Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

Our message today is singular:

The pressures on production and employment are increasing, and we are slowly moving towards an environment of lower output and employment. These moves are likely to come alongside a backdrop of heightening nominal demand. The combination of these factors is likely to push us into outright stagflation.

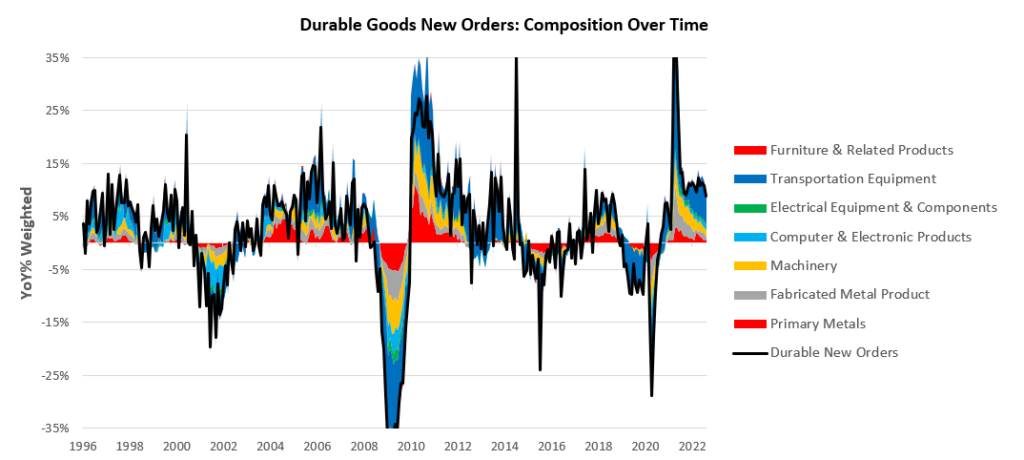

Today, we received data on the new orders for manufacturing durable goods. This information helps assess the underlying demand for manufactured items and is indicative of business demand rather than final demand, as manufacturers typically sell to other businesses rather than directly to the consumer. Resultantly, trends in new orders tend to reflect the outlook of companies, which are essentially a function of their current performance. Below, we show the most recent data for the new orders of durable goods:

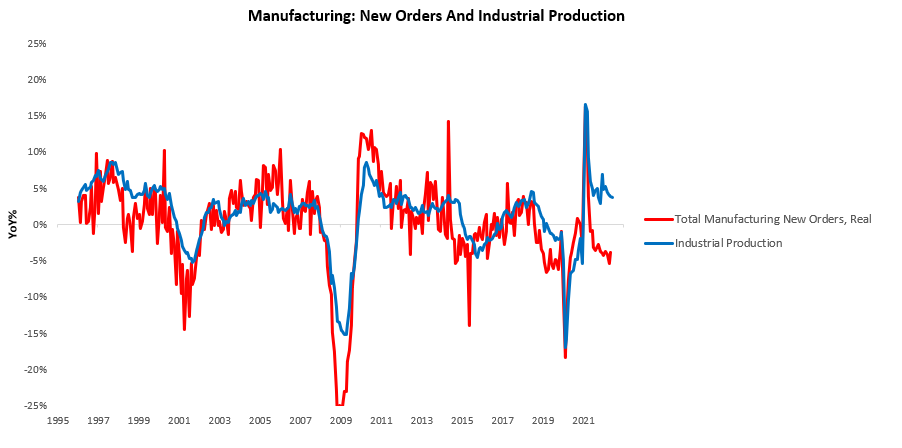

Over the last year, Durable Goods New Orders have been in a downtrend, and the latest values confirm this trend. As we can see above, durable goods orders remain healthy on a nominal basis- however, the picture is dramatically different when we adjust these numbers for inflation. New orders for durable goods are negative on a real basis, i.e., the volume of goods ordered is now declining. Furthermore, these values are at odds with industrial production, i.e., production continues to outpace new orders. We show this below:

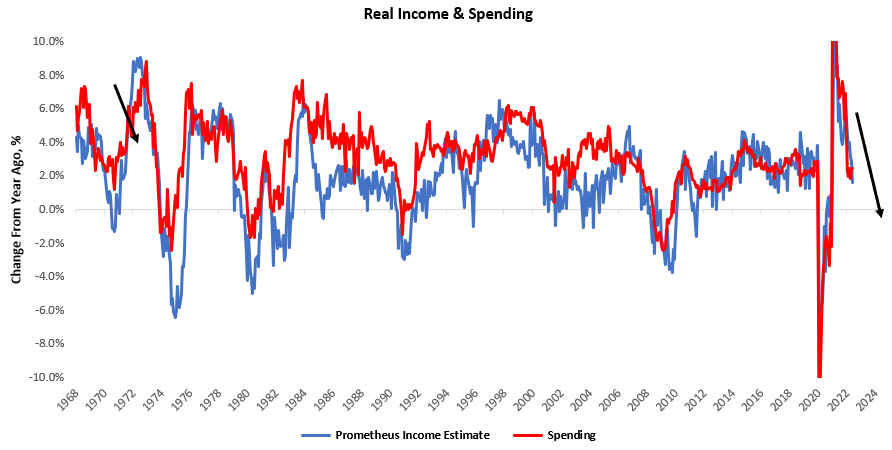

This mismatch between new orders and production is driven by the fact that consumer demand continues to deteriorate on a real basis as real incomes weaken. Below, we show how income & spending continue to weaken:

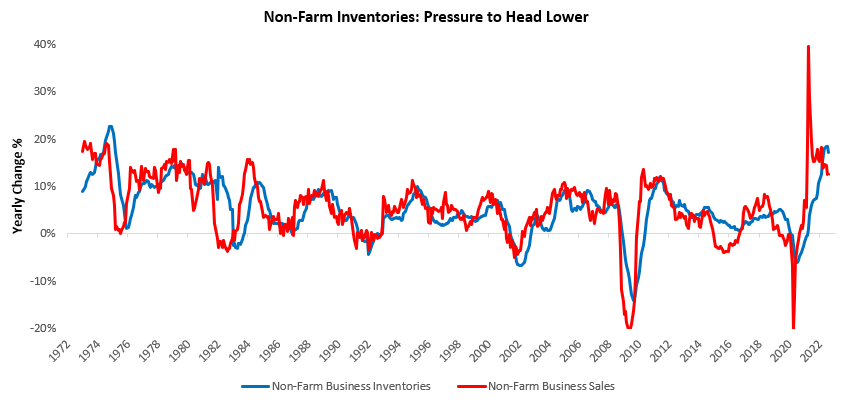

Since real incomes & spending are weak, business sales are also weak. As a result, excess production is finding its way into inventory build. Below, we show how business inventories are elevated relative to sales:

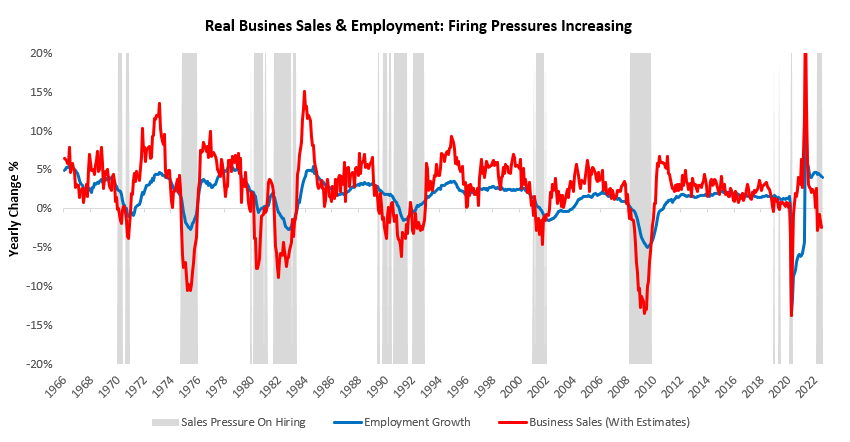

However, inventory build without adequate sales growth is an unsustainable dynamic; eventually, inventory growth will likely fall prey to weak sales. Resultantly, production will come under pressure as both final and intermediate demand dries up. Lowe output results in a lower need for workers- catalyzing layoffs. These moves are consistent with history since 1966, there have been eight periods where there has been a mismatch between sales & employment like today, and all of them have resolved themselves in labor force contractions.

