internet site is my intake , real good layout and perfect subject material .

Hey i Love your work i really appreciate that. Also take a look at our special Gym flooring dubai

This is a topic that is close to my heart… Best wishes! Exactly where can I find the contact details for questions?

As far as me being a member here, I didnt even know that I was a member here. When the article was published I received a notification, so that I could participate in Comments, so perhaps that is it. But we’re certainly all members in the world of ideas.

As usual you did an great job evaluating the problem and finding a good answer. I will stay tuned for more releases on your blog.

I simply desired to make a quick comment in order to express gratitude for your requirements for people wonderful pointers you are posting at this site. Time consuming internet investigation has towards the end for the day been rewarded with high-quality strategies to present to my guests. I would claim that many of us readers are really endowed to happen in an incredible network with biggest reason so many marvellous those with useful hints. Personally i think quite privileged to have used your webpages and check toward really more fabulous minutes reading here. Thank you for many things.

Short-term Appearing Commissioned Engineer William Clifford James Williams, (on mortgage to the federal government of India).

Very nice article. I absolutely appreciate this website. Keep writing!

I was more than happy to uncover this website. I need to to thank you for ones time for this fantastic read!! I definitely liked every bit of it and I have you saved as a favorite to look at new things in your website.

I am impressed with this site, real I am a big fan.

An impressive share, I just given this onto a colleague who was doing a little bit evaluation on this. And he the truth is purchased me breakfast because I discovered it for him.. smile. So let me reword that: Thnx for the treat! But yeah Thnkx for spending the time to debate this, I really feel strongly about it and love reading more on this topic. If doable, as you become experience, would you mind updating your blog with extra particulars? It is extremely useful for me. Large thumb up for this blog submit!