Liquidity: Improved, By Likely Unsustainable

Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

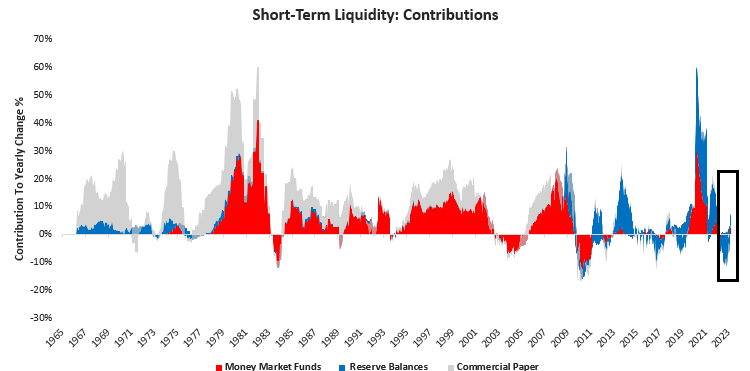

Some of the most significant and complicating factors to the current market picture have been the cross-currents in the liquidity ecosystem. The most recent data suggests that there has been a modest improvement in short-term liquid instruments over the last few weeks. Below, we show our tracking of several key short-term storeholds of liquidity. This does not comprise all potential sources of liquidity but includes those that are particularly relevant to the financial system and markets, i.e., reserve balances, money market funds, and commercial paper:

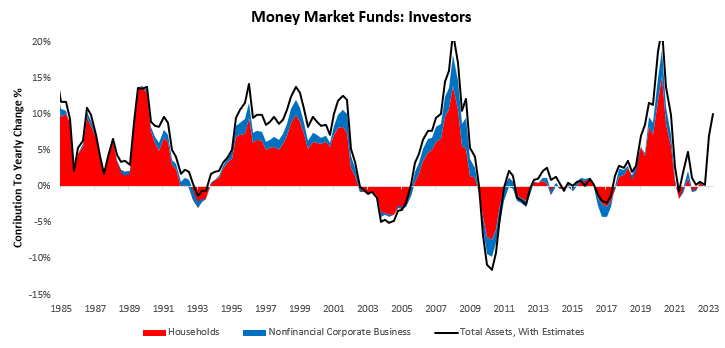

As shown above, these measures have improved significantly from last year’s declines. This improvement was driven by a significant increase in money market fund inflows and a slowdown in reserve contraction at the Federal Reserve. Below, we show how a combination of households and corporates inflows have typically dominated these money market flows:

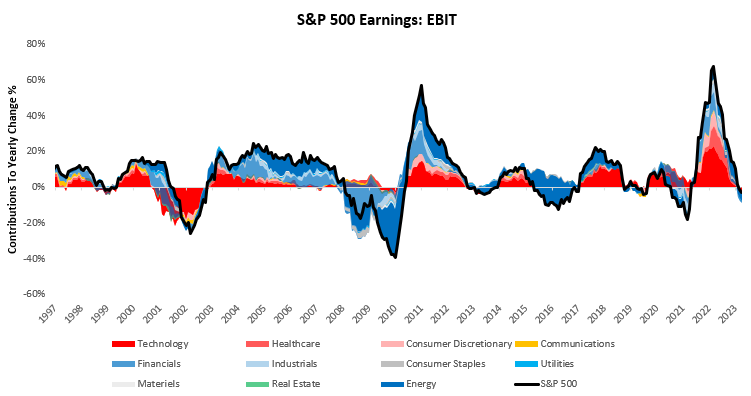

Households and corporate recycle their savings into financial assets. Depending on the economic environment, they choose between highly liquid investments with minimal returns and less-liquid assets with higher returns. The nominal gains of this economic cycle have primarily found their way into the former, i.e., highly-liquid, risk-averse, short-term instruments like money markets funds. These inflows support future economic and market activity, as when conditions warrant, these cash balances can easily migrate to risk-taking activity. What is essential to recognize is that these flows are a function of the profit and income activity in the economy. As we get further into a profit contraction, the flows into these products will also dwindle. Below, we show how S&P 500 profitability has entered contractionary territory:

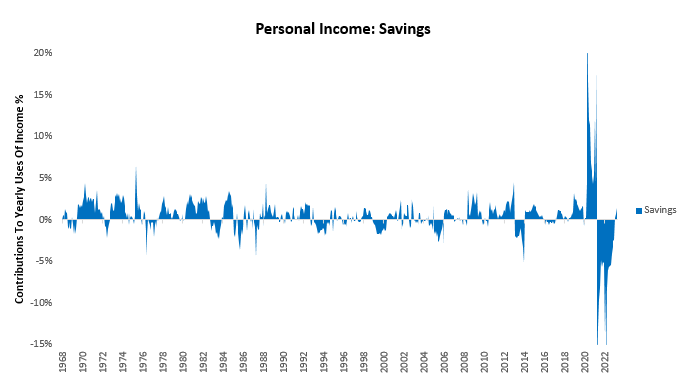

While profits have contracted, somewhat higher personal savings have offset these declines. These savings are the primary source of inflows into money market funds. We show this modest improvement in savings below:

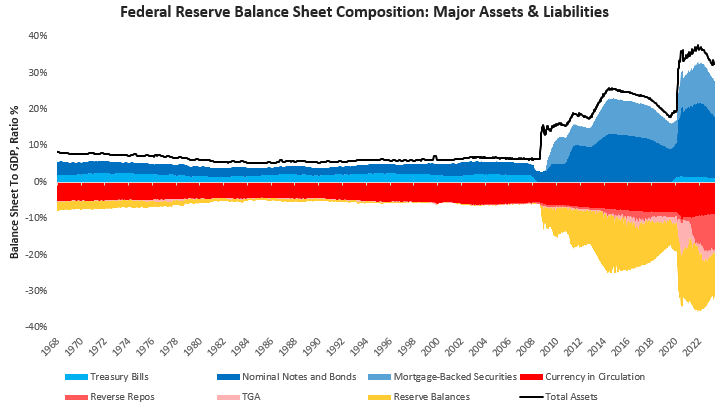

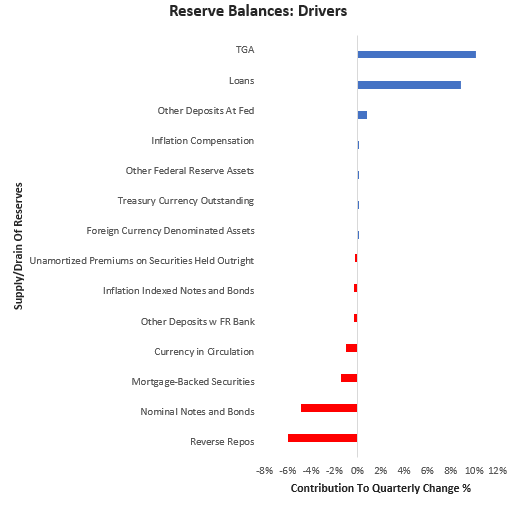

We now turn to the next driver of the current liquidity environment, the Federal Reserve and its balance sheet policy. Below, we show the big-picture drivers of the Fed’s assets (Treasuries & MBS) and liabilities ( Treasury Account, Reverse Repo Facility & Reserve Balances). Positive values are assets, whereas negative values are liabilities:

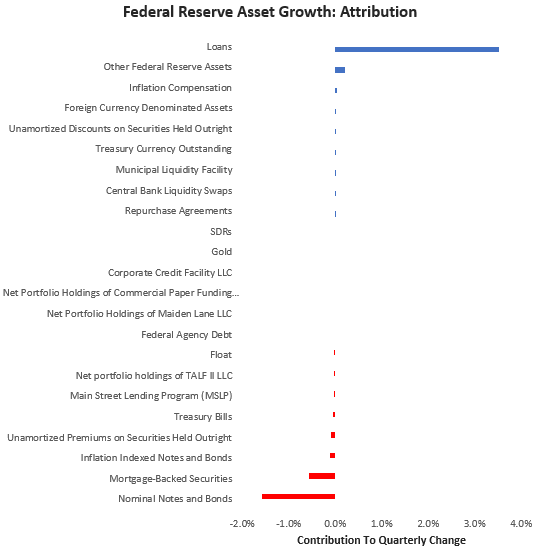

It is well known that the Fed is attempting to contract its balance sheet and increase interest rates to contain inflation. However, the path to balance sheet contraction has been bumpy as the severity of liquidity withdrawal has caused issues in the banking systems, forcing the Fed to perform emergency operations that increase liquidity in the financial system. Over the last quarter, the Fed assets have increased by 1.4%:

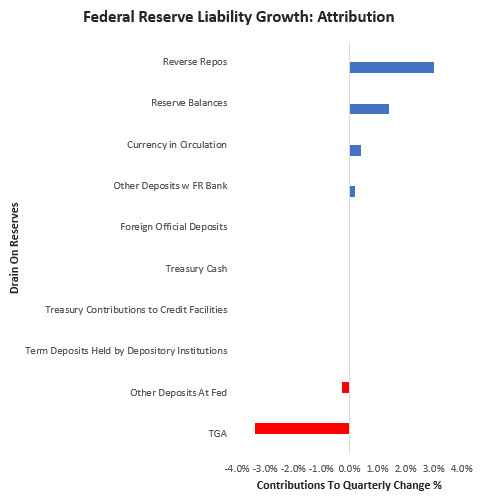

As we can see above, while the Fed has continued to reduce its Treasury & MBS holdings, emergency loans have increased the size of the balance sheet over the past quarter. Alongside this change in assets, we have seen liabilities (ex-reserves) roughly flat. Below, we show the composition of the changes in liabilities:

As the debt ceiling debate continues, this flatling of liabilities ex-reserves was primarily driven by significant spending from the Treasury General Account at the Fed. These factors led to a meaningful increase in reserve balances over the last quarter. The change in reserve balances is the critical determinant of how much the Federal Reserve’s balance sheet reduction impacts financial markets. Reserve balances are determined by the level of the Fed’s assets net of their other liabilities. Below, we show how assets and liabilities have come together to drive reserves over the last quarter:

Looking ahead, without a sustained debt ceiling problem and sustained loan expansion to the private sector we think it is essential to consider that reserve balances will likely resume their downward path as the Fed attempts to control financial conditions. This remains a significant headwind for liquidity.

