Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios. We also just released our latest Month In Macro note, which over 45 pages, explains our current assessment of economic and market conditions.

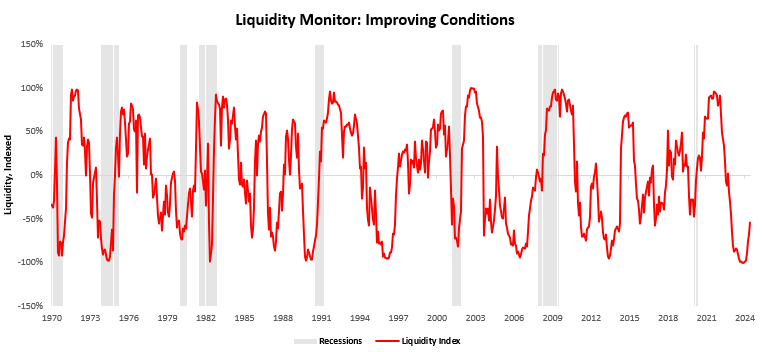

Today, we examine the incremental changes in the liquidity ecosystem. Over the last few months, we have seen a significant improvement in the liquidity environment, largely coming from the Federal Reserve controlling its liquidity drain through indirect measures. There are two dimensions two liquidity: private-sector liquidity and public-sector liquidity. The Fed’s slowing of its liquidity drain has stabilized public sector liquidity. On the other hand, sustained nominal income has continued to flow through to private sector liquidity. The combination of these dynamics has been a support to liquidity conditions. We show one of our proprietary liquidity measures that capture these dynamics:

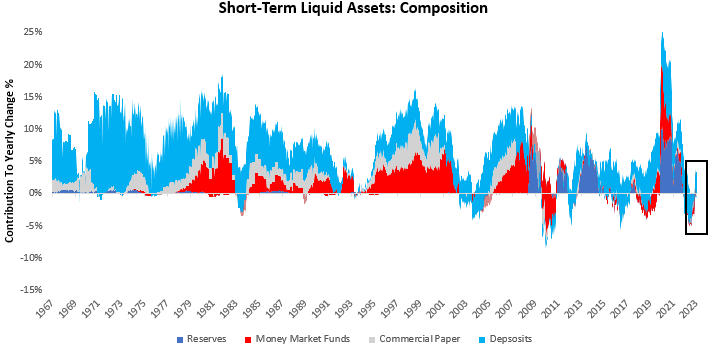

As we can see above, liquidity conditions have begun to inflect upwards. In this note, we discuss some of the components of the liquidity ecosystem driving these moves. Particularly, we focus on short-term liquid assets, which span the universe of reserves, money market funds, commercial paper, and deposits. We show our aggregate tracking of these measures below:

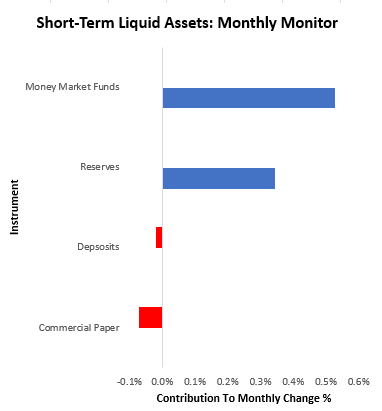

As we highlight in the box above, our short-term liquid asset aggregates have sequentially improved. Zooming into the most recent month, these most recent increases in liquidity have come from a significant improvement in money market funds and increases in reserve balances at the Federal Reserve. We show these below:

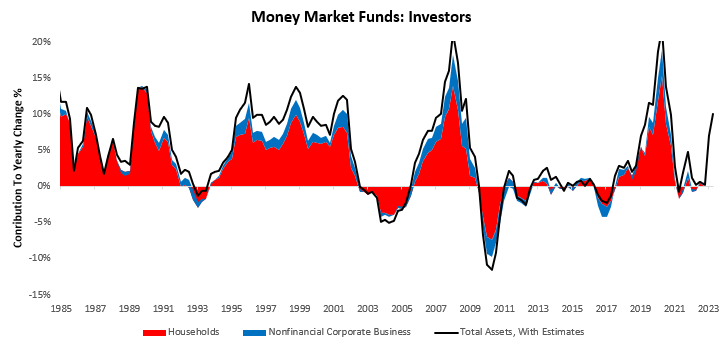

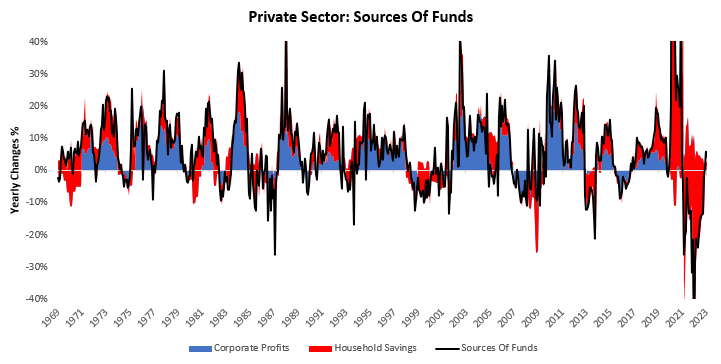

As we have detailed in the past, households and corporates are the primary contributors to the money market fund ecosystem. We visualize this below:

Therefore, as businesses and households accumulate cash balances, a significant portion of these cash balances can flow to money market funds and other parts of the liquidity ecosystem. Over the last year, corporate profits have begun to drag on liquidity supply; however, households’ savings have more than made up for the shortfall as a source of funds:

As we can see above, the reversal from contracting savings to expanding savings has been a support to the inflows to money markets. Looking ahead, to see these dynamics continue, we will need to see sustained nominal income expansion. We think this will increasingly be a headwind for liquidity as we progress through the economic slowdown.

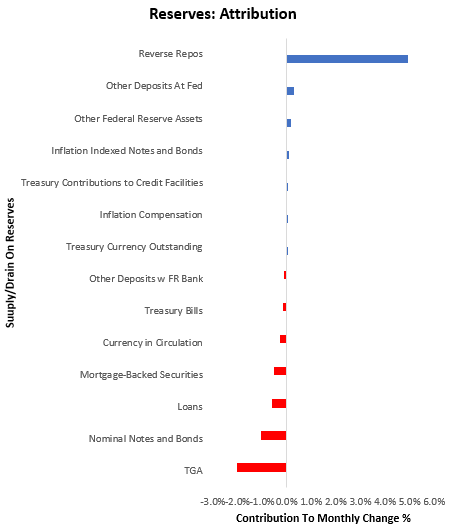

Contemporaneously, despite ongoing Quantitative Tightening, we have also seen a significant improvement in reserve balances held at the Federal Reserve. We show the attribution of these changes in reserve balances below:

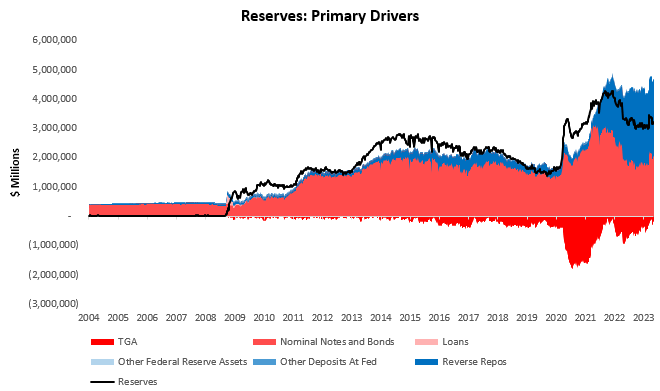

While the TGA increase has begun to drag on liquidity conditions, it has also been offset by a decrease in reverse repo usage. The combination of these drivers has created more ample reserves in the banking system over the last month. Below, we zoom out to offer the broader context of the factors draining and contributing to reserves:

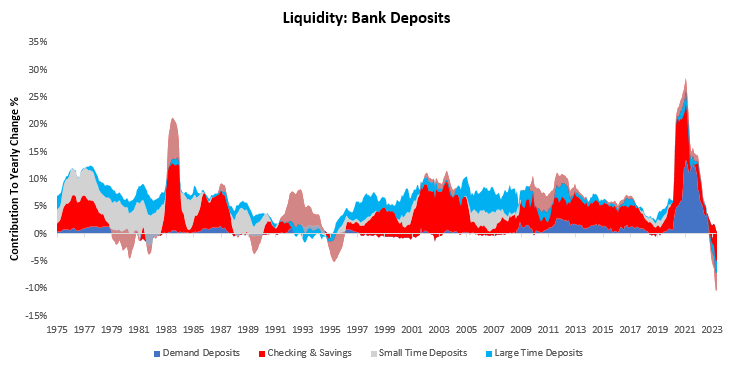

This increase in reserve balances has not facilitated a broader growth in credit creation and deposit expansion by banks. Below we show how deposits continue to contract:

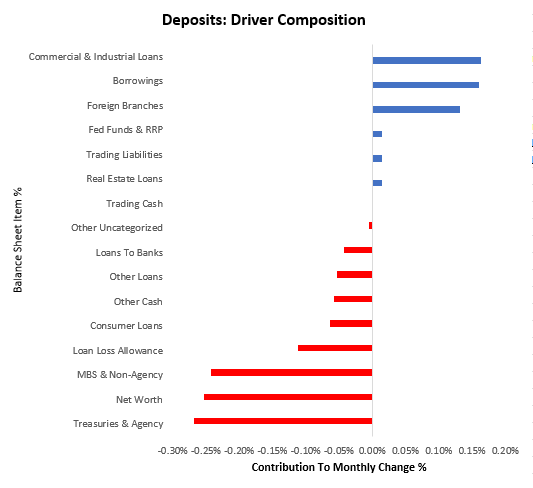

For further granularity, we decompose the most recent changes in bank deposits into their balance sheet drivers:

As we can see above, declines in bank bet-worth, financial assets, and consumer loans have contributed to the contraction in deposits. We think it is essential to note that some degree of this deposit decline is due to migration from bank deposits to higher interest-bearing money market funds.

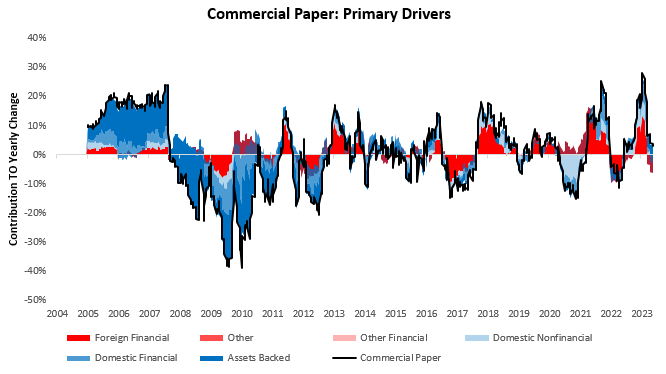

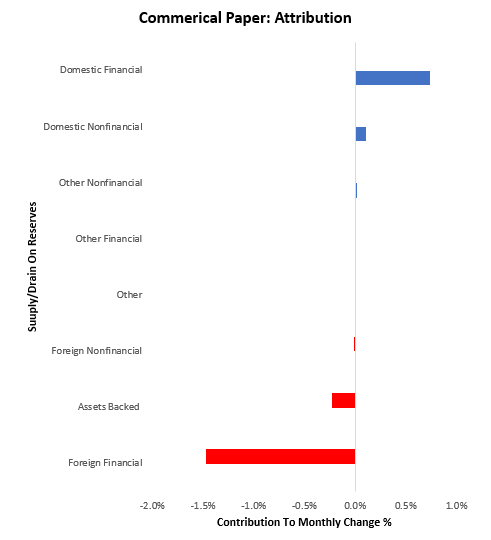

Finally, commercial paper issuance continues to soften, indicating weak corporate conditions. We show this below:

The most recent declines in issuance have come from a pullback in asset-backed and foreign financial commercial paper issuance. We show this below:

As we can see, commercial paper conditions as now distinctly different from those seen last year. Corporate conditions remain weak.

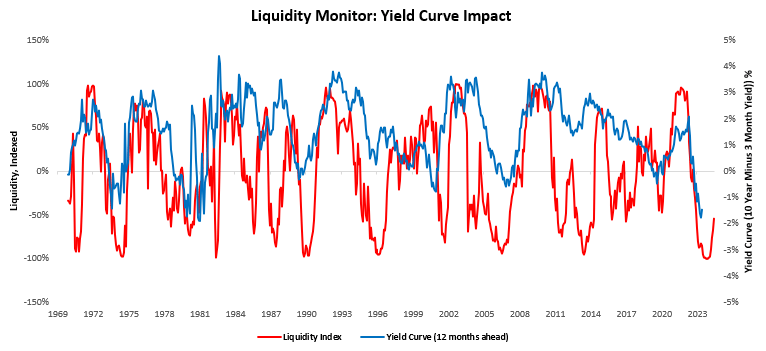

Overall, these liquidity conditions are consistent with the broader economic themes—i.e., strong consumer conditions, weak corporate conditions, and a more favorable government impulse. Putting these dynamics together, there remains potential for steeper yield curves as private liquidity remains elevated and inflation remains resilient:

Until next time.