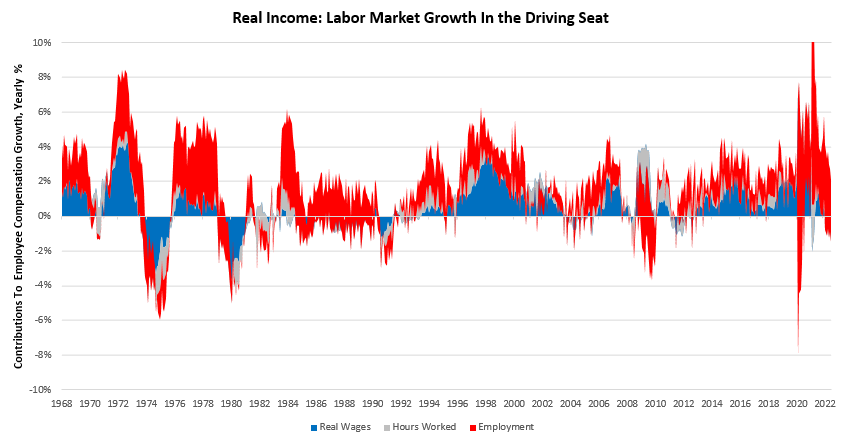

This dynamic is particularly important in today’s context, as labor force growth is the primary driver of income growth in the economy. Labor force growth accounts for more than 100% of real income growth today, as wages rates and hours worked have moved into contractionary territory. Recall income growth can come from higher wages, more hours worked, or more employment. Currently, all income gains are coming from increasing employment. We show the relative contributions below:

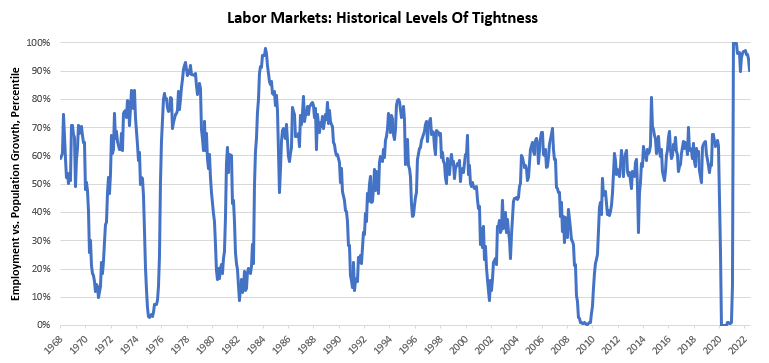

However, there are limits to how much we can increase employment (even with Fed tightening aside). We are in a historically tight labor market, i.e., there’s not much room to add more employment. Below, we show the current growth of the labor market adjusted by the population growth rate to show how extended the labor market is relative to the existing population.

