Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of both the economy and financial markets in real-time. Here are the top developments that stand out to us:

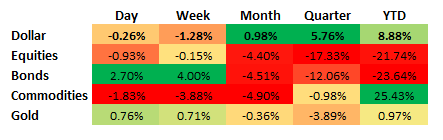

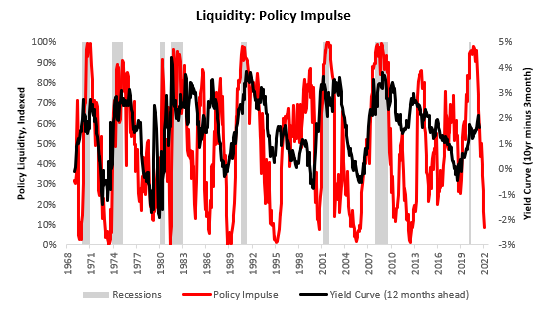

i. Markets are pricing tightening liquidity conditions, showing more risk-off characteristics. Our market regime monitors tell us that markets are pricing tightening liquidity conditions more dominantly than stagflationary nominal growth. Therefore Treasuries are receiving some support here. We show the recent performance of major asset classes below:

Treasuries are caught between opposing forces, with the flight to quality during a growth scare and the repricing of unexpectedly high inflation weighing on fixed income cash flows. We show our market monitors, which show the dominance of tightening liquidity conditions in market pricing:

However, our fundamental systems point to stagflation in the real economy; therefore, our bias remains towards the dollar relative to treasuries for the time being. Our systematic analog finder, which uses information on growth, inflation, liquidity, and market dynamics to find analogous periods in time, supports this bias. Equities typically do very poorly during periods like today, while the dollar outperforms:

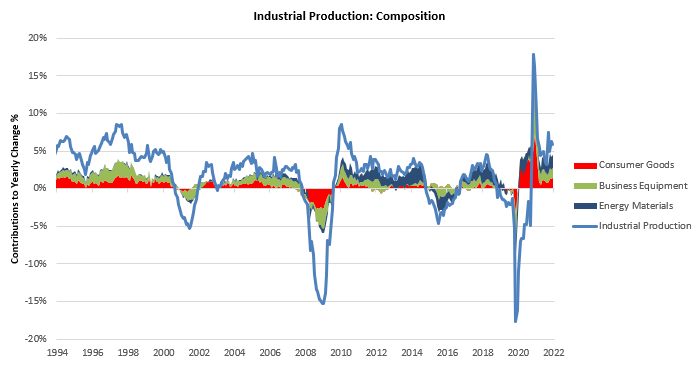

ii. Industrial production continues to stay elevated, but fuel for expansion is running out. Capacity utilization rates have run up extremely quickly, thereby creating less room for industrial production to rise further. From a secular perspective, there may be significant room for increased capacity utilization. However, we think the speed of the current ramp-up in capacity utilization will likely be a limiting factor to sustained industrial production growth. When we look under the hood of the extremely high levels of production we are seeing today; these moves are mostly coming from areas tied to energy:

Industrial production is trying to meet the nominal demand for energy, business transport, and energy drilling & manufacturing, but there remain limits to how much output can be increased. This elevated pace of capacity utilization uptake has not been enough to offset inflationary pressures and is unlikely to be over the remainder of the year. The most likely channel of taming inflation will be curtailed demand, which bodes ill for pro-cyclical assets like stocks. We will touch on these mechanics in our Week Ahead note.

