If you haven’t already, check out Episode 4 of the Prometheus Podcast! For this episode, we have the pleasure of once again hosting Darius Dale, Founder & CEO of 42 Macro. For those of you who missed our previous conversation, we highly recommend you give it a listen for a better understanding of his sophisticated framework (Click here). While in our last conversation, we focused more on mechanics, today we’re going to spend our time discussing the current state of the economy & the outlook for markets. Aahan & Darius traverse the US macro landscape, discussing everything from the Fed & inflation to the reverse repo facility and portfolio strategy. This episode is a must-listen for anyone seeking to manage macro risk during one of the most economically volatile periods in history.

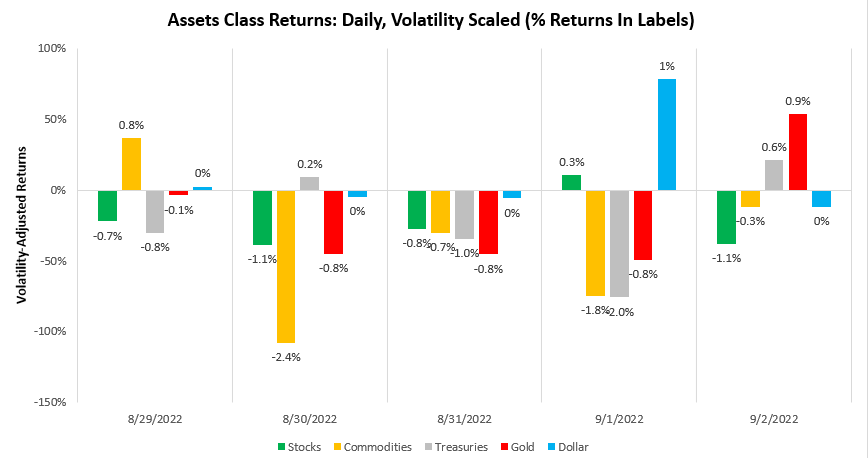

Last week, markets moved to price-tightening liquidity conditions, with major asset classes all suffering losses relative to the dollar. Investment assets suffered through the week; however, the dollar’s gains were non-linear and were concentrated on Thursday as better-than-expected economic data caused markets to price in tighter monetary policy. We show the path of market returns below:

