Over this week, we will migrate all our publishing to our new website. Please make sure to subscribe below here if you haven’t already, as we will be transferring all our mailing lists to the new website. You can check it out here.

Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

Today, we offer our expectations for CPI, along with our tracking of the fiscal impulse coming from the US government. We start with our CPI expectations.

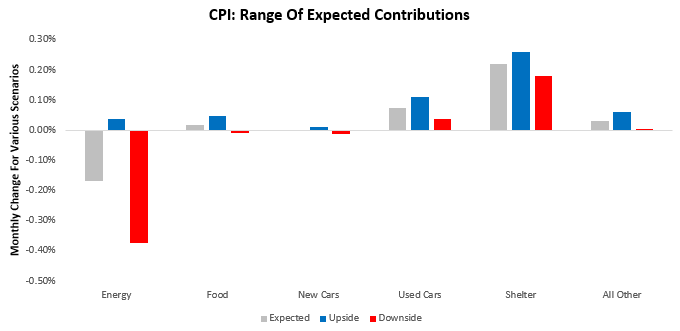

We expect CPI inflation to come in at 0.17% for the month of May. Below, we show the drivers of our expectations and the range of expected outcomes for each:

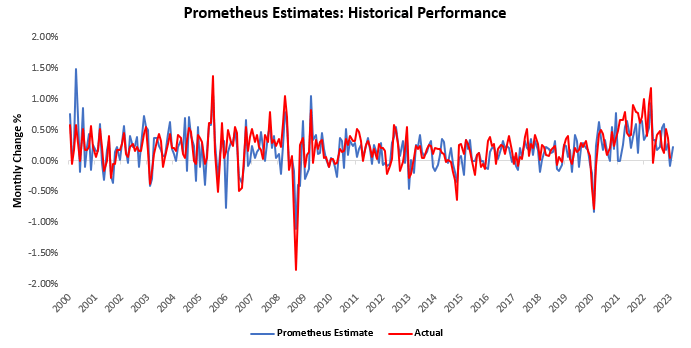

For further context, we offer a visualization of our estimates relative to realized CPI:

We think print is one for careful assessment. Particularly, we will be looking two examine two factors. First, we will looking to see whether motor vehicle inflation remains persistent. Given the industry dynamics we monitor, there is potential for new cars to see deflation as manufacturing productions alleviate some degree of supply shortages. Nonetheless, used car inflation likely shows significant potential to re-accelerate this month. Second, we will be looking to see if housing inflation can continue the deceleration we have seen in the last few prints. This would confirm that our expectations of disinflation in housing are taking hold. In summary, the print will likely look weak due to commodity factors. Still, it is imperative to note that excluding all other items, CPI inflation will remain above 2% just through the housing component. We remain far from the Fed’s objectives.

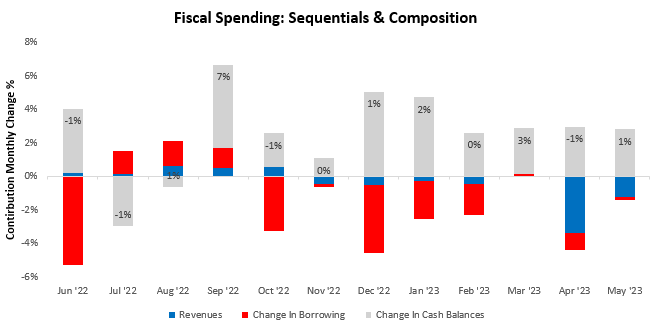

Turning to broader cyclical dynamics, we now examine the latest data on US government spending, i.e., the US fiscal impulse. Monthly spending data from the government contains significant volatility; therefore, we apply a smoothing process to extract spending trends in government data. Below, we show our estimates of the monthly changes in US government spending. We decompose this spending into its sources, i.e., government revenues, borrowing, and cash balances:

Our latest estimates for government spending in May saw spending rise by 1%, primarily driven by decreases in government cash balances. Over the last 12 months, the government has largely relied on spending its existing cash balances into the economy as the primary source of spending. We show this below:

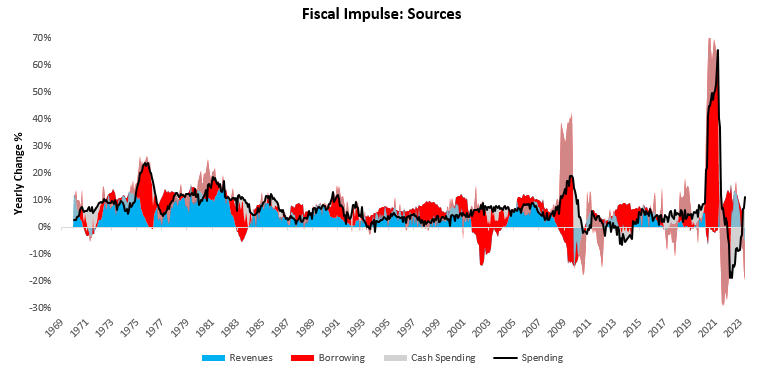

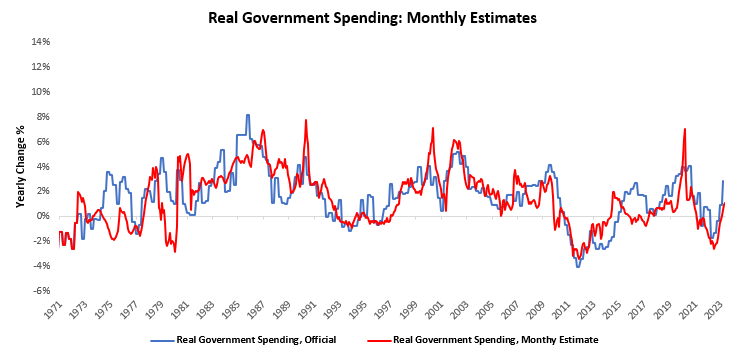

As shown above, government spending has accelerated over the last year, despite lower government revenues and borrowing. Below, we show how this has flowed through to GDP as well:

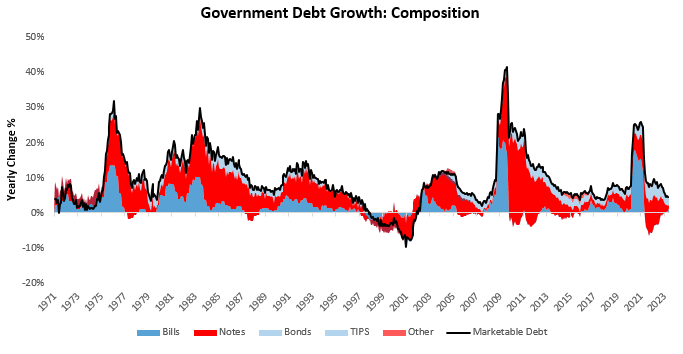

This spending has come as debt growth has slowed, but following the debt ceiling resolution, debt growth is likely to be as support to total spending and GDP in the future. We show the composition of debt growth below:

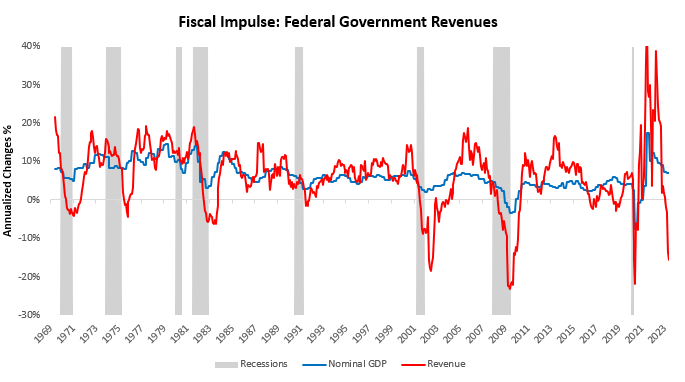

Alongside this modest borrowing growth, we have also seen significant weakness in government revenues. Government revenues come from taxes, and barring shocks to the tax code, they are a good gauge of cyclical conditions in GDP. We show this below:

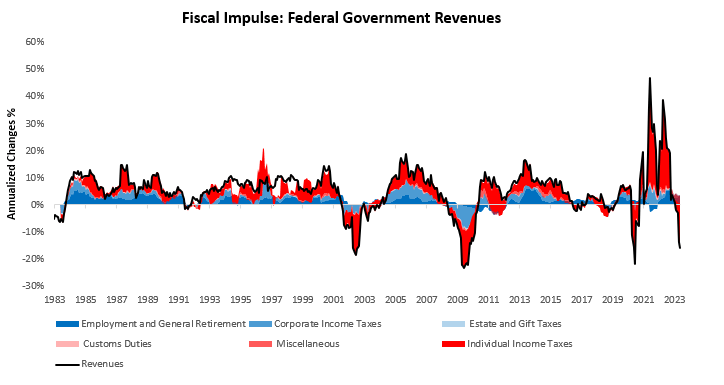

The primary driver of this slowdown has been the significant decline in personal income tax receipts. We show this below:

Overall, government revenues continue to paint a picture of weak private sector conditions. For government spending to continue to contribute to GDP, we will need to see continued borrowing, as government cash balances have largely been depleted. As business conditions deteriorate, corporate income taxes will likely soften alongside household income taxes. This decline will eventually be a headwind for government spending in GDP. In the meantime, the shortfall will need to be made up by sustained borrowing.