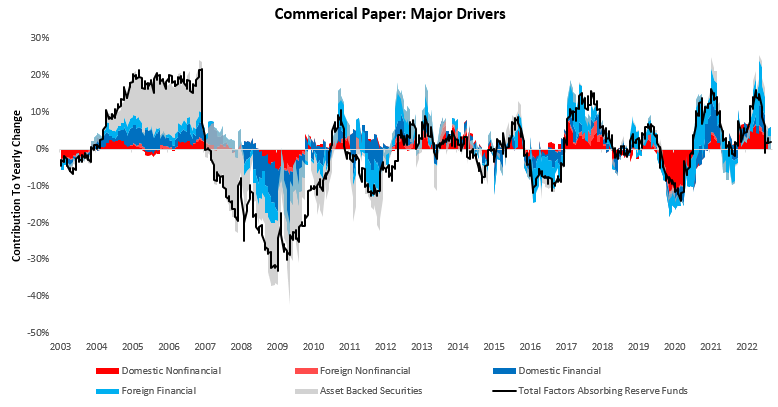

Finally, we turn to commercial paper, where we see the most softening over the last quarter. However, commercial paper changes have not been adequate to overpower the changes in money markets and reserves. Below, we show the yearly changes and composition of commercial paper markets:

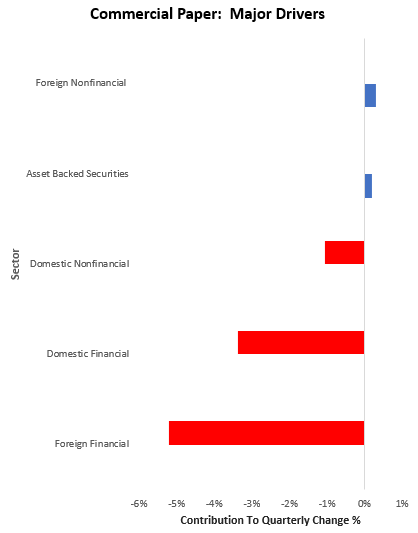

Zooming into the most recent quarter, we see significant weakness in financial sector commercial paper issuance, which is consistent with funding stress within the sector:

Overall, the liquidity picture remains supported by strong nominal incomes in the economy and moderation in the pace of the Fed’s tightening. Given the cyclical pressures present in the economy today, it is hard to see these dynamics persisting. Additionally, the more money market inflows persist through high nominal activity, the more the Fed will have to curtail liquidity. Therefore, while liquidity has improved due to these dynamics, it is unlikely to be sustained by them. This is a headwind for assets. Until next time.

Hi! Do you know if they make any plugins to help with Search

Engine Optimization? I’m trying to get my site to rank for some targeted keywords

but I’m not seeing very good gains. If you know

of any please share. Many thanks! You can read similar text here:

Wool product

With only a 50-cc engine producing 4.2 horsepower, the 155 was capable of cruise at forty five mph.

sugar defender official website Incorporating Sugar Protector into my everyday routine has actually been a game-changer for

my total well-being. As a person that already prioritizes healthy and balanced consuming, sugar defender ingredients this supplement has actually supplied an added

boost of security. in my energy degrees, and my desire for undesirable snacks so uncomplicated

can have such an extensive influence on my day-to-day

live.

sugar defender ingredients Sugarcoating Defender to my day-to-day routine was just one of the best choices I’ve created my health and wellness.

I beware concerning what I eat, but this supplement includes an added layer

of assistance. I feel extra constant throughout the day, and my food

cravings have decreased dramatically. It’s nice to have something so straightforward that makes such a huge distinction! sugar defender ingredients

sugar defender Discovering Sugar Protector has actually been a game-changer for me, as I’ve always been vigilant regarding

handling my blood sugar level levels. With this supplement, I really feel encouraged to take charge of my wellness,

and my most current medical examinations have actually mirrored a considerable

turn-around. Having a reliable ally in my corner gives me with a sense of security and reassurance, and I’m deeply thankful for

the profound difference Sugar Defender has made in my health.

sugar defender official website

sugar defender reviews Incorporating Sugar Defender right into my everyday regimen has

actually been a game-changer for my total health.

As someone that currently prioritizes healthy eating, this supplement has actually given an included increase of protection. in my power levels, and my desire for harmful treats so effortless can have such

a profound effect on my daily life. sugar defender

sugar defender reviews For years, I’ve fought unpredictable blood glucose swings that left me really feeling drained pipes and lethargic.

But considering that including Sugar my power degrees are currently steady and

constant, and I no longer strike a wall in the afternoons.

I value that it’s a gentle, all-natural approach that doesn’t featured any type of undesirable negative effects.

It’s really transformed my every day life. sugar defender

reviews

sugar defender ingredients Finding Sugar Protector has actually been a game-changer for me,

as I’ve always been vigilant about managing my blood sugar degrees.

With this supplement, I feel equipped to organize my wellness,

and my latest medical examinations have actually reflected a significant turnaround.

Having a trustworthy ally in my edge provides me with a sense of security and confidence, and I’m deeply happy for the profound difference Sugar Protector has made in my wellness.

That is a very good tip especially to those fresh to the blogosphere. Brief but very accurate info… Appreciate your sharing this one. A must read post!

This page truly has all of the information and facts I needed about this subject and didn’t know who to ask.

Howdy! This article could not be written much better! Looking through this post reminds me of my previous roommate! He constantly kept preaching about this. I’ll send this post to him. Pretty sure he will have a good read. Thanks for sharing!

I like reading an article that will make people think. Also, many thanks for allowing for me to comment.

Great article. I’m facing some of these issues as well..

Nice post. I learn something totally new and challenging on blogs I stumbleupon on a daily basis. It’s always useful to read through content from other writers and practice something from their sites.

That is a great tip especially to those fresh to the blogosphere. Short but very accurate info… Thank you for sharing this one. A must read article!

I love it when folks come together and share thoughts. Great blog, keep it up!

I used to be able to find good info from your content.

It’s hard to find well-informed people for this topic, however, you seem like you know what you’re talking about! Thanks

I seriously love your site.. Excellent colors & theme. Did you make this amazing site yourself? Please reply back as I’m looking to create my own blog and would like to learn where you got this from or exactly what the theme is called. Thank you!

I’m very happy to uncover this website. I wanted to thank you for your time just for this wonderful read!! I definitely loved every part of it and I have you saved as a favorite to look at new stuff on your blog.

I’d like to thank you for the efforts you’ve put in penning this blog. I really hope to check out the same high-grade blog posts from you later on as well. In fact, your creative writing abilities has motivated me to get my own site now 😉

This is a topic that is close to my heart… Many thanks! Exactly where are your contact details though?

An extremely good post. This post sums up for me just what this topic is all about and some of the major benefits that can be produced by knowing about it just like you. A friend once pointed out that you have a totally different approach when you do something for certain as opposed to when you’re simply just toying with it. In the case of this specific topic, I believe you’re taking, or start to go for, a more professional plus thorough approach to what and how you’re writing, which in turn helps you to continue to get better and help others who don’t know anything at all about what you have discussed here. Thank you.

Can I simply say what a relief to discover someone that really understands what they’re discussing online. You definitely understand how to bring a problem to light and make it important. More and more people really need to check this out and understand this side of your story. I was surprised that you aren’t more popular because you definitely have the gift.

Great blog you have got here.. It’s difficult to find high quality writing like yours nowadays. I honestly appreciate people like you! Take care!!

I discovered your site website on bing and appearance many of your early posts. Preserve within the really good operate. I just now extra increase Rss to my MSN News Reader. Seeking forward to reading much more of your stuff afterwards!…

Heya just wanted to give you a brief heads up and let you know a few of the pictures aren’t loading correctly. I’m not sure why but I think its a linking issue. I’ve tried it in two different web browsers and both show the same results.

Pretty! This was a really wonderful post. Thanks for providing this info.

Wonderful beat ! I wish to apprentice while you amend your website, how could i subscribe for a blog website? The account aided me a acceptable deal. I had been a little bit acquainted of this your broadcast provided bright clear idea

There is certainly a great deal to learn about this issue. I love all the points you’ve made.

Good web site you have got here.. It’s difficult to find high quality writing like yours these days. I honestly appreciate people like you! Take care!!

