Income & Consumption Rise

Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

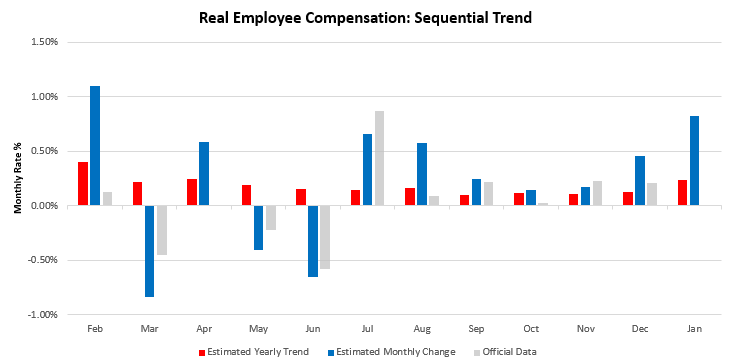

We received a slew of economic data this week, mostly on the US consumer. The latest data has showcased a significant rebound in consumer spending conditions. At the core of this strength was a reacceleration in labor market dynamics, pushing our estimate of nominal and real employee compensation. Below, we show our estimates of real employee compensation:

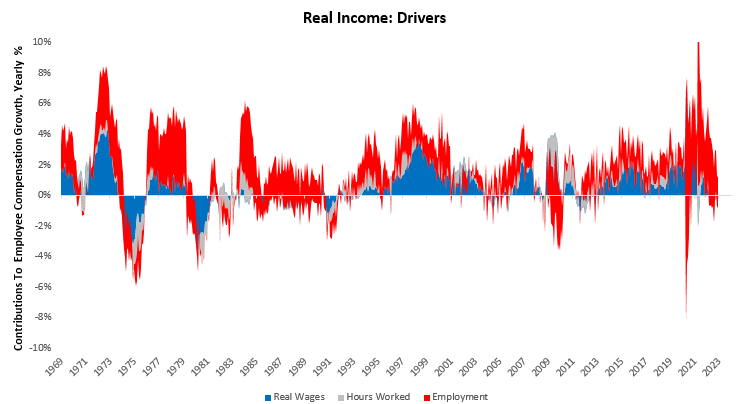

For further context, we show the evolution of the drivers of real income, i.e., wages, hours, and employment growth:

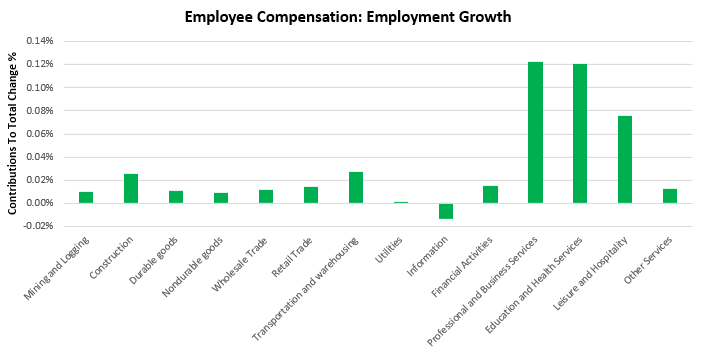

As we can see above, labor remains in the driving seat. The latest data showed a significant acceleration in employment growth, adding to total income. However, this boost to employment was fairly concentrated in non-cyclical sectors, particularly professional and business services. We show this below:

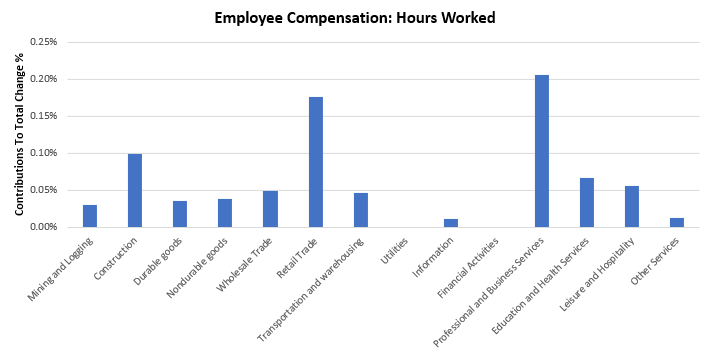

Complementing this increase in employment was a spike in hours worked, which also saw a large portion of its gains coming from professional and business services. We show this below:

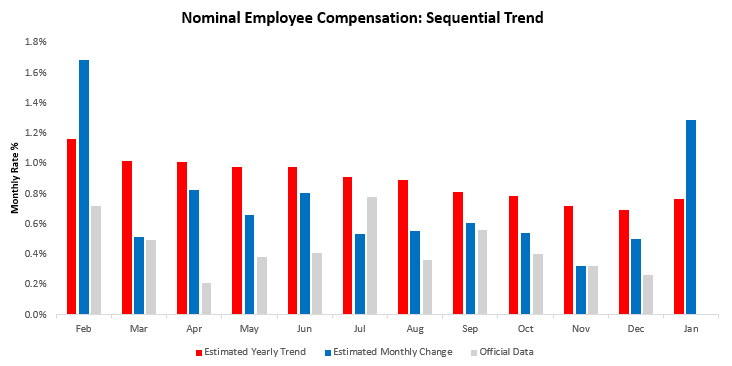

The combination of real wages, hours, employment, and wage inflation resulted in a nominal income rise, which we show below:

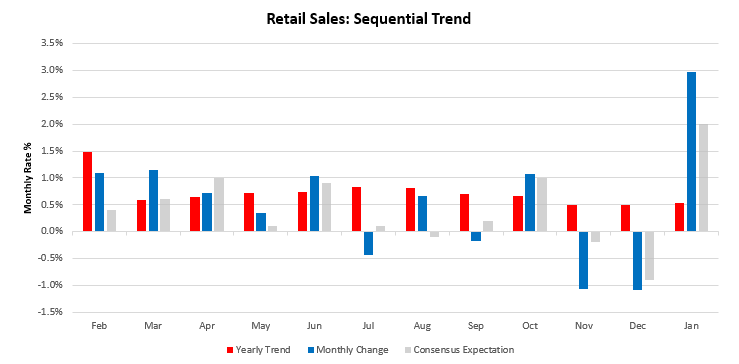

This increase in income fueled spending, which drove nominal retail sales up by 3%, a significant jump from months prior:

The latest retail sales suggest a strong likelihood of a rebound in personal consumption expenditures, i.e., consumer spending will likely support GDP and profits:

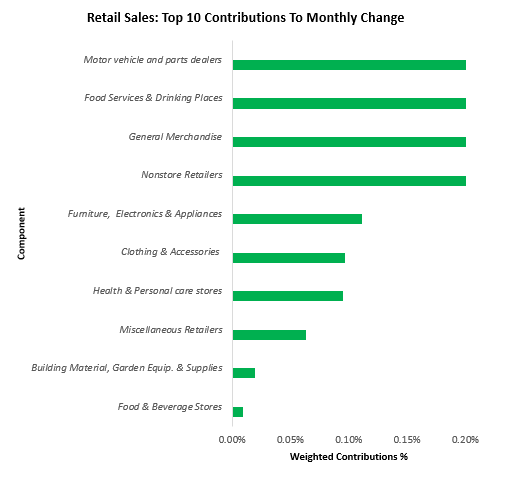

While nominal retail sales rose 3%, real sales rose 2%, reflecting a rebound in inflation. One print does not make a new trend, and retail sales remain in contraction, weighing on broader consumption. Nonetheless, the print showed strong nominal spending across the board. The primary drivers of this print were Motor vehicle and parts dealers (0.3%), General Merchandise (0.21%), & Food Services & Drinking Places (0.89%). Below, we show the top 10 drivers of the monthly change:

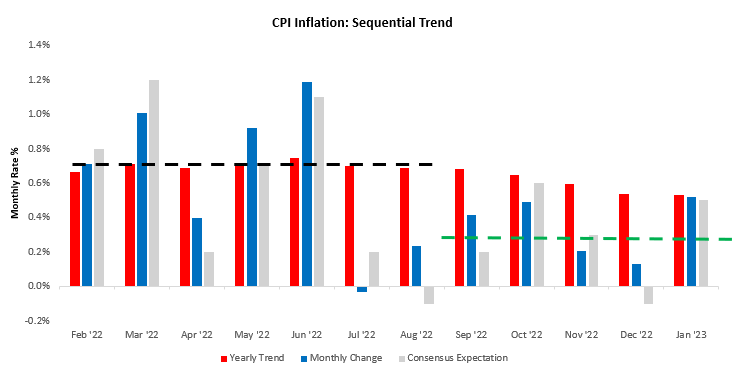

Therefore, strong employment and hours worked supported nominal income, which supported nominal spending and, in turn, flowed through to higher inflation. We saw the impact of nominal spending in CPI data this week, with CPI coming in relatively hot. CPI Inflation increased by 0.52% in January, surpassing consensus expectations of 0.5%. This print contributed to a sequential deceleration in the quarterly trend relative to the yearly trend. Below, we show the monthly evolution of the data relative to its 12-monthly trend and consensus expectations:

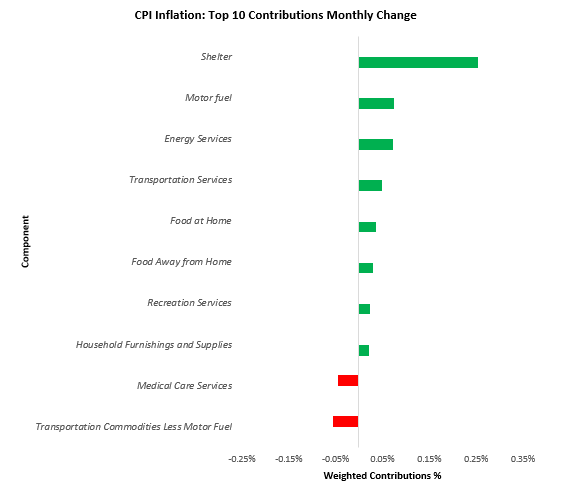

The primary drivers of this print were Motor fuel (0.07%), Energy Services (0.07%), Transportation Commodities, Less Motor Fuel (-0.05%), Shelter (0.25%), & Transportation Services (0.05%). Below, we show the top 10 drivers of the monthly change:

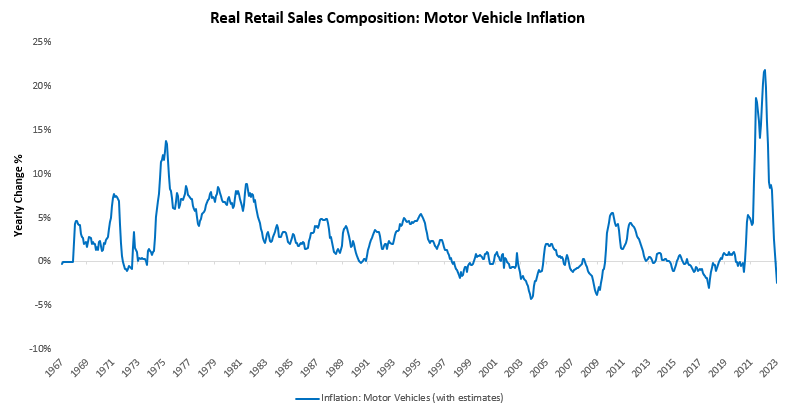

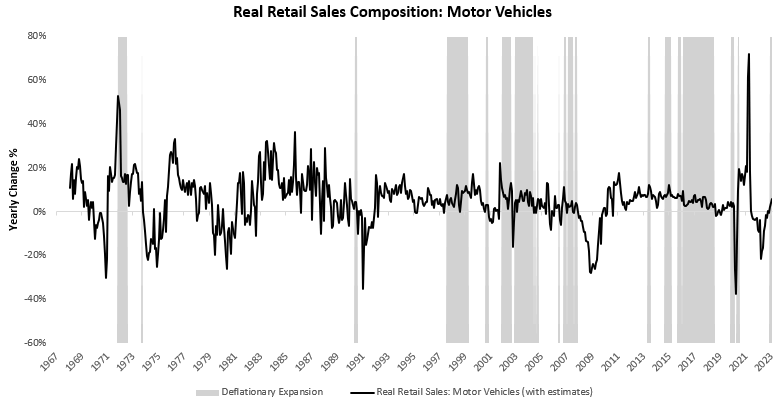

As we can see above, inflation came in largely in line with demand pressures coming from spending, with food, energy, services, and housing products increasing in price. However, the one area where price increases were inconsistent with nominal spending was automobile prices (transportation commodities). In fact, while this area received a high degree of nominal spending, automobile prices actually declined. The combination of these factors leads to a significant improvement in real automobile sales. Deflation is not uncommon in the automobile sector; in fact, it has been the primary lever used to drive output in the post-2008 world. We show motor vehicle inflation below:

Therefore, some degree of automobile deflation is likely consistent with an incremental reversion to pre-pandemic norms. Looking ahead, the question for automobile output is likely to be whether prices can be cut adequately to offset the slowing of nominal demand in order to keep output expanding, i.e., generate a deflationary expansion. So far, they have been able to do so, consistent with recent history; we show this below:

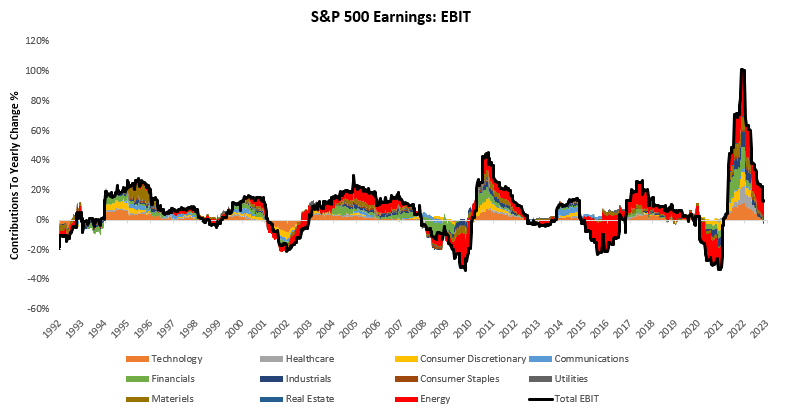

Overall, consumer spending dynamics have been positive on a real and nominal basis. The question for us is whether these increases in nominal and real spending household spending have come alongside increasing or decreasing business investment. If consumer spending increases alongside offsetting weakness in business investment, GDP growth will remain flat, but profits will likely suffer. This would worsen an already deteriorating trend in earnings, which we show below:

Overall, recent data suggest strength in consumer spending; the question is whether this comes alongside deteriorating business income. We will update you as this progresses. Until next time.

I am extremely impressed together with your writing talents as well as with the structure in your blog.

Is that this a paid topic or did you modify it yourself? Anyway stay up the nice quality writing, it’s uncommon to look a great blog

like this one today. LinkedIN Scraping!