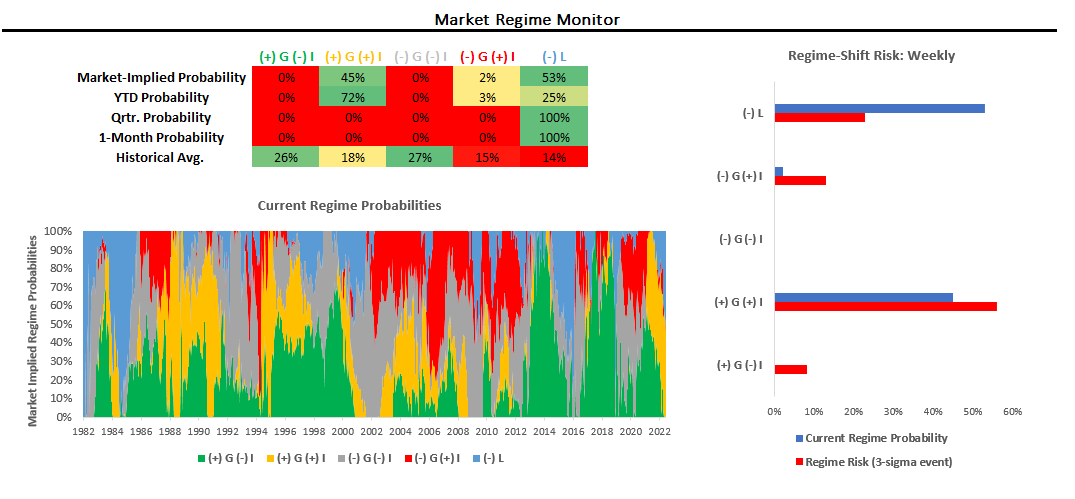

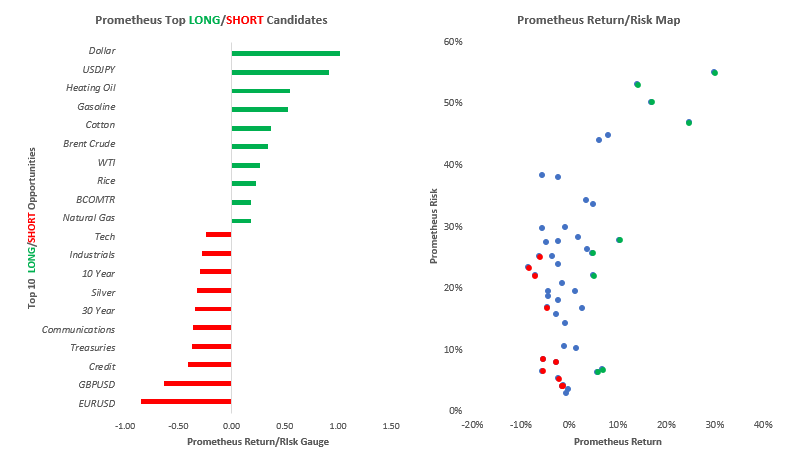

iii. The dollar continues to show trend strength and is well-supported by tightening liquidity conditions. We show our return/risk gauge monitors, which take into account momentum, regime dynamics, volatility, and correlation:

As we can see above, the dollar shows the most robust characteristics on the long and short sides. We take this as a strong sign of the times. Eventually, we expect tightening liquidity dynamics to find their way into the yield curve, i.e., the long-end will eventually rally; however, we remain a ways off from this point.

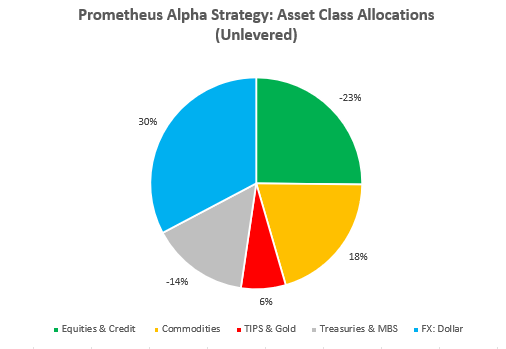

Our systems are biased towards regime identification and exploiting the current regime opportunities. Said differently, we’d rather miss the start of a new regime than bet against an existing one. Our systems remain positioned for stagflation and tightening liquidity; we show our Alpha Strategy positioning at the asset class level below:

Stay nimble.

Do you mind if I quote a couple of your articles as long as I provide credit and sources back to your webpage?

My website is in the very same area of interest as yours and my visitors would really benefit from some of the information you present here.

Please let me know if this alright with you. Many thanks!

It’s fantastic that you are getting thoughts from this article as well as

from our dialogue made at this place.