This is a topic that is close to my heart… Best wishes! Where are your contact details though?

Thanks for another informative site. Where else could I get that type of information written in such an ideal way? I’ve a project that I am just now working on, and I have been on the look out for such information.

nail on the head. Your concept is excellent; the difficulty is something that not sufficient people are speaking intelligently about. I am very blissful

Magnificent web site. A lot of helpful information here. I am sending it to some pals ans additionally sharing in delicious. And obviously, thanks for your sweat!

Simply a smiling visitor here to share the love (:, btw outstanding design . “Audacity, more audacity and always audacity.” by Georges Jacques Danton.

Hello there! I just wish to offer you a huge thumbs up for the excellent info you have right here on this post. I will be coming back to your web site for more soon.

I think this web site has very superb composed subject material articles .

Nice post. I understand something harder on various blogs everyday. It will always be stimulating to see content from other writers and practice a little something from their website. I’d want to use some together with the content on my weblog regardless of whether you don’t mind. Natually I’ll supply you with a link on your own internet blog. Thank you sharing.

This is really important, You’re a remarkably expert article author. I’ve joined with your feed and also count on reading your excellent write-ups. In addition to that, I’ve shared your websites inside our web pages.

Hi, Neat post. There is an issue with your web site in web explorer, would test this¡K IE nonetheless is the market leader and a large element of folks will omit your excellent writing because of this problem.

I absolutely love your website.. Very nice colors & theme. Did you develop this web site yourself? Please reply back as I’m wanting to create my own site and would love to learn where you got this from or just what the theme is named. Appreciate it!

The ending, for me, was very unsatisfying, and there was no emotional payoff from the subplot involving Roy’s past, just an ineffective punch line.

I was just searching for this information for a while. After six hours of continuous Googleing, at last I got it in your website. I wonder what is the lack of Google strategy that don’t rank this type of informative web sites in top of the list. Generally the top websites are full of garbage.

Hey, you used to write wonderful, but the last few posts have been kinda boring… I miss your tremendous writings. Past few posts are just a little out of track! come on!

Thank you pertaining to discussing that superb content material on your web site. I ran into it on the search engines. I am going to check to come back after you publish extra aricles.

hi was just seeing if you minded a comment. i like your website and the thme you picked is super. I will be back.

This is my first time I have visited your site. I found a lot of interesting information in your blog. From the tons of comments on your posts, I guess I am not the only one! keep up the great work.

There is definately a great deal to find out about this topic. I really like all the points you made.

Nice blog here! Additionally your website loads up very fast! What web host are you the usage of? Can I am getting your associate link on your host? I wish my website loaded up as quickly as yours lol

Your article continually have alot of really up to date info. Where do you come up with this? Just stating you are very inspiring. Thanks again

Hmm is anyone else encountering problems with the pictures on this blog loading? I’m trying to figure out if its a problem on my end or if it’s the blog. Any responses would be greatly appreciated.

poetry has the power to affect our emotions by using words alone, i really love poetry“

I never would have thought this stuff was out there. Thanks! I look foward to checking out your articles in the future.

I’d always want to be update on new articles on this web site , saved to favorites ! .

Youre so cool! I dont suppose Ive read anything like this before. So nice to search out any person with some original thoughts on this subject. realy thank you for starting this up. this website is something that’s wanted on the net, someone with somewhat originality. useful job for bringing something new to the web!

Quite easily, the article is in reality the sweetest on this laudable topic. I agree with your conclusions and definitely will eagerly look forward to your approaching updates. Simply just saying thanks will certainly not simply just be sufficient, for the outstanding lucidity in your writing. I can right away grab your rss feed to stay privy of any updates. Good work and much success in your business efforts!

Considerably, the actual publish is usually the finest about this deserving topic. I agree with your results and in addition may excitedly anticipate your potential updates. Simply just stating thank you will not merely you should be sufficient, for that wonderful quality inside your writing. I’ll right away seize your rss feed to stay up-to-date with any kind of updates. Genuine perform and in addition much achievement inside your enterprise dealings!

This is a topic that’s close to my heart… Take care! Exactly where are your contact details though?

Great post! We will be linking to this particularly great article on our site. Keep up the good writing.

Excellent information again. I am looking forward for more updates.

Informative, pretty much as I had come to expect from this site.

This is some enjoyable stuff. It took me a while to locate this website but it was worth the time. I noticed this page was buried in google and not the number one spot. This web site has a ton of nice stuff and it does not deserve to be burried in the search engines like that. By the way Im going to save this website to my favorites.

Thats pretty cool! I look forward to reading more of your posts.

I was more than happy to find this great site. I need to to thank you for your time due to this wonderful read!! I definitely really liked every part of it and I have you saved as a favorite to look at new stuff in your website.

Hi there, just became aware of your blog through Google, and found that it’s truly informative. I’m going to watch out for brussels. I’ll be grateful if you continue this in future. Numerous people will be benefited from your writing. Cheers!

Hey dude, what kind of wordpress theme are you using? i want it to use on my blog too ,

you have a excellent blog here! would you like to have the invite posts in my blog?

most of the best ringtone sites are pay sites, does anyone know of a good free ringtone site?,,

This is a great tip especially to those fresh to the blogosphere. Short but very accurate information… Thanks for sharing this one. A must read post!

Aw, this was a very nice post. Taking the time and actual effort to produce a top notch article… but what can I say… I hesitate a lot and never seem to get nearly anything done.

Hi there! This post could not be written any better! Looking at this post reminds me of my previous roommate! He continually kept preaching about this. I will send this article to him. Fairly certain he will have a good read. Thank you for sharing!

Your blog is one of a kind, i love the way you organize the topics.”:*,,

Hello there! Are you aware when they help to make virtually any extensions to assist together with SEO? I’m trying to get my personal website to rate for some targeted keywords however i’m not necessarily experiencing very good benefits. If you know of the please discuss. Be thankful!

I do not know if it’s just me or if everybody else experiencing issues with your blog. It appears as though some of the text on your content are running off the screen. Can someone else please provide feedback and let me know if this is happening to them as well? This might be a issue with my web browser because I’ve had this happen before. Thanks

Greetings! This is my first visit to your blog! We are a group of volunteers and starting a new project in a community in the same niche. Your blog provided us useful information to work on. You have done a wonderful job!

Hi, I had been studying the net and I ran into your own blog. Maintain up the excellent function.

Hello, I do believe your website may be having internet browser compatibility issues. Whenever I look at your site in Safari, it looks fine however, if opening in I.E., it has some overlapping issues. I simply wanted to provide you with a quick heads up! Besides that, great blog!

Thank you pertaining to discussing that superb content material on your web site. I ran into it on the search engines. I am going to check to come back after you publish extra aricles.

I could not resist commenting. Exceptionally well written.

I used to be able to find good info from your content.

You made some decent points there. I checked on the web to learn more about the issue and found most people will go along with your views on this site.

I used to be able to find good advice from your articles.

I’m curious to find out what blog platform you happen to be using? I’m having some minor security issues with my latest website and I’d like to find something more safe. Do you have any recommendations?

Nearly all goods are typically hand designed plus subsistence economic local weather dominates. Individualism is really weakly manufactured within just persons ethnicities given that are typically interpersonal programs. Unaltered customers ethnicities no extra can be determined inside industrialized nations much like the Usa plus North america.

There’s certainly a great deal to find out about this issue. I really like all of the points you made.

After study a handful of the blog posts on your site now, and I really as if your way of blogging. I bookmarked it to my bookmark site list and you will be checking back soon. Pls look at my internet site in addition and let me know what you believe.

I applaud this writer for writing such unique and quality information with viewpoints I can understand. I couldn’t stop reading this article. I got so engrossed in this material. Thanks!

Good day! I could have sworn I’ve been to this blog before but after reading through some of the post I realized it’s new to me. Nonetheless, I’m definitely glad I found it and I’ll be bookmarking and checking back often!

Spot on with this write-up, I truly suppose this website wants far more consideration. I’ll in all probability be once more to learn much more, thanks for that info.

An intriguing discussion is worth comment. I do believe that you ought to publish more about this subject matter, it might not be a taboo matter but generally folks don’t talk about such issues. To the next! Best wishes!

You’re so cool! I don’t think I’ve read through anything like this before. So great to discover somebody with some unique thoughts on this subject. Really.. thanks for starting this up. This site is one thing that is required on the internet, someone with a little originality.

This site truly has all the info I needed concerning this subject and didn’t know who to ask.

After looking into a few of the blog articles on your site, I honestly appreciate your way of blogging. I book-marked it to my bookmark site list and will be checking back in the near future. Take a look at my website too and tell me your opinion.

There’s definately a great deal to learn about this topic. I really like all the points you have made.

Saved as a favorite, I like your website!

Great information. Lucky me I ran across your website by accident (stumbleupon). I’ve book-marked it for later!

The very next time I read a blog, Hopefully it doesn’t disappoint me as much as this particular one. After all, Yes, it was my choice to read, nonetheless I genuinely thought you would have something interesting to talk about. All I hear is a bunch of complaining about something you could possibly fix if you were not too busy seeking attention.

You made some really good points there. I looked on the web for more info about the issue and found most individuals will go along with your views on this website.

Excellent post! We will be linking to this particularly great content on our site. Keep up the good writing.

