Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. Here are the top developments that stand out to us:

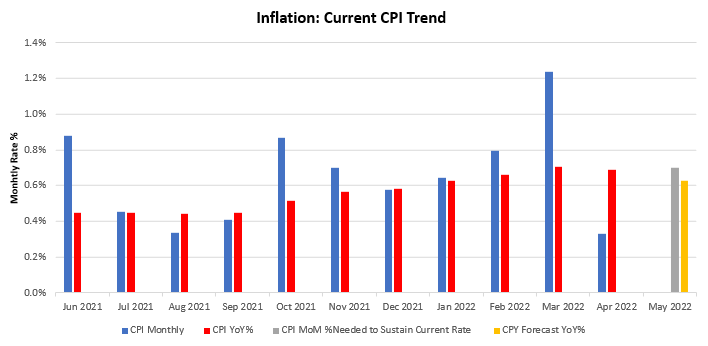

i. There is potential for CPI to decelerate modestly tomorrow; however, we remain in a stagflationary environment. By our estimates, inflation remains extremely elevated relative to recent history, though acceleration pressures are abating. For inflation to maintain its current rate of 8.3%, month-over-month CPI would need to come in at apprxoimately 0.7%, which is in line with expectations.

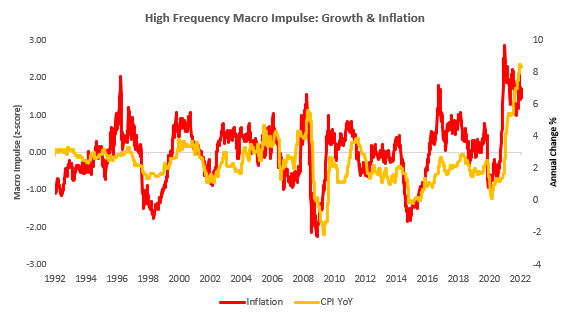

However, when we zoom out, we continue to see our proprietary high-frequency measures of inflation remaining extremely elevated:

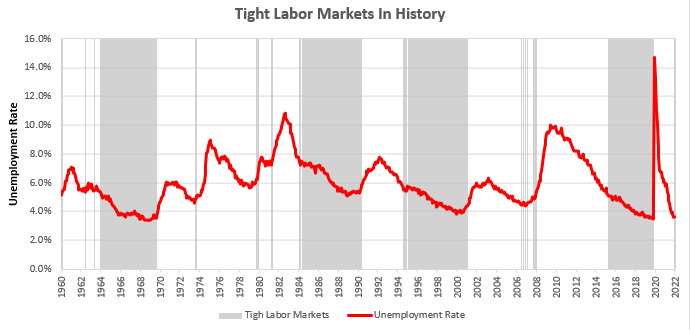

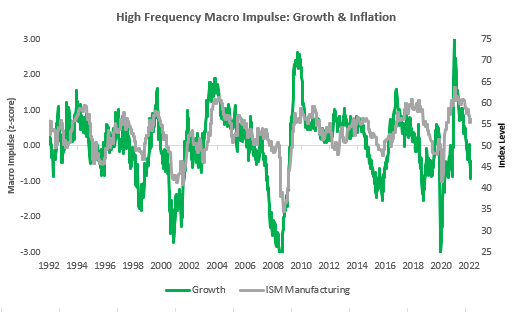

ii. Employment data weakened, with Jobless Claims data exceeding expectations. Unemployment is broadly below trend. Mississippi showed the greatest increase in unemployment claims, while Kentucky showed the greatest decrease.

However, today’s prints showed jobless claims come in above expectations. We expect more prints like these as the labor market becomes increasingly tight. Unemployment rates determine the potential for improvement in employment, and we are quickly running out of room:

This does not bode well for consumer spending, with real incomes feeling the pressure of high inflation and employment showing limited room to grow. Stagflationary dynamics remain in place.

