Long Dollar & Stocks, Short Commodities

Welcome to our official publication of the Prometheus ETF Portfolio. The Prometheus ETF portfolio systematically combines our knowledge of macro & markets to create an active portfolio that aims to offer high risk-adjusted returns, durable performance, & low drawdowns. Given its systematic nature, we have tested the Prometheus ETF Portfolio through decades of history and have shown its durability. For those of you who are unacquainted with our systematic process, we offer a detailed explanation here:

In this publication, we will discuss the performance, positioning, & risks of the Prometheus ETF Portfolio and it will be published every week on Fridays to help investors understand how our systematic process is navigating through markets. Before diving into our ETF Portfolio positions, we think it is important for subscribers to understand the context within which our systems choose their exposures. Below, we offer our latest Month In Macro note, which contains the conceptual underpinnings of our systematic process within the context of the latest economic data:

We highly recommend you get acquainted with our outlook to understand best our systematic positioning outlined in this note. Turning to this week, we saw a significant amount of economic, suggesting a rebound in economic growth. We shared our tracking of these conditions here yesterday:

We think labor market expansion is the most important driver of the uptick in economic data this year. As we have explained previously, spending comes from income, which in turn is a function of nominal wages, hours worked, and employment. The balance between spending and output determines inflation. Recently, we have seen a jump in employment and hours, which drove up incomes, and financed spending. This nominal spending supported further inflation, which we saw in both CPI and PPI data. What is crucial to identify here is that the driving factor in the chain of economic events is the impulse from increased labor and hours. We do so to assess the likelihood of continuing this trend in both activity and spending. We find this unlikely that these labor impulses can continue based on our assessment of where we are in the economic cycle.

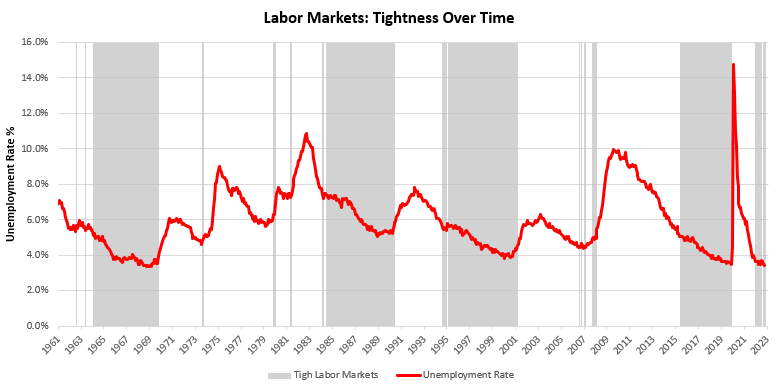

Over the last few months, we have entered a period where labor markets are cyclically and secularly tight, with unemployment rates now at 3.4%. Below, we show our assessment of past periods where labor markets have been significantly tight relative to their recent history:

As we can note from the above, labor markets can go through extended periods of tightness, i.e., tightness in itself is not a cause for loosening. However, what we think is even more important to understand is that as the labor market tightens the potential for further employment gains reduces. This is because, in the ideal state of the world, unemployment can only hit 0%, i.e., begin to move in lockstep with the labor force. Of course, it is practically impossible to have a 0% unemployment rate, and there is likely some natural unemployment rate. With this context in mind, it is essential to realize that the most recent employment data is unlikely to repeat itself on a trending basis. To help visualize this, we show the current path for unemployment based on the recent trend in data:

Based on the current trend in recent data, we would end 2023 with an unemployment rate of 1.2%. This would be wholly unprecedented and far out of line with any assessment of the natural unemployment rate for the economy. Therefore, we think this path is improbable.

Furthermore, most recent data is inconsistent with previous periods of tight labor markets. Below, we show the 3-month forward change in nominal wages, hours worked, and employment during periods when the labor market was tight or loose. To contextualize, we also show the most recent data prints in grey:

As we can see above, the most recent change in employment and hours worked is anomalous relative to previous periods of tight labor markets. Furthermore, the combination of factors this month is anomalous relative to any period in history (tight or loose). Therefore, we think it is more likely to see a slowing in labor market conditions rather than a continuation of labor market conditions. Below, we the expected path based on this assessment:

Keep in mind this projected increase in unemployment comes without any contractions in the labor market, just a reversion to a mean consistent with tight labor markets.

Therefore, looking through the drivers of the most recent acceleration in nominal spending and inflation, we continue to expect a slowdown in activity as the labor market runs out of fuel to propel nominal income. Furthermore, we expect this slowing impulse to be net support to the weakening of inflationary pressures, which will continue to stabilize at an uncomfortable high level. To be clear, we do not expect dramatic deflation but simply a stabilization of inflation rates.

While we remain confident in our assessment of inflation, this week’s market pricing did not support this view but did support our bets o tightening liquidity. Below, we show the attribution of this week’s returns from the Prometheus ETF Portfolio:

The Prometheus ETF Portfolio was flat on the week at -0.04%. Our equity allocation was generally offside this week, though our losses were somewhat offset by our dollar positions, reflecting our system’s views on tightening liquidity conditions. Overall, the diversification benefit of the portfolio was significant, as expected. Headed into next week, our systems have renewed the same bets, though with less conviction of the equity side and a short position in natural gas:

We show this at the asset class level:

This allocation has an expected volatility of 6.9% and a maximum volatility of 10%. We expect growth data to be the primary driver of market moves next week. We expect the growth picture to be mixed, with PMIs generally weaker but consumption and income data extremely strong. Overall, the mixed picture is unlikely to bring forward further expectations of policy tightening. Therefore, given the diversity of the portfolio and the likely mixed catalysts, the likelihood of achieving maximum volatility is relatively low.

We continue to navigate a turn in the economic cycle. Conditions continue to align for tightening liquidity to impact growth and inflation, which is reflected in our high cash, low conviction bets. We will delve deeper into these dynamics in notes tome come. Until next time.

Their worldwide reputation is well-deserved.

can i get generic lisinopril online

Bridging continents with their top-notch service.

They make international medication sourcing a breeze.

how to buy generic lisinopril prices

The best place for health consultations.

Top 100 Searched Drugs.

get cheap cytotec online

Their patient education resources are top-tier.

Excellent consultation with clear communication.

where can i get cheap cytotec without a prescription

Their loyalty program offers great deals.

They have an impressive roster of international certifications.

where to get cheap cytotec without insurance

A trusted partner in my healthcare journey.

Efficient, effective, and always eager to assist.

where can i get cheap lisinopril without dr prescription

This pharmacy has a wonderful community feel.

I’m really impressed together with your writing

skills as well as with the format in your blog. Is this a paid subject matter or did you customize

it yourself? Anyway stay up the nice high quality writing,

it is uncommon to look a nice weblog like this one today.

TikTok Algorithm!