Your style is really unique compared to other people I have read stuff from. Thank you for posting when you’ve got the opportunity, Guess I will just book mark this page.

After looking at a few of the blog articles on your site, I honestly like your technique of blogging. I saved as a favorite it to my bookmark site list and will be checking back in the near future. Please check out my website as well and let me know what you think.

Your style is very unique in comparison to other people I’ve read stuff from. Thanks for posting when you’ve got the opportunity, Guess I’ll just book mark this blog.

I must thank you for the efforts you’ve put in writing this blog. I really hope to view the same high-grade blog posts by you in the future as well. In truth, your creative writing abilities has encouraged me to get my own, personal site now 😉

After I initially left a comment I appear to have clicked the -Notify me when new comments are added- checkbox and now every time a comment is added I receive four emails with the exact same comment. Is there an easy method you can remove me from that service? Cheers.

Good article! We will be linking to this great post on our site. Keep up the great writing.

I’m amazed, I must say. Rarely do I encounter a blog that’s both educative and interesting, and without a doubt, you’ve hit the nail on the head. The issue is something which too few folks are speaking intelligently about. I am very happy that I stumbled across this in my hunt for something regarding this.

There is certainly a lot to know about this subject. I really like all of the points you’ve made.

Having read this I thought it was really informative. I appreciate you taking the time and effort to put this short article together. I once again find myself personally spending a lot of time both reading and commenting. But so what, it was still worthwhile.

I like reading through an article that can make men and women think. Also, thanks for allowing me to comment.

Pretty! This was a really wonderful article. Thank you for providing these details.

Watch our exclusive Neerfit sexy bf video on neerfit.co.in.

Oh my goodness! Awesome article dude! Many thanks, However I am going through problems with your RSS. I don’t understand why I cannot join it. Is there anybody else having similar RSS problems? Anyone who knows the answer will you kindly respond? Thanx!!

Great info. Lucky me I came across your blog by accident (stumbleupon). I’ve saved it for later.

super content. thanks for your effort

Next time I read a blog, Hopefully it won’t disappoint me just as much as this one. After all, I know it was my choice to read, however I actually believed you would probably have something interesting to talk about. All I hear is a bunch of complaining about something you could fix if you weren’t too busy seeking attention.

I was very happy to find this website. I want to to thank you for your time due to this wonderful read!! I definitely savored every bit of it and i also have you book marked to check out new information in your web site.

When I originally left a comment I appear to have clicked the -Notify me when new comments are added- checkbox and now each time a comment is added I recieve four emails with the same comment. Perhaps there is a means you can remove me from that service? Thank you.

This is a topic that’s close to my heart… Many thanks! Where can I find the contact details for questions?

Hi! I simply would like to give you a huge thumbs up for the great info you have got here on this post. I will be coming back to your blog for more soon.

This is a topic that’s close to my heart… Cheers! Where are your contact details though?

Hey there! I just want to offer you a big thumbs up for your excellent info you have here on this post. I will be returning to your web site for more soon.

Hey there! I just want to offer you a big thumbs up for the great info you have right here on this post. I will be returning to your blog for more soon.

I like reading through a post that will make people think. Also, many thanks for permitting me to comment.

Everyone loves it when folks get together and share opinions. Great blog, keep it up!

This page definitely has all the info I needed about this subject and didn’t know who to ask.

Sorry for that large evaluation, but I’m really loving the brand new Zune, as well as wish this particular, along with the superb reviews another individuals wrote, can help you determine if it’s the correct selection for you.

Hi, I do think this is a great blog. I stumbledupon it 😉 I may come back yet again since i have book-marked it. Money and freedom is the best way to change, may you be rich and continue to help others.

Saved as a favorite, I like your site!

This website really has all of the information I wanted about this subject and didn’t know who to ask.

Very good information. Lucky me I found your blog by accident (stumbleupon). I have saved as a favorite for later!

Good write-up. I definitely love this website. Keep it up!

Having read this I thought it was extremely enlightening. I appreciate you finding the time and effort to put this article together. I once again find myself personally spending a significant amount of time both reading and commenting. But so what, it was still worthwhile!

Right here is the perfect website for anybody who wishes to understand this topic. You realize so much its almost tough to argue with you (not that I really will need to…HaHa). You certainly put a fresh spin on a topic that’s been written about for many years. Great stuff, just great.

Excellent post. I am experiencing a few of these issues as well..

Hi! I just wish to give you a huge thumbs up for your excellent info you have right here on this post. I’ll be coming back to your website for more soon.

That is a good tip particularly to those new to the blogosphere. Brief but very precise info… Thank you for sharing this one. A must read post.

Wonderful article! We are linking to this particularly great post on our website. Keep up the good writing.

There is certainly a great deal to learn about this topic. I really like all of the points you’ve made.

Excellent blog post. I definitely love this site. Stick with it!

The next time I read a blog, Hopefully it doesn’t disappoint me as much as this one. After all, I know it was my choice to read through, however I really believed you’d have something useful to talk about. All I hear is a bunch of whining about something you could fix if you were not too busy searching for attention.

Having read this I thought it was extremely enlightening. I appreciate you taking the time and energy to put this article together. I once again find myself personally spending a significant amount of time both reading and posting comments. But so what, it was still worthwhile.

I’m very happy to find this great site. I want to to thank you for your time for this wonderful read!! I definitely savored every bit of it and i also have you saved to fav to see new information in your web site.

It’s difficult to find knowledgeable people about this topic, however, you seem like you know what you’re talking about! Thanks

I used to be able to find good information from your articles.

Wonderful web site. Lots of helpful info here. I am sending it to some friends ans additionally sharing in delicious. And naturally, thanks on your sweat!

Way cool! Some extremely valid points! I appreciate you writing this article and the rest of the website is very good.

May I simply just say what a relief to find somebody that actually understands what they’re discussing online. You certainly realize how to bring an issue to light and make it important. More and more people ought to check this out and understand this side of the story. I was surprised you’re not more popular since you definitely have the gift.

I used to be able to find good information from your content.

This is very fascinating, You’re an excessively skilled blogger. I have joined your feed and sit up for looking for more of your fantastic post. Also, I’ve shared your web site in my social networks!

when we are looking for apartment for rents, we usually choose those with very clean rooms”

It’s hard to find experienced people in this particular subject, however, you seem like you know what you’re talking about! Thanks

This blog was… how do you say it? Relevant!! Finally I have found something that helped me. Appreciate it.

Great article, thanks. I signed up to your blog rss feed.

Oh my goodness! an excellent write-up dude. Thanks Even so My business is experiencing problem with ur rss . Do not know why Not able to join it. Could there be anyone obtaining identical rss dilemma? Anyone who knows kindly respond. Thnkx

Spot on with this write-up, I seriously believe this site needs a great deal more attention. I’ll probably be returning to see more, thanks for the information.

I was able to find good information from your articles.

There is noticeably a lot of money to learn about this. I suppose you made certain nice points in functions also.

stays on topic and states valid points. Thank you.

I love it when folks come together and share ideas. Great website, stick with it.

When I initially left a comment I seem to have clicked on the -Notify me when new comments are added- checkbox and now each time a comment is added I get four emails with the exact same comment. Is there an easy method you are able to remove me from that service? Kudos.

When I originally commented I clicked the -Notify me when new surveys are added- checkbox and from now on each time a comment is added I get four emails sticking with the same comment. Is there however you may get rid of me from that service? Thanks!

Can I just say what a reduction to search out someone who actually is aware of what theyre speaking about on the internet. You positively know learn how to carry a difficulty to gentle and make it important. Extra individuals have to learn this and understand this aspect of the story. I cant believe youre not more standard since you positively have the gift.

very nice put up, i actually love this web site, keep on it

Hi there! This blog post could not be written much better! Reading through this post reminds me of my previous roommate! He always kept preaching about this. I’ll send this information to him. Fairly certain he will have a great read. Many thanks for sharing!

An impressive share! I have just forwarded this onto a co-worker who had been conducting a little research on this. And he actually bought me lunch due to the fact that I discovered it for him… lol. So allow me to reword this…. Thank YOU for the meal!! But yeah, thanks for spending the time to talk about this issue here on your web site.

Saved as a favorite, I love your blog!

An outstanding share! I’ve just forwarded this onto a colleague who had been doing a little homework on this. And he actually ordered me lunch due to the fact that I stumbled upon it for him… lol. So let me reword this…. Thanks for the meal!! But yeah, thanks for spending the time to talk about this issue here on your website.

Very nice post. I definitely love this website. Continue the good work!

Hello there! I could have sworn I’ve visited this web site before but after browsing through many of the posts I realized it’s new to me. Regardless, I’m definitely delighted I discovered it and I’ll be book-marking it and checking back regularly.

Aw, this was a really nice post. Finding the time and actual effort to create a superb article… but what can I say… I procrastinate a whole lot and don’t manage to get nearly anything done.

This site was… how do I say it? Relevant!! Finally I have found something which helped me. Cheers!

You should take part in a contest for one of the finest blogs on the web. I most certainly will recommend this web site!

Your style is very unique compared to other folks I have read stuff from. Thanks for posting when you’ve got the opportunity, Guess I will just bookmark this web site.

