Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of both the economy and financial markets in real-time. Here are the top developments that stand out to us:

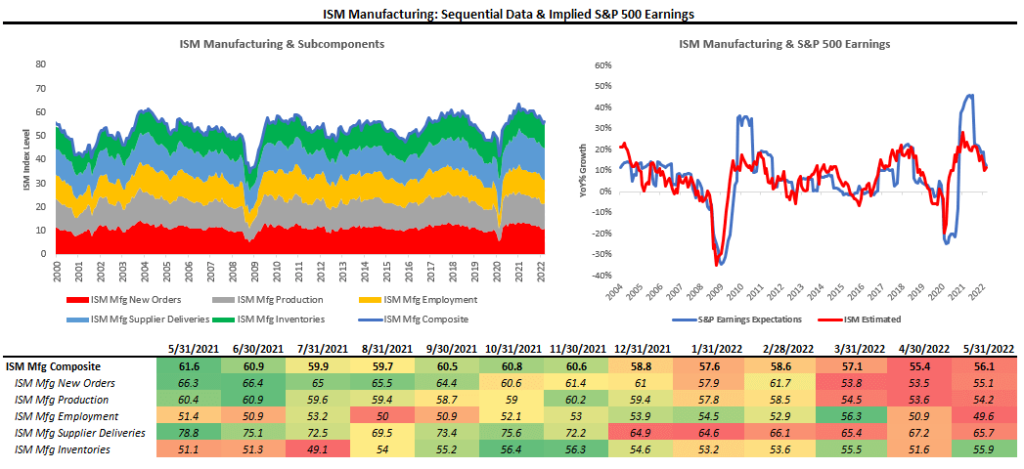

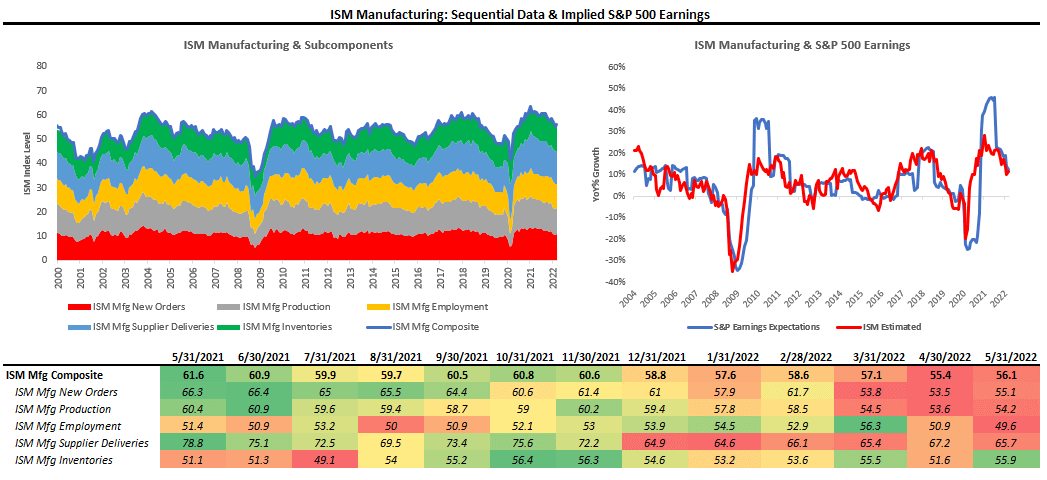

i. ISM Manufacturing PMI data bucked the slowdown trend. The latest ISM Manufacturing data showed an expansionary reading of 56.1, implying 12% YoY earnings for the S&P 500. This reading was a sequential acceleration within a decelerating trend. The largest gaining segment was Inventories, and the most significant slowdown was in Deliveries. This data was contrary to our expectations, but our systems nonetheless tell us the trend remains a weaker one:

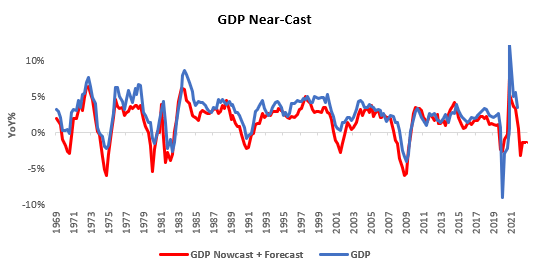

ii. The latest economic data tells us that US GDP is currently running between 0.9% to 1.2% on a year-over-year basis, down from 3.35% in December. The labor market remains tight, with wages still elevated in nominal terms, but negative in real terms. The strength of the labor market, combined with savings drawdowns and credit uptake keeps growth afloat, but it looks like a matter of time that profit pressures will dampen the employment and income outlook. We show our forward looking estimates of GDP below:

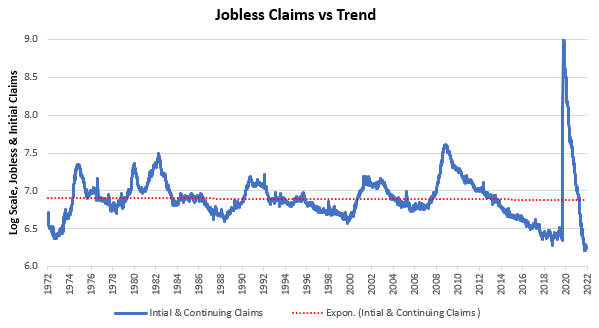

We show the low levels of unemployment supporting growth in the form of Initial & Continuing Claims relative to their long-term trend:

Unemployment is broadly below trend. We offer the state-wise composition of this trend below. California showed the greatest increase in unemployment claims, while Kentucky showed the greatest decrease.:

iii. Quantitative Tightening (QT) will continue to pressure equity valuations. Equity valuations largely depend upon the stock of liquidity that can finance and support their expansion. Valuations are more likely to compress when the monetary and fiscal authorities move to tighten liquidity conditions. With QT now beginning and no fiscal impulse forthcoming, valuations are likely to have room to widen further.

Overall, while we have received some incremental data disconfirming the slowdown in the economy, our systems continue to paint a picture of stagflationary nominal growth. This dynamic is confirmed by trend breadth in markets. Below we show our Multi-Duration Monetum Monitors, which measure time-series momentum ranging from one week up to one year, i.e., they measure the pervasiveness of the current market trend.

As we can see above, assets that prefer rising inflation, i.e., commodities and gold, have much stronger momentum supporting their prices than assets that prefer disinflation, i.e., equities and treasuries. These price trends follow economic trends, with inflation acceleration remaining the most significant economic and market risk to manage this year. Our systems that aggregate all our analyses algorithmically continue to prefer inflation beneficiaries in the current context. Our systems have navigated well this year, though the reversal we saw last week ate into performance. We show the un-levered ETF Strategy performance year-to-date:

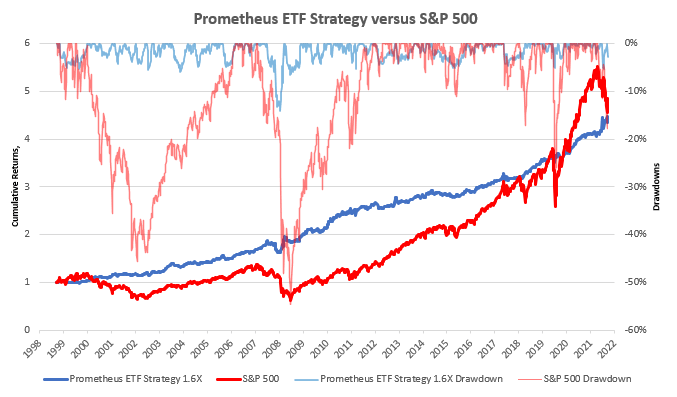

Not every week will be a positive one; however, we remain confident our systems can achieve substantial risk-adjusted returns, irrespective of the economic environment. We show the backtested history of our signals below., with our ETF Strategy levered to match cumulative equity returns for illustrative purposes:

This is a time for defense, not offense, with active management of shorts welcome. Stay tuned for tomorrow’s ETF Strategy updates. Stay nimble!