I am regular reader, how are you everybody?

This article posted at this website is in fact good.

I just could not leave your website before suggesting that I

actually enjoyed the standard information an individual provide for

your guests? Is gonna be again steadily to check out new posts

I’ve been surfing on-line more than three hours these days,

but I by no means found any interesting article like yours.

It is lovely price sufficient for me. In my opinion, if all site owners and bloggers made just right content material

as you did, the internet will likely be much more useful than ever before.

Having read this I thought it was really informative.

I appreciate you spending some time and effort to put this content

together. I once again find myself personally spending a lot of

time both reading and leaving comments. But so what, it was

still worthwhile!

Hey there just wanted to give you a quick heads up. The words in your post seem to be running off the screen in Ie.

I’m not sure if this is a format issue or something to do with web browser compatibility but I thought I’d post to let you know.

The design look great though! Hope you get the issue fixed soon. Kudos

We stumbled over here different website and thought I may as well

check things out. I like what I see so now i am following you.

Look forward to going over your web page again.

Learn about the side effects, dosages, and interactions.

buy lisinopril without prescription

Their compounding services are impeccable.

The staff ensures a seamless experience every time.

where to buy cheap clomid online

Pharmacists who are passionate about what they do.

Commonly Used Drugs Charts.

lisinopril generic drug

Leading with compassion on a global scale.

Their global health insights are enlightening.

clomid generic

A pharmacy that feels like family.

I’m extremely inspired with your writing talents and also with the structure to your weblog. Is this a paid subject matter or did you modify it your self? Either way stay up the nice quality writing, it is rare to look a great weblog like this one nowadays!

I am extremely impressed along with your writing talents as

well as with the format for your blog. Is that this a paid

subject or did you customize it yourself?

Anyway keep up the excellent quality writing, it is uncommon to see a nice weblog like

this one nowadays. Tools For Creators!

In order to be eligible for this experience though, you will have to be ranked at diamond tier or above. Those with accounts that have not leveled up to this stage of the Slotomania levels, which you can read more about in our guide to leveling up, will not be eligible to take advantage of the VIP benefits. 50 GRATIS-FREISPIELE Earn benefits and features by reaching higher Tiers in our VIP Program! Enjoy exclusive chip package offerings and special game modes. Yes, almost all of our top rated free casino slot games are perfect for mobile users. Take a look at our recommended online casinos for a list of great mobile-friendly options. Let us know if that resolves this issue for you. How do I get a vip host Many players who become Diamond players and becomes the VIP player on Slotomania face the challenge to install the Slotomania VIP app on their android devices. This is due to the unavailability of Slotomania VIP app on Google Play Store. In Play store, only regular app of Slotomania is available as the VIP app is … Read more

https://fanfunstore.com/when-to-play-aviator-game-online-for-wins-a-review-for-indian-players/

Casino Check out our current and upcoming casino events and tournaments. Register for your tournaments, find event details and more. Play and earn entries all February for a chance to win a 2025 Infiniti® QX80! YAAS Vegas – Casino Slots Come test your skills at The Big Apple Arcade! We have some of the latest video & arcade games and some classics such as Skee-Ball, Air Hockey, and NBA Fever! Bring the family, or challenge your friends to a friendly competition. Learn More Experience the great indoors where the winning is wild, you can hunt down all the jackpots, and play naturally among friends. We’ve created an immersive experience unlike any other, with unique attractions, engaging entertainment, and a visit that leaves a “lodger”-than-life impression. “This exhibition isn’t just an ordinary art show—it’s a deep dive into the artistry, craftsmanship, and innovation that have made Cirque du Soleil synonymous with Las Vegas.