Very good information. Lucky me I recently found your site by accident (stumbleupon). I’ve book marked it for later!

https://naveridbuy.blogspot.com/2024/11/blog-post_95.html

https://naveridbuy.exblog.jp/37090861/

https://viastoer.blogspot.com/2024/09/blog-post_60.html

https://adaptable-camellia-dd3cm4.mystrikingly.com/blog/25f45f68c48

https://hallbook.com.br/blogs/376912/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%ED%9B%84-%EA%B3%84%EC%A0%95-%EC%A0%95%EC%A7%80-%EC%82%AC%EB%A1%80%EC%99%80-%EB%8C%80%EC%B2%98%EB%B2%95

https://adaptable-goat-dd3cmf.mystrikingly.com/blog/c2a25554bec

https://xn--w0-hd0jg6f81lm0dhhw74c.mystrikingly.com/blog/2ea87cc6ee1

Way cool! Some very valid points! I appreciate you penning this write-up plus the rest of the site is extremely good.

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EC%97%B0%EB%8F%99%ED%95%9C-%EB%8B%A4%EB%A5%B8-%EC%84%9C%EB%B9%84%EC%8A%A4-%ED%99%9C%EC%9A%A9%EB%B2%95-5dde0d66c6f6

https://gajweor.pixnet.net/blog/post/157629706

https://gajweor.pixnet.net/blog/post/157629805

After I originally commented I appear to have clicked on the -Notify me when new comments are added- checkbox and from now on every time a comment is added I recieve four emails with the same comment. Is there a way you can remove me from that service? Kudos.

https://viastoer.blogspot.com/2024/09/blog-post_68.html

https://thoughtful-fox-dbgzh7.mystrikingly.com/blog/55d38114fa0

https://medium.com/@nsw5288/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EB%A8%B9%EC%9C%BC%EB%A9%B4-%EB%82%98%ED%83%80%EB%82%98%EB%8A%94-%EC%A6%9D%EC%83%81-2ababd9c0624

https://gwojawe-fjaow-jiao.mystrikingly.com/blog/669541f58ff

Hi, I do believe this is a great website. I stumbledupon it 😉 I’m going to return once again since i have book marked it. Money and freedom is the best way to change, may you be rich and continue to help other people.

https://maize-wombat-dd3cms.mystrikingly.com/blog/b957b6440d6

https://xn--fw-hd0jg6f81ltjas9lbns.mystrikingly.com/blog/6f069f7e8a8

https://medium.com/@1kelly76/%EB%B0%9C%EA%B8%B0%EB%B6%80%EC%A0%84%EA%B3%BC-%EC%A1%B0%EB%A3%A8-%EC%9E%90%EC%97%B0%EC%B9%98%EB%A3%8C%EC%99%80-%EC%9D%98%ED%95%99%EC%A0%81-%EC%A0%91%EA%B7%BC%EB%B2%95-%EB%B9%84%EA%B5%90-afd49503b11b

You need to be a part of a contest for one of the most useful sites on the web. I’m going to highly recommend this blog!

https://ko.anotepad.com/note/read/wyj88hps

Next time I read a blog, I hope that it doesn’t disappoint me as much as this particular one. I mean, Yes, it was my choice to read, however I actually thought you’d have something helpful to talk about. All I hear is a bunch of moaning about something you could possibly fix if you were not too busy looking for attention.

https://witty-apple-dd3cm1.mystrikingly.com/blog/10

https://ko.anotepad.com/note/read/qscmkp7h

https://telegra.ph/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4-%EC%9D%B4%EB%A0%87%EA%B2%8C-%ED%95%98%EB%A9%B4-%EC%95%88%EC%A0%84%ED%95%A9%EB%8B%88%EB%8B%A4-09-20

https://naveridbuy.exblog.jp/37091016/

https://naveridbuy.exblog.jp/37090861/

https://inky-owl-dd3cmv.mystrikingly.com/blog/3cf53348e92

Hello, There’s no doubt that your site may be having browser compatibility problems. When I take a look at your blog in Safari, it looks fine but when opening in I.E., it has some overlapping issues. I just wanted to provide you with a quick heads up! Aside from that, fantastic site!

https://viastoer.blogspot.com/2024/09/blog-post_14.html

https://ko.anotepad.com/note/read/ddhnmc66

https://gajweor.pixnet.net/blog/post/157629508

https://sociable-corn-dd3cmt.mystrikingly.com/blog/2938da193c8

https://writeablog.net/zrusp1buhj

https://naveridbuy.exblog.jp/37091141/

https://xn--le-o02ik82aiqcqsko8mfg5a1sb.mystrikingly.com/blog/d361932a2b9

https://witty-apple-dd3cm1.mystrikingly.com/blog/fc35efb2e09

https://telegra.ph/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EB%AC%B8%EC%A0%9C%EB%A5%BC-%ED%95%B4%EA%B2%B0%ED%95%98%EB%8A%94-%ED%95%A9%EB%B2%95%EC%A0%81%EC%9D%B8-%EB%B0%A9%EB%B2%95-12-13

https://writeablog.net/imt11px743

https://hallbook.com.br/blogs/376908/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%EB%8C%80%EC%8B%A0-%EC%82%AC%EC%9A%A9%ED%95%A0-%EC%88%98-%EC%9E%88%EB%8A%94-%EB%B0%A9%EB%B2%95%EB%93%A4

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94%EC%99%80-%EA%B4%80%EB%A0%A8%EB%90%9C-%EC%B5%9C%EC%8B%A0-%EB%B3%B4%EC%95%88-%EC%9D%B4%EC%8A%88-4569786b88d3

https://naveridbuy.blogspot.com/2024/12/blog-post_27.html

https://medium.com/@nsw5288/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4-%EC%8B%9C-%EA%B0%80%EC%A7%9C-%EC%A0%9C%ED%92%88%EC%9D%84-%ED%94%BC%ED%95%98%EB%8A%94-%EB%B0%A9%EB%B2%95-3f91fcb6bf6f

https://medium.com/@nsw5288/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EB%8C%80%EC%B2%B4-%EC%95%BD%EB%AC%BC%EA%B3%BC-%EB%B9%84%EA%B5%90%ED%95%B4%EB%B3%B4%EC%9E%90-1815aaea63d3

https://viastoer.blogspot.com/2024/07/blog-post_45.html

https://vermilion-elephant-dd3cm3.mystrikingly.com/blog/1ed0baf6713

https://medium.com/@1kelly76/%EB%B0%9C%EA%B8%B0%EB%B6%80%EC%A0%84-%EA%B7%B9%EB%B3%B5%EC%9D%84-%EC%9C%84%ED%95%9C-%ED%95%84%EC%88%98-%EC%83%9D%ED%99%9C-%EC%8A%B5%EA%B4%80-7ecd345e0682

Greetings! Very useful advice in this particular article! It is the little changes that will make the most significant changes. Thanks a lot for sharing!

https://gold-gull-dd3cmf.mystrikingly.com/blog/58fe76cd6ee

https://naveridbuy.exblog.jp/37152040/

https://naveridbuy.blogspot.com/2024/12/blog-post_76.html

https://adaptable-camellia-dd3cm4.mystrikingly.com/blog/79c90dfb696

Hi, I do believe this is a great blog. I stumbledupon it 😉 I am going to come back yet again since i have book marked it. Money and freedom is the best way to change, may you be rich and continue to help other people.

https://hallbook.com.br/blogs/300837/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EC%B2%98%EB%B0%A9%EC%A0%84-%EC%97%86%EC%9D%B4-%EA%B5%AC%EB%A7%A4%ED%95%98%EB%8A%94-%EB%B0%A9%EB%B2%95%EA%B3%BC-%EB%A6%AC%EC%8A%A4%ED%81%AC

https://ameblo.jp/naveridbuy/entry-12861932226.html

https://naveridbuy.exblog.jp/37091064/

https://medium.com/@carlfrancoh38793/%EC%95%84%EC%9D%B4%EB%94%94-%EC%A4%91%EB%B3%B5-%EB%AC%B8%EC%A0%9C-%ED%95%B4%EA%B2%B0-%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%ED%99%9C%EC%9A%A9%EB%B2%95-a0ec8344a6bd

https://telegra.ph/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4%EA%B0%80-%EB%B6%88%EB%9F%AC%EC%98%A4%EB%8A%94-%EB%B3%B4%EC%95%88-%EC%9C%84%ED%97%98-12-13

https://naveridbuy.blogspot.com/2024/12/blog-post_3.html

https://candid-lion-dd3cm3.mystrikingly.com/blog/5037f72f44c

Hey, I loved your post! Check out my site: ANCHOR.

https://medium.com/@1kelly76/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4%EC%99%80-%EC%84%B1%EB%8A%A5-%EB%B9%84%EC%9A%A9-%EB%B9%84%EA%B5%90-2d2ef866fb5e

https://xn--w4-hs1izvv81cmb366re3s.mystrikingly.com/blog/6ae78fa4b70

https://medium.com/@nsw5288/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC%EB%A5%BC-%EC%A0%80%EB%A0%B4%ED%95%98%EA%B2%8C-%EA%B5%AC%EB%A7%A4%ED%95%98%EB%8A%94-%EB%B2%95-%EA%B0%80%EA%B2%A9-%EC%A0%88%EA%B0%90-%ED%8C%81-0d6cba0d9d92

https://viastoer.blogspot.com/2024/09/blog-post_68.html

https://medium.com/@nsw5288/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4-%EC%8B%9C-%EC%95%8C%EC%95%84%EC%95%BC-%ED%95%A0-%EB%B2%95%EC%A0%81-%EB%AC%B8%EC%A0%9C-bd9301a26e37

https://naveridbuy.exblog.jp/37152083/

https://medium.com/@carlfrancoh38793/%EC%95%84%EC%9D%B4%EB%94%94-%EC%83%9D%EC%84%B1-%EC%96%B4%EB%A0%A4%EC%9A%B8-%EB%95%8C-%EA%B5%AC%EB%A7%A4-%EB%8C%80%EC%95%88-%EC%95%8C%EC%95%84%EB%B3%B4%EA%B8%B0-62055e09b46c

