Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

If you haven’t already, check out Episode 5 of the Prometheus Podcast! For this episode, we have another exceptional guest for you- Bob Elliott. Bob is the Co-Founder and CEO of Unlimited- a company that uses machine learning to replicate hedge fund strategies in a low-cost ETF format. Before starting Unlimited, Bob spent over a decade at Bridgewater Associates, one of the largest and most successful macro hedge funds, and was integral to building their systematic process. Bob brings a rich mixture of economic analysis, portfolio construction, and systematic thinking to this episode, which is not to be missed! Aahan & Bob cover almost every aspect of macro in their discussion and provide a rigorous framework for thinking about the current environment. If Alpha was ever available on a podcast, it’s this one!

Now, let’s dive into our observations. Summarily:

-

PMI data continues to paint a picture of declining activity, taking us one step closer to stagflation.

-

Production has shown resilience. However, our analysis of the underlying drivers shows that this strength is driven by inflationary dynamics and is unlikely to persist.

-

Despite data evolving to tell us that stagflation is the likely destination of the US economy, the equity market bounced significantly at the start of this week. Our systems see this as an opportunity.

Stocks and nominal bonds remain in a bear market. The fundamental pressures causing these moves are unlikely to relent any time soon. Therefore, while there may be a technical reprieve from downwards pressures, our systems see these counter-trend moves as opportunities to capitalize on. Let’s dive in.

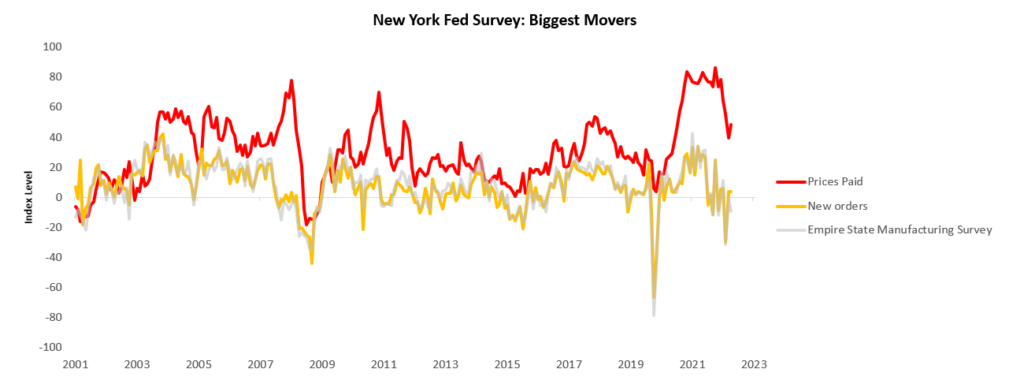

i. PMI data points to weakening activity. This week, we received PMI data from the New York Federal Reserve. The latest New York Fed manufacturing survey data showed a contractionary reading of -9.1, disappointing consensus expectations of -4.3. This reading was a sequential deceleration within a decelerating trend.

The Prices Paid & New Orders subcomponents were of particular note in this print. The prices paid component showed strength, bucking the recent trend of deceleration a dynamic similar to that which we saw in the most recent CPI & PPI data. Furthermore, New Orders remained roughly flat this print, suggesting unchanged (and already weak) future output prospects.