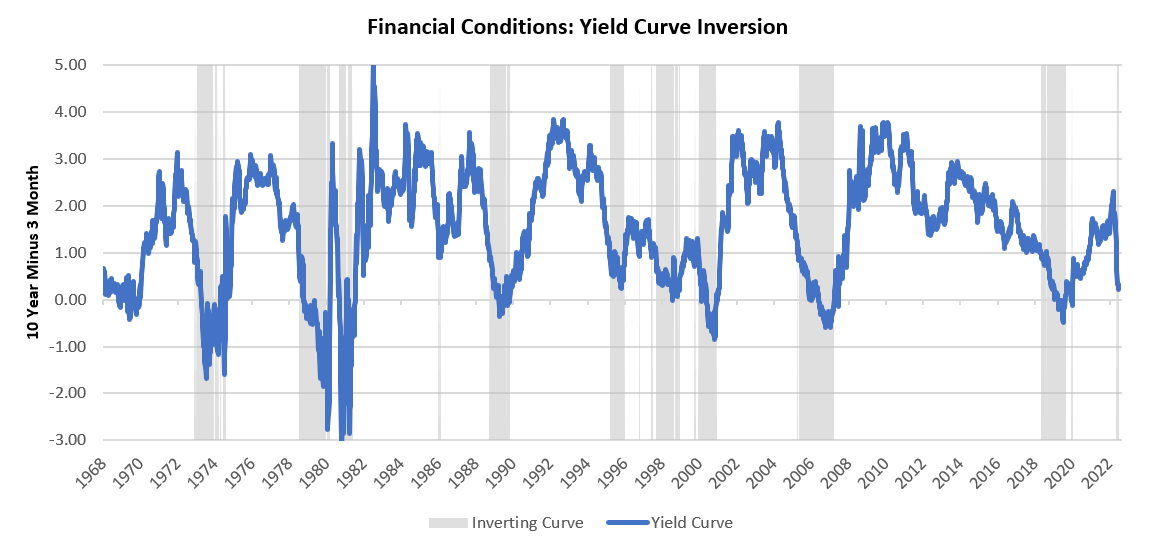

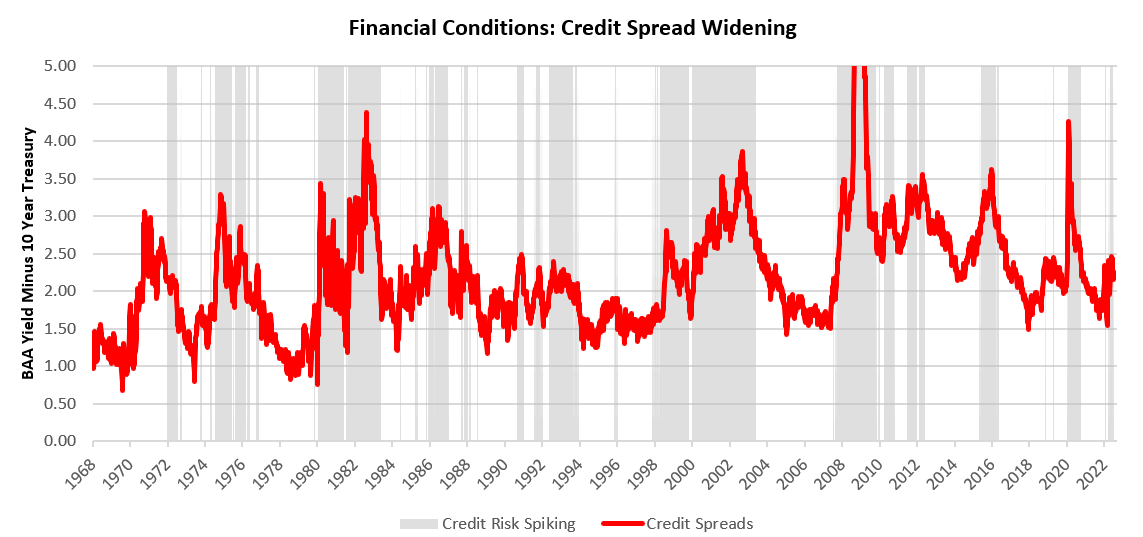

Alongside these moves, the yield curve continues to move towards inversion, and credit spreads continue to spike creating a mix of tight financial conditions for markets, making it difficult for assets to perform. We show these below:

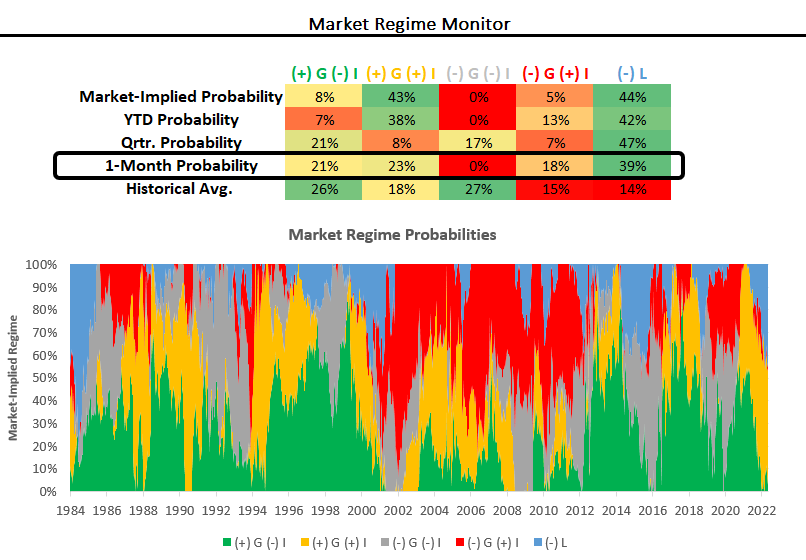

Aggregating these conditions, our market regime monitors told us last week was one where markets incrementally priced tightening liquidity conditions. Our systems attempt to capture the durable path in market regimes and continue to signal that we are in a stagflationary nominal growth environment. We show this below:

Conditions continue to align for us to remain in this high nominal growth environment far longer than most traditional asset allocations can handle. While we continue to witness a drag on real growth, the nominal spending component remains extremely strong.