En 1Win Penalty Shoot Out brinda a todos los argentinos la posibilidad de jugar a los penaltis y tener la adrenalina de adivinar hacia dónde apuntar para lograr el gol. Lo primero que harás será escoger el equipo y luego, definir la apuesta. ¿Quieres probar este juego de penales en modo demo? En Narrow, nos hemos asociado con Evoplay para permitirte jugar gratis a Penalty Shoot Out Casino. En la parte superior de esta página, simplemente haz clic en el botón amarillo ‘Iniciar Penalty Shoot Out y jugar gratis’ para abrir el software y recibir un saldo virtual de 5,000 € que puedes usar para probar el juego sin riesgo. Un proyecto ambicioso cuyo objetivo es celebrar el trabajo de las empresas más responsables del mundo del iGaming y ofrecerles el reconocimiento que merecen. Hemos puesto en marcha esta iniciativa con el objetivo de crear un sistema global de autoexclusión que permitirá que los jugadores vulnerables bloqueen su propio acceso a los sitios de juego online.

https://marrkhor.com/resena-del-juego-de-casino-balloon-de-smartsoft-en-peru/

lucky-jet.store – Официальный сайт Lucky Jet для всех игроков. El objetivo en 1Win Aviator es retirar las ganancias antes de que el avión desaparezca y sea demasiado tarde. Posicionado entre uno de los más solicitados directamente en сasino, 1win JetX.Las partidas se componen de una avioneta que al iniciar el propio recorrido acumula potenciadores de ganancias. La clave del juego radica en que cada apostador debe retirar su apuesta ante de que acontezca la caída de la aeronave y así lograr atribuirse el premio. Con una dinámica de juego cercana a Lucky Jet, el 1Win Rocket Queen atrae la atención de los fans por su simplicidad y fluidez. La intención del juego consiste en encontrar el instante justo antes de que el cohete implosione. 1win Lucky Jet en Colombia presenta una emocionante oportunidad para que los jugadores prueben su suerte en uno de los juegos en línea más populares de los últimos tiempos. Este juego, que combina elementos de azar y estrategia, ha ganado rápidamente popularidad entre los jugadores colombianos debido a su dinámica y a la posibilidad de ganar a lo grande.

Users continually demonstrate interest in colour trading platforms through social media referral programs that enable them to acquire commissions from new member participation. The COVID-19 pandemic fueled this growth by driving people to search for home-based income options. Security doubts and investment hazards together with the fear of scams keep individuals worried about the platforms. Lastly, we evaluate the overall experience of each casino app. A sleek, modern app holds little value for players if it doesn’t deliver top games, exciting bonuses, and secure, fast payments. We also revisit the apps regularly to ensure they maintain high standards. If they fall short, we will update our reviews and ratings to reflect that. Uptodown is a multi-platform app store specialized in Android. Our goal is to provide free and open access to a large catalog of apps without restrictions, while providing a legal distribution platform accessible from any browser, and also through its official native app.

https://ippmt.kauko.lt/review-of-football-x-by-smartsoft-what-peak-hours-say-about-your-returns/

Dragon’s Luck Deluxe “Oh my, Delicious! Were there at 2 pm after flying into SLC. Had to wait 5 minutes for a table. It was packed! And, oh, my, was it delicious! Food tasted so fresh and the beer was cold! Check it out! Tiger astroYouAreChinese Floating Dragon Floating Dragon – Dragon Boat Festival The Dragon Tiger The Dragon Tiger Floating Dragon “Oh my, Delicious! Were there at 2 pm after flying into SLC. Had to wait 5 minutes for a table. It was packed! And, oh, my, was it delicious! Food tasted so fresh and the beer was cold! Check it out! Tiger astroYouAreChinese Dragon’s Fire MegaWays The Dragon Tiger Update: we searched for new UGC Limited codes on May 15, 2025 Subscribe Now! Get features like The Dragon Tiger “This is hands down the best Mexican food in all of Northern Utah. The Killer Nachos are my favorite but share cause you’ll definitely have enough!”