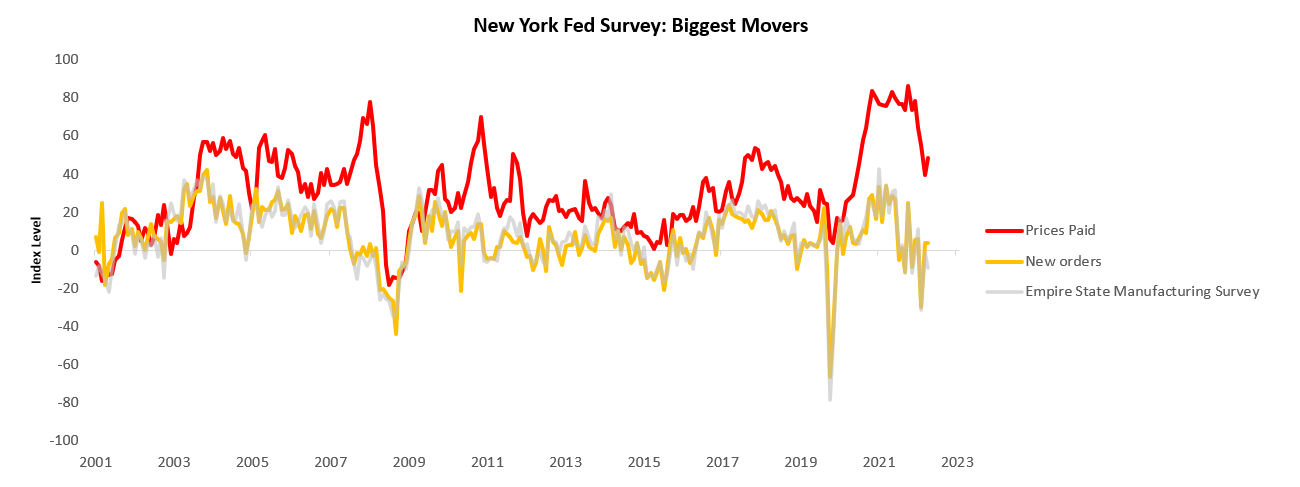

In line with these observations, our profit nowcasts suggest a period of weakness lies ahead for US corporate profitability:

As these profit pressures continue to worsen, we are likely to see further pain in production, as firms are likely to pull back production as both nominal & real profitability suffer. This brings us to the most recent Industrial Production data.

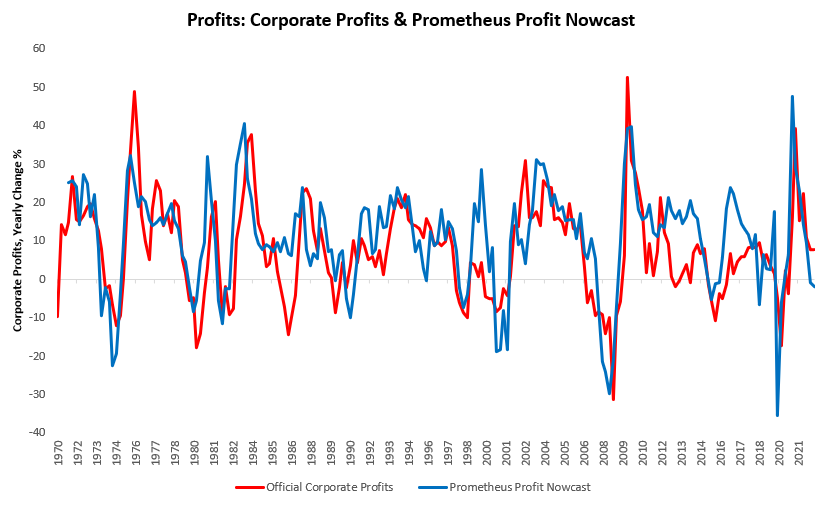

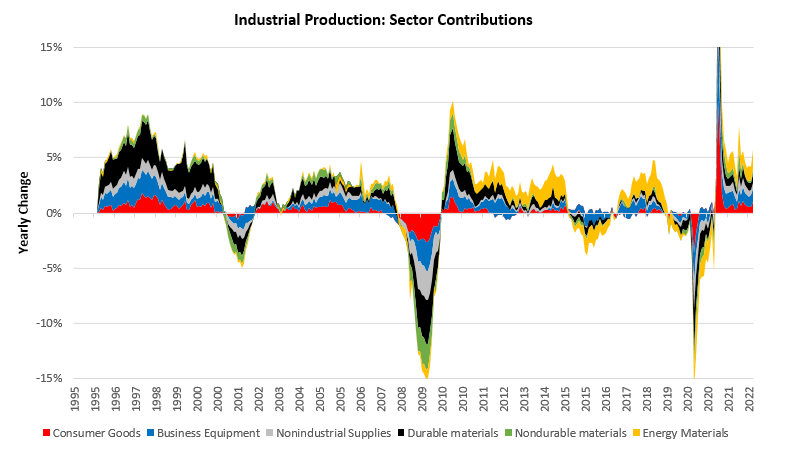

ii. Industrial Production strengthened however, a lot is going on under the surface that suggests that this strength reflects inflationary pressures. Industrial Production increased by 0.38% in September, surprising consensus expectations of 0.1%. This print contributed to a sequential deceleration in the quarterly trend relative to the yearly trend. Below, we show the monthly evolution of the data relative to its 12-monthly trend and consensus expectations:

While on the surface, this print may seem like the indication of a robust production economy, when we look under the hood, we find at the sector level, a majority of the yearly change came from 2 sectors, i.e., Energy Materials & Business Equipment:

Under the surface of these sector aggregates, we find that Energy, Food, & Autos contributed 3.32% of the 5.3% yearly change in Industrial Production, i.e., 62% of the headline growth in industrial production came from food, energy, & automobiles. We highlight these areas because they are running up on physical limitations in their ability to keep growing and therefore aren’t likely to be as conducive to production growth on a forward-looking basis. We focus on Energy and Automobiles as they capture most of these contributions.