The eventual resolution of this dynamic will likely come from a substantial deterioration in the labor market, but we remain off from this outcome. Until these dynamics change markedly, we likely remain in a dynamic of stagflationary nominal growth, with a high potential for a transition to outright stagflation. This risk is imperative to understand, as the allocations that have worked over the last 40 years are unlikely to work well in this environment, as evidenced by price action year-to-date.

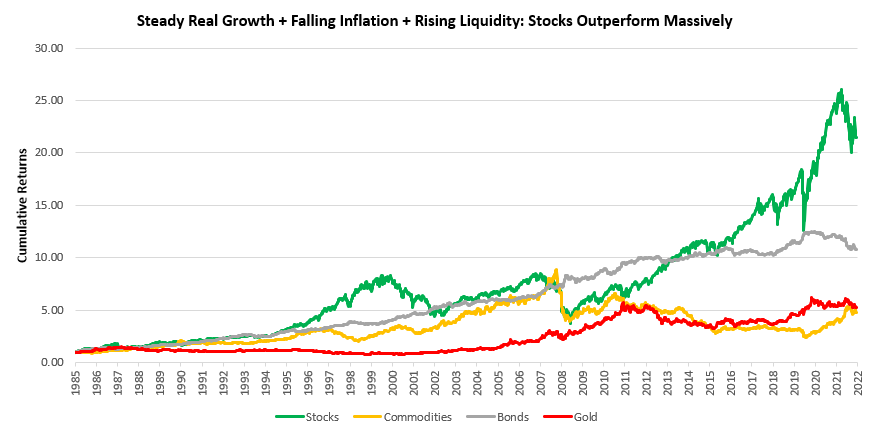

We think this environment is particularly challenging because of the dramatically different opportunity set it presents relative to what market participants have seen over recent decades. Below, we show a cumulative return series that most investors are used to seeing:

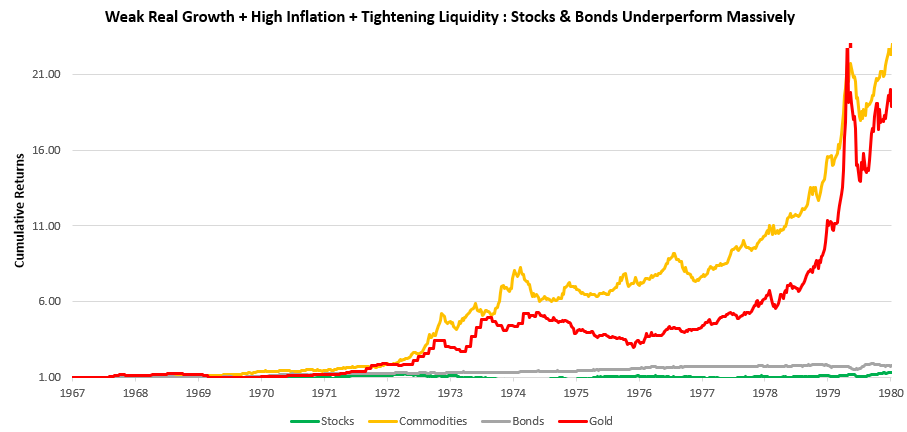

However, this outperformance is not a feature of equities (or bonds) as an asset class but rather of sample selection. Below, we show the cumulative returns for the same set of assets from 1967 to 1980:

The purpose of the above illustrations is not to make a secular forecast for inflation or stagflation but to understand the risk that traditional asset allocations face in an inflationary environment. Resultantly, we continue to think investment strategies that are both nimble and have a strong mechanical understanding of the environment are likely to outperform those that continue to attempt to revert to more conventional dynamics. Our research was designed with these environments in mind, and we continue to expect them to navigate this path successfully and continue to monitor where they could fall short.

