Modest Nominal Spending & Mixed Production

Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

Today, we received incremental new information on both consumer spending and output in the form of retail sales and industrial production, respectively. After dissection, these data point to a weakening in real consumer demand and a transportation-driven improvement in manufacturing production. Overall, weaker incomes, moderating spending, but increased (automobile) production for April.

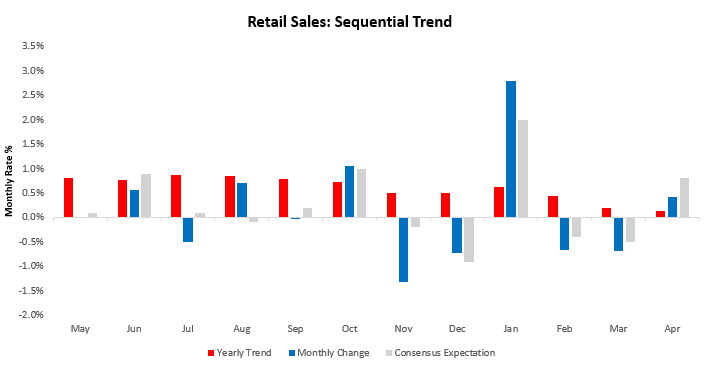

We start by looking through retail sales and inventories. Retail Sales increased by 0.42% in April, disappointing consensus expectations of 0.8%. This print contributed to a sequential deceleration in the quarterly trend relative to the yearly trend. Below, we show the monthly evolution of the data relative to its 12-monthly trend and consensus expectations:

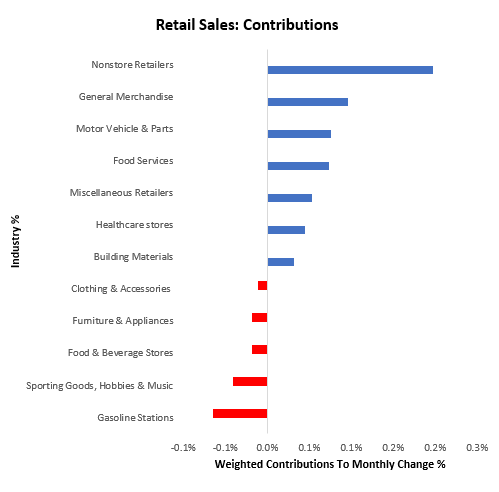

Below, we show the composition of these sales over the most recent month:

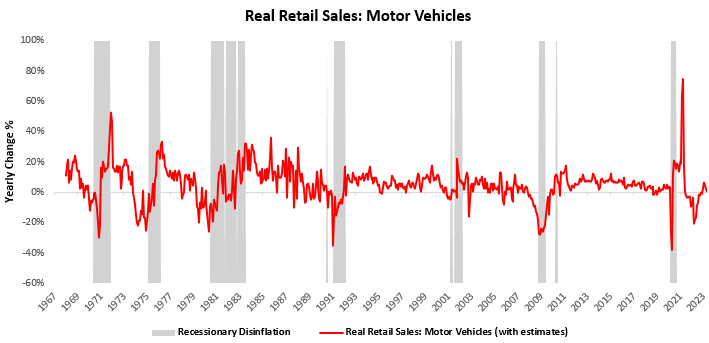

Above, we highlight that nominal motor vehicle sales continued to improve. However, our estimates of real sales showed a contraction of 1.1% in real motor vehicle sales:

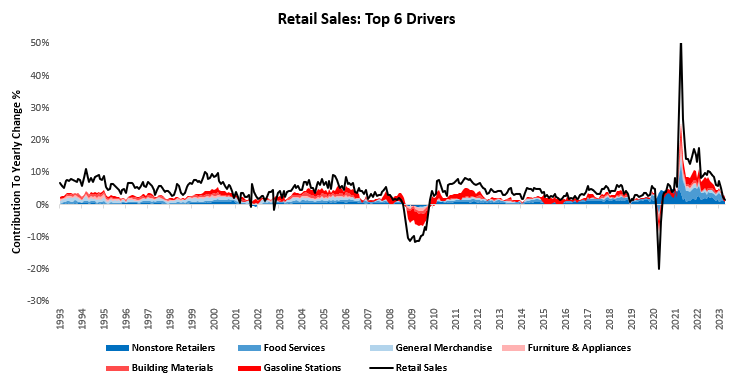

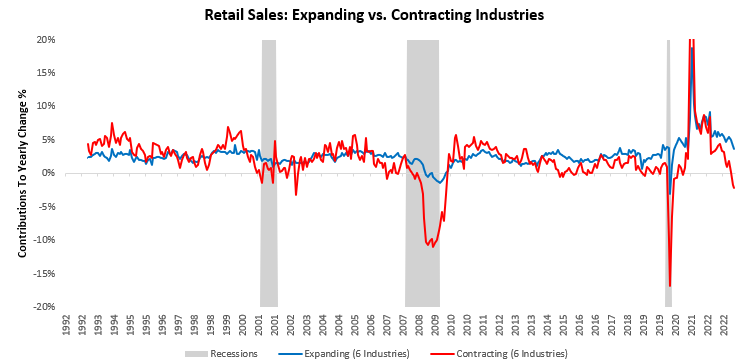

Zooming out, nominal retail sales have expanded by 1.6% over the last year. Below, we zoom out to show the 6 major drivers of strength in shades of blue (Nonstore Retailers, Food Services & General Merchandise) and weakness in shades of red (Furniture & Appliances, Building Materials & Gasoline Stations):

Weakness within the retail sales complex has continued to accumulate, with 50% of industries now showing negative nominal growth versus one year prior:

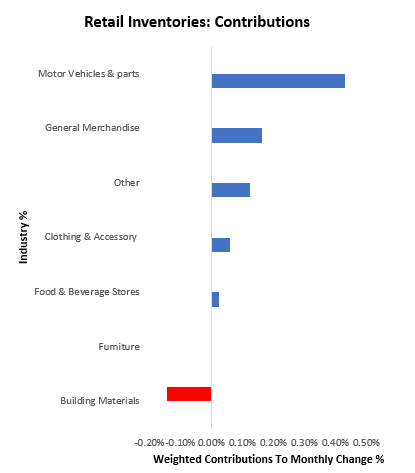

Consistent with the most recent sales data, the latest inventory data showed that retail inventories increased by 0.66%. Below, we offer the composition of these sales over the most recent month:

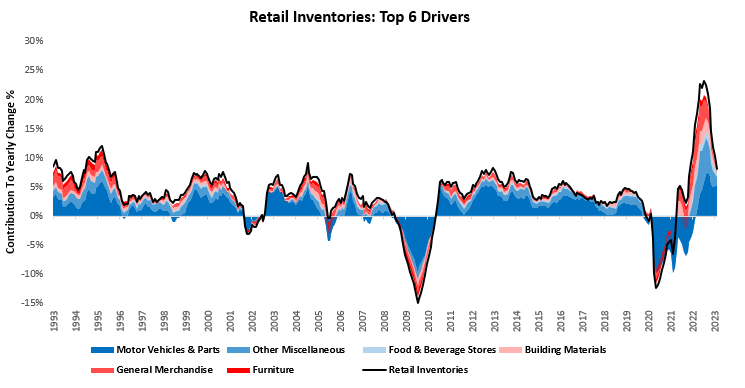

As we can see above, motor vehicle inventories continue to drive inventories higher. This remains consistent with the extremely low level of motor vehicle inventories that dealers possess and are inclined to replenish. This has been the dominant driver of inventories over the last year:

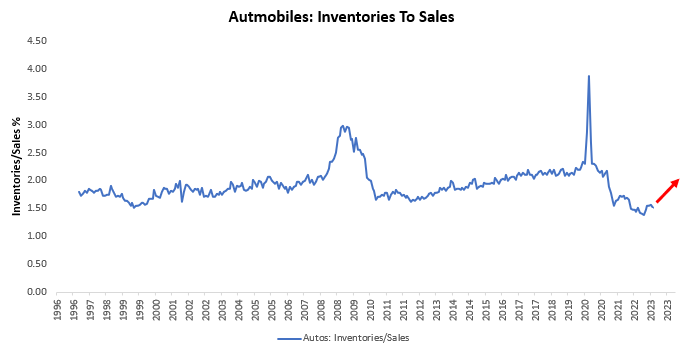

Given the dearth of automobile inventories, we expect this to be an ongoing pressure unless automobile sales deteriorate meaningfully. Below, we show the extremely low levels of inventories relative to sales:

Keep in mind higher inventories to sell can be achieved through either more inventories or fewer sales; it remains to be seen how we will get to equilibrium. For the time being, inventories continue to scale.