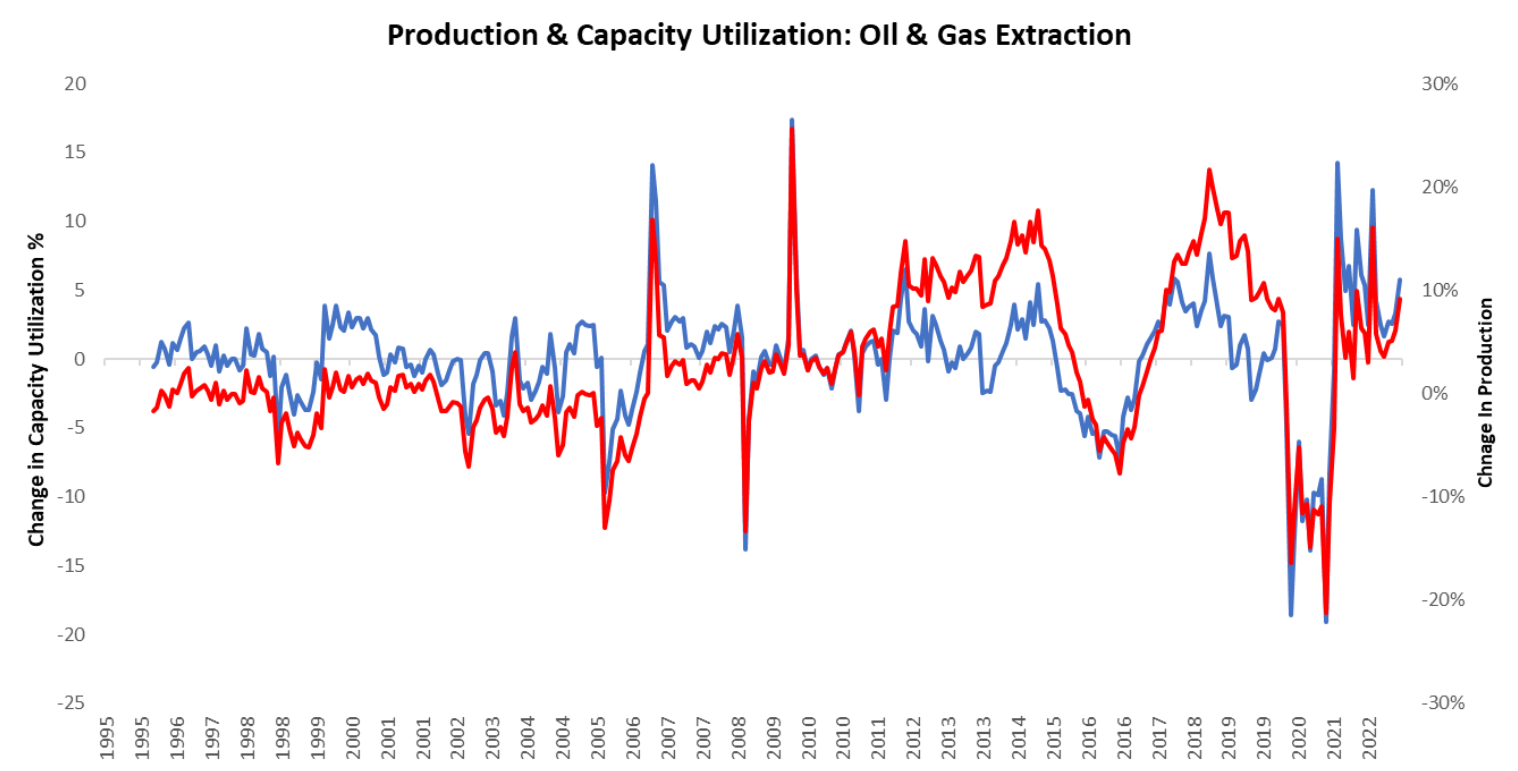

Energy production is unlikely to continue to grow at as quick a pace due to capacity limitations. Production is a function of capacity utilization and the change in existing capacity. Therefore, to increase production, one needs to either increase the amount of current capacity usage or increase overall capacity through capital expenditures. Capital expenditures don’t instantaneously result in new capacity, and often there can be a lead time of several years until capital expenditures result in increased capacity. Resultantly, most incremental production is met through the increase of capacity utilization. We show this relationship below for Oil & Gas extraction, i.e., the start of the energy supply chain:

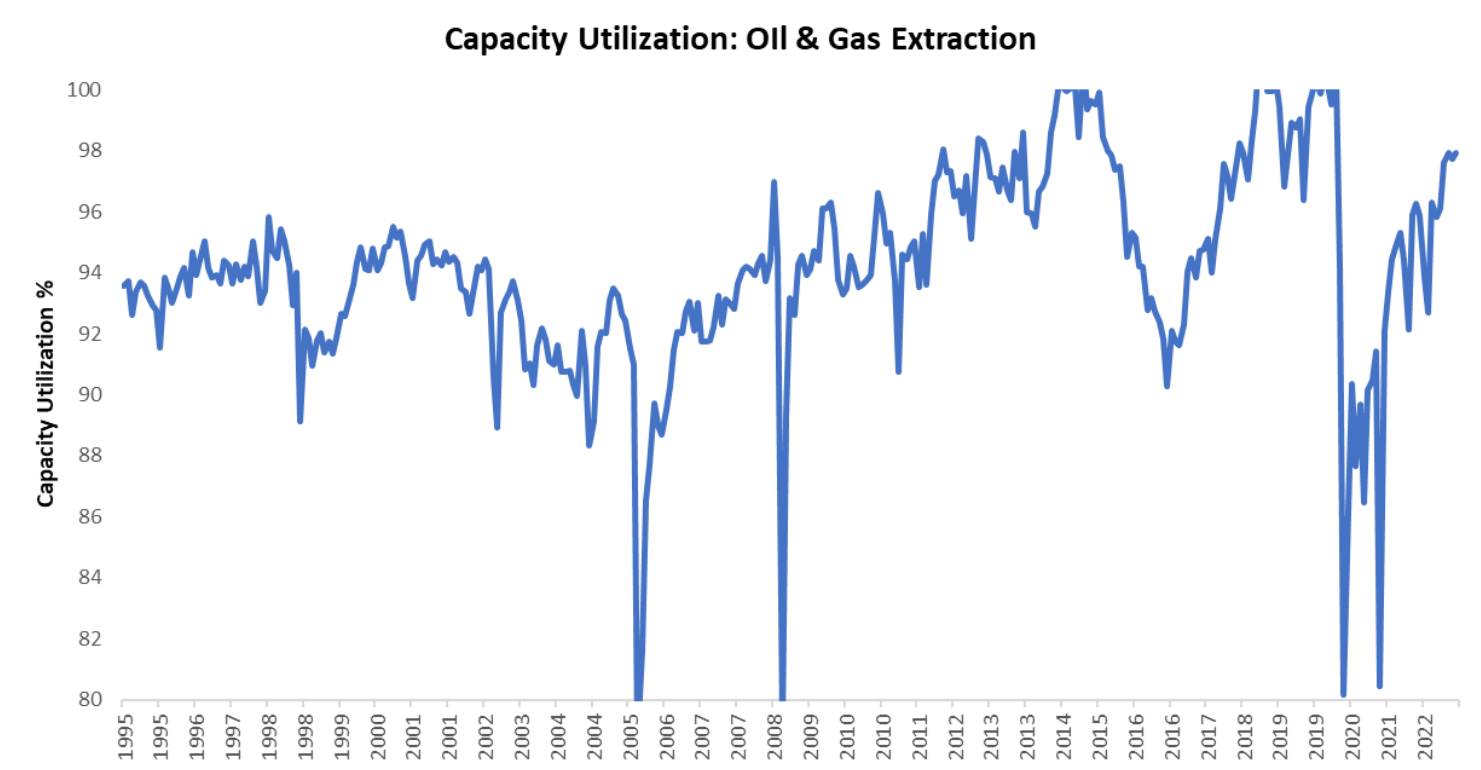

As we can see above, production is largely met through increased capacity utilization. However, today there remains very little excess capacity left to increase output:

Therefore, while capacity utilization can rise a little further, this dynamic puts a very real cap on how contributive energy production can be to aggregate production.