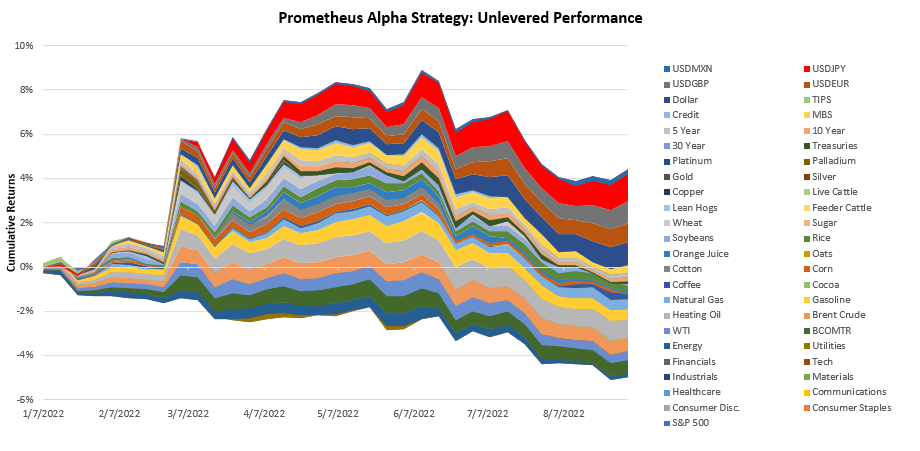

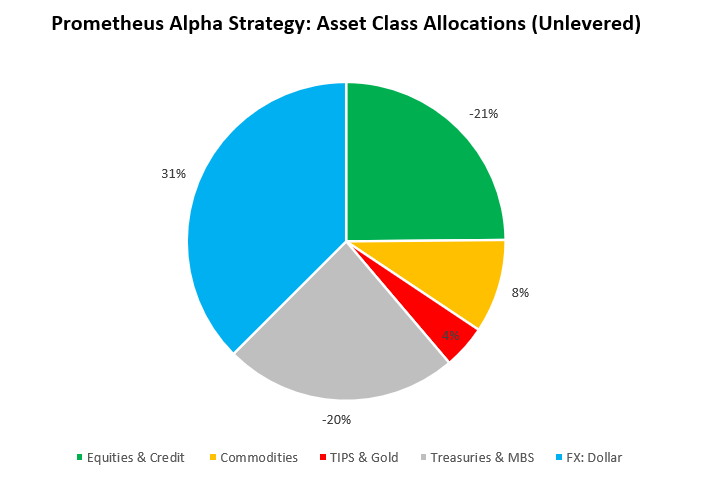

In this context, last week proved a successful one for our systematic Alpha Strategy, which continued to short Treasuries & Equities while maintaining long positions in the Dollar. Our Alpha Strategy targets a 10% volatility dynamically using leverage, but we show the year-to-date unlevered performance attribution below:

Our positioning heading into next week remains fairly unchanged, and our systems maintain the same core exposures at the asset class level:

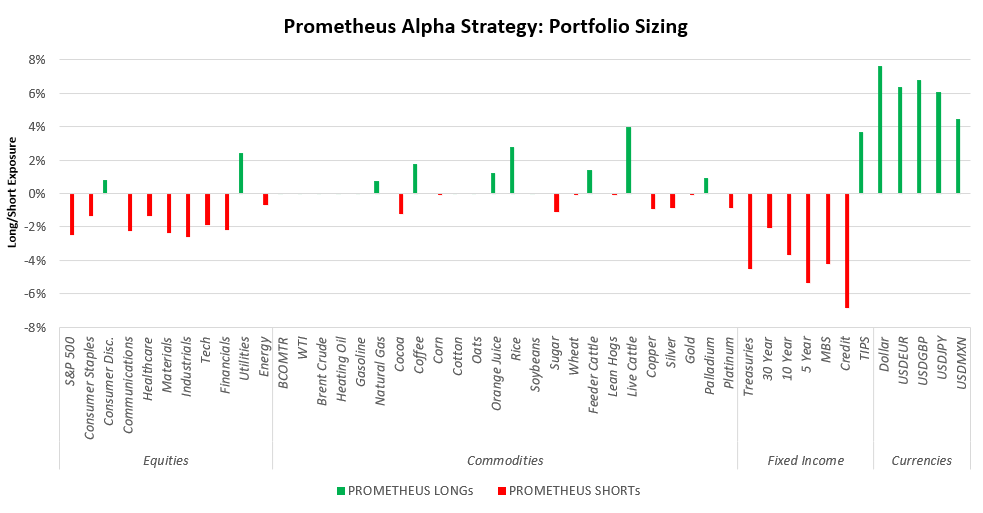

We zoom in to show these positions at the security level:

Before we dive into our outlook, we show the upcoming events on the data calendar relevant to our systematic tracking of economic conditions:

-

Monday:

-

Tuesday: S&P Services & Composite PMI, ISM Services & Composite PMI

-

Wednesday: Trade Balance, MBA Mortgage Apps

-

Thursday: Jobless Claims, Consumer Credit

-

Friday: Wholesale Inventories & Trade, Household Net Worth

Our systems continue to tell us that the environment remains unconducive to significant cyclical improvement in PMI data. Furthermore, we will continue to monitor inventory data carefully, as we think this will be a critical indicator in determining the future outlook for corporate profitability. We address our outlook below:

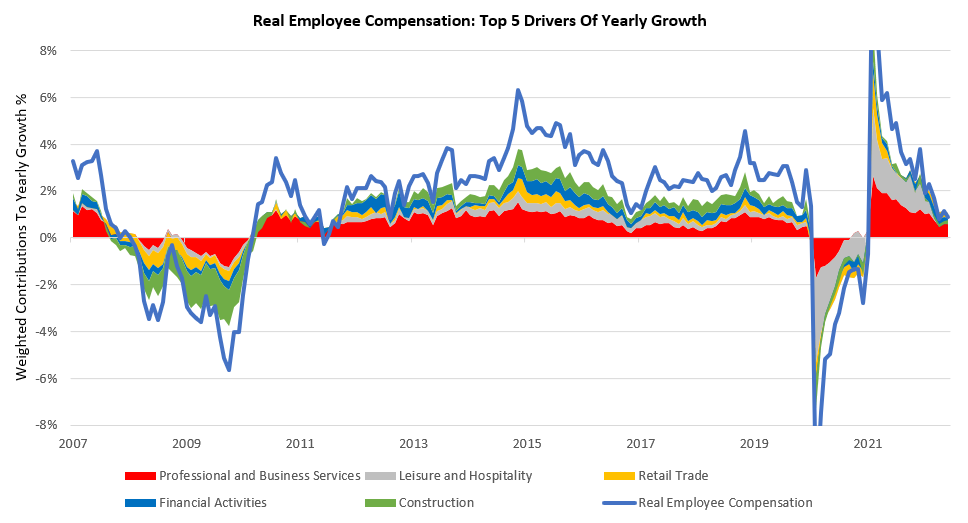

i. Pressures on real income and activity are abundant. In the recent past, we have highlighted how stagflationary dynamics create negative feedback loops, which pressure real economic growth variables lower. These pressures are born through the investment channel wherein nominal dollars create less output per unit invested, creating lower real output and incomes. Below, we show our tracking of real growth tells us that aggregate employee incomes are now flirting with contraction on a real basis:

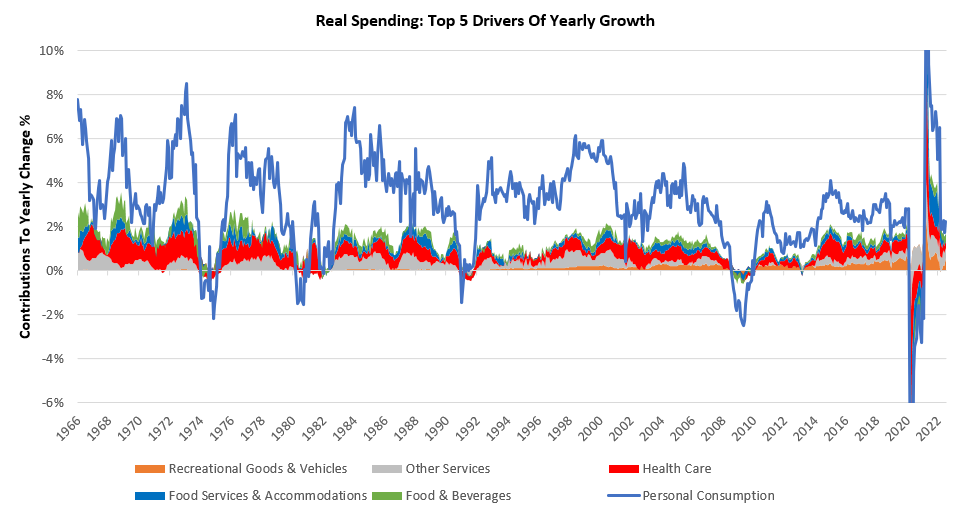

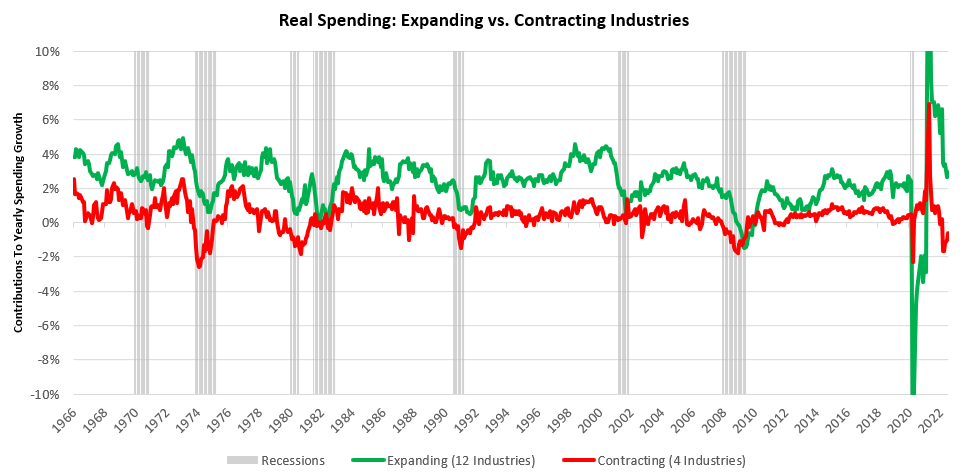

This income translates into real spending, and we are seeing pressure on this channel as well:

Furthermore, four of sixteen industries are already in contraction on a real basis. These industries are highly cyclical areas, i.e., Motor Vehicles & Parts, Furnishings & Durable Household Equip., Food & Beverages, & Gasoline & Energy Goods. We show this decomposition below:

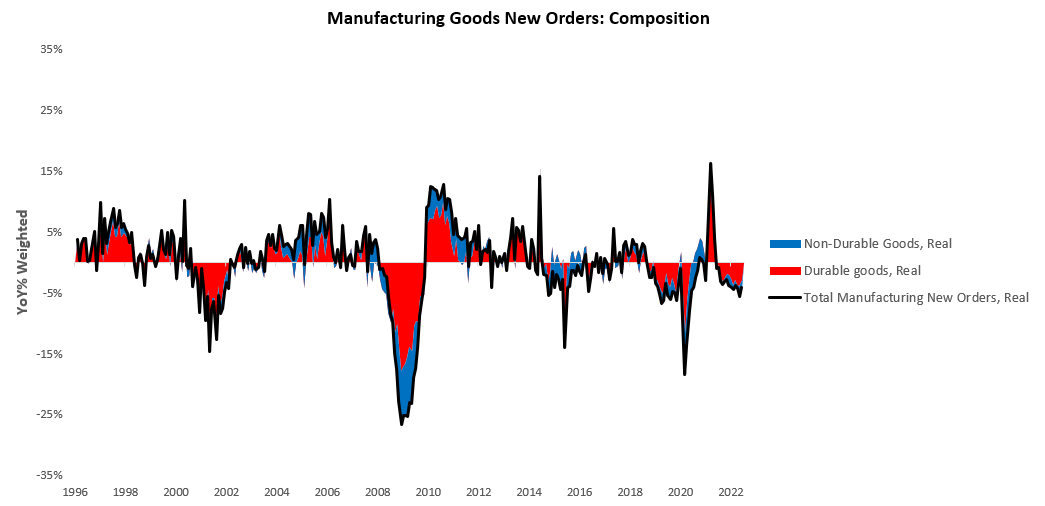

Furthermore, real new orders for manufacturing goods are now in negative territory:

Therefore, the pressures remain in place for real output & production to move lower, i.e., further weakening in real growth.

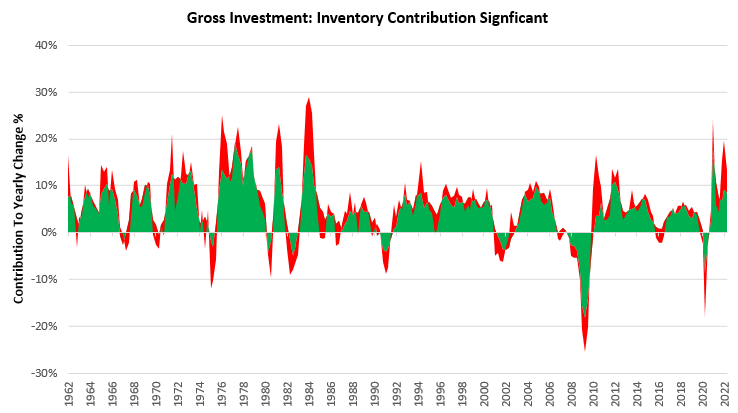

ii. We are watching inventories carefully to signal the next steps for profitability. Profitability is driven by gross investment activity relative to nonbusiness savings. Inventory build can help pad profitability in the short term because one business’s inventory growth is another business’s sales growth. However, inventory build has limitations and can only go so far as it does not increase production capacity, and there is a finite ability to add inventories due to physical limitations. However, inventory build is less penalized during inflationary periods, which can result in periods of elevated inventory rises. We judge today to be one of these periods, with inventory build contributing significantly to nominal gross investment:

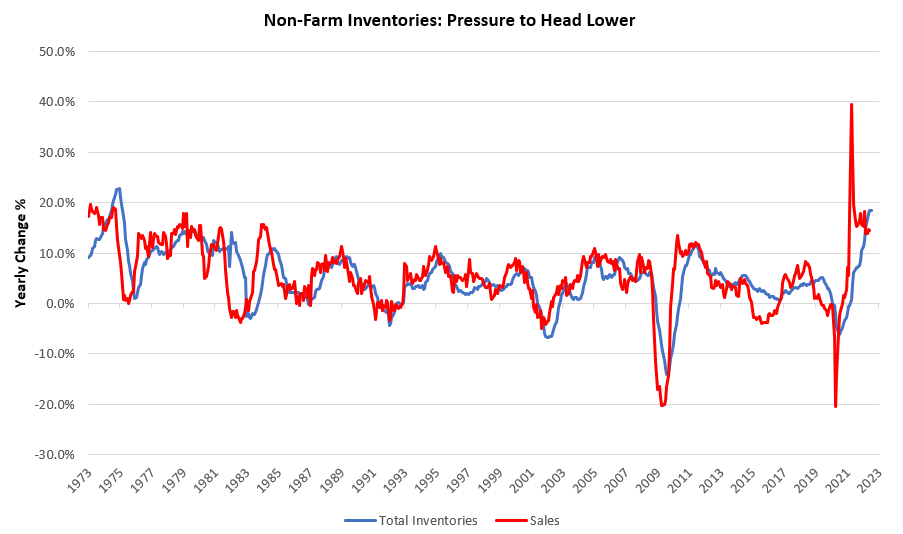

However, with nominal sales decelerating on a year-over-year basis, the pressure is increasing for inventories to fall:

Our tracking of economic conditions now highlights that variables often defined as lagging indicators are now the marginal drivers of change for the economic cycle. The marginal change in variables like employment, production, & inventories will determine the next steps in the economic cycle.