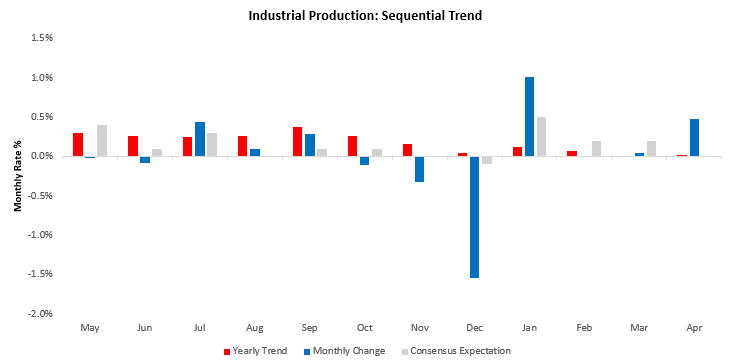

Alongside this weak real consumer demand, we saw positive industrial production growth. Industrial Production increased by 0.48% in April, surprising consensus expectations of 0%. This print contributed to a sequential acceleration in the quarterly trend relative to the yearly trend. Below, we show the monthly evolution of the data relative to its 12-month trend and consensus expectations:

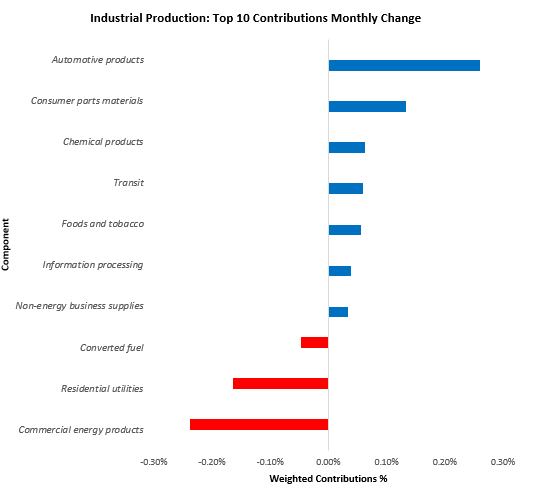

Below, we show the top 10 drivers of the monthly change:

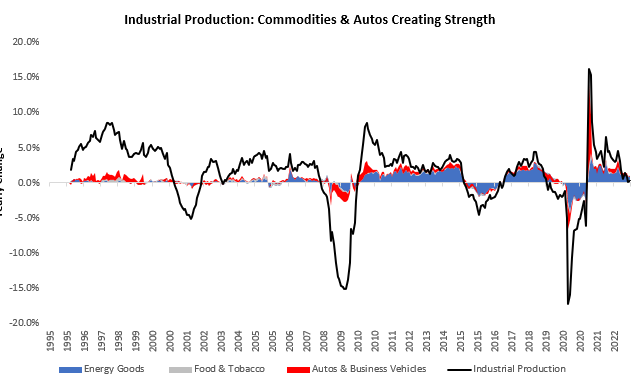

We once again note the strength of automotive products, consistent with strong business demand for automobiles & parts. Zooming out, we show how food, energy, and autos account for all the strength in industrial production (and then some):

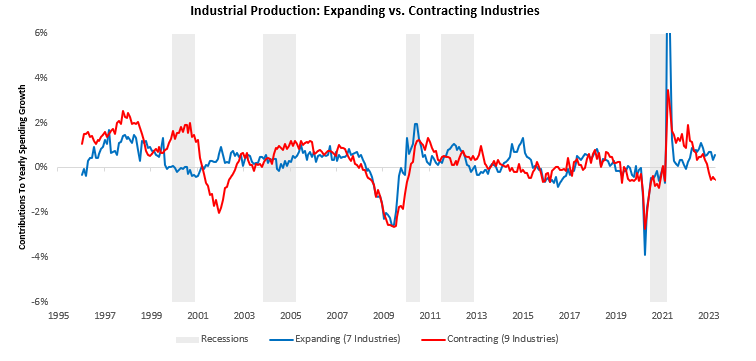

Barring these categories, industrial production is down about 0.80% versus one year prior. Below, we show that this weakness is broad-based across categories. In fact, more industries are contracting than those expanding:

Overall, the picture painted by the latest data points to downward pressures on real consumer spending, particularly in goods. On the other hand, production remains supported by strong business demand for automobiles. The combination of these factors creates a mixed impact on GDP. Nonetheless, we think it is important to recognize that most of the improvement in production comes from idiosyncracies rather than a strong cyclical environment.

I’m really inspired together with your writing abilities and also with the structure in your weblog.

Is that this a paid theme or did you customize it yourself?

Either way keep up the nice high quality writing, it is rare to see a great blog like this one

nowadays. Snipfeed!

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.