Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

If you haven’t already, check out Episode 7 of the Prometheus Podcast! For this episode, we have another fantastic guest for you-Andy Constan. Andy is the Founder & CIO of Damped Spring Advisors, a macroeconomic research firm specializing in Hedge Fund consulting. Andy brings a great deal of experience to the table, having worked at some of the biggest macroeconomic hedge funds- including Bridgewater & Brevan Howard. Andy has also generated some serious alpha this year, using his flow-based approach to time key inflections in asset markets so this episode is must-listen if you’re trying to navigate today’s volatile markets.

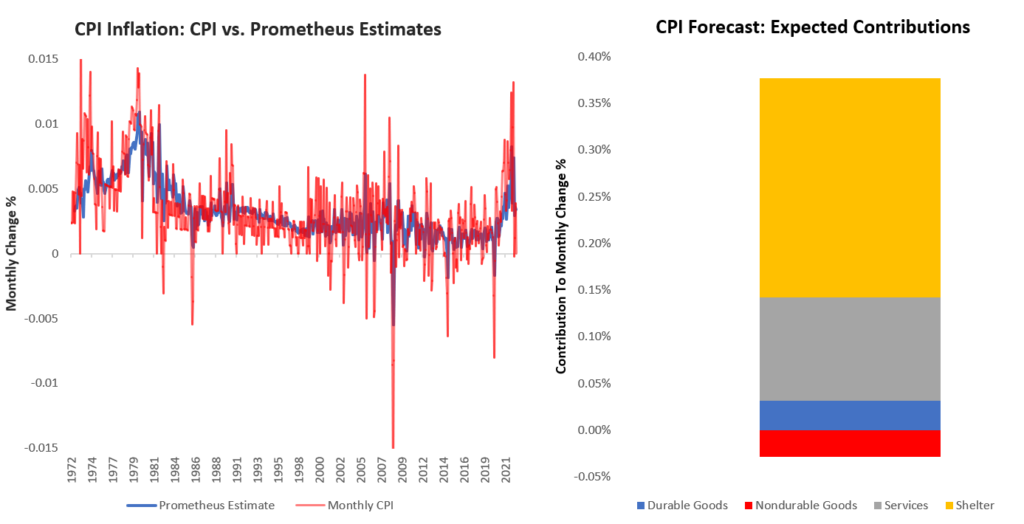

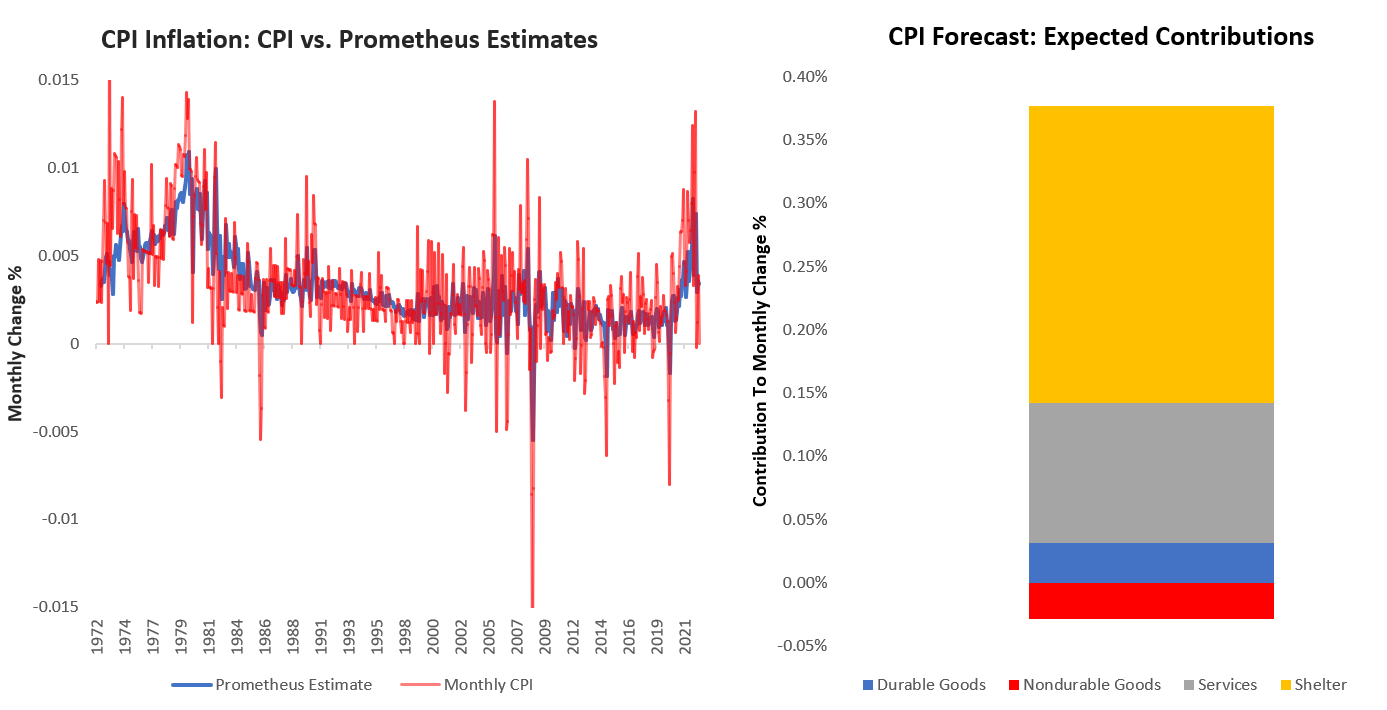

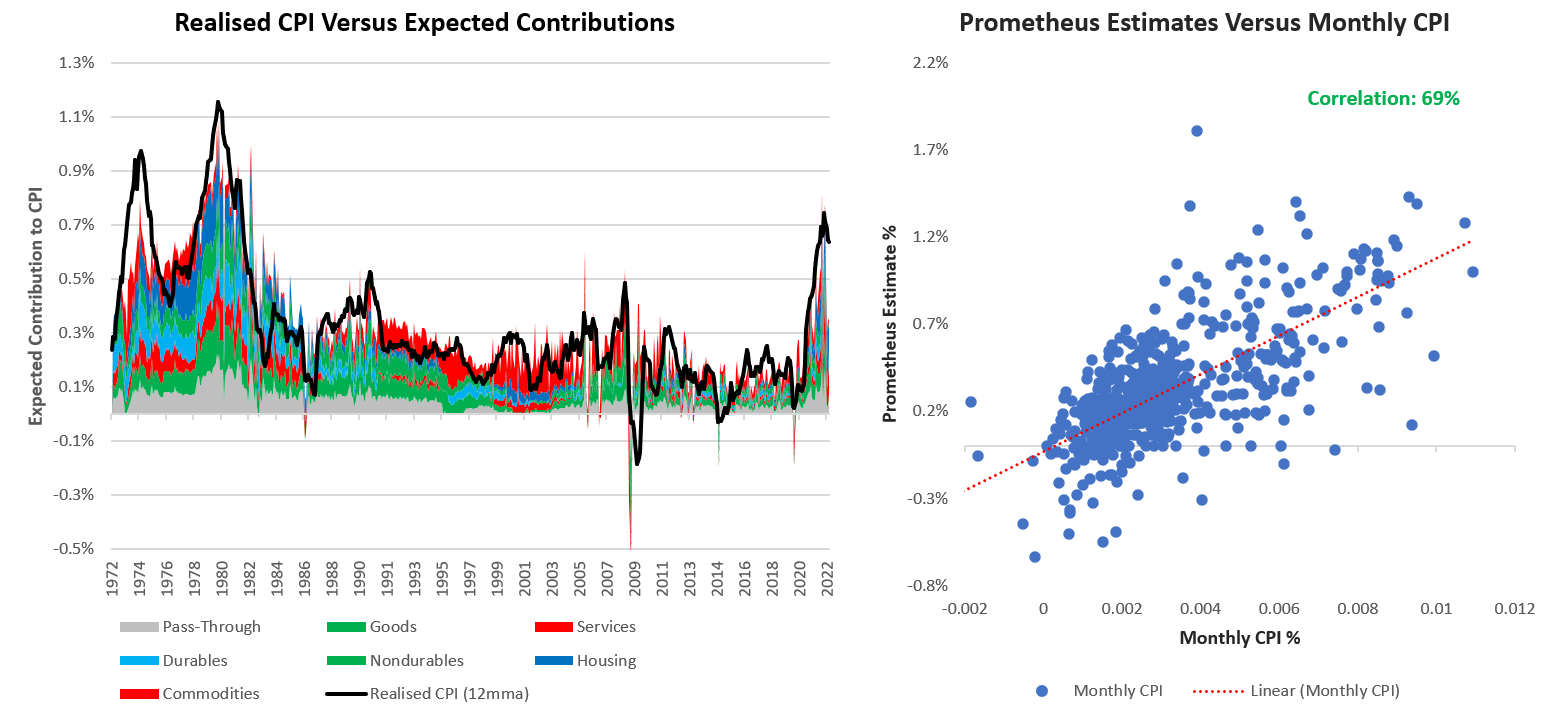

We will keep it brief our systems expect a disappointment in consensus expectations of CPI tomorrow. Our systems expect a CPI print of 0.36% versus consensus expectations of 0.6%. The primary driver of this move is the potential for a decrease in non-durable goods inflation alongside a strong housing contribution. The balance of these two will determine the outcome of the print:

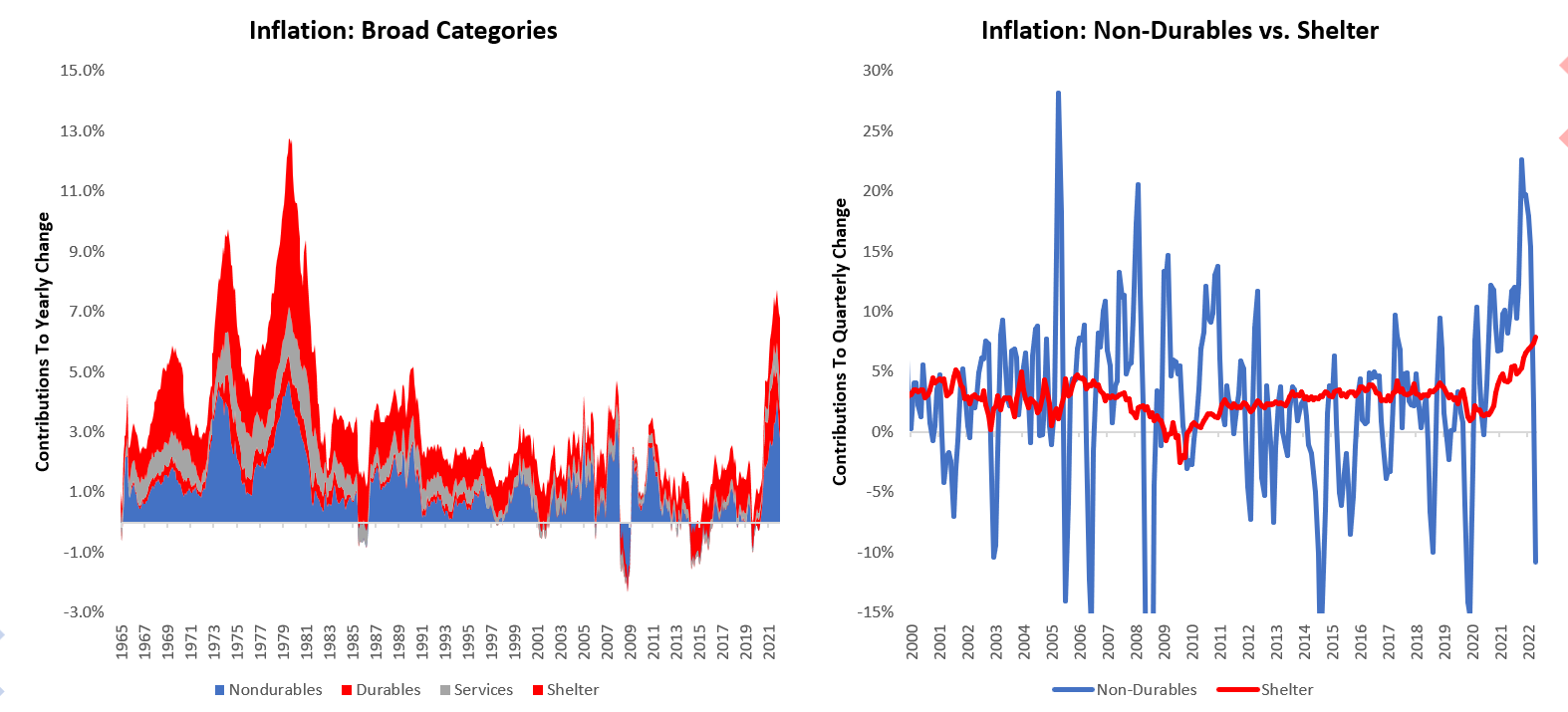

As we have said previously said, the balance between goods disinflation & services inflation will determine the pace & path of inflation. Particularly, this print will likely be driven by the balance between Non-Durable Goods (non-core items) & Housing:

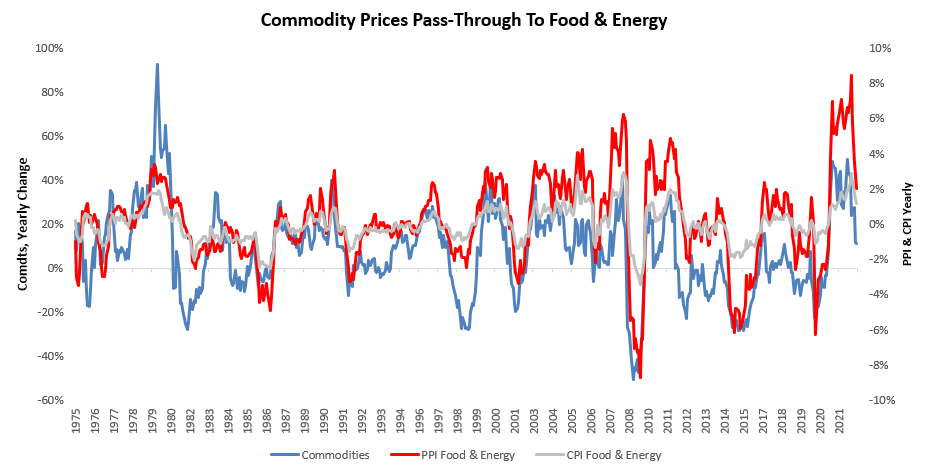

Our expectation is that the pass-through from commodities into PPI & CPI will result in weaker-than-expected nondurable goods inflation:

Our systems have been good guides for inflation to come, & while this projection is fairly out-of-consensus, we find there is a significant chance of disappointment. This finding is bolstered by the historical accuracy of the our estimates:

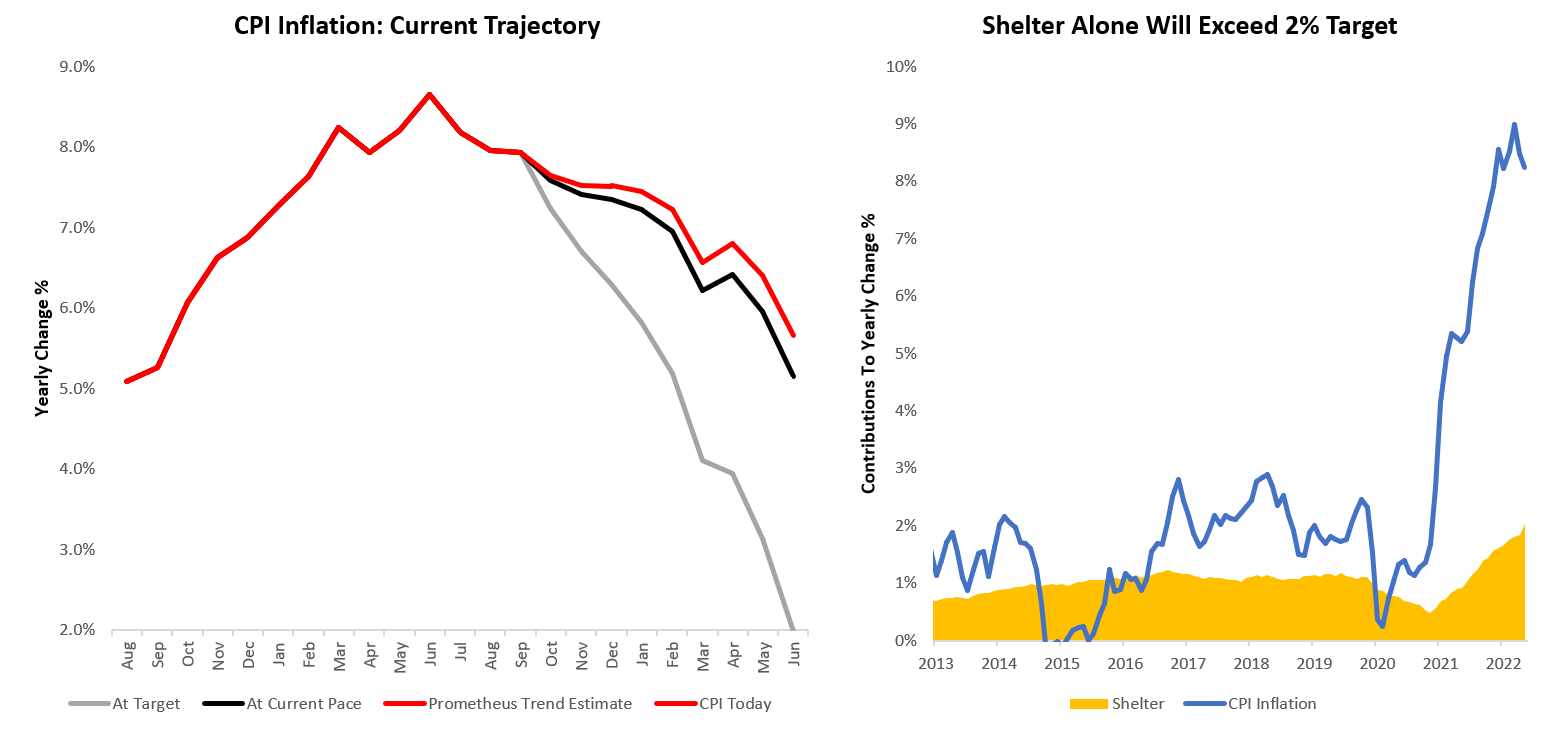

Taking a step back, while we think there is indeed a significant chance of a CPI miss tomorrow, this is simply a function of idiosyncratic dynamics. On a cyclical basis, we continue to expect strong and persistent inflationary pressures. We show this below:

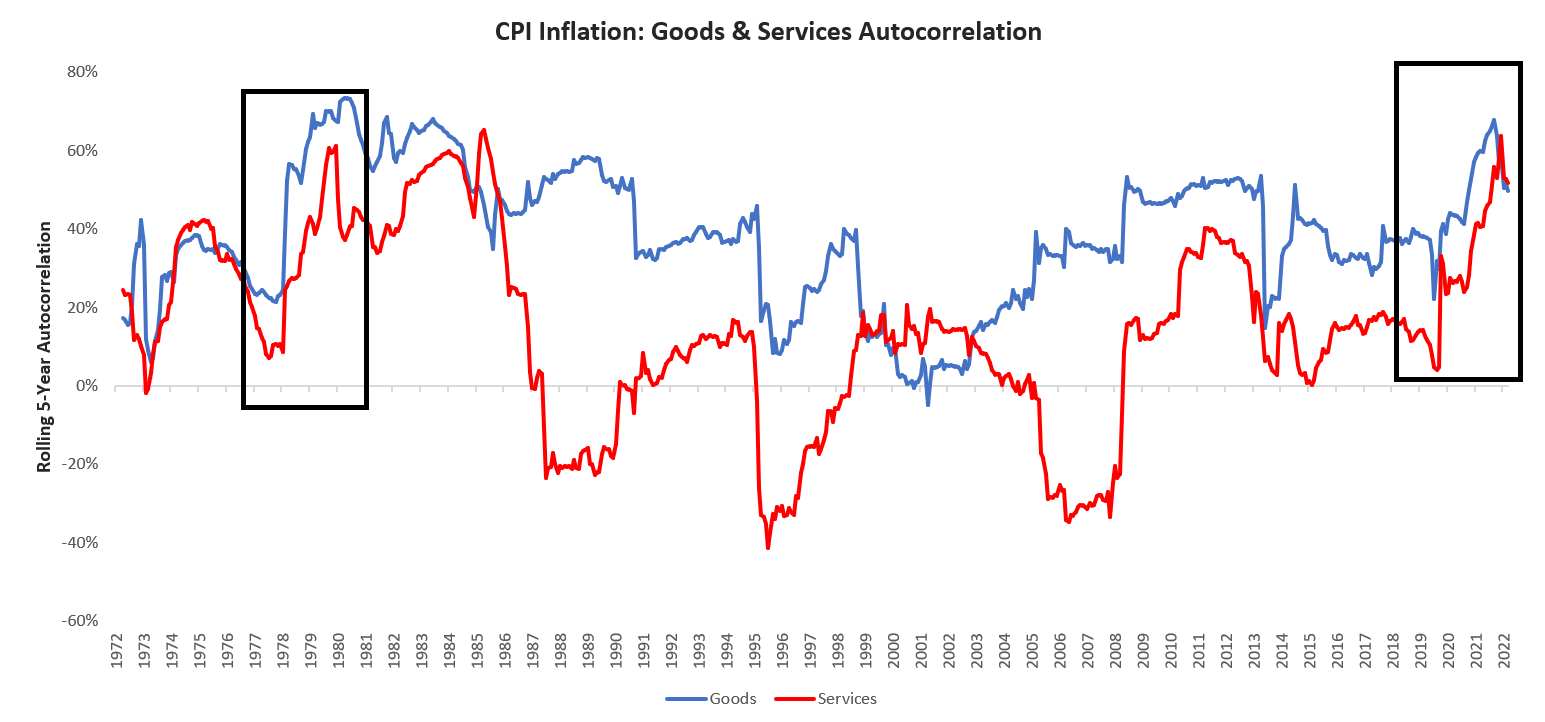

Particularly, we think it is important to note (as shown above) that shelter alone will contribute to inflation in excess of the 2% Fed target not to mention other persistent inflation pressures. We show these pressures in the form of autocorrelations below:

Inflationary pressures are entrenched but that doesn’t mean every print will be higher than the previous one. Stay nimble.

A harmonious blend of local care and global expertise.

order lisinopril price

Every pharmacist here is a true professional.

The staff provides excellent advice on over-the-counter choices.

cost cheap clomid pills

I’m grateful for their around-the-clock service.

Their international partnerships enhance patient care.

can you buy cheap lisinopril without a prescription

Delivering worldwide standards with every prescription.

Their international health campaigns are revolutionary.

can i buy cheap lisinopril pills

Love their range of over-the-counter products.

All trends of medicament.

cost of clomid without a prescription

They make international medication sourcing a breeze.

Thanks for the ideas you write about through this web site. In addition, quite a few young women that become pregnant do not even make an effort to get health insurance because they are full of fearfulness they might not qualify. Although some states at this point require that insurers provide coverage no matter the pre-existing conditions. Prices on these guaranteed options are usually bigger, but when considering the high cost of medical care it may be a safer strategy to use to protect one’s financial future.

I have taken notice that in unwanted cameras, specialized sensors help to {focus|concentrate|maintain focus|target|a**** automatically. Those sensors regarding some cams change in in the area of contrast, while others make use of a beam of infra-red (IR) light, specially in low lighting. Higher specs cameras often use a mix of both models and likely have Face Priority AF where the photographic camera can ‘See’ some sort of face as you concentrate only in that. Thank you for sharing your ideas on this website.

Thank you for the auspicious writeup. It in fact was a amusement account it. Look advanced to far added agreeable from you! However, how could we communicate?

I used to be suggested this blog by my cousin. I am not certain whether or not this put up is written by way of him as no one else recognize such particular approximately my trouble. You are wonderful! Thank you!

great post, very informative. I wonder why the other specialists of this sector don’t notice this. You should continue your writing. I am sure, you’ve a great readers’ base already!

Wow that was odd. I just wrote an incredibly long comment but after I clicked submit my comment didn’t appear. Grrrr… well I’m not writing all that over again. Anyhow, just wanted to say great blog!

I do agree with all of the concepts you have offered in your post. They are really convincing and can definitely work. Nonetheless, the posts are very quick for newbies. May just you please lengthen them a bit from subsequent time? Thank you for the post.