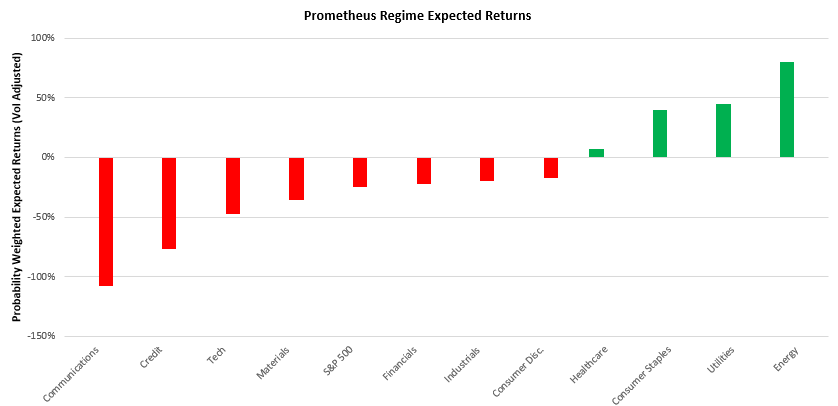

iii. Equities continue to show weak expected returns in this environment. Equities are ill-equipped to deal with stagflationary nominal growth, and we are seeing this in our expected return measures:

Resultantly, we continue to short equities and credit.

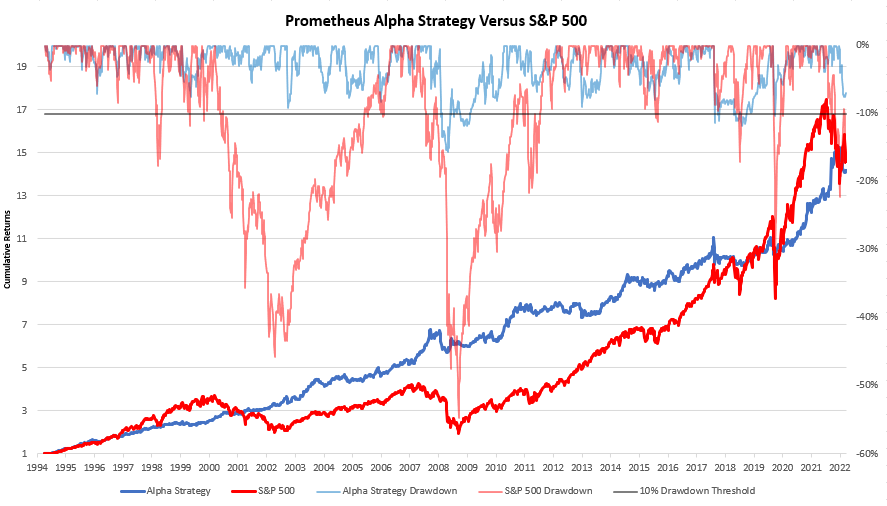

Netting all these factors, we continue to remain positioned for stagflationary nominal growth and tightening liquidity conditions. Our approach continues to perform well in a dramatically different environment relative to history, and we expect it to continue to do so. Below, we show the cumulative performance for our Alpha Strategy, which targets volatility of 10% through the dynamic use of leverage and is currently modestly levered at 1.39X:

Stay nimble.

Their global reputation precedes them.

can i buy lisinopril

The staff always goes the extra mile for their customers.

Their international health campaigns are revolutionary.

order generic cipro

Generic Name.

They provide peace of mind with their secure international deliveries.

does gabapentin potentiate klonopin

They make prescription refills a breeze.

I love the convenient location of this pharmacy.

can i order clomid without a prescription

Everything about medicine.