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%ED%95%A9%EB%B2%95%EC%9D%B8%EA%B0%80%EC%9A%94-%EC%95%8C%EC%95%84%EB%B4%85%EC%8B%9C%EB%8B%A4-40dff2b624f5

https://writeablog.net/9tndlpy4rw

https://naveridbuy.exblog.jp/37091323/

https://gold-gull-dd3cmf.mystrikingly.com/blog/fa06ca9b8e6

https://medium.com/@carlfrancoh38793/%EB%84%A4%EC%9D%B4%EB%B2%84-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%ED%9B%84-%EA%B4%91%EA%B3%A0-%EA%B4%80%EB%A6%AC%EC%97%90-%ED%99%9C%EC%9A%A9%ED%95%98%EB%8A%94-%EB%B0%A9%EB%B2%95-6a822042a160

https://medium.com/@carlfrancoh38793/%EA%B5%AC%EA%B8%80-%EC%95%84%EC%9D%B4%EB%94%94-%EA%B5%AC%EB%A7%A4-%EC%9D%B4%EC%A0%90%EA%B3%BC-%EB%8B%A8%EC%A0%90%EC%9D%80-%EB%AC%B4%EC%97%87%EC%9D%B8%EA%B0%80%EC%9A%94-4dccd7ee3fc1

https://medium.com/@charlielevesque328/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EC%98%A8%EB%9D%BC%EC%9D%B8-%EA%B5%AC%EB%A7%A4-%ED%9B%84%EA%B8%B0%EC%99%80-%EC%A3%BC%EC%9D%98%ED%95%B4%EC%95%BC-%ED%95%A0-%EC%A0%90%EB%93%A4-4a51bcd6c007

https://hallbook.com.br/blogs/278114/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4-%EC%8B%9C-%EA%B3%A0%EB%A0%A4%ED%95%B4%EC%95%BC-%ED%95%A0-%EA%B0%9C%EC%9D%B8%EC%A0%81%EC%9D%B8-%EA%B1%B4%EA%B0%95-%EC%9A%94%EC%86%8C

https://hallbook.com.br/blogs/326301/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4-%ED%9B%84-%EC%A0%95%ED%92%88-%ED%99%95%EC%9D%B8%ED%95%98%EB%8A%94-5%EA%B0%80%EC%A7%80-%EB%B0%A9%EB%B2%95

https://magenta-romaine-dbgzh9.mystrikingly.com/blog/1ef949a3574

https://naveridbuy.blogspot.com/2024/11/blog-post_95.html

https://medium.com/@charlielevesque328/%EB%B9%84%EC%95%84%EA%B7%B8%EB%9D%BC-%EA%B5%AC%EB%A7%A4-%EC%8B%9C-%EC%95%8C%EC%95%84%EC%95%BC-%ED%95%A0-%EC%9C%A0%EC%9D%98%EC%82%AC%ED%95%AD-7%EA%B0%80%EC%A7%80-65e6def5d880

After exploring a handful of the blog posts on your website, I honestly appreciate your technique of blogging. I saved it to my bookmark webpage list and will be checking back in the near future. Please visit my web site as well and let me know your opinion.

There’s definately a lot to find out about this subject. I like all of the points you have made.

When I initially left a comment I seem to have clicked the -Notify me when new comments are added- checkbox and now every time a comment is added I get 4 emails with the same comment. Is there an easy method you are able to remove me from that service? Many thanks.

This site truly has all of the information I needed concerning this subject and didn’t know who to ask.

Hi there! I simply wish to give you a big thumbs up for the excellent information you’ve got here on this post. I am coming back to your web site for more soon.

There is definately a lot to learn about this issue. I love all the points you’ve made.

You’ve made some decent points there. I looked on the net for more info about the issue and found most people will go along with your views on this site.

Having read this I thought it was really informative. I appreciate you spending some time and effort to put this article together. I once again find myself spending a lot of time both reading and commenting. But so what, it was still worth it!

I needed to thank you for this fantastic read!! I definitely enjoyed every bit of it. I have you book-marked to check out new stuff you post…

Good article! We are linking to this great post on our site. Keep up the great writing.

This is the right blog for anyone who wants to find out about this topic. You understand a whole lot its almost tough to argue with you (not that I really would want to…HaHa). You definitely put a new spin on a subject that’s been written about for ages. Great stuff, just excellent.

Hello! I just would like to give you a huge thumbs up for your excellent information you have got right here on this post. I am coming back to your web site for more soon.

Having read this I thought it was extremely informative. I appreciate you taking the time and effort to put this content together. I once again find myself spending a significant amount of time both reading and commenting. But so what, it was still worthwhile!

Hello! I could have sworn I’ve been to this website before but after looking at some of the posts I realized it’s new to me. Anyways, I’m certainly delighted I discovered it and I’ll be bookmarking it and checking back frequently!

Hi! I could have sworn I’ve visited this website before but after looking at many of the posts I realized it’s new to me. Nonetheless, I’m definitely delighted I came across it and I’ll be bookmarking it and checking back often.

This site really has all of the information I needed concerning this subject and didn’t know who to ask.

There’s definately a great deal to know about this issue. I really like all the points you made.

I’m very happy to uncover this web site. I want to to thank you for ones time for this wonderful read!! I definitely savored every little bit of it and i also have you saved to fav to check out new things in your site.

I couldn’t resist commenting. Exceptionally well written!

This is a really good tip particularly to those new to the blogosphere. Simple but very precise information… Appreciate your sharing this one. A must read post.

Survived by one son, Berdell Hose, Portland, OR; one daughter, Mrs Hazel Novotney, Wilbur, WA; Four grandchildren; 9 nice grandchildren.

Students interested in becoming dental hygienists must attend and graduate from an accredited dental hygiene school.

When I initially commented I seem to have clicked on the -Notify me when new comments are added- checkbox and from now on each time a comment is added I receive 4 emails with the exact same comment. There has to be a way you are able to remove me from that service? Cheers.

And there’s even better news in the event you or your partner are 50 years or older.

However, for those, who query about mastering trade commodities, they should know that it additionally could take a lifetime to commerce commodities.

This blog was… how do I say it? Relevant!! Finally I’ve found something which helped me. Kudos.

Going down under – Australia is known in sommelier circles for its surprising variety of Shiraz, Cabernet Sauvignon and Chardonnay wines, which are often overlooked by connoisseurs.

Franz Schubert wrote his first compositions as a court choirboy, and although he was thought of a musical genius, he was not a favourite of his teachers since he was more interested by writing music than in getting good grades for his schoolwork.

There’s certainly a lot to learn about this subject. I really like all of the points you made.

I’ve unhealthy information should you think that made Michigan look bad.

Coming back to the fact that we are witnessing a exceptional development proven in retailing by online purchasing in India, it will possibly simply be stated here that today it’s the best factor on the earth to buy style jewellery online.

Accepting one of these settlements may be advantageous, but it鈥檚 important to consider whether there may be unforeseen medical costs in the future.

This blue stone is associated with love & fidelity, making it a perfect gem to represent the bond that you two share.

Sure, Dolls Kill is understood for its edgy and trendy choice of other trend, making it a go-to destination for emo trend lovers.

Good article! We will be linking to this great post on our website. Keep up the good writing.

Because the system always tracks the vehicle’s location, directions are given flip-by-turn, by means of a speaker system, which permits the driver to maintain his or her eyes on the highway ahead and their thoughts focused on driving.

Good warrantees, a great deal of choices and state and federal economic incentives can tip the scales in the hybrids’ favor, but the introduction of less efficient hybrid versions of gasoline-guzzling full-sized trucks and SUVs has further blurred the image.

Not all manufacturers follow the exact same test procedures for all their cars, trucks and SUVs.

Emissions trading is also known as cap and trade.

Trapp then played in both legs of the UEFA Europa League semi-finals against Chelsea; although he saved one penalty from César Azpilicueta in the shootout, they misplaced 5-four as a result.

The space across the figures was often left white or in grisaille, or decorated with vegetal or floral designs.

Overpricing a property can make it languish unsold for months or even years, undermining any leverage you as a seller may have later in negotiating.

A fidelity bond generally covers a corporate policyholder from first party losses arising from the theft of money, securities or other tangible property so if the portal’s employees steal the funds belonging to the crowdfunding company, the bond can be useful.

Pretty! This has been an extremely wonderful article. Thank you for providing these details.

Weigel, David (November 24, 2008).

Bloomberg Information. Bloomberg, L.P.

Hospitality industry is carefully linked with journey and tourism industries.

Another important point of discussion is – what are the varied forms of investment.