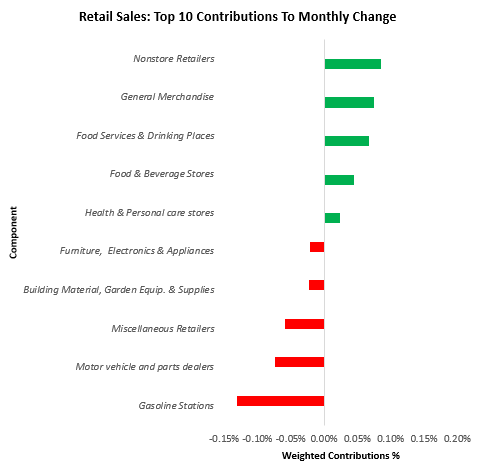

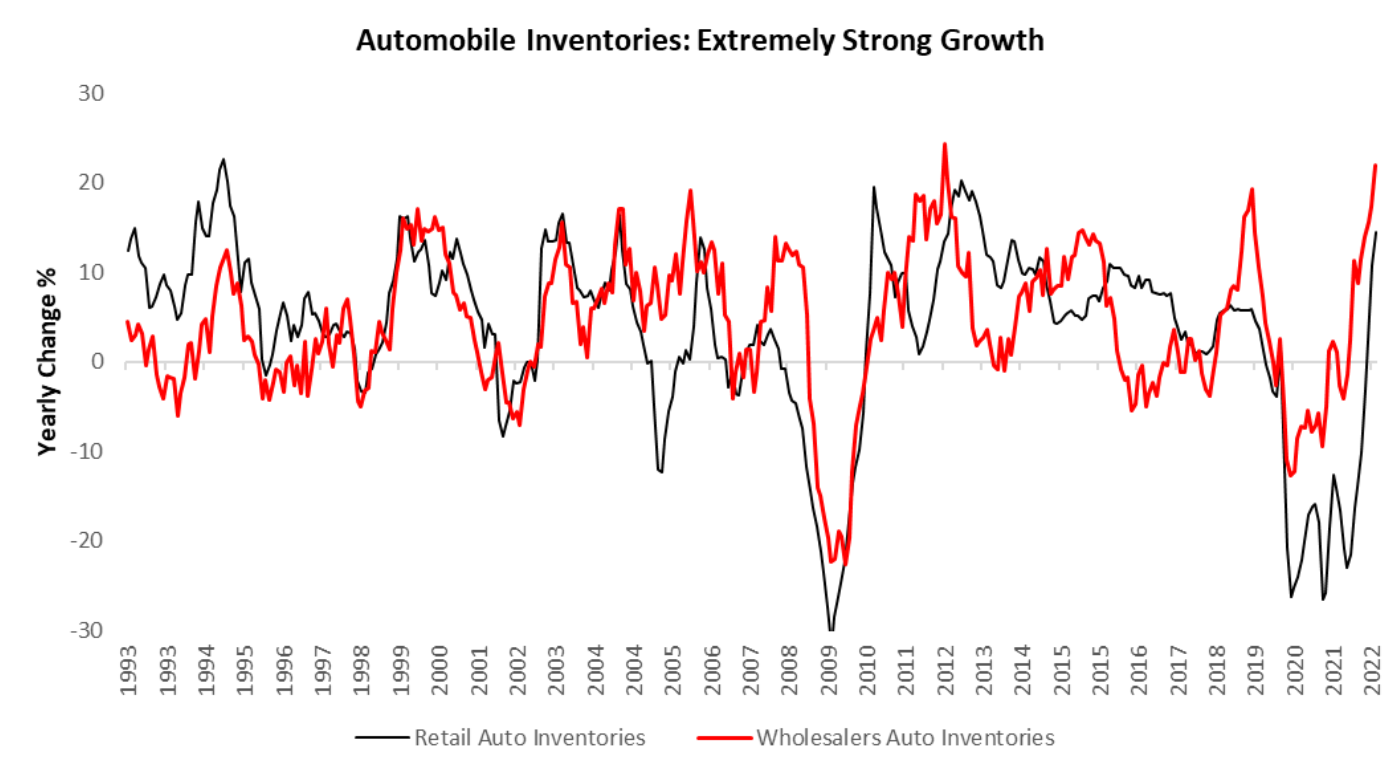

The final demand for automobiles does not justify continued production expansion. Production can find its way into only two places sales or inventories. Currently, we are seeing wholesalers and retailers purchasing automobiles but largely unable to offload them to consumers. We saw evidence of these pressures in the most recent retail sales data:

Since we are not seeing final demand for automobiles from consumers, these produced vehicles make their way into automobile inventories:

Therefore, while energy is limited by production constraints, automobile production is likely to be limited by demand constraints. In our tracking of consumer spending, we are seeing a significant breakdown in final demand for autos. This decline results in higher inventories.

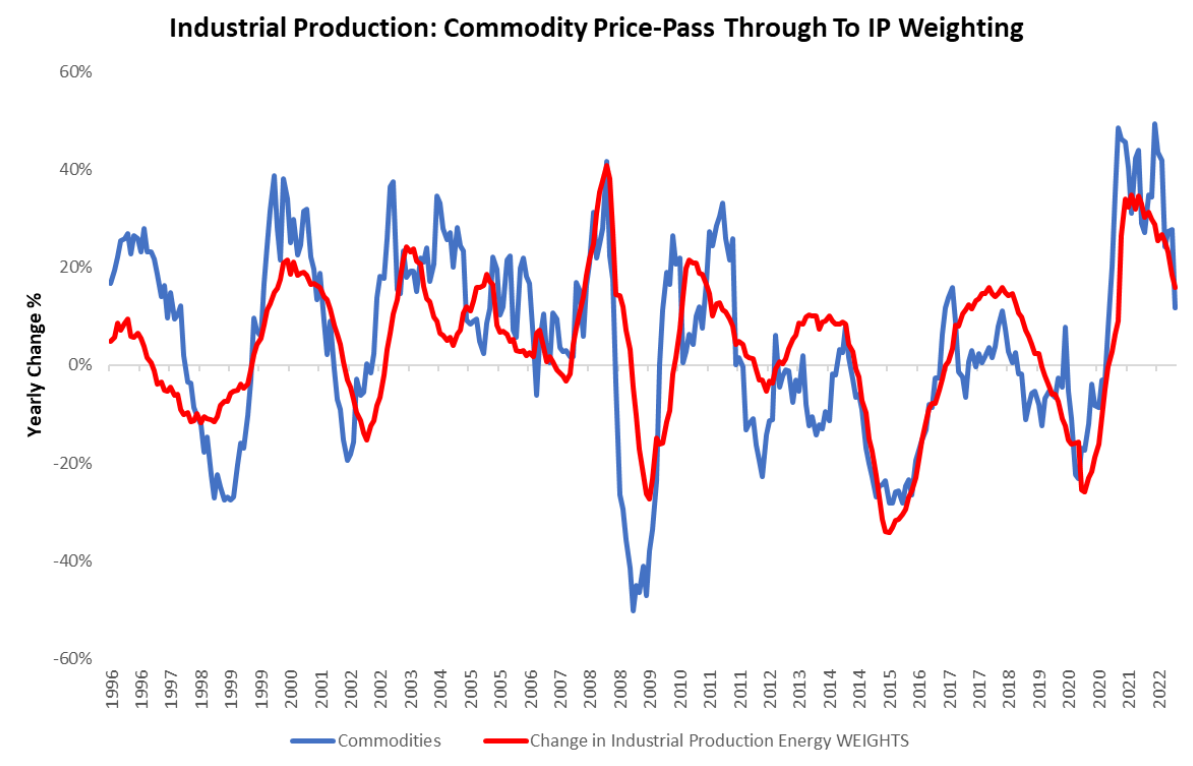

Stagflationary dynamics are distorting production data. Finally, while it is indeed intended for Industrial Production data to be “real,” i.e., un-influenced by inflation- we live in a nominal world, and nominal activity seeps into everything. Below, we show how this impacts the weighting of various indices in Industrial production using the example of energy:

The weights of subcomponents in IP take into account “unit value added OR prices” to decide the weight of components of the index. In today’s environment, in which energy prices are rapidly rising- the relative weight of energy rises in IP massively, resulting in the index reflecting some degree of nominal activity. This pass-through can be seen in the strong correlation between the weight of energy production and broad commodities indices.

