Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

Here are our top three observations today:

-

Monetary likely needs to be tighter if the Fed wants to tame inflation.

-

PMI data reinforces that we are seeing a slowing in business activity.

-

Tightening liquidity is showing its impacts in markets, and there is more to come.

The combination of these factors makes it relatively hard to add long exposure to any asset. As a result, our systems have generally maintained positions shorting assets. We discuss the above points below:

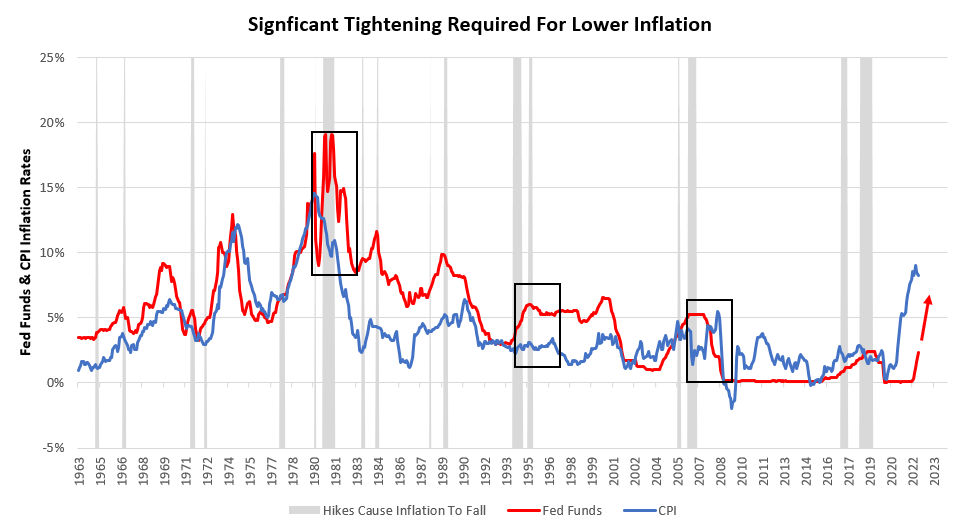

i. Monetary policy likely needs to be tighter if the Fed wants to tame inflation. Markets have recently moved to price the tightening of liquidity conditions, both coming from quantitative tightening from rising interest rates. While quantitative tightening strongly influences asset markets, it is less useful in impacting inflation. The Fed’s primary tool for fighting inflation is raising interest rates. Raising interest rates increasing the cost of borrowing across the economy, dampening credit creation and borrowing- thereby bringing down nominal activity. However, this mechanism can take a while to show its full effect, as debt often carries fixed interest rates, and the impact of higher rates slowly makes its way into new financing and cost structures. Nonetheless, this tool is by no means ineffective, and 74% of disinflationary periods since 1962 have been preceded by hiking cycles. Below, we show periods where interest rate hikes have facilitated lower inflation:

The above visual shows CPI inflation alongside the Federal Funds rates. Additionally, we highlight periods where hiking cycles (persistent increases in Fed Funds) result in falling inflation over the next twelve months. We then highlight three periods that we think are appropriately illustrative of the pressures at play, i.e., that interest rates need to be significantly higher relative to inflation to catalyze lower future inflation. Historically, interest rates have needed to be about 2% above CPI to catalyze decelerating CPI. This gap could be created via higher rates or lower inflation. We find it is typically much more of the priori.e., interest rates need to rise to match an elevated level of inflation if they are to catalyze lower future inflation.

Our current estimates of CPI trend of 6.5%, alongside Fed Funds at 3.25% and Nominal GDP growth of 9%, suggest that the gap between inflation and policy rate remains too large. While this gap will likely be closed by some inflation deceleration, we think there is a strong likelihood that interest rates will have to make up a significant amount as well. While this potential is priced to some extent in Fed Funds futures markets, there remains room for further repricing contingent on the inflation picture. This dynamic will be particularly important to Treasury bond investors, who will require the safety of no further hikes to be enticed into buying Treasuries across the spectrum. For the time being, the risks remain skewed to the downside for these investors, creating a challenging environment ahead.