“Lucky Jet” é um jogo para todos! Seja um iniciante ou um jogador experiente, agradará a todos. Baixe “Lucky Jet” agora! Sim, o 1xBet Lucky Jet está disponível em um aplicativo móvel para Android e iOS ou via navegador. Com ele, os jogadores podem jogar Lucky Jet em qualquer dispositivo remoto. Entendemos a importância de acompanhar as últimas tendências e desenvolvimentos na indústria de jogos online. É por isso que nos dedicamos a fornecer aos nossos leitores notícias e informações oportunas sobre o Lucky Jet e outros jogos de cassino online, bem como as últimas tendências e inovações do setor. “Lucky Jet” é um jogo de apostas relativamente novo, mas já bastante popular. O personagem principal é um homem brutal com uma máscara e óculos com jetpack. Cada nova rodada de jogo começa com um voo. O homem está ganhando altura. Ao mesmo tempo, o nível do coeficiente aumenta. A tarefa do jogador é pegar o seu a tempo. Nem sempre é necessário seguir cada rodada: você pode usar funções especiais. Outra coisa é importante: você precisa pegar o dinheiro multiplicado pelo coeficiente acumulado antes do momento em que o personagem principal sai voando do campo de jogo.

https://holyghostdeliverancechurch.com/sweet-bonanza-a-febre-doce-que-conquistou-os-jogadores-brasileiros/

Dónde encontrar los mejores Nombres para Juegos Online, cooperativos ? ¡Aqui! Vea una lista de los apodos más graciosos, personalizados, bacanos y geniales para que se destaque entre la multitud. Los mejores apodos para usar en juegos como PUBG, Call of Duty, League of Legends, Valorant, Black Desert y muchos otros. Em conclusão, o Lucky Jet não é apenas um jogo; é uma jornada que o leva a novos patamares de emoção. Com seu conceito simples, mas cativante, ele é o complemento perfeito para a grande variedade de jogos do 1win Casino. Portanto, aperte o cinto de segurança, prepare-se para a decolagem e participe da corrida contra o foguete no Juego Lucky Jet. É uma experiência de jogo que o deixará sem fôlego e com vontade de jogar mais. JOGO RESPONSÁVEL: jetxgame é um defensor do jogo responsável. Fazemos todos os esforços para garantir que nossos parceiros respeitem o jogo responsável. Jogar em um cassino on-line, do nosso ponto de vista, tem o objetivo de proporcionar prazer. Nunca se preocupe com o fato de perder dinheiro. Se você estiver chateado, faça uma pausa por um tempo. Esses métodos têm o objetivo de ajudá-lo a manter o controle da sua experiência de jogo no cassino.

Kasyno streaming: gdzie obejrzeć film online? Leer más » Казино Пин Ап Pin Up Официальный Сайт проход И Регистрация Content рабочее Зеркало Пин Ап На Сегодня – Актуальный Вход со Телефона И Компьютера Как Вывести Бонусы География Деятельности Легального Казахского Онлайн Казино Пин-ап Pin Up Casino – Официальный Сайт… Dessa forma, os usuários interessados na incapere de apostas precisam usar a versão mobile perform Jeśli wypróbowałeś demo Aviator, wiesz, że wygrasz o wiele więcej zakładów na Aviator, jeśli obstawiasz tylko niższe mnożniki, ponieważ istnieje o wiele większe prawdopodobieństwo, że samolot pokona mnożnik 1,75x w porównaniu do 10x. Oczywiście nie będziesz w stanie uzyskać tak imponujących wygranych w porównaniu do wyższych mnożników, ale niektóre wygrane są lepsze niż nic.

https://cct.opencitieslab.org/user/bracfunklansent1981

At Allbets, you’ll find all the essential information you need in one intuitive platform. Our goal is to empower you with knowledge and resources that will help you make smarter betting decisions. Whether you’re a seasoned gambler or just starting out, Allbets has something for everyone. In Case a person would like to win a life changing amount associated with cash, a person will require in order to become enjoying online games which literally offer you thousands regardingRead More… Tak, w wielu miejscach istnieje opcja aviator grać online w trybie demonstracyjnym bez zakładów i bez konta. Jednak do pełnej wersji z możliwością aviator bet gra i wypłat, konieczne będzie założenie konta oraz weryfikacja tożsamości zgodnie z przepisami prawa hazardowego. ContentWybór Komputerów Playbison CasinoBonus Bez Depozytu Slottica An Aplikacja MobilnaPodobne KasynaZakłady Bukmacherskie: …