Overall, our assessment of the most recent Industrial Production data leads us to believe that future conditions are unlikely to be as accommodative to higher production but are likely to remain elevated alongside high nominal growth. The combination of these outcomes will push the Fed to tighten further, creating an even more difficult environment for assets.

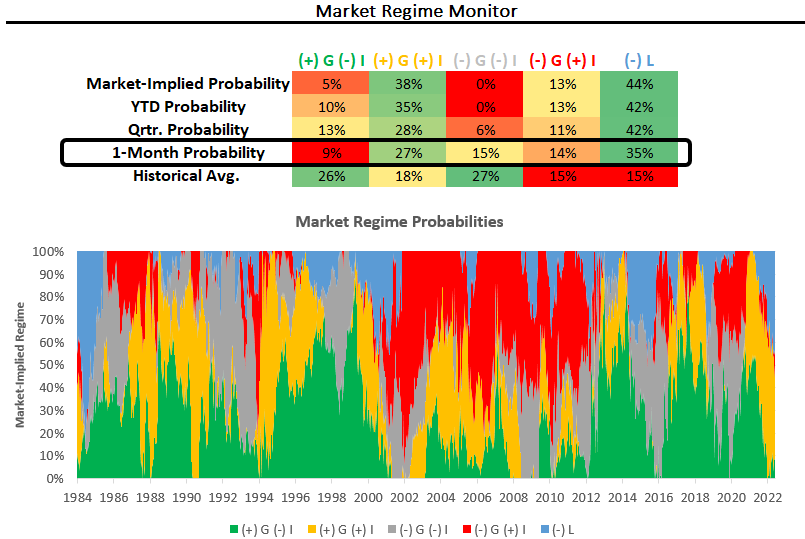

iii. Despite the recent rally, equities remain in a bear market. Our estimates for the trajectory for growth, inflation, & liquidity continue to tell us that we are in an environment unfavorable to equities. Furthermore, our market regime monitors continue to show a dominance of the market pricing of stagflationary nominal growth and tightening liquidity conditions. We show our regime monitors below:

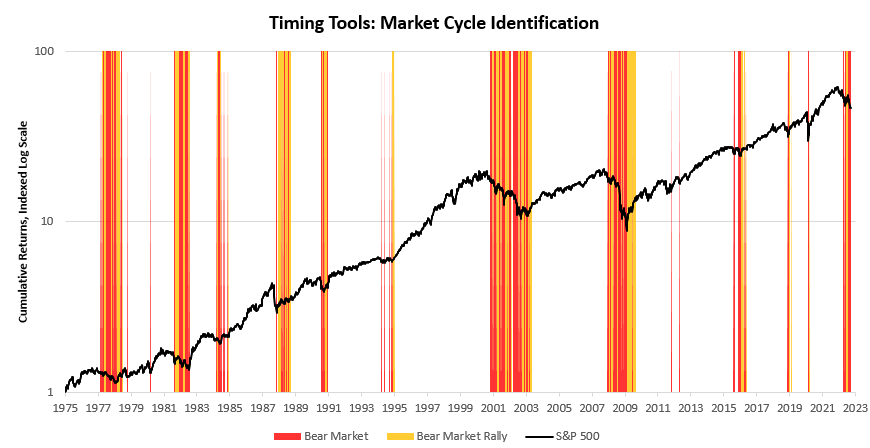

Additionally, we offer a visual from our proprietary timing tools, which allow us to classify the current environment into various stages of the market cycle. Currently, the S&P 500 remains in a bear market:

Therefore, given our systems outlook for macroeconomic factors and current market price dynamics we view this week’s price action as a potential opportunity for those willing to short assets. The ensemble of economic data we track continues to tell us we are headed to outright stagflation amidst one of the most severe liquidity withdrawals on record.

We continue to think that the hierarchy investors must abide by today is as follows:

-

Capital preservation remains of paramount importance. High cash positions are not an opportunity cost but rather opportunities for future returns being long assets.

-

True diversification across asset classes is required. The financial system is not built for continuous periods of tightening liquidityas conditions unfold, cash will once again flow to assets, the distribution of which will depend on the environment.

-

Active management remains essential for outperformance. Those with the ability to effectively short assets are likely to generate outsized returns relative to traditional benchmarks.

Stay nimble.

supplement closest to steroids

immediate effects of steroids