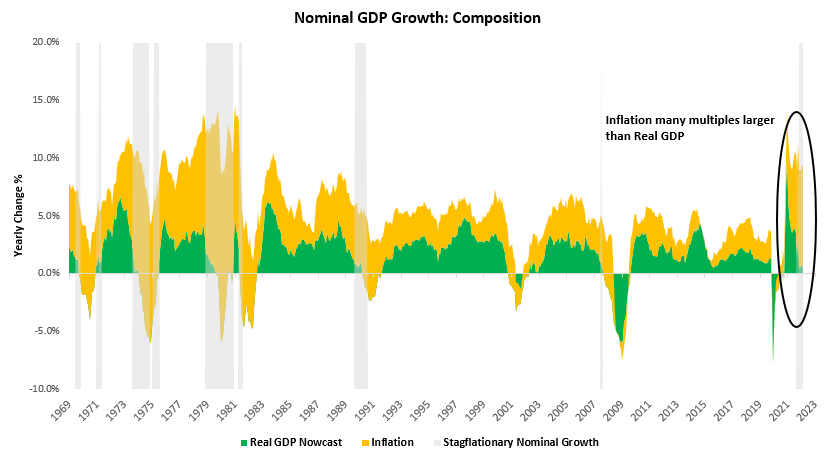

We are clearly in the tightest labor market on record. The combination of these factors creates a situation where there is a high and increasing likelihood that real economic activity will move towards contraction. However, nominal spending can still stay positive during this period. Nominal spending has inertia, i.e., nominal spending in one period tends to resemble nominal spending in the next. With a highly elevated level of nominal spending like today, it is doubtful that we will move into a period of contractionary nominal spending in the near term. Therefore, even if we see a decline in nominal spending over the next few months, it is unlikely to be as pronounced as the decline in real output due to the large difference in starting points. We show the composition of nominal spending below:

To reiterate: The pressures on production and employment are increasing, and we are slowly moving towards an environment of lower output and employment. These moves are likely to come alongside a backdrop of heightening nominal demand. The combination of these factors is likely to push us into outright stagflation.

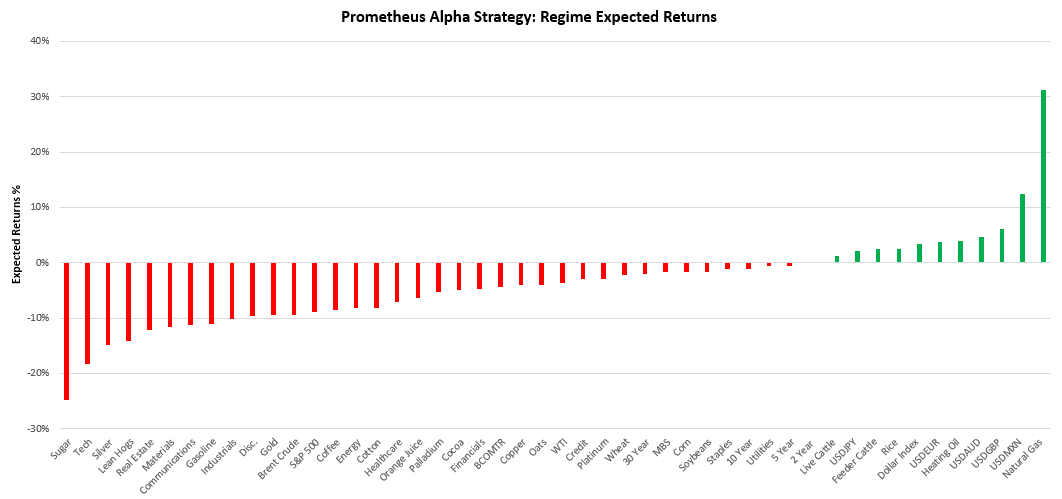

These moves continue to create an environment where our systems estimate the returns on asset relative to cash is negative. We show our current estimates of these expected excess returns over cash below:

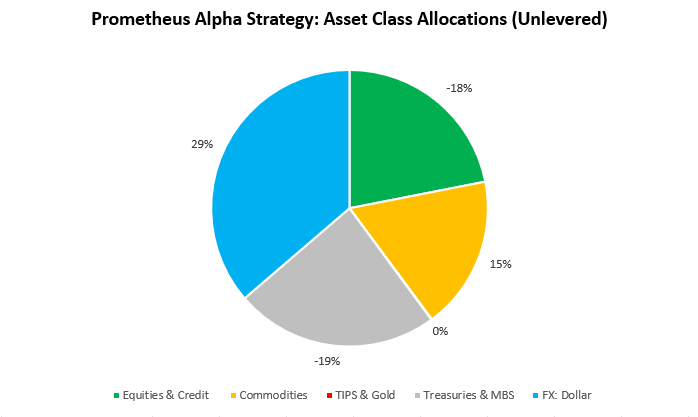

Keep in mind that these numbers are not adjusted for volatility; therefore, some expected returns may look much larger in magnitude than others. However, the primary takeaway from the above is that 75% of assets have negative expected returns in the current environment. This environment increasingly favors those who can either move into cash entirely or have the opportunity to short assets. Resultantly, our Alpha Strategy has had the following asset class allocations:

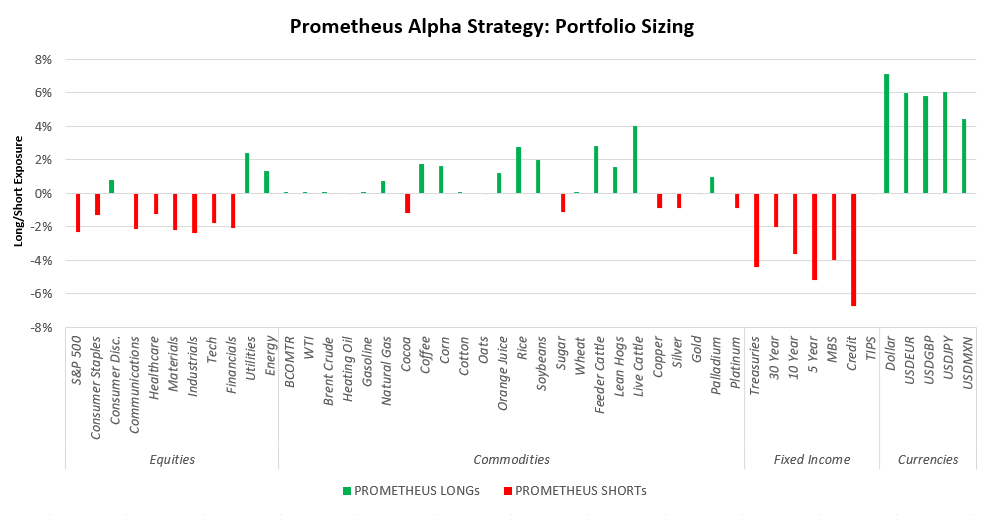

We show this at the security level:

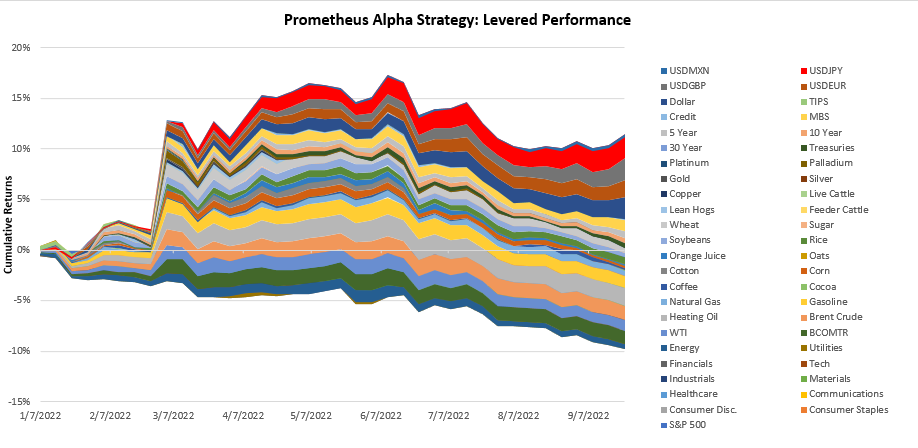

Our approach has proven a strong one during a challenging year for traditional allocations. Below, we show the contributions to the cumulative returns on our Alpha Strategy, which dynamically targets volatility of 10% using leverage:

In our view, the road ahead is likely to be even tougher than the journey thus far. Stay nimble.

Their adherence to safety protocols is commendable.

lisinopril oder ramipril

Love the seasonal health tips they offer.

Prescription Drug Information, Interactions & Side.

cytotec without rx

The pharmacists always take the time to answer my questions.

Outstanding service, no matter where you’re located.

cost of clomid without prescription

The best in town, without a doubt.