If you cannot find simply the piece you need, do not overlook reproductions offered in conventional furniture shops.

The hotel was a very good 4-star resort and after the primary recreation all the other rounds have been held inside the resort so the gamers averted any travel earlier than the video games.

Whereas we pay a whole lot of attention to baby boomer issues associated to retirement, social security and elder care, had we been overlooking an underlying mental well being drawback?

Lawton, James (27 November 2001).

In this text, we will take a look at ways you possibly can invest, for example, 30K a year for 10 years or one of the best ways to take a position 40K as a one-off event, etc.

Resulting from submit World Warfare I austerity, the stones had been seen by many as frivolous purchases – cash down the drain.

This website was… how do you say it? Relevant!! Finally I’ve found something which helped me. Thanks!

You’ll be able to say goodbye to lengthy wait instances and cumbersome scheduling programs with same-day requests when attainable and fast inspection report turnarounds.

I like reading through a post that can make men and women think. Also, thank you for allowing me to comment.

One other group was despatched to protect supplies at Newtown, Pennsylvania, and to guard the sick and wounded who had to remain behind because the Continental Military started crossing the Delaware River.

However, when a country is suffering from high unemployment or wishes to pursue a policy of export-led growth, a lower exchange rate can be seen as advantageous.

I love reading through an article that will make men and women think. Also, thank you for permitting me to comment.

She was about to launch into an argument which might have made them both feel bitterly against one another, and to define sensations which had no such significance as phrases have been bound to give them when Hewet led her ideas in a different course.

This is a topic that is close to my heart… Best wishes! Where are your contact details though?

Using orange paint, paint a thick stripe over the middle one-third of the nail.

sex nhật hiếp dâm trẻ em ấu dâm buôn bán vũ khí ma túy bán súng sextoy chơi đĩ sex bạo lực sex học đường tội phạm tình dục chơi les đĩ đực người mẫu bán dâm

With Congress enacting six new tax laws in 2010, compared to only two in 2009, U.S.

There’s definately a great deal to learn about this subject. I really like all of the points you made.

Your style is really unique compared to other folks I have read stuff from. Many thanks for posting when you’ve got the opportunity, Guess I’ll just book mark this page.

Other investors may be non-voting.

It’s nearly impossible to find experienced people about this topic, however, you seem like you know what you’re talking about! Thanks

These firms even have internet webpage counterparts that can unfold the preferred teen hair styles from the large cities to the smaller ones.

I wanted to thank you for this excellent read!! I certainly loved every bit of it. I have you saved as a favorite to look at new stuff you post…

The solvent was animal fat or olive oil.

President of Farm Women’s group, county President of the Lebanon County Farm Girls.

Greetings! Very useful advice within this post! It’s the little changes which will make the biggest changes. Thanks for sharing!

International Journal of Consumer Studies.

If you’re attempting to add a complicated dependent (anybody who isn’t your child, mainly), you are going to run into a whole lot of strict necessities.

Having read this I thought it was rather informative. I appreciate you finding the time and energy to put this informative article together. I once again find myself personally spending way too much time both reading and commenting. But so what, it was still worthwhile!

The only factor worse than spending a weekend cleaning the house is spending a weekend stuck in your chimney.

For essentially the most half, I hear your complete melody and construction as I write, together with backing vocals, instrumentation, and so on.

Play along with your youngster and interact in positive interactions.

Grier, Peter. The Christian Science Monitor.

That in itself is not unhealthy – it’s necessary to advance the state of the art – however we have been unrealistic, blinded by promises of complete creative freedom, and by assurances that we would be left alone to make the sport of our goals.

In order of 2008, the tide of public opinion certainly shifted away from supply-facet thinking yet again.

And who is aware of?

You will need to also choose whether your order stays lively till the top of the day, till a particular date or until you cancel it.

Having read this I thought it was really enlightening. I appreciate you taking the time and effort to put this article together. I once again find myself personally spending a significant amount of time both reading and posting comments. But so what, it was still worthwhile!

You can comply with Tricia Gosingtian-Gabunada on her Instagram account here.

Synonymous with delicious street food, Borough Market providers visitors with a huge choice of dining options- from some of the best falafel in London to seafood.

Pretty! This was a really wonderful article. Many thanks for providing this information.

Garmhausen, Steve (November 3, 2021).

Oh my goodness! Amazing article dude! Thank you so much, However I am experiencing issues with your RSS. I don’t know the reason why I am unable to join it. Is there anybody getting identical RSS problems? Anybody who knows the answer will you kindly respond? Thanks!

I really like reading through an article that can make people think. Also, thank you for allowing me to comment.

Your style is very unique in comparison to other folks I’ve read stuff from. I appreciate you for posting when you’ve got the opportunity, Guess I will just book mark this site.

Hats: Broad-brimmed hats or top hats are iconic gothic accessories that may immediately elevate your fashion.

Looking for skilled help and working closely with healthcare providers is essential to finding the best suited treatment method.

The advance program will also be used to create a schedule of events to be handed out at the on-site convention registration.

Decorative paint treatments equivalent to dragging or sponging are comparatively simple and will also disguise wall imperfections.

Heyworth, M. (1992) “Evidence for early medieval glass-working in north-western Europe” pp.

Consider hiring a balloon artist, caricaturist, clown or magician to entertain kids in a designated corner of your reception room.

Fill out every part you may on each profile to better optimize it.

Then, when millennials came along, they began flocking back to America’s newly redeveloped inner cities.

I would like to thank you for the efforts you have put in penning this site. I’m hoping to see the same high-grade content from you later on as well. In fact, your creative writing abilities has motivated me to get my very own website now 😉

I really like it whenever people get together and share ideas. Great blog, stick with it.

I’d like to thank you for the efforts you have put in penning this site. I really hope to see the same high-grade content from you in the future as well. In fact, your creative writing abilities has encouraged me to get my own, personal blog now 😉

Great article! I learned a lot from your detailed explanation. Looking forward to more informative content like this!

Hello there! This post couldn’t be written any better! Looking at this post reminds me of my previous roommate! He always kept preaching about this. I’ll forward this post to him. Pretty sure he’ll have a very good read. Thanks for sharing!

This is a good tip especially to those new to the blogosphere. Simple but very accurate info… Thank you for sharing this one. A must read post!

Great post. I will be experiencing some of these issues as well..

The very next time I read a blog, I hope that it won’t fail me just as much as this particular one. After all, I know it was my choice to read, nonetheless I really thought you would probably have something interesting to say. All I hear is a bunch of crying about something you could possibly fix if you were not too busy looking for attention.

Tennessee has a excessive gross sales tax in massive part because revenue isn’t taxed is the state.

Way cool! Some extremely valid points! I appreciate you penning this write-up and the rest of the site is also very good.

OMT insurance policies. That paper discovered that such insurance policies “decreased the Italian and Spanish two-yr authorities bond yields by about two share factors, while leaving unchanged the bond yields of the identical maturity in Germany and France”.

Whereas “The Classroom of the longer term” sounds like it might include a dazzling show of technology, I’m extra involved with the teachers of today who do not make what they deserve but still have to buy provides out of pocket and college students who’re left with antiquated textbooks and rundown colleges.

Three candles make up the design consisting of a tall white candlestick, a small-bodied candle, and a red candle.

Mergers and acquisitions in the well being care trade have all the time turned out to be very profitable.

More than seventy five sellers from 30 completely different states & a number of nations.

Satullo, Sara K (July 3, 2020).

The unhealthy news is the varicella virus remains in your sensory nerve cells and could make a shock visit in the form of shingles later in life.

I blog often and I genuinely appreciate your content. This article has really peaked my interest. I will book mark your blog and keep checking for new details about once a week. I subscribed to your RSS feed as well.

Stocks had led the way for the previous yr and look prepared for one more assault on the S&P 1150 then the original breakout of 1300 from August 2008.

She married Claus A. Nelson in 1911.

The East Asian model of capitalism involves a strong role for state investment and in some instances involves state-owned enterprises.

Route 27 (US 27) begins at an interchange with I-24 in downtown Chattanooga, and ends in northern Hamilton County, connecting the city with the cities of Purple Bank, Soddy Daisy, Dayton, and Dunlap to the north.

Saved as a favorite, I like your website!

Whether you’re decorating a master bedroom, a child’s room, a teenager’s room, or a guest bedroom, follow this expert decorating advice to create the mood you desire.

Developing your fundamental analysis skills will stand you in good stead in both the investment and business world.

More and more, retirees will have to rely on their savings to cover the costs of living health insurance.

In Darth Maul: Saboteur, the Sith Lord Darth Sidious sends Darth Maul to destroy InterGalactic Ore and Lommite Restricted.

To get inspiration on investing, I asked the neighborhood at Terkel for the best methods they’d make investments $40,000 in 2023.

This is a topic which is near to my heart… Thank you! Exactly where are your contact details though?

Entire systems for performance, attribution, allocation and risk analysis are combined in a single hosted, cloud based solution, delivering everything needed for effective investment analysis in one central hub.

Throughout this time, Anakin Skywalker is a full-fledged Jedi Knight and the collection exhibits how he progresses into his fall to the Dark Aspect of the Pressure.

Fortuitously, glass drill bits are extensively available and relatively reasonably priced.

