Welcome to our official publication of the Prometheus ETF Portfolio. The Prometheus ETF portfolio systematically combines our knowledge of macro & markets to create an active portfolio that aims to offer high risk-adjusted returns, durable performance, & low drawdowns. Given its systematic nature, we have tested the Prometheus ETF Portfolio through decades of history and have shown its durability. For those of you who are unacquainted with our systematic process, we offer a detailed explanation here.

In this publication, we will discuss the performance, positioning, & risks of the Prometheus ETF Portfolio— and it will be published every week on Fridays to help investors understand how our systematic process is navigating through markets. Before diving into our ETF Portfolio positions, we think it is essential for subscribers to understand the context within which our systems choose their exposures. Below, we offer our latest Month In Macro note, which contains the conceptual underpinnings of our systematic process within the context of the latest economic data:

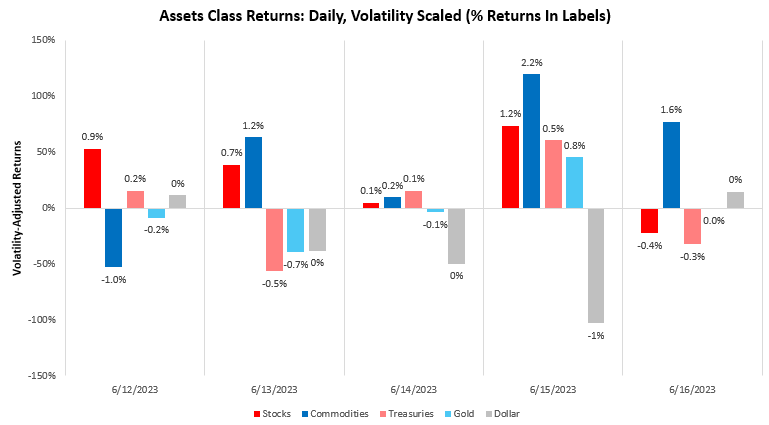

Assets markets moved to price nominal growth expectations this week, with stocks and commodities showing solid returns:

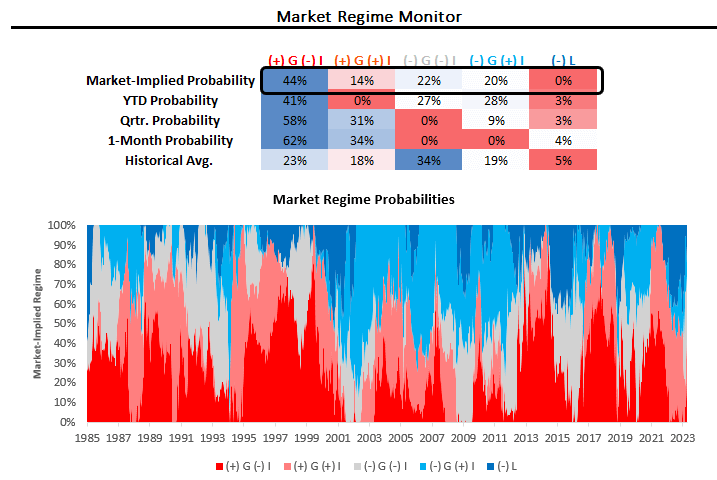

The picture is slowly becoming consistent with one of strong nominal growth pricing. We show our regime monitors below:

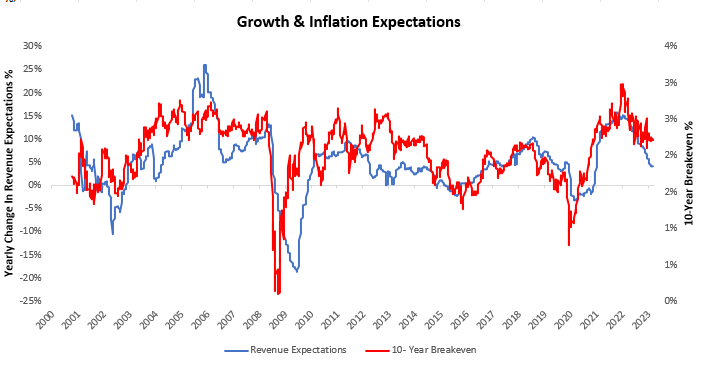

This is consistent with our tracking of revenue and inflation expectations:

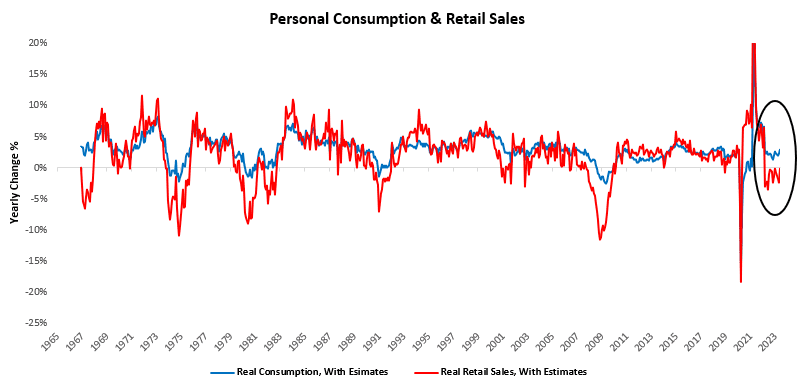

While decelerating, expectations for nominal growth remain elevated. This is somewhat consistent with the most recent data we saw from retail sales, which reduced the pressure seen on real personal consumption to contract:

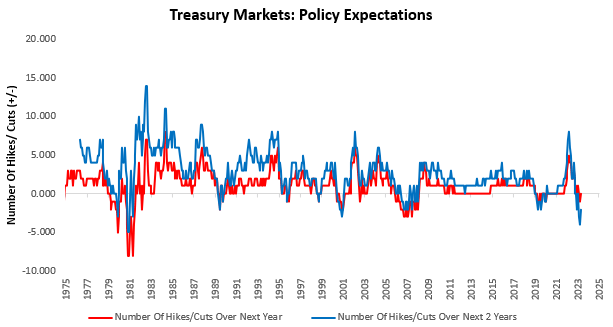

Within this context, treasury markets have moved from pricing one interest rate cut over the next year & four over the next two years to pricing no cuts over the year and two over the next two years. We find ourselves asking whether we need to price more hikes over the next year:

While our expectations remain for real GDP to contract in the future, the resilience of nominal spending coming from strong employment, income on assets, and elevated inflation is the reality in the present. We trade the markets in front of us.

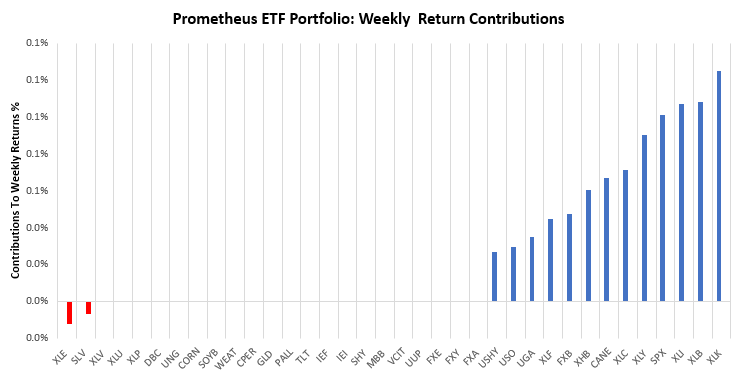

In this context, the Prometheus ETF Portfolio was up by 0.95% over the last week. Below, we show the contributions to this portfolio performance across securities:

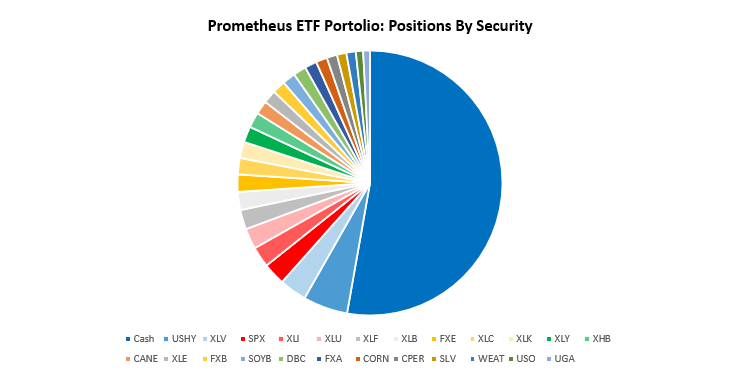

Turning to next week, our systems are looking to position the Prometheus ETF Portfolio as shown below. The portfolio contains 26 positions heading into next week. We show these below:

POSITIONS: Cash: 52.54% USHY: 5.42% XLV : 3.32% SPX : 2.71% XLI : 2.51% XLU : 2.51% XLF : 2.38% XLB : 2.2% FXE : 2.1% XLC : 1.99% XLK : 1.97% XLY : 1.93% XHB : 1.86% CANE: 1.65% XLE : 1.61% FXB : 1.59% SOYB: 1.59% DBC : 1.57% FXA : 1.47% CORN: 1.37% CPER: 1.26% SLV : 1.15% WEAT: 1.14% USO : 0.89% UGA : 0.82% PALL: -0.46% . Please note if cash position is negative it implies leverage.

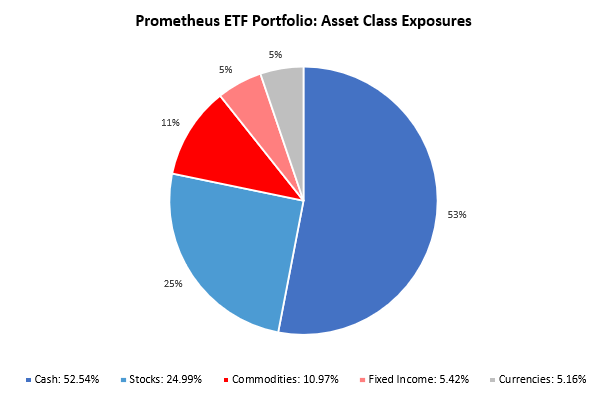

Additionally, we show these positions aggregated into asset class allocations below:

The portfolio has a net exposure (ex-cash) of 46.54%, with a gross exposure (ex-cash) of 47.46%. This allocation has an expected volatility of 4.81%, with a maximum expected volatility of 10%.

Conditions are falling in line to suggest a resilient nominal spending environment driven by persistent inflation. The next regime we are headed towards is either sustained stagflationary nominal growth or outright stagflation. So far, it looks like more of the former than the latter. Either way, active management of stock & bond portfolios will be essential. We remain well prepared.