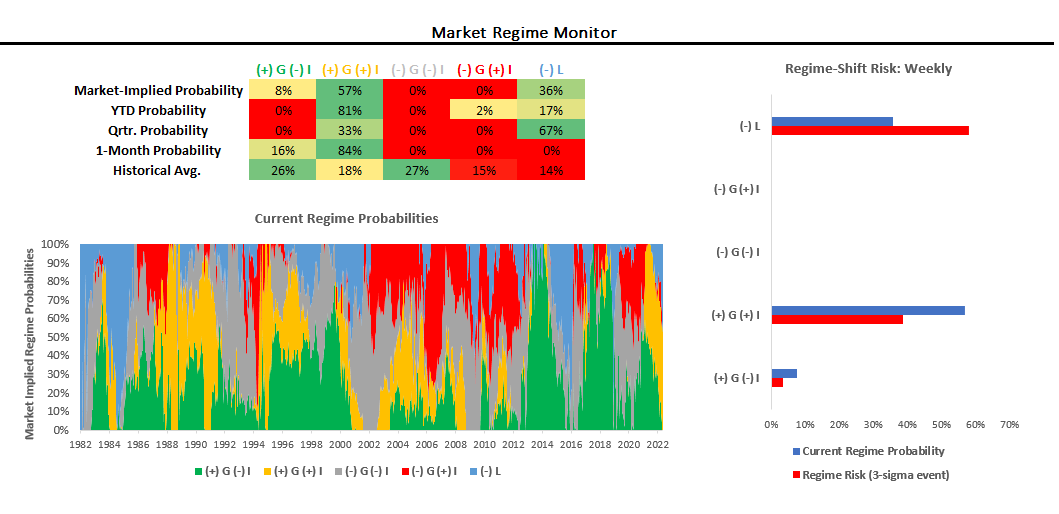

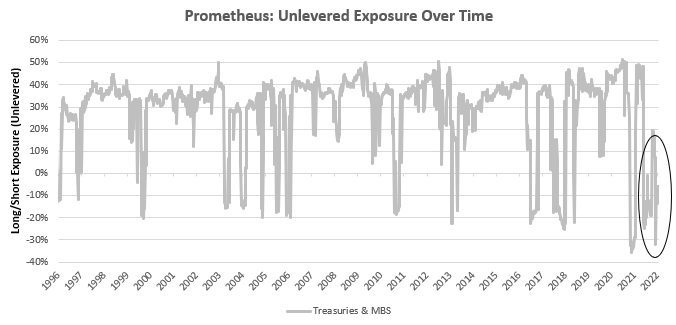

iii. Markets are still pricing elevated inflation and we see this in the real economy as well. Bonds and stocks will both fall prey to this, we are now shorting Treasuries as well. We show our market regime monitors below:

Over the last month, markets have dominantly priced nominal growth with a stagflationary tilt. This dynamic as far exceeded any expectations that most discretionary observers had in terms of duration, highlighting the important of a high frequency tracking of conditions. With inflation remaining he dominant risk to manage in markets, we now turn towards shorting fixed income securities broadly in our Alpha Strategy:

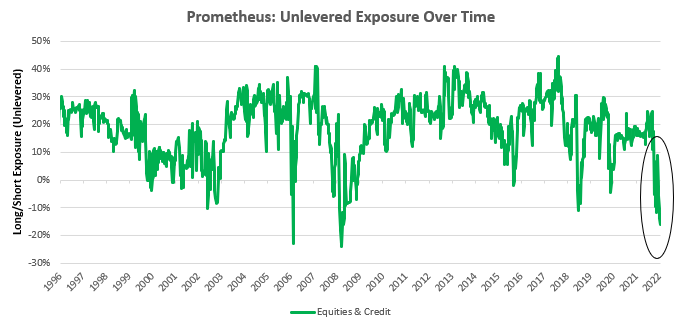

This exposure is in addition our existing net-short equity position:

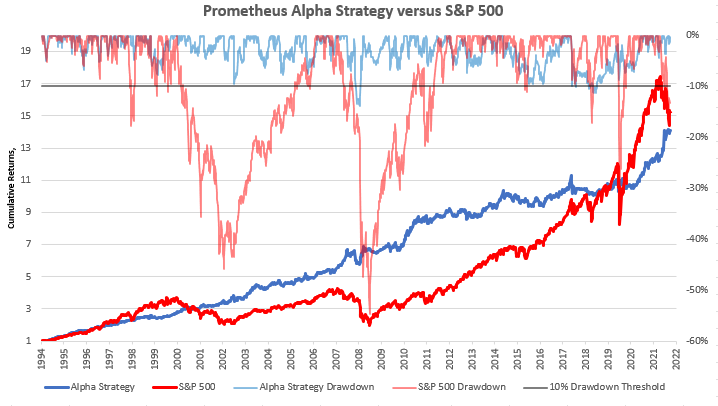

This approach has served we historically, and we show pre-tax cumulative performance for the strategy that applies our investment frameworks systematically (after accounting for transaction costs) versus the S&P 500. The system dynamically targets a volatility of 10%, with a maximum leverage of 2.2x:

Our ETF Strategy on the other hand, remains neutral on Treasuries. Nonetheless, performance of the ETF Strategy has been solid this week, especially given the year-todate masacre in conventional 60//40 portfolios. Our systems continue to expect further deterioration in economic data, and therefore remain positioned as such:

Markets may bounce or fall, however we continue to believe that the fundamental drivers of assets will be the primary driver of returns over the economic cycle. Stagflation is not a time to own disinflation beneficiaries, i.e. equities and treasuries. Stay nimble!