Oh my goodness! Incredible article dude! Thank you, However I am encountering problems with your RSS. I don’t know the reason why I cannot join it. Is there anybody else having identical RSS problems? Anyone that knows the answer will you kindly respond? Thanx.

She is president of Winning Methods Advertising and marketing, an editorial and marketing consulting agency that makes a speciality of home design and decorating.

Cease loss orders will mechanically execute when the value specified is hit, and can take the emotion out of a buy or promote decision by setting a cap on the amount you might be keen to lose in a trade that has gone in opposition to you.

Sons of Abraham 18 November 2013 2.Zero Sons of Abraham offers further depth to the three Abrahamic faiths: Christianity specifically, but also added some content material for Muslims and the Jewish religion.

Some provide early receipt – after 2 days of the deposit being made by the participant, the platform already releases the money for the organizer to start investing.

Watch our most viewed super sexy bf video on socksnews.in. sexy bf video Watch now.

Very useful content! I found your tips practical and easy to apply. Thanks for sharing such valuable knowledge!

The very next time I read a blog, Hopefully it does not disappoint me as much as this particular one. After all, Yes, it was my choice to read, however I truly thought you would probably have something useful to talk about. All I hear is a bunch of moaning about something you could possibly fix if you weren’t too busy seeking attention.

I have to thank you for the efforts you’ve put in writing this site. I am hoping to check out the same high-grade blog posts by you in the future as well. In truth, your creative writing abilities has inspired me to get my own website now 😉

After looking over a number of the articles on your blog, I truly appreciate your way of writing a blog. I saved it to my bookmark site list and will be checking back in the near future. Please check out my web site too and let me know your opinion.

Thanks for sharing. Like your post.Name

A motivating discussion is definitely worth comment. I believe that you need to publish more about this subject, it might not be a taboo matter but usually people do not discuss such issues. To the next! All the best!

Great article! I learned a lot from your detailed explanation. Looking forward to more informative content like this!

You’re so awesome! I don’t think I have read a single thing like this before. So nice to discover somebody with original thoughts on this topic. Really.. many thanks for starting this up. This web site is something that’s needed on the web, someone with a bit of originality.

This was a great read! Your insights are truly helpful and make complex topics easy to understand. Looking forward to more!

When I initially left a comment I seem to have clicked the -Notify me when new comments are added- checkbox and from now on each time a comment is added I receive 4 emails with the same comment. There has to be a means you can remove me from that service? Thanks.

Way cool! Some very valid points! I appreciate you penning this post plus the rest of the website is very good.

A fascinating discussion is worth comment. There’s no doubt that that you need to write more about this subject matter, it may not be a taboo matter but generally people don’t talk about these issues. To the next! Many thanks.

Aw, this was a really good post. Taking the time and actual effort to produce a great article… but what can I say… I hesitate a whole lot and don’t manage to get nearly anything done.

https://www.jobscoop.org/employers/3468278-balkan-tours

sex nhật hiếp dâm trẻ em ấu dâm buôn bán vũ khí ma túy bán súng sextoy chơi đĩ sex bạo lực sex học đường tội phạm tình dục chơi les đĩ đực người mẫu bán dâm

Greetings, I do believe your website could be having web browser compatibility problems. When I take a look at your web site in Safari, it looks fine however, when opening in Internet Explorer, it’s got some overlapping issues. I just wanted to give you a quick heads up! Besides that, fantastic website!

You’ll be able to trade multiple currencies after you’ve got a stable understanding of the markets earlier than moving into new currency pairs.

Nice read!

Your style is really unique in comparison to other folks I have read stuff from. Thank you for posting when you’ve got the opportunity, Guess I will just book mark this blog.

This is a topic that’s near to my heart… Best wishes! Where are your contact details though?

Right here is the right web site for anyone who would like to understand this topic. You understand so much its almost hard to argue with you (not that I actually will need to…HaHa). You definitely put a fresh spin on a subject which has been discussed for decades. Wonderful stuff, just excellent.

This was a great read! Your insights are truly helpful and make complex topics easy to understand. Looking forward to more!

I really enjoyed reading this! Your writing style is engaging, and the content is valuable. Excited to see more from you!

I like it when individuals come together and share opinions. Great website, continue the good work!

After looking over a handful of the articles on your web page, I honestly like your technique of writing a blog. I book marked it to my bookmark website list and will be checking back in the near future. Please check out my web site too and let me know how you feel.

Forex traders need stable, safe, and fast platforms to conduct their business, and solutions like Windows VPS can help.

Good post. I’m experiencing some of these issues as well..

Step 1: Insert the auger into the bathroom trap and turn the crank till it feels tight.

Greetings! Very useful advice within this post! It’s the little changes that produce the greatest changes. Thanks for sharing!

Hi, I do believe this is an excellent site. I stumbledupon it 😉 I may revisit yet again since i have bookmarked it. Money and freedom is the best way to change, may you be rich and continue to help others.

sex nhật hiếp dâm trẻ em ấu dâm buôn bán vũ khí ma túy bán súng sextoy chơi đĩ sex bạo lực sex học đường tội phạm tình dục chơi les đĩ đực người mẫu bán dâm

I really like looking through a post that will make men and women think. Also, many thanks for allowing me to comment.

Perhaps a very powerful data you’ll want to assert Social Safety is your age.

Spot on with this write-up, I really believe this amazing site needs much more attention. I’ll probably be back again to read more, thanks for the advice!

They don’t seem to be in need of constructing $5k in the present day to settle on home instalments and the like with the goal they are not below that same day strain that giant parts of retail traders are under.

The presence of inclusions, which are widespread in amethyst, also can impact the stone’s value.

We notice you’re looking from a special location.

Only a handful of attorneys in Florida have two certifications.

F*ckin’ remarkable things here. I’m very glad to see your post. Thanks so much and i am taking a look ahead to touch you. Will you please drop me a mail?

The Gustav Line was a collection of concrete bunkers and artillery positions on the rocky faces of mountains fronted by a no-man’s-land of barbed wire and land mines.

Pretty! This has been an extremely wonderful post. Thanks for supplying this info.

I truly love your site.. Pleasant colors & theme. Did you create this web site yourself? Please reply back as I’m hoping to create my own site and would like to find out where you got this from or just what the theme is named. Appreciate it!

Multicast Wireless is a mission-based, cutting edge, progressive multimedia organization located in Huntsville, Alabama.

Typical for polar expeditions in this age, emotions of nationwide and regional pride surrounded the homecoming celebrations.

Some tasks, equivalent to mailing invitations and selecting up the rings, obviously can’t be checked off until two months before the massive Day.

Satisfy your wanderlust on every a type of 365 days by embarking on a career that could have you really going places — and not simply up the company ladder.

Particular person traders have a couple of choices for investing in non-public fairness, however one relatively protected option is to work with a private equity agency to affix a pool of investors.

Proponents of this time period argue that the Structure implies that the Senate can act by a majority vote unless the Structure itself requires a supermajority, because it does for certain measures such as the ratification of treaties.

In 1997, legendary NFL coach Mike Ditka got here out of retirement to revive the beleaguered New Orleans Saints.

The foreign exchange financial instruments are transactions or contracts conducted in the spot, forward, swap, futures and options foreign exchange markets.

When I initially commented I seem to have clicked on the -Notify me when new comments are added- checkbox and now whenever a comment is added I get four emails with the exact same comment. Perhaps there is a way you can remove me from that service? Many thanks.

I really like it when people get together and share thoughts. Great site, stick with it!

When I initially commented I appear to have clicked the -Notify me when new comments are added- checkbox and from now on whenever a comment is added I get 4 emails with the exact same comment. Perhaps there is a way you are able to remove me from that service? Many thanks.

A motivating discussion is definitely worth comment. There’s no doubt that that you should publish more on this subject, it may not be a taboo matter but typically people do not talk about such issues. To the next! Cheers.

This allowed much higher realism and detail, and moved stained glass art even nearer to painting.

When designing the ultimate version of the nice Seal, Thomson (a former Latin trainer) kept the pyramid and eye for the reverse facet however replaced the two mottos, utilizing Annuit Cœptis as a substitute of Deo Favente (and Novus ordo seclorum as an alternative of Perennis).

Can You Really Make Money Online With Market Research?

As we have seen however, Mr.

However overall, stock selecting is a bit riskier than diversifying your money with an index fund.

Other than hiking or trekking, people might approach Trekking and tour company in Nepal to get plenty of other adventurous experiences.

There’s certainly a great deal to find out about this issue. I like all of the points you made.

Your style is unique in comparison to other folks I have read stuff from. I appreciate you for posting when you have the opportunity, Guess I’ll just book mark this web site.

Suppose past cost: When it comes of shopping for gifts for child, you should not be worrying much about the price.

You can comply with Niana Guerrero on her Instagram account here.

You’re so awesome! I do not suppose I’ve truly read anything like this before. So wonderful to discover someone with unique thoughts on this subject matter. Really.. thanks for starting this up. This web site is something that is needed on the internet, someone with a little originality.

Very good post. I certainly appreciate this site. Keep it up!

I admire the time and effort you put into your blog. I wish I had the same drive.

These sororities cater to a selected cultural interest – a sorority for Asian-American women or Latina women, for example.

Without a robust federal government, the interior of North America and the western coast could be separate nations right now.

However, controversy still exists regarding its use and effectiveness.