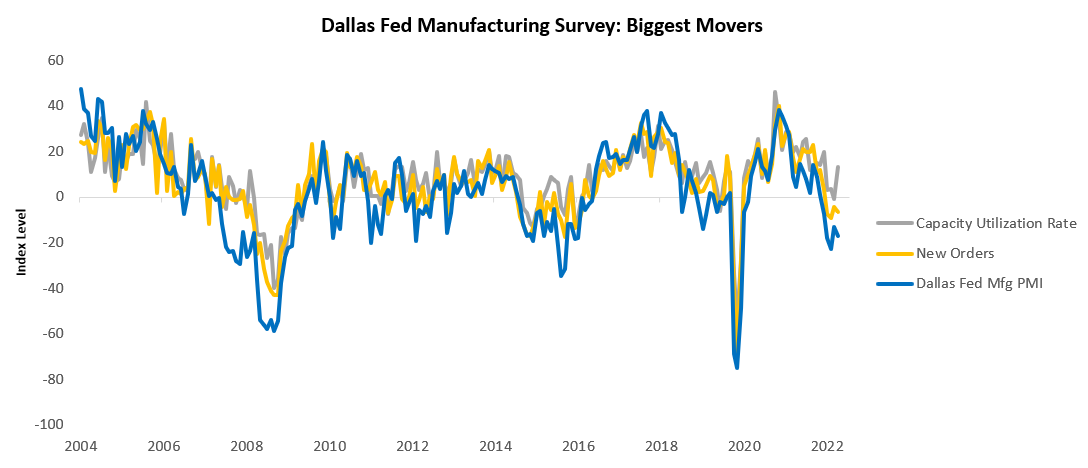

ii. PMI data reinforces that we are seeing a slowing in business activity. The latest Dallas Fed Manufacturing PMI data showed a contractionary reading of -17.2, disappointing consensus expectations of -9. We show this below:

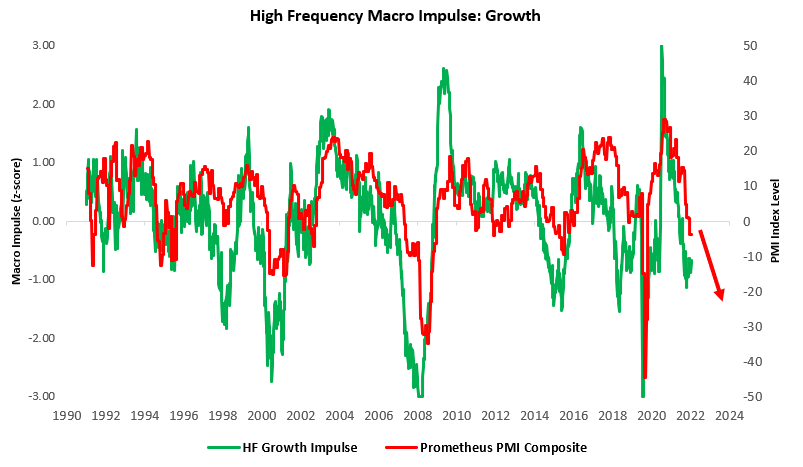

This reading was a sequential deceleration within a decelerating trend. The largest gaining segment was Capacity Utilization Rate, and the most significant slowdown was in New Orders. Our proprietary high-frequency growth gauges have led these moves:

Our systems expect more downside in economic activity ahead, creating significant headwinds for equities & credit.

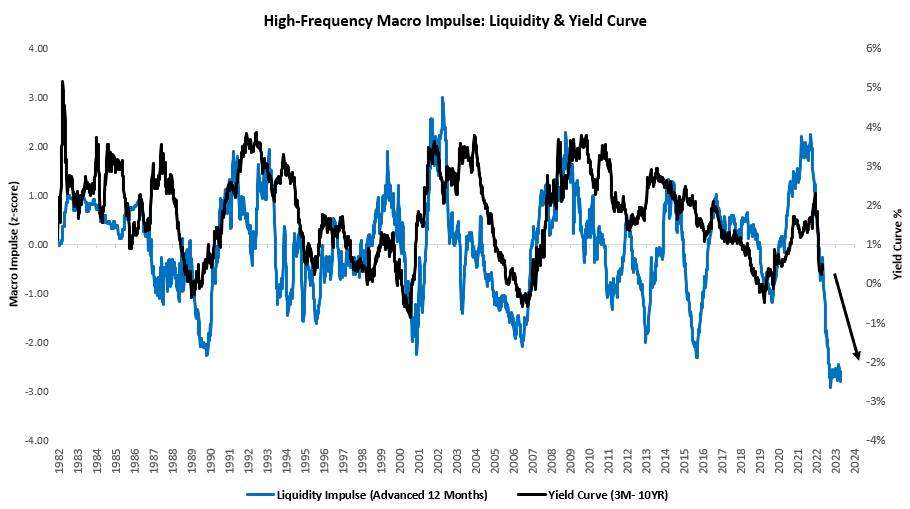

iii. Tightening liquidity is showing its impacts in markets, and there is more to come. The Federal Reserve is now at the full pace of its quantitive tightening program which we explained in depth here:

As explained in this previous note, the path for Quantitative Tightening is aggressive, sucking liquidity out of financial markets at a rapid pace, creating an extremely difficult set of conditions for all assets. Our proprietary gauges of liquidity inflected late last year, suggesting that this year would be a difficult one for markets. These same gauges have shown no relief in liquidity conditions and continue to indicate that the yield curve will invert, i.e., market conditions are likely to worsen:

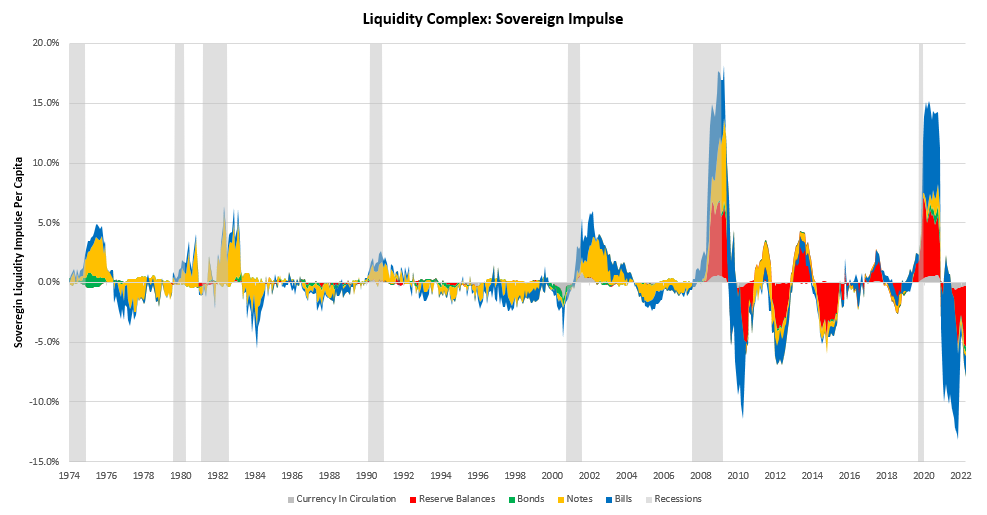

At the heart of this liquidity-drain is quantitative tightening, which is moving to significantly contract its reserve balances. As we can see below, reserve balances are the primary driver of the reduction in the growth of government liabilities (private sector assets).

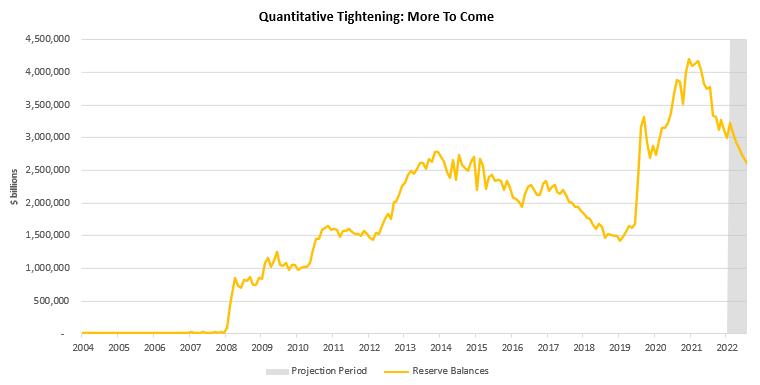

Quantitative tightening is likely to continue on its current pace, and the Treasury will continue to maintain roughly the same level of cash, i.e., reserves will continue to decline. We show our updated projections below:

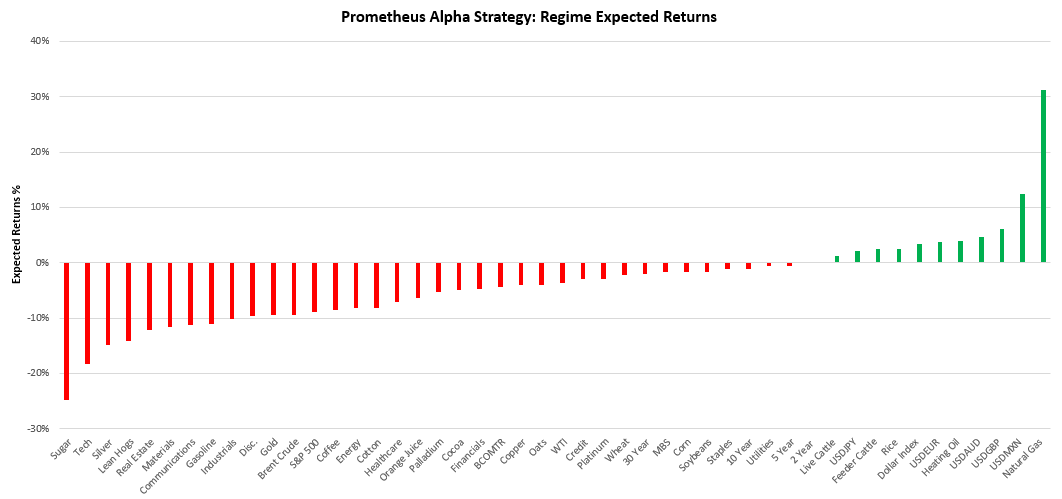

These moves continue to create an environment where our systems estimate the returns on asset relative to cash is negative. We show our current estimates of these expected excess returns over cash below:

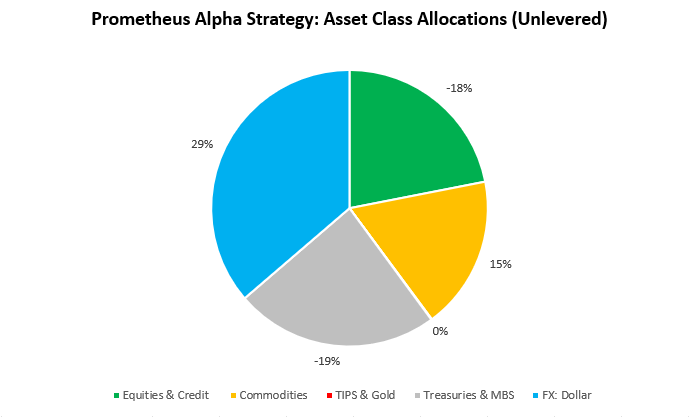

Keep in mind that these numbers are not adjusted for volatility; therefore, some expected returns may look much larger in magnitude than others. However, the primary takeaway from the above is that 75% of assets have negative expected returns in the current environment. This environment increasingly favors those who can either move into cash entirely or have the opportunity to short assets. Resultantly, our Alpha Strategy has had the following asset class allocations:

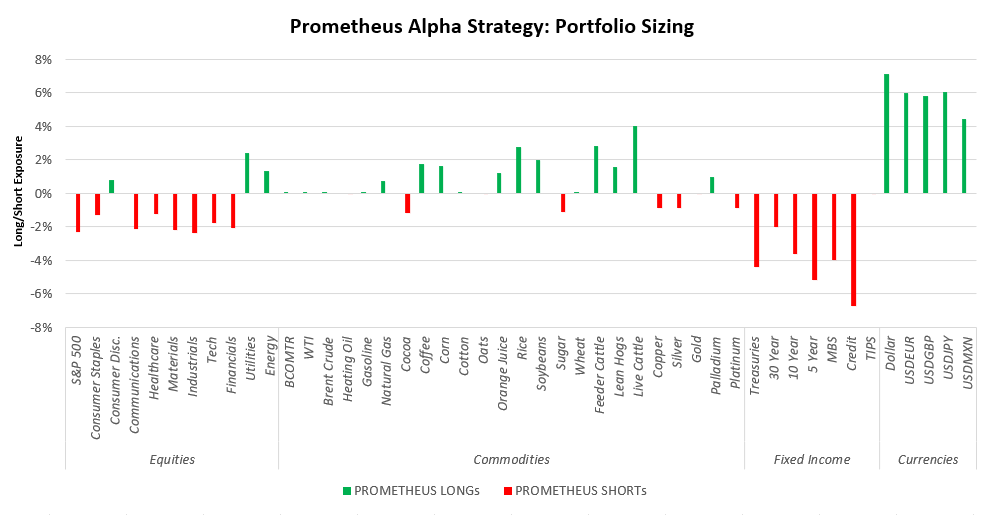

We show this at the security level:

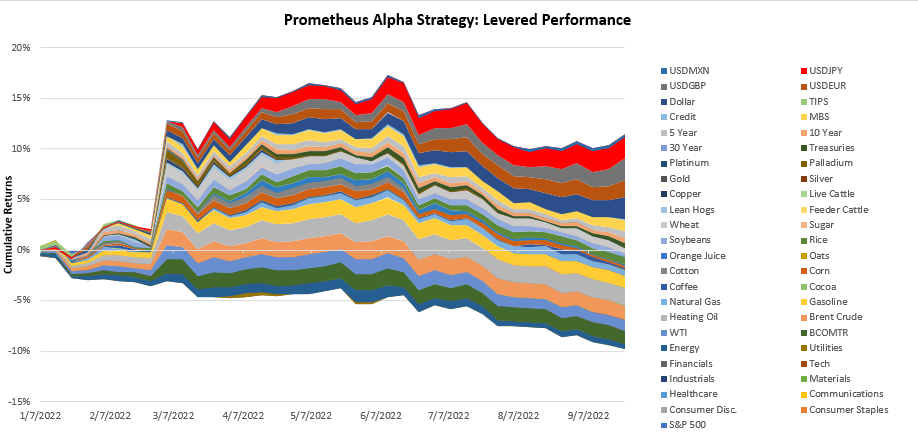

Our approach has proven a strong one during a challenging year for traditional allocations. Below, we show the contributions to the cumulative returns on our Alpha Strategy, which dynamically targets volatility of 10% using leverage:

In our view, the road ahead is likely to be even tougher than the journey thus far. Stay nimble.